Yves here. This post is certain to annoy some readers. Note that Kelton does not address under what circumstances it is desirable to have the government run a surplus versus a deficit, merely what the implications are. Bill MItchell is rather forceful on this matter:

The US press was awash with claims over the weekend that the US was “living beyond” its “means” and that “will not be viable for a whole lot longer”. One senior US central banker claimed that the way to resolve the sluggish growth was to increase interest rates to ensure people would save. Funny, the same person also wants fiscal policy to contract. Another fiscal contraction expansion zealot. Pity it only kills growth. Another commentator – chose, lazily – to be the mouthpiece for the conservative lobby and wrote a book review that focused on the scary and exploding public debt levels. Apparently, this public debt tells us that the US is living beyond its means. Well, when I look at the data I see around 16 per cent of available labour idle in the US and capacity utilisation rates that are still very low. That tells me that there is a lot of “means” available to be called into production to generate incomes and prosperity. A national government doesn’t really have any “means”. It needs to spend to get hold off the means (production resources). Given the idle labour and low capacity utilisation rates the government in the US is clearly not spending enough. The US is currently living well below its means. But the US government can always buy any “means” that are available for sale in US dollars and if there is insufficient demand for these resources emanating from the non-government sector then the US government can bring those idle “means” into productive use any time it chooses.

Spending equals income. Someone has to spend for incomes to exist. For incomes to grow there has to be growth in spending. There are three sources of spending growth in a macroeconomy – the external sector (if net exports are positive); the private domestic sector; and the government sector (if the budget is in deficit).

That is indisputable. Economic growth is defined in terms of production and production only occurs if there are goods and services being purchased. Firms do not produce to hold inventory. Firms may invest in response to their guesses about future sales. These guesses will be heavily influenced by current consumer actions.

So when you get commentators and high-level monetary officials arguing that growth comes from not spending you have to ask why anyone would listen to their views and why they are paid to express them. I don’t mind bloggers who do it for free saying what they like but when highly-paid and highly-visible express views that are not grounded in any economic theory that is comprehensible but nonetheless seek to influence the policy debate then I get angry.

One problem in the US is that these decisions are politicized due to a lack of consensus on national priorities and an unwillingness to admit that we need a significant change in economic policy. Even though the evidence is all around us that the economic paradigm of the last 30 years, of using rising consumer debt to substitute for rising worker wage levels, is tapped out, those at the top of the economic heap still benefit from reimplementing it even if it isn’t very successful and looks likely to end in tears very soon. As we wrote in ECONNED:

The situation we are in now echoes that of the Great Depression. Although scholars still debate its causes eighty years later, a persuasive view comes from MIT economics professor Peter Temin. Temin, in his Lessons from the Great Depression, first sets forth the prevailing explanations and explains why each falls short. He argues that the culprit was the impact of World War I on the gold standard.

Recall that starting roughly in the 1870s, major European economies increasingly adopted the gold standard, and a long period of prosperity resulted. The regime was suspended in the UK and the major European powers during the war. Afterward, they moved to restore it, sometimes at considerable cost (England, for instance, suffered a nasty downturn in the early 1920s). But the aftereffects of the war meant the Edwardian period framework was unworkable. The deflationary forces they set in motion could have been countered by countercyclical measures after the Great Crash. But that was impossible with the gold standard. Indeed, as Temin notes, “Holding the industrial economies to the goldstandard last was about the worst thing that could have been done.”

Now readers may have trouble with that comparison, particularly since the conventional wisdom is that our policy responses have been so much better than those of the early 1930s. But the key point here is that the institutional framework locked the major actors into a particular set of responses. They were not able to see other paths out because they conflicted with an architecture and a set of beliefs that had comported themselves well for a very long time. It’s hard to think outside a system you grew up with. And remember, the gold standard did not break down overnight; the process took more than a decade.

By Stephanie Kelton, Associate Professor of Economics at the University of Missouri-Kansas City, Research Scholar at The Levy Economics Institute and Director of Graduate Student Research at the Center for Full Employment and Price Stability. Cross posted from New Economics Perspectives.

Imagine two people sitting on opposite ends of a 15-foot teeter-totter. The laws of physics dictate that the seesaw will balance if the product of the first mass (w1) and its distance (d1) from the fulcrum (i.e. the balancing point) is equal to the product of the other mass (w2) and its distance (d2) from the fulcrum. Thus, the physicist can show that the teeter-totter will be in balance when the fulcrum is placed 6 feet from the end holding a 150lb person and 9 feet from the end holding a 100lb person. Moreover, the laws of physics ensure that an imbalance will arise if the mass or the relative position of one of the people is changed.

The laws of accounting allow us to demonstrate that similarly powerful concepts apply to the science of economics. Beginning with the simple identity for GDP in a closed economy, we have:

[1] Y = C + I + G, where:

Y = GDP = National Income

C = Aggregate Consumption Expenditure

I = Aggregate Investment Expenditure

G = Aggregate Government Expenditure

For economists, this is as obvious as stating that a linear foot is the sum of 12 sequential inches. It simply recognizes that the total amount of money spent buying newly produced goods and services will yield an equivalent income to the sellers of these products. Thus, it demonstrates that expenditures are a source of income.

Once earned, income can be allocated in one of three ways. At the end of the day, all income (Y) will be spent (C), saved (S) or used in payment of taxes (T):

[2] Y = C + S + T

Since they are equivalent expressions for Y, we can set equation [1] equal to equation [2], giving us:

C + I + G = C + S + T

Or, after canceling (C) from both sides and moving terms around:

[3] (S – I) = (G – T)

Equation [3] shows that there is a direct relationship between what’s happening in the private sector (S – I) and what’s happening in the public sector (G – T). But it is not the one that Pete Peterson, Erskin Bowles, or President Obama would have you believe. And I want you to understand why they are wrong.

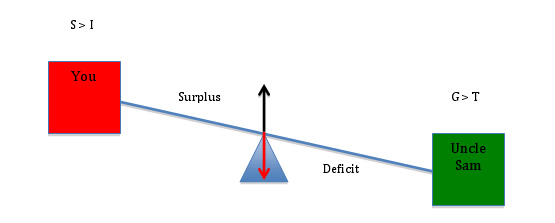

To understand the argument, imagine that you and Uncle Sam are sitting on opposite ends of a teeter-totter. You represent the private sector, and your financial status is given by (S – I). Your budget can be in balance (S = I), in deficit (S < I) or in surplus (S > I). When your financial status is positive (S > I), you are net saving. When your financial status is negative (S < I), you are net borrowing. Uncle Sam’s financial status is equal to (G – T), and, like yours, his budget may be balanced (G = T), in deficit (G > T) or in surplus (G < T). When you interact, only three outcomes are possible.

First, it is conceivable that (S = I) and (G = T) so that (S – I) = 0 and (G – T) = 0. When this condition holds, the teeter-totter will level off with each of you experiencing a balanced budget.

In the above scenario, the government is balancing its receipts (T) and expenditures (G), and you are balancing your savings and investment spending. There is no net gain/loss.

But suppose the government begins to spend more than it collects in taxes (i.e. G > T). How will Uncle Sam’s deficit affect your position on the teeter-totter? The answer is as straightforward as increasing the mass of the person on the right-hand side of the seesaw. As Uncle Sam’s financial position turns negative, your financial position turns positive.

This should make intuitive as well as mathematical sense, because when Uncle Sam runs a deficit, you receive more financial assets than you lose through taxation. Put simply, Uncle Sam’s deficit lifts you into a surplus position. Moreover, bigger deficits mean bigger surpluses for you.

