Yves here. How long will the Lucky Country’s good fortune hold?

By Leith van Onselen who has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs. You can follow him on Twitter at twitter.com/leithvo. Originally published at MacroBusiness

From Capital Economics comes an interesting note on Australia’s private debt position:

We can’t rule it out completely, but recent suggestions that Australia is the second most likely country in the world to suffer a debt crisis and recession in the next one to three years seem overblown. The level of household debt isn’t as high as it appears at first sight. And the latest data suggest that the danger posed by the high share of interest-only mortgages is starting to recede…

There are certainly reasons to be concerned. There’s a risk that at some point a major fall in house prices and/or a rise in interest rates will mean that some of the debt won’t be repaid. The latest data, however, suggest that the risk isn’t as big as it first appears and that it may even be shrinking.

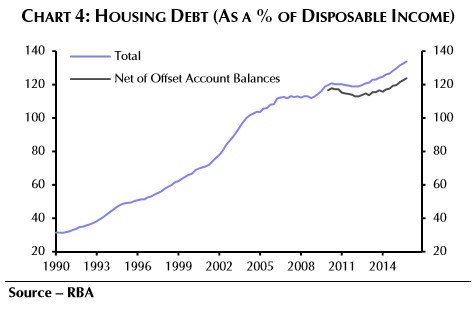

To start with, Australia’s household debt to GDP ratio looks higher than it really is as it doesn’t take into account the cash that households have in offset accounts…

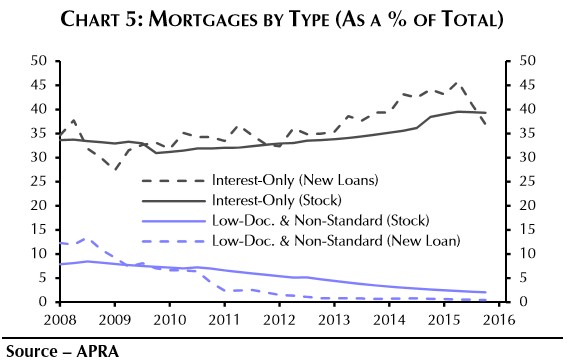

Admittedly, the real concern is that 40% of all mortgages are interest-only mortgages, which are more vulnerable as and when interest rates rise significantly from their current record lows. Make no mistake, this is the single, biggest risk to the housing market and the health of the banks. However, the tighter lending conditions and the recent small rises in banks’ mortgage rates mean that interest-only mortgages have started to account for a smaller share of all new loans…

Overall, we don’t want to sound complacent about the outlook for the Australian economy (we are actually more downbeat than most) and we can’t completely rule out a debt crisis triggered by problems in the mortgage market in a few years’ time. However, the real problem probably won’t emerge until the RBA starts to raise rates from record lows, which may not happen for a year or two yet. And the latest evidence suggests that by then, the foundations of the mortgage market may be looking a bit more solid.

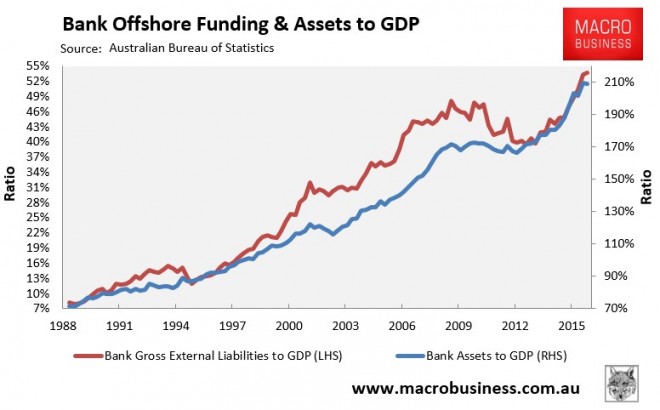

For mine, the bigger risk lie on the liability side of the banks’ balance sheet, whereby they have borrowed obscene sums from offshore to pump housing (see next chart), in the process leaving the banking sector and economy exposed to the whims of global capital markets and the risks of a sudden liquidity shock:

It has also put constraints around the Federal Budget in that it must continually strive for surplus to maintain Australia’s AAA credit rating, otherwise any downgrade would automatically flow-on to Australia’s banks, raising their cost of funding.

Whether or not Australia is likely to experience some kind of financial crisis within the next three years is a moot point. But having one of the world’s most overvalued housing markets, combined with overly indebted households and an extreme reliance on offshore funding, is hardly a good situation to be in and the opposite of prudence.

Running a government deficit should´nt be a problem för Australia given that all government bonds are issued in their domestic currency(AUD). RBA is still the buyer of last resort. But large bank-funding abroad for housing is a big financial risk incl any currency-risks(currency-funding in a crisis). Maybe RBA have to take proactive measures like securing currency credit-lines.

tony

This is about private debt, and it is unlikely the government wants to deficit spend when they have the perfect excuse to cut social spending and privatise public asssets instead.

Yes, and at least when I was there, the central government fetishized running surpluses (!) while the states ran deficits.

ScottW

Interest only loans are the final straw in trying to juice home prices. Since a home’s price is directly tied to monthly payment, once you suck out the principle payment and hit rock bottom on interest rates, there is no where to go but down in home value. Sounds like an American style housing crisis. Are they as deep into CDO’s, MBS’s, etc. down under as we were here?

