Yves here. Quelle surprise! Most bank customers do not like the idea of negative interest rates. And most would do the rational thing in deflation, which is to hoard cash or squirrel their funds into other investments.

By Mark Cliffe, Chief Economist, ING Group. Originally published at VoxEU

As doubts grow about the effectiveness of quantitative easing, monetary policymakers are leaning towards cutting interest rates further into negative territory as their preferred mode of easing. But this begs crucial and untested questions of whether banks will be willing to pass on the cost to their retail depositors, and of how depositors might react if they did so. This column notes a recently published survey in which a large majority of respondents said that they would withdraw their savings, and yet few would spend more. Although it could be argued that savers might react less negatively when confronted with the reality of negative rates, their powerful aversion to the prospect raises troubling questions about the potential effectiveness of this policy tool.

In their struggle to keep up the momentum of economic growth, central banks are turning to negative interest rate policy (NIRP) as their weapon of choice. Amid doubts about the impact of further large-scale asset purchases, the Bank of Japan (BOJ) has recently followed the ECB and other European counterparts in imposing negative rates on the reserves that banks hold with them. Meanwhile, weak economic data has even prompted talk of the Federal Reserve potentially having to reverse course and join the NIRP club.

But there are doubts about NIRP too. In particular, if banks resist passing on negative rates for fear of triggering a deposit flight, they will fail to incentivise savers to spend. NIRP could still work via boosting asset prices or driving down the exchange rate, but, as the BOJ has discovered, this is a confidence trick that is liable to succumb to the vagaries of financial market sentiment.

So are the banks right to fear the zero lower bound (ZLB)? The obvious problem is that we have no experience to go on, since no bank has been brave enough to breach it in a significant way. The banks are clearly concerned that cutting savings rates below zero would lead to a customer backlash and significant withdrawals of deposits. But with loan rates often contractually linked to money market rates, shielding savers from lower rates comes at the cost of bank profitability, capital generation, and willingness to lend. This, in turn, blunts the intended stimulus that the central banks are trying to deliver by lowering rates.

So the response of retail customers to negative interest rates remains largely untested. In an attempt to fill this gap, ING commissioned IPSOS to survey around 13,000 consumers across Europe and – for comparison purposes – in the US and Australia to ask them how they have responded to low interest rates and how they might react to negative interest rates (ING 2016).

Such surveys have an obvious drawback: there is inevitably a gap between what people say and what they do – inertia often kicks in. Nevertheless, the results are remarkable. They indicate that zero is a major psychological barrier for savers. No less than 77% said that they would take their money out of their savings accounts if rates went negative. But only 12% would spend more, with most suggesting that they would either switch into riskier investments or hoard cash ‘in a safe place’.

Survey Highlights

1) Response so far to low savings rates

In order to provide a context for the consumer reaction to the possibility that savings deposit rates might go negative, the survey began by asking respondents about how they have responded so far to low interest rates.

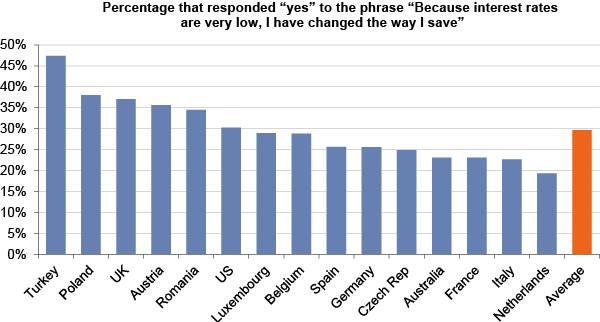

Figure 1. Nearly a third of savers have changed their behaviour due to low rates

Source: ING International Survey (IIS)

It asked whether the low rates had prompted a change in their behaviour and, if so, how. Across the 15 countries surveyed, 31% of respondents said that they had changed their savings behaviour (see Figure 1). The figures were higher in Eastern Europe, the UK (37%) and Turkey (47%), where rates have traditionally been higher or more volatile.

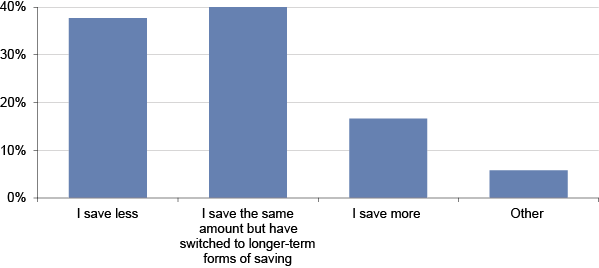

As to how savers had changed their behaviour in the light of low interest rates, the most popular answer, accounting for 40%, was that they were saving the same amount, but had switched to longer-term forms of saving (see Figure 2). Across countries, the highest proportion of respondents to have made this switch was in the UK, with 49%, and the lowest was in Austria, with 28%.

Figure 2. How have you changed the way you save?

Source: ING International Survey

The next most popular response, at 38%, was from those who have been saving less – the response most desired by the central banks. That said, ‘saving less’ does not necessarily translate fully into ‘spending more’, particularly for those households relying on interest income.