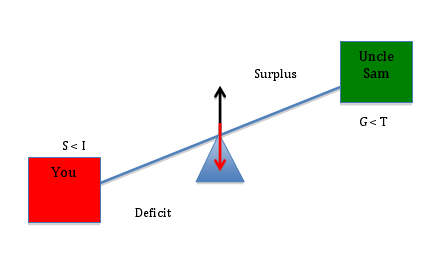

Finally, let’s see what happens when Uncle Sam tightens his belt. Suppose, for example, that we were able to duplicate the much-coveted surpluses of 1999-2001. What would (and did!) happen to the private sector’s financial position?

Because the economy’s financial flows are a closed system – every payment must come from somewhere and end up somewhere – one sector’s surplus is always the other sector’s deficit. As the government “tightens” its belt, it “lightens” its load on the teeter-totter, shifting the relative burden onto you.

This is not rocket science, but it appears to befuddle scores of educated people, including President Obama, who said, “small businesses and families are tightening their belts. Their government should, too.” This kind of rhetoric may temporarily boost his approval ratings, but the policy itself will undermine the efforts of the very families and small businesses that are trying to improve their financial positions.

* I’ll be back with a second installment that shows what happens when we ‘open’ the economy to take into account the foreign sector (and the relevant financial flows). Many of us have been working with financial balance equations for years (see here for references), so the current effort is nothing new. I am merely trying to make the arguments more accessible by changing the way they are presented.

It might be appropriate to link this article to this excellent video.

The soundtrack might be a little stilted, but stick with it. Factually it is bang on – the private sector cannot ensure full employment if the country has the capability to produce more goods than the country needs.

Debt and Deficit in a Nutshell

http://youtu.be/Ei_B5MTJofI

Does she take into account the exponential growth of interest on money ? Where do those interest payments come from ? Oh yes, they come from future borrowers taking out loans and creating money. So her little closed system requires perpetual borrowing… but what if there are no worthy borrowers and no valid reasons to make loans ? I guess we could make loans with no expectation of ever being paid back fully.

They will always be paid back fully. The idea that a fiat currency cannot pay its bills is so far off base it isn’t even wrong.

There is no need for a fiat currency issuer to borrow to fund deficits.

I wonder why we do it then. Seems like the politicians are really just debt merchants in disguise, desiring to economically enslave all within their purvue

(purview)

It’s a political constraint, not an economic constraint. Read Randy Wray’s Understanding Modern Money. A sovereign issuer like the US, the UK, or Japan is in a completely different position than a US state or a member of the eurozone.

It’s a political constraint, not an economic constraint. Yves Smith

Yes, royalty and other elites must have a risk free place to park their loot.

Isn’t it actually a legal constraint?

Our laws say that only the central bank (the Fed) can issue currency or create money – the U.S. government is not allowed to do that. The government can’t get its hands on that money except by borrowing it, an act that comes with an inconvenient obligation to repay that money in the future. That makes monetizing the government’s debts a lot more difficult and inefficient than it would be if the government itself could create new money to repay its debts. This was done to reassure fiat-currency skeptics that the money-creation power would be hard to abuse.

I don’t doubt that Obama would be befuddled if he ever bothered to try to understand this stuff, but that’s beside the point. He doesn’t care about it. He’s a corporate class war ideologue who cares about nothing but using the power of government to maximize corporate extractions.

If people think MMT education can help develop the radical consciousness, then go to it. But it needs a far greater and more aggressive normative content to accompany the descriptive. This typical timidity:

Note that Kelton does not address under what circumstances it is desirable to have the government run a surplus versus a deficit, merely what the implications are.

is part of the problem.

But let’s not pollute it with lies about the alleged befuddlement of the Leadership. They know exactly what they’re doing. They’re conscious criminals, nothing more and nothing less.

@Yves – “One problem in the US is that these decisions are politicized due to a lack of consensus on national priorities.”

@attempter – “But let’s not pollute it with lies about the alleged befuddlement of the Leadership. They know exactly what they’re doing. They’re conscious criminals, nothing more and nothing less.”

Yes, there IS a “consensus” on national prorities – at least among the “owners” – and that consensus is to do exactly what they ARE doing. Not just “conscious criminals” – more like the parasitic aliens in “Independence Day” – i.e. they will happily suck us all dry and move on to the next victims. And like them, what do they expect us to do? They expect us to die.

Excellent! So if we raise the deficit by, say, 10.000% the private sector gains wealth by 10.000%!

That means, we just have to spent more to save more!

Thats propably as close to the malthinking of the US 2002-2007 as is gets!

Excellent! So if we raise the deficit by, say, 10.000% the private sector gains wealth by 10.000%! reiter

Actually, some money creation is good. As long as the money does not lose purchasing power then no one should complain. So at least some deficit spending is NORMAL.

But borrowing government money into existence is completely unnecessary and is a gift to the rich. The Federal government should stop borrowing immediately and pay off existing debt as it comes due with new debt-free fiat.

A roughly 10% increase would be helpful, I don’t think we need to be precise down to the thousandth of a percent :)

We are all poorer as a nation as a result of thinking like yours.

The MMT folks consistently say that the constraint on government spending is inflation. Bill Mitchell points out we have a lot of economic slack, hence we don’t have an inflation constraint. In case you haven’t noticed, labor hasn’t had any bargaining power for quite some time.

Also, since 97% of the money supply is credit then would not the following be a inflation-free way to create a debt-jubilee?

1) Forbid the banks to issue any more new credit. All loans would have to be from funds designated for that purpose (CD’s,etc.) This would be massively deflationary as existing credit was paid off but no new credit was issued. So …

2) Send every American a monthly check of new debt-free fiat equal in total to the amount of credit that was paid off that month.

So, over time, the entire US population would become debt-free with no price inflation!

The ‘extra money’ seems to percolate to the wealthy causing strange types of ‘inflation’ such as commodity and equity bubbles which are ultimately as damaging to over-all economic health

Hrmm….

Cultist MMTers trying to roll the fiction out into the mainstream?

Good luck with that.

All you’ve said is you don’t like it. I see no substantive rebuttal.

And it’s your reaction that is cultish. The Catholic Church reacted the same way to Galileo saying the earth revolved around the sun, as I recall.

“There is nothing so powerful as an idea whose time has come.” Victor Hugo

Welcome to Rome 300 A.D. except we have paper – FedLOL!

“A simpler possible explanation for the debasement of coinage is that it allowed the state to spend more than it had. By decreasing the amount of silver in their coins, Rome could produce more coins and “stretch” their budget.”

Yes, inflation is a form of tax. But what of it? Governments have to collect VAST AMOUNTS IN TAX if governments are to supply what voters want them to supply. “Inflation tax” is pretty harmless as long as inflation doesn’t too far above the 2% target. If we weren’t paying “inflation tax” we’d have to pay more tax some other way for a given level of government spending.

Moreover, inflation tax is a tax on people holding on to large quantities of money for extended periods: i.e. people who cannot think of anything to do with their money. I’m all in favour of that.

I’m in favor of taxing whatever it is I think you have too much of.

Ah MMT’ers, “I print therefore I am” – Money is Debt and Debt is Money – welcome to the Matrix 2.0.

Of course, in this world everyone gets a job because the government just prints up some more pesos and hands out the shovels.

“Under this regime, government simply creates new money and spends it (and/or reduces taxes) in a recession. Conversely, when inflation looms, government reins in money via extra tax (and/or reduced public spending) and “unprints” it, or extinguishes it. As to government debt, that becomes near irrelevant: it can gradually be whittled down to near zero and be left at that level.”

How has this worked so far? Government is great at printing/spending money but they’re not so great at extracting it back out. It opens up a Pandora’s box of problems.

Yet there is some nice and tidy equation that economists always pull out: G − T = S − I or Government Budget Deficit = 666. Voilà – that explains it all

But once the genie is out of the bottle it’s hard to get it back in: while the rest of us try to put gas in our car and food on the table.

