A remarkable airbrushing of the state of knowledge about hedge fund returns unwittingly demonstrates how long it takes investors who are desperate for a free lunch, in terms of outperformance without taking commensurate outsized risk, to give up on fantasies. It appears to take eight to nine years.

Let’s be clear about the implications of the Financial Times story: Either by accident or design, it makes it sound as if investors just woke up to the fact that hedge fund performance is not what it is cracked up to be, and are embracing new products that offer some of the desired attributes of hedge funds (having performance not correlated much with that of other asset classes) at lower cost.

Earth to Financial Times: this was old news as of when I started blogging, in 2006,as NC archives attest. And those supposedly newfangled products existed back in the pre-crisis stone ages too.

Here’s the claim in the Financial Times article:

Hedge fund managers are arguably the celebrity chefs of the money management industry. They are best able to whip up returns that make investors drool. But financial engineers are unpicking their secret sauce and finding new ways to sell it by the bottle…

In contrast, hedge fund managers attempt to deliver “alpha”, the returns over and above the market itself, through a staggering array and diversity of strategies, ranging from betting on global currency movements to surfing on the corporate acquisitions boom.

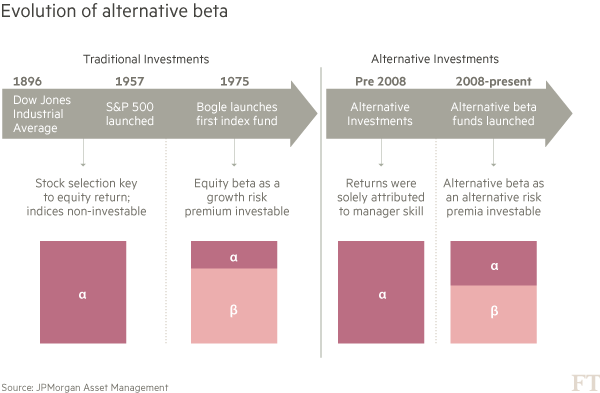

That story line is a complete crock. Hedge fund managers, well before 2008, were widely acknowledging that they did not deliver alpha, or manager outperformance, and were explicitly marketing the idea that they still provided something worth paying for, which they called “synthetic” or “alternative” beta. Not only did we point out then that investors could construct these exposures for far less money than the prototypical hedge fund “2 and 20” performance fees (2% annual management fee, 20% of the upside performance over a specified benchmark), but we noted that there were established funds back then doing precisely that.

Our very first post in 2006 hectored CalPERS for continuing to invest in hedge funds even after they’d underperformed stock and bond indexes for the last three years, and flagged that synthetic hedge fund products had been launched as of then:

The rationale for hedge funds’ eyepopping fees is that investors are paying for “alpha,” that is, the excess return (meaning the return in excess of the “market” return). Investors are willing to pay for alpha because it is considered to reflect an investment manager’s skill, and managers who can regularly outperfrom the market are rare indeed.

But Ms. Wood [of CalPERS] is talking about something completely different. Targeting a particular risk/return tradeoff isn’t an alpha proposition at all. It is instead “synthetic beta,” (or “alternative beta”). And synthetic beta can be produced comparatively cheaply.

A 2005 survey (http://www.edhec-risk.com/edhec_publications/RISKArticle.2005-08-10.3923/view, free subscription required) found that 70% of the investors recognized the role of alternative beta in overall hedge fund results. But this knowledge hasn’t yet translated into a recognition that they are overpaying.

But some of the providers do, and are launching clones to undercut hedge funds. Merrill Lynch introduced its Passive Factor Index earlier this year. Goldman Sachs launched its “hedge fund replication tool,” Absolute Return Tracker Index (http://www.ft.com/cms/s/5b8331c0-82fc-11db-a38a-0000779e2340.html), earlier this month.

From a March 2007 post, Is Alpha All It’s Cracked Up to Be?:

As we have discussed, the problem is that a lot of fees are being paid, but not a lot of alpha exists. In fact, the gap between expectations of hedge fund performance and actual performance has grown so large that the salesmen have come up with a new rationale: “synthetic beta.” You are not paying for alpha, you are paying for a very particular combination of market exposures.

The problem with that is there is no reason to pay a 2/20 fee structure for that. A customized exposure, no matter how exotic, could be designed and implemented more cheaply.