Meanwhile, the survey showed that a significant minority – namely 17% – of those who have changed their behaviour have actually increased their saving in response to lower rates. This may reflect the fact that the lower income resulting from lower rates may be making life harder for those who have target income or long-term savings goals, forcing them to save more to compensate.

Interestingly, US savers came out top on this account, with 26% of ‘changers’ having increased their savings, as many as those who had cut their savings. Lacklustre income growth may be partly to blame here. By contrast, only 5% of the Dutch had increased their savings.

Response to a Possible Move to Negative Savings Rates

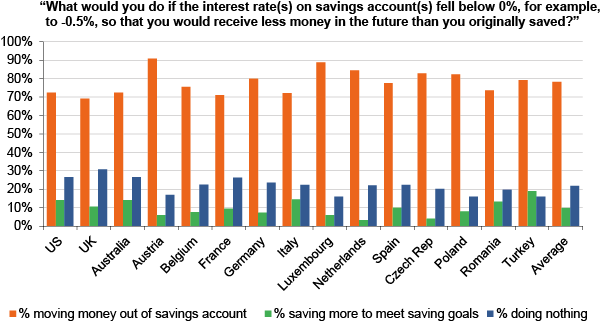

The survey then asked how they might react if rates went negative. Although there is room to doubt if all respondents might actually react as they say if this became a reality, the strength of feeling revealed by the survey is striking. Only 23% of the total sample said that they would do nothing in response (see Figure 3). This compares with 69% of the sample who said that they have not changed the way that they save in response to low interest rates so far. The survey suggests that crossing the zero bound is a major psychological shock to consumers.

The negative reaction to the possibility of negative interest rates is an interesting application of the behavioural economics concept of ‘loss regret’. Feelings evoked by seeing interest rates cut from, say, zero to -0.5% are stronger than those from 1% to 0.5%. The difference is that the former is perceived as an outright loss, while the latter merely as a smaller gain.

There are also political and cultural dimension. Many will see negative rates as an unfair ‘tax’ on small savers, particularly in cultures that celebrate saving as a virtue. In this respect, a significant minority of 11% would save more (Figure 3)

Figure 3. Nearly 80% of savers would respond to negative interest rates

Notes: Weighted by country, age, gender and region, significance tested on 95% level. As respondents were allowed to choose more than one answer, the country total may exceed 100%.

Source: ING International Survey

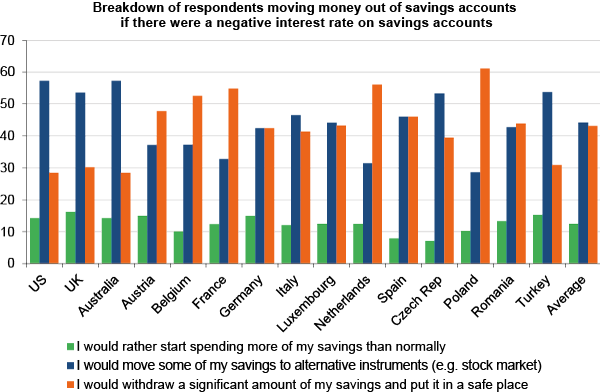

Figure 4 shows only those who plan to move at least some of their money out of savings accounts (some 78% of the respondents). Some 10% would spend more, almost exactly matching the proportion of those who intend to save more. The remainder are almost evenly split between those who would switch into alternative assets or simply put their savings ‘in a safe place’.

In other words, around 40% who would respond to negative rates (or 33% of the total sample) said that they would hoard cash. In the Netherlands, France and Belgium, this proportion rises to more than 50%.

Figure 4. Switching into investments and hoarding cash are the most popular options

Note: As respondents were allowed to choose more than one answer, the country total may exceed 100%

Source: ING International Survey

Assessment

This survey makes sobering reading for both banks and central banks. For the banks, the results suggest that they might be right to be reluctant to cut rates below zero. Only 23% of savers would not react, and a smaller proportion still would save more. Four-fifths would move at least some of their money out of their savings accounts. Some of this might find its way into other bank products, but more than a third say that they would take some of their money out and hoard it.

The strength of the responses perhaps reflects the immediate shock of being confronted with the unprecedented possibility of incurring a charge to keep savings in bank accounts. Provided rates went only mildly negative, say no more than -0.5%, or the cuts were perceived as temporary, then the reaction might, in practice, be milder than the survey suggests.

Banks would be faced with an uncomfortable choice between not cutting retail rates below zero, and so seeing their profit margins squeezed, and doing so and risking a substantial deposit outflow.1 They might perhaps mitigate a profit squeeze by raising fees, or increasing the cost of mortgages, as some banks in Switzerland have done. However, these would undoubtedly also meet with customer resistance and official consternation.

Moreover, even if the banks dare to pass on negative rates to retail savers, the stimulus to spending would be far less than the rate cuts so far. Indeed, in the total sample, marginally more (11% versus 10%) of respondents said that they would save more, not less, in the event of negative rates.