“It will purge the rottenness out of the system. High costs of living and high living will come down. People will work harder, live a more moral life. Values will be adjusted, and enterprising people will pick up the wrecks from less competent people.” liquidationists headed by Secretary of the Treasury Mellon 1930

Yet there is some nice and tidy equation that economists always pull out: G − T = S − I or Government Budget Deficit = 666. Voilà – that explains it all pezhead9000

That’s why private currencies must be allowed too.

I suppose that if Rome had found vast new gold and silver deposits then those new coins would not have been inflationary?

In fact, that is what happened when the Spanish conquered South America, price inflation in Spain.

The purpose of PM coins was not because they had intrinsic value but to make them difficult to counterfeit. That need is obsolete.

It’s a false equivalence. Sure, S-I=G-T, but the flaw here is thinking that S-I>0 is somehow better than S=I. It’s not. What we do know is that I leads to economic growth. G, in and of itself, does not. Hence what we are seeing here is the form S takes. In a balanced budget, S=I, savings is invested. In a G>T scenario, the difference has to come from somewhere, and that deficit sucks up some of S, “crowding out” (remember that?) private investment, and thus decreasing growth. When the government runs a surplus, some of T is/can be returned to the economy as I, and the economy grows.

To think that S-I>O is a “positive balance” for anyone is a severe misunderstanding; it simply means that some of S is invested in goverment bonds instead of something productive.

“…and that deficit sucks up some of S, “crowding out” (remember that?) private investment…”

Please provide empirical evidence that ‘crowding out’ occurs while high-rates of unemployment persist.

Thank you.

Actually, crowding out doesn’t exist under ANY circumstances. Money removed from reserves (by borrowing) are immediately replaced into reserves by the same loan, where they are available over and over to “fund” new loans. MMTers phrase this as “loans creating deposits”, but I find it easier to think of this as “the money’s got to go somewhere.” In other words, you not only have to look at the money coming out of reserves for the loan, but where that money ends up going. And where it ends up going is right back into reserves. Yeah, the money has a new “owner”, but it simply stays in reserves forever.

Ha! Brilliant stuff!

I think you’re right, too. When one person borrows, another tends to credit. Just ask your accountant.

I was trying to argue with some old codger, though. And to say this directly would have confused and disoriented him.

“Urrr… what’s that box in the corner — the one with the moving pictures? It’ll corrupt the youth… Oh! it will… mark me words!”

Also, deficits can be increased through tax-breaks — which, even if your ‘theories’ were correct, couldn’t ‘crowd out’ private investment.

I think you’ve accepted dogma without thinking it through properly…

“To think that S-I>O is a “positive balance” for anyone is a severe misunderstanding; it simply means that some of S is invested in goverment bonds instead of something productive.”

Governments buy their own bonds with newly issued reserves. It’s a bit like what the Fed did with QE. They issue fresh reserves and use them to buy up bonds. The reserves — as Bernanke himself said — don’t ‘come from’ anywhere; they’re just credited on a computer.

I think you need to do some reading up on how central banking works before you start spouting off undergraduate macro…

The BoE put together a video of how QE works — and it shows how reserve issuance works (i.e. the reserves are freshly issued, not taken from savings):

http://www.bankofengland.co.uk/education/inflation/qe/video.htm

Note that the robot lady says the money is ‘created electronically’. That’s the key point here.

I wish people would stop calling the MMTers ‘cultists’ and the like. Most central banks operate using the same principles that MMT advocates. Indeed, MMT is derived from studying actual central banking operations.

The original example was talking about a closed system (no external trade, etc.). Of course, when the central bank devalues the currency, there is the appearance of greater wealth initially.

There is evidence for crowding out in the current economy; businesses are hesitant to invest, at least in part because of uncertainty associated with deficit spending.

On the other hand, the examples of Japan and current U.S. indicate thate central bank purchases of government debt don’t actually help the economy either.

You know the reason undergrad texts are often called “Fundamentals of Economics” is because they talk about, you know, Fundamentals.

“There is evidence for crowding out in the current economy; businesses are hesitant to invest, at least in part because of uncertainty associated with deficit spending.”

Doubtful. They’re uncertain due to a lack of aggregate demand. Most central banks recognise this — only people on the internet think otherwise.

“On the other hand, the examples of Japan and current U.S. indicate thate central bank purchases of government debt don’t actually help the economy either.”

First of all, that’s not what I was talking about. My point was that spending was not constrained by savings. It doesn’t matter the effects of government spending are in that context. What you said was factually incorrect. Now you’re parrying that by changing the subject.

Second of all, Japan and the US use different spending policies. Japan has come to favour fiscal policy — the US are still toying around with pointless QE programs.

There is strong evidence that unemployment is being kept down in Japan due to fiscal stimulus and GDP kept up. I’m afraid you don’t know what you’re talking about (that’s obvious from the way you conflate what Japan do and what the US do).

But, more fundamentally, you were wrong about the saving and government spending thing. Regardless of what government spending does or does not do it is NOT constrained by savings. Central bankers recognise this — you don’t.

This spreading of misinformation — followed by parrying when called out on it — is infuriating. I’ve written a piece on this that should run here in the next few days. Mythmakers are stalking around comments sections all over the internet spreading their gospels of nonsense. They’re not economists, they don’t know how central banks work and yet they still think they know better than everyone else. Nothing gets my goat quite like this.

So inflation is the answer to all problems?

Your argument is that G can be greater than T if the central bank monetizes the debt, leading to an increase in S rather than a decrease in I. That is, by definition, inflation.

Japan, by the way, has had anemic growth for the last 20 years, never exceeding 3%, and usually under 2%. That policy doesn’t seem to be working well.

“Your argument is that G can be greater than T if the central bank monetizes the debt, leading to an increase in S rather than a decrease in I. That is, by definition, inflation.”

First of all — AND EVERYONE READING THIS TAKE NOTE — you have now changed the subject. What you are saying now is COMPLETELY different from what you were saying before.

No, that is not ‘by definition’ inflation. Inflation is a sustained increase in the prices of core goods as listed by the CPI. I find it shocking that you actually think you can comment on this without understanding what inflation is — but then, I don’t think you are either properly educated or rational, so it’s not so surprising.

Japan has monetised debt — the US has, in a sort of a way too (through QE). Neither of these actions have led to a sustained increase in the CPI.

I know why this is because I understand how the system works. You do not, so you won’t be able to explain this.

Philip:

You have to remember there are some that define inflation as an increase in the money supply, and also define the cause of inflation as an increase in the money supply.

Then they criticize us for not studying the fundamentals.

“You have to remember there are some that define inflation as an increase in the money supply…”

Yes, I know. And they’re just making up definitions because they can’t think properly. Even Friedman would have admitted that inflation was a sustained rise in prices — anyone who says otherwise is a hack that cannot read or think properly.

” That is, by definition, inflation.”

Where is the demand for money in this? There is a reason why MMT is a superior paradigm – it accounts for the demand for money.

And if you think the government budget constraint is a useful thought in any way, shape or form, go to these two posts:

http://traderscrucible.com/2011/03/29/solvency-and-value-insolvency-and-debasement/

http://traderscrucible.com/2011/04/29/chapter-2-in-which-the-traders-crucible-slays-the-intertemporal-government-budget-constraint-and-mr-rowe-demonstrates-his-worth/

It is fundamentally flawed and cannot be salvaged. The government budget contraint is wrong, period. Nearly 100% of the current mainstream economic thinking about the deficit is based on a fatally flawed idea.

“businesses are hesitant to invest, at least in part because of uncertainty associated with deficit spending.”

Small business owner here, and…um….no.

Investment is related to demand. Right now, customers are tightening their belts and have pulled spending way back because they are over the their heads in debt. There has been a generational change in the way people view debt that is resonating through the landscape.