TheCatSaid

A recent post that mentions Australia’s situation (emphasis mine):

I know that the U.S. market is well past the point of no return with respect to indebtedness and illiquid pension liabilities. I know that hundreds of public companies – many of whom have been off-shoring assets for years – have massive liabilities for securities and financial misrepresentations. My guess is that off-shoring has as much to do with known fraud as it does “tax efficiency”. I know that several countries have adopted U.S. market models only to run the risk of greater instability. Australia, for example, is drinking the Kool-Aid around venture capital and making illiquid markets part of its pension scheme without realizing that the U.S. VC model required highly nuanced tax loss harvesting, robust middle market private equity, and price collusion – none of which are suitably in place for the average Australian investor. The ECB is pretending that the quantitative easing (read Ponzi scheme) that has failed in the U.S. will somehow have a better outcome in fractious Europe. The oil rich Middle East is now realizing that its gilded age may be losing some of its glint with oil depressed and unlikely to rise soon. And Pandora’s box has had some lid slippage with the Petrobras corruption allegations in Brazil. In other words, the current system has run its course and the Bretton Woods experiment has concluded.

And I’m not alone. In his March 9, 2016 note entitled “Japanese Policy Failure Means Disaster for Us All”, John Mauldin details what he and others see in the near future with the “major economic disruption in Japan.” Citing work by Mohamed El-Erian, he details the reflexive and unchartered courses being implemented by central banks which have been using classical economic theory in a market that has not fully understood the implications of demographic shifts, productivity challenges, quantitative international trading techniques and countless other anomalies.

[Omitting significant info re: Japan and skiping to the first part of the post’s conclusions]

As was the case in the turns of the 19th and 20th century, these transitions are not without their opportunistic winners. The few wealthy individuals who, in moments of crisis, can offer bailouts to governments (often to pay for wartime indebtedness) are the ones who set the tone for centuries of predatory enslavement of the general population. Only this time, the denomination of “wealth” might be a bit tricky as the mere accumulation of debt-based currencies may in fact render the “wealth” quite ephemeral and fleeting. While synthetic derivatives and swaps, agency debt, “risk-free” bonds, and the like may be proliferating once again like fungal spores in a rainforest, the arbiter of the impending dislocation will likely be those who have elected to secure control of resources and means of production. A world awash in financial instruments and hedges will likely become a barren landscape when those who have been chasing amoral yield for its own sake are exposed.

Australian banks have balance sheets seriously bloated with residential mortgages and the basic premise is that they are “too big to fail” thus relying on the support of the Federal government by way of an implied guarantee and an actual guarantee (in the case of deposits to a limited level) in the likely eventuality that they become stressed. Income stream growth is now a function of a myriad ‘other practices.’ Small business and commercial finance is being strangled yet this is where future innovation is born. The ratings of some will not stand proper scrutiny and the auditors party. Also they operate in an ineffectual regulatory environment with practices that please pirates especially those recycling investments globally. Election soon. The real economy is a distant memory.

From Australia

If you think Australia will survive its debts, you are living in fantasy land, and not taking into account China’s financial position, nor are they factoring in Japan’s coming collapse, whom of the later we are very much financially tied to as China!

Running a government deficit should´nt be a problem för Australia given that all government bonds are issued in their domestic currency(AUD). RBA is still the buyer of last resort. But large bank-funding abroad for housing is a big financial risk incl any currency-risks(currency-funding in a crisis). Maybe RBA have to take proactive measures like securing currency credit-lines.

This is about private debt, and it is unlikely the government wants to deficit spend when they have the perfect excuse to cut social spending and privatise public asssets instead.

Yes, and at least when I was there, the central government fetishized running surpluses (!) while the states ran deficits.

Interest only loans are the final straw in trying to juice home prices. Since a home’s price is directly tied to monthly payment, once you suck out the principle payment and hit rock bottom on interest rates, there is no where to go but down in home value. Sounds like an American style housing crisis. Are they as deep into CDO’s, MBS’s, etc. down under as we were here?

A recent post that mentions Australia’s situation (emphasis mine):

[Omitting significant info re: Japan and skiping to the first part of the post’s conclusions]

[Leading to discussion of personal options.]

Full post, The Bigger Short, is highly recommended.

Steve Keen also recently put up a list of nations he see most likely to have a private debt crisis soon.

http://www.forbes.com/sites/stevekeen/2016/03/27/the-seven-countries-most-vulnerable-to-a-debt-crisis/

Australian banks have balance sheets seriously bloated with residential mortgages and the basic premise is that they are “too big to fail” thus relying on the support of the Federal government by way of an implied guarantee and an actual guarantee (in the case of deposits to a limited level) in the likely eventuality that they become stressed. Income stream growth is now a function of a myriad ‘other practices.’ Small business and commercial finance is being strangled yet this is where future innovation is born. The ratings of some will not stand proper scrutiny and the auditors party. Also they operate in an ineffectual regulatory environment with practices that please pirates especially those recycling investments globally. Election soon. The real economy is a distant memory.

If you think Australia will survive its debts, you are living in fantasy land, and not taking into account China’s financial position, nor are they factoring in Japan’s coming collapse, whom of the later we are very much financially tied to as China!