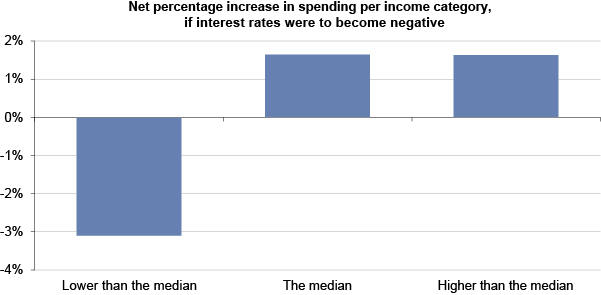

Figure 5. Reaction to negative rates also depends on income

Source: ING International Survey

One important caveat to this is suggested by the disaggregated results of the survey. These show that richer, older, and more educated respondents would be more inclined to spend than other respondents in the event of negative rates (Figure 5). Since these groups tend to have higher savings levels, more spending by them would more than likely offset lesser spending by the poorer, younger, and less educated groups, giving a greater stimulus to spending.

Nevertheless, the results strongly suggest that the cuts in interest rates below zero are likely to give a smaller boost to consumer spending than cuts in rates above it. Moreover, they also highlight the unpredictability of pursuing NIRP. With the credit channel weak or blocked, central banks have been relying largely on rising asset values and weaker exchange rates to provide the needed stimulus. But the BOJ’s recent adoption of NIRP has had the opposite effect. Evidently, the initial market reaction has been to see it as an act of desperation. The risk is that this negative sentiment will infect the real economy, serving to depress spending. If so, the danger is that NIRP will have an impact on economic growth that is not merely non-linear, but perversely negative.

Endnote

[1] Banks in Belgium will not have this choice. The Ministry of Finance decided last year that interest rates on regulated savings cannot fall below 0% (the minimum is 0.01% base rate + 0.10% fidelity premium for money staying at least a year on a savings deposit).

See original post for references

You know I could have sworn there were other ways for governments to stimulate growth. Tested, very effective ways… Oh well, I guess not. After all if the super-genius rulers of the universe can’t think of anything to try besides just lowering interest rates, possibly below zero I must be wrong.

You know, if these clowns were in Indiana Jones’ place they would probably have tried fighting that expert swordsman with their bare hands.

When all you have is a hammer……..

…it makes for a very rough process when you’re trying to screw something.

We used to have this thing called government that was supposed to address problems. These days all it seem to do is create them and then tell the bunch of us to figure it out. Meanwhile they’re collecting 6 figure incomes for thanking the Capitol hill police, naming park benches and either doing nothing or screwing crap up. I sure wish I could fail upward.

You need a degree from Harvaaaard to do that.

It would be hilarious, if it weren’t so pathetic, that Americans actually pay for these d-bags to lie to them…does that make any sense to you – paying someone to lie to you? Doesn’t make any sense to me…

It’s quite the quandary- The banks need people to spend money but the government fear mongering on retirement actually discourages it. As it stands the government has been telling Americans they haven’t been saving enough to cover the gap at retirement between what they’ll need and what they have presently. It also doesn’t help that most Americans know the government is salivating and looking for opportunities to expand their Social Security slush fund by raising the retirement age and or cutting benefits. Then there’s our health care system which is shifting to higher deductibles. What do they want people to do? If they spend that money they’re going to get scolded for not saving for that deductible. So people are squirreling away for that. Additionally a lot of the economy is tied up in future spending- 529s, HSAs, 401ks, etc, etc- a lot of our economy seems to be slated for future spending rather than stimulation for the present economy. At the end of the day if you are spending 30% on housing, 20% for retirement, another 20% on your health care premium plus deductible, that leaves you 30% and you haven’t even covered utilities, transportation, food and in the case of many of our young people educational loans. What exactly are they expecting people to spend?

Mind you I’m not an economist but it seems that they might want to get together with the government and actually discuss how to give households more discretionary income if they want people to spend whether it be by addressing our very expensive health care system, the housing problem that has people spending in excess of 30% in many localities, figuring out how to shore up the retirement system instead of fear mongering with this idea that the government is going to go bankrupt providing a modicum of security for the elderly, or even doing something about the fact that our education system has a bunch of money tied up which prevents young people from being able to set up households and spend money on anything other than student loan payments. If you solve micro- then you might be able to fix macro.

Speaking of micro, fresno dan posted this at the Water Cooler yesterday:

http://www.epi.org/publication/charting-wage-stagnation/

Obviously, you need more assets that you can turn into cash money!!!

Fortunately, you are full of them – hearts, lungs, kidneys, livers – do you REALLY need BOTH your eyes? As well as the fact, you have all this meat on your bones….as well as your bones – just reverse mortgage your body to the Soylent Green corp and you’ll be rolling in money!!! *** As they say at Davos, Win-Win!

***as there are people who don’t recognize parody, apologies to Johnathan Swift…

I am one of those people who does not recognize parody. Before I got to your last sentence I was about to remind you that eyes are not currently transplantable so an eyeball is not a transferrable asset.