Either the debt levels go down or wages go up. Either way, the only solution for small businesses is for their customers to have more discretionary cash. Debt is not cash. Credit is not cash. The US consumer has finally learned the difference.

Debt at the business and household level is completely different that government deficit spending by a currency issuer. Drawing an analogy between the two is sorely misguided. That’s why Kelton wrote her post.

Doc,

“the difference has to come from somewhere”

Your statement here implies that there is an account “somewhere” where your so-called “difference” has to come from. Where is this account? What is this account? Can you point to this account in the Fed’s Z.1? Is your account that is ‘somewhere’ a stock? Because G-T is a comparison of two flows… are you saying that the difference between two flows (measured per unit time) is a stock (measured at a moment in time)?

It’s like you are saying: “To pass another automobile safely, you have to accelerate from 55mph to 65mph, where do we get the additional 10 miles?”

Both your Units dont match up and the difference between the two measured flows at t1 and t2 doesnt “come from somewhere” ….

Check out work by Wynne Godley and many others today…

Resp,

In the example, there are no “flows”, there are G (a total amount), T (a total amount), S (a total amount) and I (a total amount)

The fundamental problem remains: what is the definition of “net private savings” other than “savings in excess of investment”. What does that mean?

“The fundamental problem remains: what is the definition of “net private savings” other than “savings in excess of investment”. What does that mean?”

That’s NOT the problem. You’re just changing the subject because you were called on your bullshit.

You claimed that government spending ‘crowds out’ private investment. Me and the other guy pointed out that this is not true because central banks issue fresh reserves to buy up government bonds — so saving does not have to be diverted into the government bonds to keep government spending (i.e. deficits) afloat.

Then you start talking about the ‘meaning’ of private saving.

Yawn.

This is typical. People are called on their BS and then they start naval-gazing and changing the subject. I propose that there’s no point in arguing with these people as they are completely dogmatic and irrational. Maybe I should start following my own advice… hmmm…

And just to point out, net private savings is the income not spent or invested by the private sector. Not exactly rocket science…

But then, I think you raised this point because you were proved to be talking nonsense on another point.

You: “Government spending soaks up private investment, thus crowding out the private sector…”

Me: “No it doesn’t — the government issues new reserves to buy up the bonds. This is what they did in QE.”

You: “Eh… look! a cat!”

Doc,

GDP for instance is a flow. G is a component of GDP so G is a flow also.

G is Government spending. In the context of this post, it has to be measured not as “a total amount” but it is always some total amount per year or per quarter or some other measure per unit time.

For instance you could say: What is the Department of Defense spending? It is $600B this year, this is a flow.

Or you could say: How much does DoD spend on a F/A-18 Hornet? One F/A-18 is $50M total, this is a stock.

So you see you have to be careful to keep your units straight when doing these types of comparisons. you cannot directly compare stocks with flows. It would be like saying you cannot travel 1000 miles because you are only going 60mph: since 60 is less than 1000 you can never get there? Of course not.

There is much scholarly work out there on this, search on “stock flow consistent macro models”, Resp,

http://bilbo.economicoutlook.net/blog/?p=4870

I suggest you check into what’s been happening in the real world before opining. The business sector in the US has been net saving since 2003, and net saving is unheard of in an expansion. The corporate sector has been net saving in all advanced economies and most developing economies ex China since the mid 2003, some since the late 1990s.

There is absolutely no risk of crowding out. We are a long long way from that happening.

I wouldn’t even go into empirics here. That gives too much leeway to people who argue this rubbish. The very idea is theoretically unjustified. If government spending is financed by reserve issuance and does not rely on taking over financial assets from the private sector, then the idea that their could be a ‘crowding out’ is nonsensical.

Central banks issue reserves to set the interest-rate by buying up government bonds. This interest-rate will not rise as long as the central banks don’t want it to rise. They just issue more reserves to ‘soak up’ the government debt.

It might have made sense in a gold standard economy — maybe. But certainly not in a fiat currency economy.

Resources on ‘crowding out’:

http://pragcap.com/the-austrians-are-intrigued

Bill Mitchell (scroll down to the ‘More Fiction’ section):

http://bilbo.economicoutlook.net/blog/?p=10959

I particularly like this quote from PC — especially if you want to keep things nice and empiric:

“This [i.e. the crowding out hypothesis] all makes sense in theory. If the government competes with the private sector for borrowings then someone must be getting “crowded out” by all of this, right? But an odd thing has happened in the last 10 years. Taxes have declined, government spending has surged and interest rates have fallen. In essence, the entire premise of the “crowding out” theory has fallen flat on its face. This isn’t the first time history has seen this occurrence. The Japanese economy has been the most notable case. The key here of course, is interest rates. There has been no “crowding out” effect whatsoever. “

“Central banks issue reserves to set the interest-rate by buying up government bonds.”

Sorry, that’s the wrong way around. That should read: “Central banks issue bonds to set the interest-rate by buying up idle reserves”.

I agree Phillip. The empirics are secondary to combatting the wrong headed assumptions head on.

Although it is great to point out that crowding out isn’t just boneheaded, its also empirically wrong.

Agreed. But it’s quite clear. These people do NOT listen to facts. Because they’re weird ideologues.

My uncle is a Jesuit (how Irish am I?) Anyway, from his adolescence he was trained in the dogma of the Catholic Church. Needless to say, he doesn’t argue rationally. Now I love my uncle and he’s a decent guy. But he has no ability to argue without the supports that were given him by the Church — because he believes it.

Ditto for economics ‘graduates’ in economics.

This has to die. Like the Church died in Ireland. These people are irrational — highly irrational — and it needs to be recognised.

Phillip,

I just posted this crazy chart at my blog. I wanted to show the strong relationship between U.S. government debt to GDP ratio and U.S. 10 year bond yields.

There is a strong relationship, but unfortunately for the ‘sky is falling’ crowd, the relationship is exactly opposite of what they claim.

You’d think 50 years of data would give them pause, but nope. They are louder than ever.

The ‘science of economics’? Surely, you jest? Economics is about as scientific as alchemy.

This teeter-totter idea totally ignores the effects of debt. Uncle Sam creates the money, you pay the interest – nearly all of it. If I borrow $100 to buy bread, or the government borrows $1 billion to buy cruise missiles, the effect is to make Uncle Sam (a nice avuncular green on the right) into a very fat uncle indeed, sitting very close to the fulcrum. ‘You’ (a nasty socialist red, note) are a long way to the left of the fulcrum – a tiny minnow by comparison. Soon, Uncle Sam will be sitting right on top of the fulcrum. When that happens, ‘you’ will discover that the consumption of bread and the consumption of cruise missiles can’t be so glibly cancelled out.

These models are always incomplete without introducing Nature “N” and Imagination “Im”.

Let’s you’re 1 million people and you live on a big desert.

You have no government, little trade, minimal income. You live in nomadic subsistence. Then someone discovers something called “oil”.

The interaction of your N-wave and someone elses’ Im-wave creates something called “Wealth” or “W”, which jumps into existence as it were from nothing, as all things really do if you really think about it. Where does a flower come from, a seed, and where does that come from, a flower, etc. etc. Eventually you reach the big bang. Which came from nothing. if you believe in the Big Bang, which I do not.

So you reach a state where you still have no real G or T. Yet money pours in from outside your borders in the form of Investment. So you do have a situation where I = C + S but only because N + Im = I.

So if I = N + Im — or really f(n, Im) = I

then Investment will always be a function of two infinite probability waves in the form of N and Im, which defy Cartesian analysis and truly any form of predictively confident mathematical modeling. This is the economic metaphorical equivalent of the Heisenberg Uncertainty Principle. You can know where Nature and Imagination are right now, but at the expense of knowing their momentum. If you know their momentum, then you lack precision as to what the immediate implications are of where they are right now (sort of anyway). If N and Im are horses and carriages, then what are the implications when technology = combustion engine? You may know the T momentum, but never precisely what the implications are for horse and carriages.