An article in the current Economist, “What’s it all about, alpha?” covers some of the same territory, namely the seeming lack of real alpha, the claims made for the virtues of specialized profiles (the article doesn’t use the term “alternative beta”) and the rise of hedge fund clones based on the view that a lot of hedge funds are charging a lot of money for strategies that can be replicated more cheaply.

The piece is more than a bit distressing, because it serves up arguments that are bunk. The first is that even if hedge fund’s attractive (or seemingly attractive) is simply making the right mix and match of market returns (or betas) that’s worth paying for.

Uh, no. Any investor in a hedge fund has other investments (unless he is a fool). Institutional investors like pension funds hire fund consultants to help them determine asset allocation (as in what markets to be in, meaning what combination of betas to buy, as in how much in domestic stocks, foreign stocks, domestic bonds, etc.). So any “beta mix” decision by a hedge fund could run counter to other investments being made. Put it another way: the hedge fund isn’t being hired to choose which betas to invest in. That’s someone else’s job.

There is also a very strange discussion of style bias. Even hedge funds are expected to adhere to a style. There are hedge fund indices by style, and they are measured relative to the appropriate index. For example, hedge fund strategies include global macro, event arbitrage, emerging markets, distressed, convertible arbitrage, market neutral, etc. Not adhering to your style is very bad and fund consultants and investors punish you for it. If you are an emerging market fund, you can’t go and buy US biotech stocks, no matter how much money you’d make. Similarly, not fitting within a style box also gets you punished. I know of a US fund that has excellent performance that is neither precisely “long-short” nor “market neutral” and that has hurt them in fundraising. Another fund, despite being affiliated with the Basses, was positioned as “opportunistic” which meant they could do anything, and they too found it hard to raise money.

But the story makes it sound as if hedge funds have no style constraints, which simply isn’t true from a practical standpoint. And you can have style biases within your style, but so what? If it doesn’t produce measurable alpha, it’s just noise.

And in April 2007, Now It’s Official: Hedge Funds Deliver No Alpha:

Ha. We were suspicious in back in 2005 when Edhec-Risk, an asset management research company, issued a report, “Hedge fund industry: is there a capacity effect?” which examined whether various hedge fund strategies were becoming too crowded for the managers for the managers to earn excess returns. And excess return (meaning earning more than the relevant market returns), or alpha, represents manager skill. That in theory is why investors pay the huge fees that hedge funds demand (a 2% annual fee + 20% of profits is typical, and some funds get even more than that). Excessive competition was recognized as an issue well before the Edhec report (it led to a collapse of performance in convertible bond arbitrage), but the fact that it was deemed worthy of a formal inquiry suggested widespread interest, meaning widespread concern. And more recent stories have made it clear the problem of lack of alpha is becoming more pronounced.

Even back then, there were efforts to finesse the alpha problem. Oh no, hedge funds’ value wasn’t simply alpha. No, it was that they could generate unique exposures (that theory is “synthetic” or “alternative” beta). While that may be true, first, hedge funds are sufficiently closemouthed about the particulars of their investment approach that it is well nigh impossible to know exactly what sort of synthetic beta you are getting, and hence to know how it will fit with the rest of your portfolio. Second, there is no reason to pay 2% up 20, as the fee structure is described, for mere alternative beta. You can construct that on your own much more cheaply (and some investment banks are offering services that do precisely that).

So even though Merrill has announced that hedge funds are no longer generating alpha, don’t expect a rush for the exits. People want to believe, despite all the evidence, that some investors have a magic touch. And if they don’t get that, they will console themselves with alternative beta.

From MarketWatch, “Hedge funds have lost ‘alpha,’ Merrill director says:”

Merrill Lynch & Co. managing director Heiko Ebens had an awkward message for hedge fund managers and investors attending the 2007 MARHedge conference in San Francisco on Tuesday.

“Alpha has essentially disappeared” from the hedge fund industry, said Ebens, who heads equity derivatives strategy for Merrill in the U.S.

Mind you, we weren’t following the hedge fund beat all that actively, yet it was evident more than nine years ago that hedge funds were delivering little to no alpha, the hedge fund managers were offering up clever rationalizations for their fat fees despite that, and investment banks were launching products to take advantage of the rising awareness of this issue.