Corneas, though.

neel kashkari, the new eu ministry for all things fiscal, the gang of 20 promoting fiscal over monetary; and janet pleading with congress to go fiscal… and nirp: NIRP is good idea if it promotes government fiscal spending because the money the government “borrows” from itself actually earns some tip money and the borrowing and spending could go to create and subsidize an entire complex of new environmental industries with jobs, remember jobs? We need govt spending. We need to control capricious, useless debt creation. We need to clean up the planet. We need jobs before the whole system implodes, as in yesterday. And we need to take the hot air out of the sails of the debt and balanced budget hysterics. So if people won’t spend (bec we are all angry and tapped out and jobless, etc.) we have an excellent solution that is facilitated by NIRP, tried and true-good old gov’t spending, it could solve all our problems and earn some on the side.

PLain and simple . Last way to rob the pensions and 401k’s . Sap the last vestige of freedom , These people at the Global Feds are a den of thieves .Remember Fed only exists to take care of the big banks . Wealth destruction for us , riches for them . ZIRP will cause a worldwide depression . Get ready . Worst nightmare come true.

“Although much maligned, negative interest rates are the first real attempt to fix the problem of unproductive savings. Negative interest rates really are a tax on unproductive saving. There is no reason they shouldn’t work.

Look at Japan, the Japanese state can now earn interest ‘revenue’ by borrowing money to finance stimulus. This is a great result. Up until now a Japanese bond holder has been sitting pretty earning a real yield in a deflationary economy as a reward for maintaining a depressed economy. Now they are being asked to periodically transfer wealth to the state who will actually spend it. Banks and bondholders hate it which strongly suggests it is the solution we have all been searching for.” – H/T sweeper

Whilst I’m not wonky enough to know the validity of such in a granular sense [so many moving parts], back of the envelope does suggest a sort of pressure similar to what FDR did wrt private hoards of gold. That still leaves the issue of targeted spending in the form of fiscal expenditure and additional measures e.g. the Citi data London link I gave – http://www.nakedcapitalism.com/2016/02/links-22616.html#comment-2555153

Skippy… would be interesting to see others comments.

Skippy;

What I foresee is a negative feedback loop. NIRP drains money out of the pockets of ‘savers.’ The Government feeds this newfound money back into the Financial Economy, (as separate from the “real” economy.) Little to no ‘actual’ expansionary economic activity occurs. The Financial Managers skim some of this ‘churn’ into their own pockets. Said FMs spread some of this money to their cronies. The ‘savers’ receive less of a ‘return’ on their involuntary investment than they have contributed. Wealth is concentrated “upwards.” Most importantly, faith in the existing financial order declines more rapidly over time. Politically speaking, said loss of faith would be a positive result. Eventually, when the Public removes its’ consent to be victimized by the FM class, either a formally two tier system will emerge, or the FM class will be ‘chastised.’ Such a ‘removal of consent’ can be passive in nature. An active ‘removal of consent’ would be viewed by the FM class as revolutionary, and rightly so. The problem with this outcome is that such ‘movements’ require leadership to succeed. That future ‘leadership’ is the problematic part of the equation. Most revolutions that I have read about were managed by persons who could be considered “fanatic” by disinterested observers. That’s the danger.

My basic point is that no one seems to have thought all this out thoroughly. It is, after all, Political Economy we are speaking about, not just numbers on a screen or a page.

What I see is an opportunity for another Javits to come along and ‘tinker’ with the ‘system’, with similar results.

Oh undoubtedly it can be gamed, as you suggest, but does that mean every region is playing the same tune or that the fat cats can be bled by such overt means. Especially – if – there is a fiscal component, there has been a public call for it – from increasing voices. Early days I admit.

Skippy… did you have a gander at the Citi data and various conclusions, some were actually contra to what one expects from that mob…

I haven’t looked at the figures yet. It’s on this afternoons reading list. I often shoot so fast my foot gets in the way.

As for sectional rivalries; you have a very good point. Maybe I’m giving “them” too much credit. (No pun intended.)

I don’t know Ambrit, personally, I think you are spot on (and anyway, that’s why we have two feet.)

I’ve been musing that perhaps we could turn a profit on this by selling mattresses outside of banks!

Or, … this is a sizzler…, we could start a chain of “Savings” banks built to look like mattresses.

Big Box Springs

Brooklin Bridge…

I thought we could put away the designer ideology of libertarianism and consider specific regional events, without back tracking to the G20 new world order or Bilderberg group CT, and the only means of warding off their gaze was mattresses of gold.

I think above should be view from at least two perspectives – corporations and citizens and then workout the effects. Seems the designer ideology was actually created to get citizens to think like a corporation, that way individuals inadvertently support corporatist rhetorical arguments from the singular perspective…

Skippy… there is a lot up in my comment w/ the big data dump, so it would be nice if that was actually addressed beyond individualistic perspective wrt mattresses… TA…

Skippy, this is a dead thread, but if you do come back here, your response to my comment was totally justified (and quite good). Your original comment really did deserve serious response (and from people with experience).