So now corporations are sitting on 1-2 trillion in cash that they won’t invest, for lack of a perceived situation where I = f(N, Im) = W > 0. I suppose the result of that analysis is always a matter of opinion, which reinforces the Im contribution to W and the uncertainty principle.

There’s more to it, but that’s enough confusion for now.

QED

well, I think one item is missed here, namely debt. as long as we can add more debt and the servicing of debt has little impact on our capacity to spend, things work well. however we did pile up on debt that the servicing is slowly the problem and sucks energy out of our capability to spend despite the vulgar manipulation of interest rates. people who continue to preach further increase of debt are despicable in my eyes because they do promote further speculation and further theft from those who lived all along within their means. the incorrect policies of the past many years cannot be corrected by simply pushing harder in the same direction instead of cleaning the system of those unpayable debts.

“however we did pile up on debt that the servicing is slowly the problem and sucks energy out of our capability to spend ”

Nope. As I point out above, the debt — that is, the government bonds — are financed by reserve issuance. Have a look at the BoE video I posted that explains how this works in relation to QE.

Japan has proved that this model is sustainable. They are running at well over 200% debt-to-GDP and their servicing costs — that is, the yields on their government bonds — remains low.

Japan has proved the model is sustainable. It is sustainable until it isn’t.

THAT is truly profound. *mutters under breath* Fucking idiot…

Dear Philip;

Get a grip man! The Japaneese are accused of coming up with Zen. What more like a Zen aphorism than Erics retort. Remember, in Zen, the content of all communication is a Void. The Big Empty Circle strikes again! Have a chuckle, it’s good for your blood pressure.

”

It is sustainable until it isn’t.

”

~~eric anderson~

I would venture even further to posit, “All categories of Ponzi are sustainable until no-longer-sustainable”.

“Those unpayable debts”??? What unpayable debts? Paying off the national debt is easy. All we need do is print money and buy back the debt, which on its own would probably be too inflationary. Solution: mix the latter inflationary method of paying off the debt with a deflationary way, i.e. raise taxes and use the money collected to pay off part of the debt. Mix the inflationary element and the deflationary element in the right proportions, and you have a debt pay back system which is neither inflationary nor deflationary. I.e. GDP remains the same, number of people employed stays the same, etc etc. For more details, see:

http://goarticles.com/article/Let-s-print-money-and-buy-back-the-national-debt/4680247/

Paying off the national debt is easy. All we need do is print money and buy back the debt, which on its own would probably be too inflationary. Solution: mix the latter inflationary method of paying off the debt with a deflationary way, Ralph Musgrave

Good thinking so far.

i.e. raise taxes and use the money collected to pay off part of the debt. Ralph Musgrave

Nope. A better way is to reduce the ability of the banks to leverage that new money. That way, the new money could compensate for the shrinkage of the money supply as existing loans were paid off. No new taxes would be required, just less (no?) new counterfeiting by the banks.

Once one realises that the banks are counterfeiters then solutions become obvious such as a bailout of the entire population and fundamental reform.

I understand your sentiments completely. It is absolutely true, that the private sector should never ‘pile on’ debt. The private sector, which prmarily serves private interests, should always live within it’s means. However a sovereign government, which has the power to issue currency( either directly or via a central bank), need never worry about the monetary amount of it’s fiscal defict, nor worry about how it intends to ‘fund the deficit’ ; it can either issue currency directly or engage in the facade of having it’s central bank purchase it’s bonds and issue currency n exchange). What constrains a sovereign government is the impact of it’s spending on inflation ( which is legitmately important becasue Inflation steals from all creditors and savers), but this can be controlled through taxation and credit policies. It is also concerned with whether the projects the governemnt funds are benefical to the nation. It is the cultivation of longterm benefits, capabilites and resources that result in prosperty for a nation, not the among of ‘money’ that it saves

Well, when I look at the data I see around 16 per cent of available labour idle in the US and capacity utilisation rates that are still very low. That tells me that there is a lot of “means” available to be called into production to generate incomes and prosperity. Yves Smith

Agreed. The solution is:

1) Abolish the government backed counterfeiting cartel, the banking system, that drove people into debt.

2) Bailout the entire population equally with new-debt free fiat.

3) Allow genuine liberty in private money creation so the economy need never suffer a money shortage again.

correction: make that “new debt-free fiat”. No more government debt!

This would require the elite to impoverish themselves voluntarily, would it not ? How likely do you think that is to happen ? We see uprising around the world right now, and people on the verge of violent opposition to their governments, as apparently the only way to real change. It’ll be no different here in the USA. Once they consume all the public pension money they’ll start into private accounts, forced buying of US Treasuries and such which will only lose value. I’m sure unemployment will continue rising, since there is just so much debt which is not economically productive. At some point you get a critical mass of unemployed and starving people, and the violence intensifies, just as we’re seeing in Greece, Spain, the mideast countries, etc. The difference in the USA of course is that our country is filled with guns and weapons of all types. Without a massive debt forgiveness, the result will be a bloodbath. Alas, poor Babylon, the mother of harlots… all the nations of the earth weeped for her at her destruction.

This would require the elite to impoverish themselves voluntarily, would it not ? R Foreman

The rich would still be rich. In fact, they would receive an equal bailout check too (Of course, it would mean relatively little to them. :) )

However, the wealth disparity would be greatly reduced.

Alas, poor Babylon, the mother of harlots… all the nations of the earth weeped for her at her destruction. R Foreman

Yep, that sounds like US. I note that LA has seven hills too and is the US’s biggest seaport.

> However, the wealth disparity would be greatly reduced.

Yeah, that’s the part I don’t think would sit too well with them, judging by the massive taxpayer funded bailouts of debtholders of the past few years.

> Yep, that sounds like US. I note that LA has seven hills too and is the US’s biggest seaport.

:)

Urban legends.. will George Washington rise from the sea with ten horns ?

Yeah, that’s the part I don’t think would sit too well with them, R Foreman

But their heads, their heads would sit more securely.

“A half a loaf and a head

beats all the loaf and dead.”

I think that the biggest issue today is that the there is no social contract between the US government and the population about economic policy. “Socialist” countries can work very well when the government is in tune with its citizens and vice versa. On the other hand, purely libertarian countries end up looking more like Somalia where there is virtually no government.

The US wants to have a libertarian philosophy while providing Socialist level services. This is a fundamental disconnect and we are seeing the results today in completely grid-locked government with polarized parties.

The recent by-election Buffalo indicates that people still want their safety nets. This has been proven over and over again over the past 30-years. It is time for our politicians to figure out how to tweak Social Security and drastically overhaul Medicare and Medicaid so that they are simply not captured by service providers or become philosophical hobby-horses.

Countries like Canada have “socialistic” policies like negotiating with drug companies. The US wants to provide single-payer health care systems that are precluded from negotiating prices with drug companies – instead leaving it up to the “free market”, whatever that is in this context. How can that possibly work?

We are also seeing it with public unions. Public unions have Eurozone structures and guarantees while the private sector does not. If we want to limit the size of government, then that will need to change. However, it would be nice if we could have a real debate and negotiation rather than the ham-handed Wisconsin debacle.

Unfortunately, I think that it will take a 1932 or 1968 level social crisis to bring everybody to the table for real discussions instead of philosophical and political posturing.

Of course government, like businesses, must tighten their belts. Afterall, as a society we somehow afford to have more people sitting idle and the GDP has doubled in the past generation. We can no longer afford to maintain the institutions of the past and must retrench.

It makes perfect sense.