So what does the Financial Times article reveal? The degree to which the mainstream media, even a finance-focused publication like the Financial Times, will repeat industry propaganda which lets lazy and complicit investors off the hook. It took CalPES a full eight years to kick its bad hedge fund habit, but to its credit, it finally did that in late 2014. Yet we see the Financial Times repeating the canard that hedge funds outperform, when that hasn’t been true for quite a while, and even worse, hedge fund results have been tracking equities more closely than in the past, undermining their claimed “alternative beta” virtue.

So what this article reveals is how strong inertia is in investment management. We’ve had close to a decade of investors knowing that hedge fund performance is not what it is cracked up to be, and concerted efforts at developing cheaper alternatives. Yet apparently only now is that approach becoming mainstream. It looks as if Max Planck’s saying, “Science advances one funeral at a time,” applies just as well to investment management.

I suspect inertia is strongly at play for the survival of the industry, but I would also have to imagine that it is related to unsophisticated portfolio managers being sold on the ease of outsize returns hedge funds promise to deliver. Apart from that, many people who believe in the hedge fund marketing story are likely in a position to influence investment decisions. The likely criminal hedgie Steven Coen was until recently a member of the board of trustees at Brown University. I wonder what kind of advice he provided to the managers of the University Endowment?

Finally, I have to imagine that hedge funds can be a good source of employment for government officials who steer pension decisions. A lucrative position to generate business seems to await any crooked politician who willfully will sell out the workers who have contributed their earnings to a supposedly stable pension fund.

Probably more crooked than unsophisticated.

Bribes and kickbacks are good sources of income for govt officials while still employed by the govt. And the alpha there is huge–a $5000 investment in an alderman can yield millions in profits.

The real battle is between the collective good and selfish individualism. Will we live by compassion or predation- that is the question.

I’m jaded enough or paranoid enough to believe that MSM misses like this are deliberate, they’re policy. There existed a system that harvested tremendous wealth from the great unwashed prior to the GFC that the Republicrats backstopped to the point of collapsing credibility back in 2008-9. That collapse of credibility has defined the MSM focus since.

While a thousand ways have been found within the complexity of Dodd-Frank to put the wheels back that rotten system, they haven’t been able to soak much from the unwashed largely because there’s so little left there: turning education and healthcare into financial products is small beer considering the lack of blood in the stones being squeezed.

But while the focus has been on these issues in the MSM, the bezzel beyond scrutiny ’till now has moved up market to bleed the lower echelons of the 20% who have seen income increases and wealth accruals since 08. Like the grudging coverage in the NYT of Sanders, can’t really avoid him so might as well trash him, FT is losing credibility with its readers, that same 20%, as they begin to suspect it of being in on the bezzle: time to white wash the time line, voila, we just discovered this!

Why does it come as a surprise that the average HF is not delivering alpha? The average long only absolute returns manager does not either, a fact that has long been known and is in every decent finance book. I would be curious to see how to see how the AUMs of long only absolute returns and HF managers compare. I don’t understand the obsession on HF managers, they tend to be a very boring lot. This excessive media focus is yet another example of our celebrity obsessed medias. The bottom line is that alpha generation is a v rare skill, whether in a long only or long/short/leveraged context. It exists but is not easy to find, especially as the incentive structure implicit in fixed management fees discourages alpha. A good manager attracts more AUM and larger AUMs makes alpha generation more difficult. And with v large AUMs, the temptation is to play it safe and reduce redemption risks and keep the fat management fee, rather than take more risk to generate alpha and a performance fee. So the alpha generation in HF investing is also with identifying managers who are good and won’t give in to the temptation of asset gathering. There are not many of them around but they exist. You just got to find them.

“There’s sucker born every minute”

You have to believe in something for nothing though – easy money …

Wall Street is a fad driven industry. Hedge funds are just the latest product, which like the return of bell bottoms, has gotten stale. The clever parasites will find a new new thing to continue the strip mining of the real economy until the host either mounts ab effective immune response (Bernie?) or collapses and dies. This is how Rome fell.

An investment product that is massively lucrative for its managers gets an undeservedly large flow of funds despite poor performance?

Why, I’ve never heard of such a thing before.