Not long after my clownish antics, I wished there was a delete feature but unfortunately that was after the actual one disappeared.

Thanks for your kindness below…

It happens, no sweat Brooklin Bridge…

The other problem with hope in revolutionary movement leadership is that leadership can be decapitation-striked by armed servants of the Deep State.

I thought that was a settled matter here on NC, the term d’art deep state as a commentator and associates coped it for endless promotion.

Skippy…. shall we just evoke the Anunnaki – ????? – and deist with the “they”…. groan~~~

Yes, I remember Banger. “Deep State” was never dismissed. It was hooted down. Banger helped make that easy by going on and onnn and onnnnnn about it exactly the same way each time.

On the other hand, Banger sometimes raised questions which were never answered, only dodged. One particular claim of his could be objectively evaluted to see if it is empirically based on provable facts or not. And that claim is . . . . that the killshot entered RFK’s head from behind RFK, at the very same time that Sirhan Sirhan was standing (and shooting) from the side-fromt of RFK. That claim can be proven factually true or false by someone with the time and diligence to look at all relevant reports. I don’t have the energy to do it, but it can be done.

Banger thought walls of insinuation was analytical rigor and was taken to task for it, with reason, after repeated warnings.

Skippy… you should know libertariansim is vulgar from my prospective, using its dialectal style with me is counter productive…. good luck with that MPS thingy…

I’d prefer they target the savings of the 1%. For some reason they always want to target mine which is why I always wonder if these folks are not retired microscope makers. They seem to have a fixation on tiny tiny accounts.

I’m going to be generous here, if not outright brave and suggest they give the honor of fixing the problem of unproductive money usage to the 1%, perhaps in the form of higher taxes combined with larger inheritance tax combined with stricter rules about off shore bank accounts.

Unlike Ambrit, who rarely (if ever, really) shoots himself in the foot, I must do it all the time cause like more and more retired people, my socks are full of holes.

Thanks but, as Phyllis reminds me, it’s the holes in my head I should really worry about.

Now, if you were an amoral, wealth obsessed narcissist, you wouldn’t have that hole in the sock problem! You do have that problem, so we know to embrace you as “one of us.”

Skippy is our Zen tap on the head. Focus on the real world he tells us. I try skippy, I really do.

Agree, my apologies to Skippy. I confess, however, the idea that monetary policymakers did something right in this atmosphere just goes against all one’s senses, but akkk, aarrrg, uhhhh, Skippy’s, gaakk-comment grrrpp does pxeerp make owwwww a lot of sense, …thud.

Ahem now I see your latter comment.

This is why I brought up the question, too see what others thought of it from a broader perspective and hopefully some that had a more experienced and granular purview.

Skippy… no dramas mate… Cheers

One does have to wade through those charts. However, they do show a trend. I do find it curious that no ‘heavy hitters’ piped up, if at least to try and deny your point. Is this a case of ‘the dog that didn’t bark in the night?’

Sometimes, the best thing the minions of “The Bank of Nibiru” can do is, nothing.

If NIRP were applied against savings OVER the FDIC individual savings insurance limit it would get some people angry, and it might have some good effect that the governators are claiming it will have.

But if NIRP were applied against Dollar One and Counting of every lower class savers’ meager little savings; anger, rage and hatred would become deep and broadbased throughout what we might laughingly call the “lumpenbourgieosie”. It would be a plot to take away some money from people who cannot afford to lose any money at all. The purpose would be to try and torture those people into moving their money into heavily gamed and potentially future-worthless “assets” of the sort handled by FIRE sector “money managers”. Knowledgeable lumpensavers would reject that response as effectively as they could.

If NIRP were applied against lumpensavers like me, how might I respond? If the percentage were small . . . . say 0.5% . . . . I would sit tight for a year andd reduce my spending and see if enough other people would reduce spending likewise to were the sellers of goods and services felt tortured into lowering their prices for goods and services by 0.5%. If they did, then I would figure that my savings had not lost any actual value, and I would leave my savings in the bank to see what happened next.

If the governators tried raising NIRP enough to make it hurt some more every month, and I suspected they would steal my money faster than deflation could restore the value of my remaining money to pre-theft levels, then I would prepay whatever expenses I could . . . rent for a year, etc, durably storable consumer goods for use over time, etc. I would leave just barely enough money in the bank to do things that can only be done with in-the-bank money and I would try to find some way to move all the rest of my meager savings into NIRP proof forms. It might lose value anyway, but at least the governators would not get any of it.

Or perhaps I should say the “bankernators” rather than the “governators” . . . if it really IS two different groups of people.

The point being is not to – just – observe from the individualistic state and if your worried about being liquidated that has already happened [see wealth transfer from 70s onward and hockey stick post GFC] and increasingly so.

Skippy… this is actuality a significant departure from the aforementioned, so it behooves not to – read – things into it.

I remember once reading that a Soviet Red Army General, either Tukhachevsky or Zhukov ( I forget which) once said: “quantity has a quality all its own.” So yes, while the big picture system’s eye view on all this is important, the single individual’s eye view is important also.