The problem with Americas economy boils down to who is benefiting and who is paying the cost. As the conservative ruling power elite continue to increase their strangle hold on the power and wealth of this nation it is we the majority who pay the cost while they the conservative ruling power elite benefit, until we reverse that trend America will not have a just society or a healthy economy.

The Ruling Class is not conservative in any sense of the word conservatism that I would recognize. Both parties are profligate spenders. That’s not conservative. Neither is enriching the politically connected with tax dollars a conservative principle. It is a bad behavior of some who claim to be conservatives (and some who claim to be moderate, or “progressive”), and that’s as close as it comes to conservatism.

It is the conservative ideology of war profiteering that contributes to this mess, it is the conservative policy of bringing 20 million illegals into America to increase their profit that contributes to this mess, it is the conservative policy of socialism for the rich that contributes to this mess, it is the conservative behavior of firing millions of living wage earning Americans and taking those jobs to a communist nation that contributes to this mess, it is the conservative ideology of blind support for Israel that contributes to this mess, it is the conservative policy of undermining the unions, undermining our education system to end the teaching of evolution, undermining the rules and regulations that protect our citizens. It is mostly the conservative mindset that profit is more important then prosperity that contributes to this mess. All of the 400 richest Americans are conservative and it is these people who control our government and our wealth. I understand you middle class conservatives do not want to share the blame with the conservative ruling power elite so you deny that these folks at the top are conservative or that it is conservative ideology that is responsible for most of the ills our nation faces. Your strategy seems to be one part denial and one part the other guy did it. The church blames the hippies for their pedophilia, the banks blame home buyers for their criminallity, the conservatives (republican and democrat) use terrorism as an excuse to steal our wealth and rights then blame liberals for being to soft, stealing credit and shifting blame is the prime characteristic of conservatives. Conservatives state they stand for small less intrusive government, where is the proof of that? They state they stand for fiscal resposibility yet it is they who ran us 14 trillion in debt, they say they stand for social values yet their social policies are hateful and bigoted. Stop blaming everyone but yourselves and start taking responsibility.

Excess military spending is one of the only ways we allow deficits to be run. It’s a sad commentary.

MMT doesn’t have an answer for everything. MMT does not cure cancer or stop corruption, it doesn’t grant immortality or make poverty go away.

It just makes money work the right way. This somes some, but by no means all, of our problems.

MMT is 1/3 of the solution. The other two thirds are a universal bailout of the population and the allowance of genuine private money supplies.

1. Link missing in last para at “see here for references”

2. It would be interesting to see the same metaphor used to explain “leverage” and securitization, with a numerically tiny green block overbalancing a much larger red block….

For once, a link problem is not my fault. There’s no link in the original.

So to pay off the existing bondholders, they can just issue more bonds, ad infinitum? Japan can do it because people expect Japan will be able to pay it back – this might or might not be true. This model isn’t working out for Greece, Ireland, or Iceland. Nor in Africa. Somehow government debt can create a paradise? Create wealth?

We do have to pay for blowing up people and buildings “over there”. I guess that is “wealth creation”.

But here is also where the see-saw breaks down. The government must borrow from some one if it isn’t pulling a WZ (whisky-zulu, weimar-zimbabwe). Whatever surplus is alleged on the SI side had been transferred by the purchase of bonds to the GT side. It is the “T” term, but in another, more voluntary form, over a maybe limited time.

If the system is truly closed, then whatever units go to one side have to come from the other side.

(S-D)-I ^ G-(T+D)

The fakery is to assume D on the left is “savings”. Making “savings” bigger doesn’t create wealth.

If you do inflate, S-I stays the same in real terms. You still have the same labor, factories (whats left), services, but they are redenominated. Where S might buy a Ford Explorer today, the same numerical S buys a cup of coffee tomorrow.

S*F-I*F ^ G*F-T*F

We can reprice things in pennies instead of dollars, which would add two zeros everywhere but no one would be wealthier. And in fact we would be poorer since government would extract the wealth at the earlier, higher value, paying 100% of the original, and the value of everything would descend to 80% (you would need 125 units sometime afterward to purchase what the government did with 100 units).

We saw that in microcosm in home prices ascending well past the debt servicing ability of the group paying the price. They rose in NOMINAL terms, and it was a bubble.

If I could have bought 40 oz of gold before, and can only buy 6 now, what do you call it?

But that is why there are fiat currency laws, because people like Yves and Stephanie want to destroy and torture the poor with inflation as tax instead of even taxing the rich. If the poor demanded silver (there is a move in mexico for that) or gold, then they couldn’t be crushed by these misguided ideas. The poor need the purchasing power the most, and need interest rates to be low the most. Running huge deficits destroys purchasing power and causes interest rates to skyrocket. They both want a return to 1978-1982 and are getting it. That is their paradise gained. Bringing it back and going further would surely destroy everything. Everything her see-saw diagram says would apply back then, but what ACTUALLY happened?

Hard money is just the ticket for a deflationary economy. Don’t confuse a flight to commodity assets as a wish for a hard money standard.

I think the poor would look forward to an increase in wage rates – wait, that is wage inflation, what do we do???

Running deficits does not increase interest rates – in fact, history shows the opposite. Even during the Carter stagflation, in 1979 the budget was moving toward balance (from 2.7% deficit of GDP to 1.6%). Surprise! Federal Fund Rate moved from 14% to 18%. Oh, well, try another theory.

Continuing Yves’s “annoying some readers” theme, a little Behavioral Econ:

“Recall that starting roughly in the 1870s, major European economies increasingly adopted the gold standard, and a long period of prosperity resulted.”

Deflationary busts (1840’s,1930’s,2007-?) that last a decade or longer occur approximately every hundred years. The long recoveries in between are not due to events like adopting the gold standard, Societies as a whole are bipolar and the elevated mood phase in between busts involve increasing borrowing and spending of whatever medium is available at the time.

When the current irritable phase is over, laws will be passed to prevent more irritable phases and the cycle will start over.

Bold moves like massive government stimulus are controversial and short lived during the irritable phase and major wars often coincide with bottoming and turns back toward the elevated mood phase (Civil War,WWII).

maslof makes an important point about mass psychology — a fatal omission from rational expectations theory. Crowds aren’t rational!

I will add a technical corollary, to address this assertion from ECONNED:

‘Deflationary forces’ were not a necessary consequence of the gold standard. Rather, they derived from its inept implementation.

First the gold standard was suspended during wartime (paper money, of course, being an engine of war finance). Naturally, wartime inflation ensued. Then the gold standard (primarily at the insistence of coupon-clipping banksters) was reimposed at the prewar parity, forcing the wartime inflation to be painfully sweated out. It was this badly chosen peg — not the discipline of gold in enforcing the peg — which constituted Willie J. Bryan’s ‘crown of thorns upon the brow of labor.’

Nothing about the gold standard mandates the dogmatic 19th century obsession with maintaining an historical peg at all costs. As an illustration, if the U.S. repegged to gold today at an above-market $2,000 an ounce, the result would be inflationary, until a new stable-price equilibrium was established. The gold standard could even be implemented with a crawling peg that floats upward at a constant 2% per year, if the ‘inflation as a social lubricant’ theory holds sway (bad idea, I’d say).

Disdainfully calling the gold standard an ‘Edwardian period framework’ is a cute rhetorical device to make it sound anachronistic. But wars don’t make gold obsolete — the use of this timeless standard goes back centuries.

Since Yves Smith is listed as the sole author of ECONNED, the phrase ‘As we wrote in ECONNED …’ presumably invokes the royal ‘we,’ in keeping with the preceding monarchical imagery. This humble subject ventures to suppose that Her Majesty may be mistaken. That is, I think I disagree …

Yves, I found it a little difficult to sort out what was whose writing. Do I have it right, that the indented sections at the beginning were from Bill Mitchell, the short non-indented paragraphs above the teeter-totter part were yours, and the discussion of teeter-totters was Stephanie Kelton’s?

Some issues with Mr. Mitchell’s writing:

One senior US central banker claimed that the way to resolve the sluggish growth was to increase interest rates to ensure people would save.

Who is this banker? Please include the relevant quotation so we can see for ourselves whether this is an accurate representation of what this person said.

A national government doesn’t really have any “means”.

Really? What do you call tax receipts?

Spending equals income.

As stated, this completely ignores the roles played by saving and borrowing. “Spending by one entity generates income for another” is correct without making unsupportable claims about the relative sizes of these two flows over any given timeframe.

As for Ms. Kelton’s little discussion, my biggest problem is the way she segues from discussing what can be said about a closed economic system to discussing the U.S. economy as though those things are true of the U.S. economy. Does she hope we won’t notice, or is she somehow unaware that the U.S. economy is not a closed system?

Please read Randy Wray’s Understanding Modern Money. A sovereign currency issuer does not need to tax to spend. Its constraint in inflation, not taxes. We are at nada risk of inflation. If the US were to deficit spend, we’d drive spending to where we’d like to see it happen from an economic and national priorities perspective (well, assuming we had any….they seem to be dictated by the needs of the health industry, the banksters, and the defense industry).

Instead, with QE, we pump money into the hands of the financial system, hopin’ somehow that it stimulates the US economy. But money is fungible, we have no capital controls, so it is running overseas and into commodity speculation. Brilliant.

As to your last point, it looks like you got to the first paragraph or two of what Kelton wrote and quit reading. She clearly states at the end that her next post will be about what happens when you treat an economy as an open system.

You are falling for a fallacy. Fiat emission for spending purposes is direct debasement. Purchasing power faces a serious fall when the forces of depressionary deflation subside or are counteracted by the ongoing debasement.

Nada risk of inflation you state? In US housing and US labor rates, most likely. Food and energy is altogether different.

What you seem to be advocating is devaluation. This is a logical solution for America.

Fiat emission for spending purposes is direct debasement. Allen C

Not necessarily. The money supply consists of base money + credit. If the amount of credit shrinks then the amount of fiat can be increased to compensate with no net change in the money supply

Purchasing power faces a serious fall when the forces of depressionary deflation subside or are counteracted by the ongoing debasement. Allen C

That’s easily prevented – just reduce the ability of the banks to create new credit via leverage restrictions.

I concur with your technical response.

I might further add the reserve currency dynamic. Foreigners will continue to dump the USD as they experience real inflation. It matters little to them if US housing and US labor prices are flat.

One last comment if I may (sorry). You are fabulous BTW.

The Fed via QE is effectively monetizing (albeit with inefficiency to the benefit of the banksters) the US fiscal currently. The Fed regular buys recent US issuance on a regular basis.

I’m all for discontinuing the charade. Treasury can simply print the extra money for expenditures and save a step. The impact is largely the same, however.

Capital controls. History provides a clear picture…

Ms. Kelton should not have discussed the U.S. economy in this post about closed systems, she should have talked instead about the world economy (which IS a closed system). Or she could at least have stated at the outset that she’s aware the U.S. economy is not a closed system, but if it were one then the following would be true… The footnote at the end does not correct this problem because it still implies it is legitimate to analyze the U.S. economy as a closed system (she hasn’t committed to an opinion either way on whether the U.S. economy is an open or closed system).

I didn’t say anything about deficit spending; are you responding to someone else’s comment with your first two paragraphs? All I meant to say was a government that collects taxes has “means,” contrary to Mr. Mitchell’s strange assertion that a national government doesn’t really have any means.

You are correct that a government that monetizes its debts also has “means” even if it collects no taxes, but this is true only in a narrow legal sense – and as soon as other economic actors with any autonomy at all figure out that this is what’s going on, that currency won’t be welcome in their wallets anymore!

She started with a closed system because it is easier to understand intuitively. The addition of outside parties does make it more complex. But it doesn’t invalidate the intuition about public deficits = private savings.

In fact, foreign entities are nothing more than people who want – or do not want – to hold savings in the domestic currency. But adding this layer in the beginning makes the basic idea that much more difficult to see.

I think it was disingenuous of Ms. Kelton to argue that President Obama and “scores of educated people” are befuddled when they call for both the U.S. public sector and the U.S. private sector to tighten their belts.

In an open economy in which both the private sector and the public sector are in debt to foreigners, this kind of across-the-board belt-tightening makes a lot of sense if your goals include avoiding default and keeping the repayment of your debts more manageable.

If, as I suspect is true, much of our borrowing and spending actually creates income for others rather than for Americans, then keeping our foreign debt from increasing prevents further degradation of our future spending power while doing less harm to the U.S. economy than many think it would.

Ms. Kelton is pretty insulting to President Obama and others with her “rocket science” quip. They just don’t understand how things work (in a closed economy), she says. Well, maybe the problem is that they understand that the U.S. economy is NOT a closed economy. Maybe they are proposing we stop buying more from abroad than we can pay for out of current income, so at least we stop building up more debt. After all, that borrowing results in income for others, not for Americans.

“Maybe they are proposing we stop buying more from…”

Karen,

You shouldnt have to use the word “maybe”. If they were competent, you would know what their policy was and it would be working for all of us.

It is only unfair to pick on the Obama Admin because both political sides in economic policymaking are corrupt, depraved, morons.

We need truly new economic thinking based on the macro realities that Ms. Kelton is identifying in her post.

Resp,

Yes both major parties seem to be for smaller deficits.

Hmmm. What are the odds that they are correct?

Pretty much zero I would expect.

I’m no fan of the Obama Administration. I just think that Ms. Kelton hasn’t made her point.

She describes how a closed economy works, then ridicules people who don’t seem to understand that the U.S. economy works that way. But of course if the U.S. economy is an open economy, as it plainly is, her ridicule misses the target, doesn’t it?

There may be systematic problem with “our” brand of capitalism that cannot be corrected because doing so means to destroy what this “brand” of capitalism stands for. This is a ism of -create something from nothing- by the way of continuing growth of money supply, and the inflation it creates from this growth is actually income. This income has to be greater than the overhead cost of maintaining the financial system, and law of order. We are in an oil-age just left the stone-age short time ago. Mickey mouse mathematics of what constitutes GDP and so forth… who are you kidding? We need something complex equivalent of weather system simulation, by interconnecting over 200 computers in a network and each node trading with rest of the networked nodes for its self interest to simulate the world economy in inter-dependence.

The US is in a debt trap. Period.

Greece provides a current, reasonable example excluding one key point. There is NO backstop for the US!

This is like a Friends episode where everyone waits for Joey to catch up. Get it, America?

Greece’s government owes money in a currency it does not control. The US government owes in money it controls.

If your debts are denominated in pieces of paper that you can generate it changes the game completely. You never have to pay it back, you never have to worry about borrowing anything and you can clear it at the stroke of a pen.

However with great power comes great responsibility. you have to keep the paper under control. Fortunately you have the power to confiscate it from whoever you choose, and you can lock up anybody who tries to copy it.

It matters what things are denominated in.

Agreed! My point is the existence of the debt trap, not the resolution.

Greece is very likely to return to the drachma.

Wait till more unemployed engineers put their minds to the money problem…

Recall that starting roughly in the 1870s, major European economies increasingly adopted the gold standard, and a long period of prosperity resulted.