Why would I say that? I am a still-employed lumpensaver. Retirees on a fixed micro-income from meager savings and investments are another kind of lumpensaver. There are many millions of lumpensavers. If I am different from all those other millions, then how I would respond to NIRF against Dollar One and Counting of meager savings is irrelevant to the consideration of anything at all. But if my brain is similar enough to 40 million other lumpenbrains that my reactions might predict 40 million other sets of reactions to the same identical policy, then 40 million individual sets of reactions all moving in a similar direction becomes a major big picture force.

If I am one odd mosaic tile in isolation, I can be offhandedly and breezily dismissed. But if I am one of 40 million tiles all arranged, 40 million tiny tiles adds up to One Big Picture. And the wannabe NIRF engineers might want to consider what 40 million lumpensavers with 40 million hearts filled with hate might do in response to a NIRF attack against us and our savings.

You should stick to – the – reality and stop manufacturing your own special version of paranoia. America is not currently nor likely in the near term to use NIRP, its a case by case observation wrt regional agents using it and the potential effects over time.

Skippy…. it would have been better to stick to the data dump and its relationship to the post.

I’m thinking “bail in” at the point you mention. The penultimate financial peculation was given a test run in Cyprus, no?

agree, skippy

The devil is in the details. Is there going to be a similar taking applied to all assets, or just money in a bank account? Will your stawk market portfolio shrink an extra half percent just because of negative interest rates?

If the negative rate is set to 10%, can I borrow a million bucks and have the bank pay me $100,000 yearly? Government should love it, as it can tax that income.

On an instinctive, “animal spirit” sense, negative interest seems wrong.

. . . Up until now a Japanese bond holder has been sitting pretty earning a real yield in a deflationary economy as a reward for maintaining a depressed economy.

Bond holders are not at fault for maintaining a depressed economy. That would be economists with a seat at the policy table, a table non economists are unqualified to sit at. From the James Galbraith post next door.

The CBO and the OMB took the measure of these views as though they were an unbiased sample, which they were not, and as though the situation were within the normal post-war range, which it was not. It’s hard to imagine a set of forecasting principles and consultation practices less well-suited to recognizing a systemic breakdown. Short of a decision to override the forecasting exercise – a decision that could only have come from the President, for which he was not qualified, and that would have been open to criticism as “political” interference in a technical process – there was no way for an unvarnished analysis of the grim situation to make it to the center of policy-making.

To use a Buffetism, the current crop of economists should be plowed under. Crop failure.

From your link from the other day, I found a short description that explains a lot.

Gunnamatta

. . . To me it is obvious that it is the demand – supply balance that is the issue. The accumulation of capital, its concentration, and its tax avoidance, and its marginal propensity to buy entire political systems is the root of the problem . . .

Perhaps, economists might get a clue if their jawbs were outsourced to a cheap labor nation.

The study alluded to polled individual savers on their reactions. How much of the aggregate ‘savings’ available to the economy does this encompass? Many individual ‘savers’ are involved in group savings efforts through 401Ks, retirement syndicates, mutual funds, etc., etc. These funds are not directly managed by the individual. From reading here, I get the uncomfortable feeling that the larger ‘savers’ will scramble into even riskier ‘bets’ to improve ‘yields’ over all. Far from dampening speculation, short termism will enhance ‘risk on’ behaviour. IBG/YBG will almost guarantee a larger than expected ‘disaster’ in the money managing arena.

How the financial managers respond to Negative Interest Rates will be even more important than what small individual savers do.

Low income people have tons of experience with negative interest rates, they just aren’t called that. They are called fees.

Put $500 in an account and don’t touch it. Every month a bankster will dip into it and grab some of your money for him or herself. Soon it it will all be stolen.

This is a case where less income means less ignorance. The fees with CalPERS, 401k fees, most all of’em seem to carry a load that’s hidden by TMI in the fine print. The invisible vig.

” And most would do the rational thing in deflation, which is to hoard cash or squirrel their funds into other investments.”

hypothethical: say -1% interest rates + the normal fees at your bank.

It’s not looking irrational to squirrel away a few grand in cash and then buy a safe, shotgun and some rounds.

sigh. wf.

Mr. Mattress isn’t going to charge me to keep my money and the banking cartel will……..seems like a pretty safe bet to me what a “rational” market participant will do when deciding how to proceed.

I’m kinda surprised they needed a study to tell them that if the banks start taking a percentage of people’s savings on top of the fees already charged that they’d see an exodus of people deciding to become the “unbanked.”

Aren’t these the same people who keep telling us that an increase in price leads to a fall in demand?

Hey, but be all means don’t dare spend or save any of those nefarious benjamins !!!!

No Benjamins for me. Just some Grants, Jacksons, Hamiltons and Lincolns.

And bunches ( well . . . small bunches) of Jeffersons and Washingtons.

Typical of our bumbling policy makers to let the negative rates cat out of the bag before they made cash illegal.

Don’t worry. They will close that cash “loop hole” soon enough, to punish those guilty of the unspeakable and anti social sin of thrift.