Really? From what I know of the history of this period, nearly the exact opposite was actually the case:

“Everybody, however, who has studied these matters, knows that the contraction of the world’s currency was the cause of the low prices of that time, and, to my mind, the present fall of prices may be chiefly and as clearly traced to those changes which took place in the world’s monetary systems in the years 1873-4. The depression seemed to be permanent, general, and universal. Simple logic demanded some cause equally permanent, equally general, and equally universal…

Valowski and the late Ernest Seyd predicted the results a priori, i.e., from the causes and even before the policy came into operation. The former, when asked in 1870 “What would be the result of demonitizing silver?” replied, “A serious disturbance will shake the universal market; an enormous fall in prices will be the necessary consequence.” The latter said “It was a great mistake to suppose that the adoption of the gold valuation by other States besides England would be beneficial. It will only lead to the destruction of the monetary equilibrium hitherto existing, and cause a fall in tho value of silver, from which England’s trade and the Indian silver valuation will sufler more than all other interests, grievous as the general decline of prosperity all over the world will be.”

from THE GOLD AND SILVER QUESTION

1893 “The Accountant”

By G. J. Murray.

It may have been a mistake, because as far as I know the mid 1870’s were smack in the middle of what is known as the Long Depression:

http://en.wikipedia.org/wiki/Long_Depression

The Long Depression was a worldwide economic crisis, felt most heavily in Europe and the United States, which had been experiencing strong economic growth fueled by the Second Industrial Revolution and the conclusion of the American Civil War. At the time, the episode was labeled the Great Depression, and held that title until the Great Depression of the 1930s. Though a period of general deflation and low growth began in 1873, (ending about 1896) , it did not have the severe “economic retrogression [and] spectacular breakdown” of the latter Great Depression.[1]

As a general response to the many commenters here who were brought up during the neoliberal takeover of university economics (and are therefore confused by MMT), no, MMT does not say you can “print” money endlessly without causing inflation. Obviously, that is nonsense, and no MMTer would claim otherwise. MMT simply specifies that inflation is regulated far more via taxation than is commonly thought, and far less via spending. In other words, if you have inflation, you might equally look to tax policy as to spending policy to find its source.

Now that should not be all that dissimilar to what you know via the neoliberal schools. The difference is that MMT does not tie spending vs taxes together as an identity (i.e., the Quantity Theory of Money), with inflation as the direct result of the former exceeding the latter.

In fact, it is trivial to demonstrate instances where the Quantity Theory is not true, and in BOTH directions. It’s easy BOTH to produce inflation where the Quantity Theory says it shouldn’t exist, and to not produce inflation where the Quantity Theory says it should. All that MMT does (in this instance, at least) is explain in theory why in practice the empirical results are what they are, and not what the Quantity Theory says they should be.

The Quantity Theory of Money is simply wrong, as is the 30 years of paid economic quackery expended to defend it, and taught to you to justify those expenses. Sorry if you went to school during that time. Perhaps you could ask for your money back. I’m certain that’s what Austrians would say you should do.

You mean MV = PY is dead?

It was never alive.

Just taking off the italics.

I’ve seen this argument before in other blog posts here. This version seemed a bit clearer, perhaps because it was very simplified.

My biggest question is not what happens when current account balances are added, but how money creation by government and banks is accounted for. The argument seems to rely on a closed, zero-sum system, so what if we add a “money created” term on either side?

(If there is one thing I’ve learned from following all this in recent years, it’s that “money” is far from a simple concept).

The savings of the corporate sector in the US and EU is likely balanced out by the funding of its investments in China and India, based on anecdotal evidence from my employer.

I await Kelton’s discussion of an open system with great interest.

I came so very late to a really fine discussion. I dislike the the teeter-totter analogy because the private and public sectors are qualitatively different. Both can create money out of thin air, the private sector in making loans, the government sector by increasing the money supply, but ultimately private side money creation has to be backed up by the government creating money to cover the private side activity. So there is a fundamental asymmetry at the heart of the model.

When I look at the economy, I look at it in terms of wealth inequality, kleptocracy, of the paper economy vs. the real economy. I ask myself where does all this fit into such a model, or rather how good is a model that does not address these issues. When I see discussions like this, I go further, and ask what is the nature of money, what does scarcity really mean, what is the relationship of resources, physical and intellectual, to the structure of our economic system and the mediating function of money in creating artificial scarcities. These are the questions and issues that preoccupy me. I see nothing in those cute graphics or the identities they purport to show that has any relevance to any of my concerns.

Yves, Yves. This is not an argument or article I would expect from you.

This reeks of sophistry.

You cannot get something from nothing, nor continually refinance growing deficits. I have spent many years in finance to know this is true. It does not matter whether you are an individual, corporation, or a nation-state.

The bond market we eventually bring discipline to this overspending madness. The longer the bond market takes, the worst the pain will be when the day of reckoning comes.

The bond market we eventually bring discipline to this overspending madness. The longer the bond market takes, the worst the pain will be when the day of reckoning comes. MrMoney

LOL! The US government has no need to and should not borrow in the first place so who should care about the bond vigilantes? Not US.

Yes, governments have dangerous money creation powers but the solution is not to issue government money as debt. The solution is to allow the private sector to create and use its own private monies so as to be able to escape government money mismanagement.

attempt to kill italics

FBeard,

You should check out my post about how the Government Budget constraints are wrong.

“Solvency cannot be and is never an issue, so the yield of a government bond in its own currency is divorced from solvency. There isn’t a link because the government cannot be insolvent. This idea about government bond yields and government solvency is true even when most people don’t believe it is true. For example, it is true right now, today. “

“You cannot get something from nothing, nor continually refinance growing deficits. I have spent many years in finance to know this is true.”

Ha ha! You’re kidding right?

The longer I work in finance, the more I get for “nothing.”

Good one Mr. Money ;)

Yves, your equations fit precisely the economic model.

However, the real world has several BIG features that cannot be accurately measured, hence cannot be readily modeled:

The underground economy which is not measured because by nature its illegal.

Imputed costs for goods and services for which there are no transaction costs – owning a home, a farm, or a labor swap co-operative.

These sectors are substantial portions of our economy, and until your econometric models represent reality, they remain models with limited utility.

Ms Kelton, there’s a say in Yale: Generalization is the sin of knowledge. When you talk about things like Public expenditure (G in the “simplyfied model) you are putting under the same label things as diverse as : bombs thrown in Irak or Afganistan, food stamps, salaries paid to unemployed , money expent in building roads or bridges without any consideration of the efectiviness of that expenditure. Let’s explain it.

Imagine that you pay for a bridge 100M. You have contracted people bought cement and iron and you truly beleive that thats GDP. Suddenly, someone comes and shows you the same bridge two miles down the river built at 50M. Would you still argue that the state has crreated value or simple has REDISTRIBUTED wealth from some people to other.

Isn’t it curious that some people talks so liberally generally about public expenditures without a single consideration of efficiency? Well, the truth is that public infrastructures, wars or food stamps cost between double and five times if publicly expent.

Isn’t it curious that some people talks so liberally generally about public expenditures without a single consideration of efficiency? Ivan The terrible

Efficiency is not the point. The point is to get money into the economy to counter the over-indebtedness of the population.

So let’s forget government spending and:

1) Abolish the government enforced counterfeiting cartel, the banking system, which is the cause of the over-indebtedness.

2) Pass out debt-free money equally to the entire population to enable borrowers to pay down their debt and to compensate savers for years of artificially suppressed interest rates.

Then there would be no need for inefficient government spending.

If the US government can issue an infinite amount of fiat money without negative consequences why does anyone work in this country? Instead of filing an income tax return every year we should change the system so we file an income request each year. I simply tell the government how much money I want them to print for me and then ‘they’ send me a check. I then use this money to buy what I want from China, India or Brazil where the people are all so foolish they still believe they need to work and produce stuff the rest of the world wants to buy.

These type discussions always remind me of a blindfolded men describing an elephant. Depending on what part of the elepahnt they are currently touching the description varies wildly. The only difference is that presumably people trying to describe an elephant don’t have an agenda!