So you wanted to save for retirement did you? Shame on you!

I’m not a gold bug; however, where to maintain a store of value out of reach of the government and negative interest rates?

Historically, gold has proven the safest store of value. One does not need to buy ounces; but rather very small denominations of a government’s currency. Given that maybe also made illegal there are very small gold bars and jewelry to consider.

Small purchases in cash cannot be traced or identified.

Do not buy as investment for future profits; but rather a secure storage of assets already in hand.

The smart people I know do not pay attention to price; they just buy every month regardless; for future security.

You sure talk like a gold bug.

Gold has gone from $660 an oz to nearly $1900 and then back down in the last eight years. You can hardly call that sort of volatility “a store of value”.

The only value I can think of gold having is if it becomes the only medium of exchange that is even accepted as money at all. And if that extreme stage is reached, I would rather have spent my money ( if I had that much money) on land and house provably my own, roofwater harvesting systems, waterfree composting toilet, superinsulation, solar or other home-made electricity sources, super productive gardens, micro-orchards, etc., and a lifetime supply in a burglarproof bombproof storage shed of those things I will use till I die but can not make by hand.

Then I would be in a position to laugh at the people who hoarded gold. Let them try eating it. Let them try wiping their butts with it or cooking a meal with it.

A few points…

– Outside the US, there is a push to kill cash… Here in Canada, over the last few weeks, many articles as well as an interview on Radio-Canada have been promoting getting rid of cash. 2 biggest reasons are to get rid of black market and just because technology will lead us there anyway so why be the last adopters? Of course, no mention of capture with negative rates.

– Those keeping cash in the bank are typically risk averse. If they are already saving a disproportionate amount, negative rates will incite them to save even more…. especially if inflation is low!!!

– What savvy investor would lend long term at 0 or 1%? Obvious problem for long-term growth…

– It’s not because it works in some countries at -0.5% that it will work at -2 or -5%.

– They are giving more money to the same ones who are parking it, expecting growth but further reducing velocity. Most of these positive net worth investors are over 55+ and not on the verge of starting new companies. They want safe investments so they won’t be looking at VC or start-ups…

what deflation?

i see. It _might_ happen. The wolf _might_ come.

Good to see the WMD trick still has some life left in it.

Banksters are to Savers as Jihadis are to Shiites………….

Thank you, Yves. I wondered when you were going to put up a post on NIRP. I am beyond horrified with this potential disaster. I decided back in the crash of 2008 that I was done, done, done with putting my hard-earned money into the stock market casino whether via a 401(k) or a Roth (lost 40% of my principal in my Roth). My Dad used to say the only people who should be in the stock market are the ones who can afford to lose their money–so why oh why are all of us stumblebum middle class wage slaves consenting to have all of our retirement funds, if we’re lucky to have employer-sponsored plans, in that casino?? This makes no sense to me.

So I’ve subsequently been trying to save diligently to recoup my 2008 losses and I am simply keeping my savings in liquid form, certainly not earning interest at all. I bank at a credit union, and I am absolutely sick to my stomach that these banksters are now going to make me pay to keep my money safe.

And now the push for a cashless society, which of course is just another way for the banksters to fee us to death.

Honestly, I am so sick and tired of this and I am sick at heart because there is just no place to go. This godawful capitalism is everywhere, and it continues to serve only the very, very wealthy. Of course most of the middle class is apathetic and addicted to the “convenience” of their smart phones (I do not own one and never will).

So I suspect thanks to ignorance we here in the U.S. aren’t that far away from having NIRP forced upon us, and those of us who do not want to pay $700 for a smart phone plus $200 a month for a smart phone will be forced to buy a smart phone since we won’t be allowed to pay cash anymore.

What in the hell is the matter with us?

Because of ferengi rules of acquisition !!

I also have my assets in cash deposited at a bank. When it’s gone it’s the plastic bag over the head. I figure I have ten years. Toodle loo

No Soap Radio

The Mindless Stupidity of Negative Interest Rates:

“this is the Great Stagnation Middle Class Elimination. You can bet that the “General Jack D. Ripper” faction at the Federal Reserve is thinking the unthinkable – and thinking about it incorrectly.”

Consider this quote from a MarketWatch article:

“…pushing rates into negative territory works in many ways just like a regular decline in interest rates that we’re all used to.”

That’s patently false – so much so that it borders on insanity.”

Can anyone show a clear, connect-the-dots example where negative interest rates have stimulated an economy? Can anyone clearly explain how charging an institution or business to hold deposits is in any way stimulative – not “net stimulative,” but stimulative at all?

No one can… because it defies all common sense.”

http://hotstocks.nyc/2016/02/02/the-mindless-stupidity-of-negative-interest-rates/

Old problem for commoners:

“What do you do when the Sovereign is a jerk?”

When you have sovereign money, you can end up with a jerk in charge of the money supply.

There is no modern set of checks-and-balances to constrain the power of today’s central bankers. There is no representative control, or even real public accountability, for today’s central banks. You could say that our central banks are still politically primitive, and in need of political reform and modernization.

The Fed isn’t some independent actor at odds with our elected representatives. It was created by the legislative process. It is doing what our political class wants it to be doing.

1. Negative rates tighten credit conditions because they work like taxes on banks. Negative rates have further reduce NIMs in Japan, in Sweden, Switzerland and Denmark, therefore if banks try to hold profitability constant they have to raise rates for loans.

2. Negative rates represents a switch from carrot to stick. They are inevitably coercive. Coercive policies are fast more likely to result in unanticipated deadweight losses.

3. MMT would suggest that negative rates will result in less aggregate demand not more, because the government will be extracting payments from the population.

But hey, maybe I just don’t understand properly. Maybe the idea is more of a ” I for one welcome our new billionaire class leaders and their coercive self serving policies” sort of situation?

Doesn’t the government already have the means to extract money from the population?

I thought we called them tax rates.

Oh wait, I forgot, our useless Congress won’t raise them because it’ll make people like Bill Gates or the Waltons cry.

negative rates are an admission that too much (reserve) money has been created

if those reserves got out the results wont be good. that is why banks are being paid interest to keep reserves sitting quietly at the fed.

What would be the U.S. income tax implications of negative bank interest rates? Would a taxpayer be allowed to enter a negative number on line 8a of form 1040, or would the taxpayer be required to withdraw money from the account and claim a capital loss?

i doubt they will be able to get negative rates to depositors in the US. there are too many legal hurdles and yellen would face fury (and may be an audit :) at the congress.

it would be easier if they retired the reserves behind maturing treasuries.

Random thoughts:

1. We already have negative real interest rates. I get like 0.5% interest on my savings account, and the TRUE rate of inflation of my costs is maybe 5%. It’s not inspiring me to spend – on the contrary, it makes me feel poor and want to hang on to as much as I can.

Of course, hyperinflation would induce me to spend as fast as the money arrived in my account, but that’s another story.

2. Why should banks care about retail customers? Can’t they get as much cash for zero interest as they want direct from the government? Do retail customers even matter?

3. Negative retail interest rates sounds a lot like confiscation. A tax on people who don’t have the ability to move money overseas etc.

4. Of course negative interest rates can be used as an excuse to get rid of cash – and create total government control of everyone’s spending on anything. No, we’ve decided you can’t have a second ice cream cone today.

5. How about the government loans money to the big banks at a negative interest rate? I mean, the treasury gives a trillion dollars to Goldman Sachs, and then pays Goldman Sachs 5 % interest to hold onto it. Don’t laugh, that’s actually pretty close to what we have going on now…

I think the word ‘negative’ is omitted from Yves’ introduction, most bank customers do not like the idea of negative interest rates. Right?

Good catch, Kevin!

NIRP=Financial Repression

There is no tool or policy or reform of evil madmen. Nor is there for otherwise good men caught in a madman’s web – and the latter category fits so many people who would otherwise not do harm.

If someone means harm they must be caged or destroyed. Failure to do so is what is trapping us all.

ZIRP, NIRP, QE

The real problem is 50 years ago a hidden cancer suddenly manifested openly in Western and particular American elites and it was never excised. So it metastasized into every area and institution.

Let’s call it the Treason of the Highborn. Once the birthmark of high birth it’s now practically a pass into the elite club – even the price of admission.

We’re learning the timeless lesson the hard way that the punishment of betrayal is so high because it rewards at ratio’s and ease of commission with such devastating consequences that the harsh old school penalties are being proven true.

cheers all

An excellent point! Bravo.

How the economy is affected by a stimulus program will of course depend on what sector receives the increased money supply. In my naive view, lowering fed interests rates has increased digital supply for the financial sector, and as expected, generated a nice bubble in the form of asset inflation. Little of this money has gone into the real economy, so that sector still lags. What’s interesting about the proposed negative interest rates is that this time, the targeted sector for a money supply reduction will be funds that are now effectively sequestered as cash savings. This money is likely to be (i) withdrawn and put under mattresses (although monetary goose-down is in short supply: “http://www.zerohedge.com/news/2016-02-27/global-run-physical-cash-has-begun-why-it-pays-panic-first” ), or (ii) reallocated into the form of financial instruments, or (iii) drained away as bank interest, which is equivalent to (ii).

How does moving conservatively-held assets into the casino help Main Street? This is such an obvious fail I can only conclude it’s deliberate. Or maybe I just don’t realize how wise our planners are…Right.

i agree completely with your assessment. furthermore, it’s unconscionable in a society that requires every individual to fend for themselves because it hampers their ability to do just that. more of lambert’s rule 2 of markets in action.

“conservatively-held assets” – I guess that depends whats conservative about it w/ an eye to productivity.

How about a world where wealthy individuals and corporations paid reasonable rates of taxes? That and cutting the military/security budget in half (and still be far more powerful than everyone else combined) over 4 years would pull the US and globe out of this long, low roll all by itself.

If my savings account went negative interest I’d fire my bank immediately and just stash the cash in a safe.

Maybe my secret fantasy of buying some asset with a briefcase full of money isn’t too far off…