By Raúl Ilargi Meijer, editor-in-chief of The Automatic Earth. Originally published at Automatic Earth

Looking through a bunch of numbers and graphs dealing with China recently, it occurred to us that perhaps we, and most others with us, may need to recalibrate our focus on what to emphasize amongst everything we read and hear, if we’re looking to interpret what’s happening in and with the country’s economy.

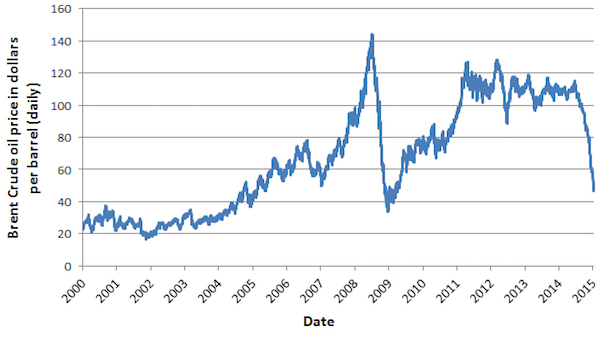

It was only fair -perhaps even inevitable- that oil would be the first major commodity to dive off a cliff, because oil drives the entire global economy, both as a source of fuel -energy- and as raw material. Oil makes the world go round.

But still, the price of oil was merely a lagging indicator of underlying trends and events. Oil prices didn‘t start their plunge until sometime in 2014. On June 19, 2014, Brent was $115. Less than seven months later, on January 9, it was $50.

Severe as that was, China’s troubles started much earlier. Which lends credence to the idea that it was those troubles that brought down the price of oil in the first place, and people were slow to catch up. And it’s only now other commodities are plummeting that they, albeit very reluctantly, start to see a shimmer of ‘the light’.

Here are Brent oil prices (WTI follows the trend closely):

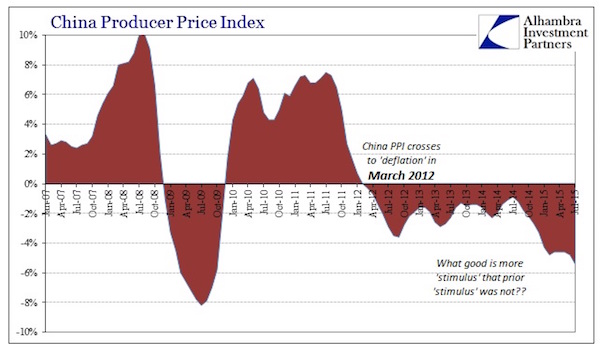

China Deflation Pressures Persist As Producer Prices Fall 44th Month

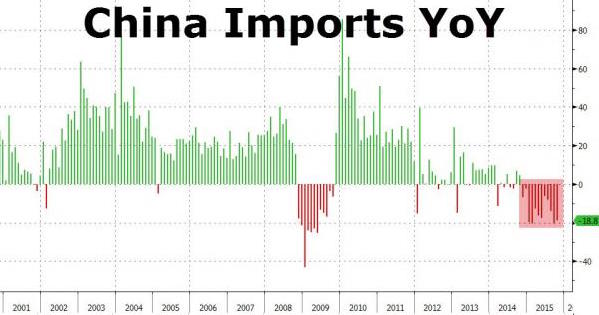

China’s consumer inflation waned in October while factory-gate deflation extended a record streak of negative readings [..] The producer-price index fell 5.9%, its 44th straight monthly decline. [..] Overseas shipments dropped 6.9% in October in dollar terms while weaker demand for coal, iron and other commodities from declining heavy industries helped push imports down 18.8%, leaving a record trade surplus of $61.6 billion.

44 months is a long time. And March 2012 is a long time ago. Oil was about at its highest since right before the 2008 crisis took the bottom out. And if you look closer, you can see that producer prices started ‘losing it’ even earlier, around July 2011.

Something was happening there that should have warranted more scrutiny. That it didn’t might have a lot to do with this:

China’s debt-to-GDP ratio has risen by nearly 50% in the past four years.

The producer price index seems to indicate that trouble started over 4 years ago. China dug itself way deeper into debt since then. It already did that before as well (especially since 2008), but the additional debt apparently couldn’t be made productive anymore. And that’s an understatement.

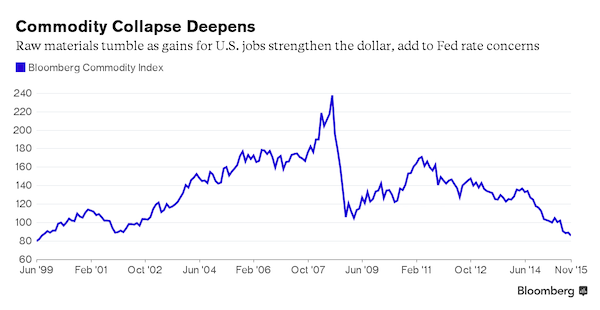

Now, if you want to talk correlation, compare the producer price graph above with Bloomberg’s global commodities index:

Moreover, if we look at how fast China imports are falling, and we realize how much of those imports involve (raw material) commodities, we can’t escape the conclusion that here we’re looking at not a lagging, but a predictive indicator. What China doesn’t purchase in raw materials today, it can’t churn out as finished products tomorrow.

Not as exports, and not as products to be used domestically. Neither spell good news for the Chinese economy; indeed, the rot seems to come from both sides, inside and out. And no matter how much Beijing points to the ‘service’ economy it claims to be switching towards, with all the debt that is now deflating, and the plummeting marginal productivity of new debt, most of it looks like wishful thinking.

And that is not the whole story either. Closely linked to the sinking marginal productivity, there is overleveraged overcapacity and oversupply. It’s like the proverbial huge ocean liner that’s hard to turn around.

There are for instance lots of new coal plants in the pipeline:

China Coal Bubble: 155 Coal-Fired Power Plants To Be Added To Overcapacity

China has given the green light to more than 150 coal power plants so far this year despite falling coal consumption, flatlining production and existing overcapacity. [..] in the first nine months of 2015 China’s central and provincial governments issued environmental approvals to 155 coal-fired power plants — that’s 4 per week. The numbers associated with this prospective new fleet of plants are suitably astronomical. Should they all go ahead they would have a capacity of 123GW, more than twice Germany’s entire coal fleet; their carbon emissions would be around 560 million tonnes a year, roughly equal to the annual energy emissions of Brazil; they would produce more particle pollution than all the cars in Beijing, Shanghai, Tianjin and Chongqing put together [..]

And new car plants too:

China’s Demand For Cars Has Slowed. Overcapacity Is The New Normal.

For much of the past decade, China’s auto industry seemed to be a perpetual growth machine. Annual vehicle sales on the mainland surged to 23 million units in 2014 from about 5 million in 2004. [..] No more. Automakers in China have gone from adding extra factory shifts six years ago to running some plants at half-pace today—even as they continue to spend billions of dollars to bring online even more plants that were started during the good times.

The construction spree has added about 17 million units of annual production capacity since 2009, compared with an increase of 10.6 million units in annual sales [..] New Chinese factories are forecast to add a further 10% in capacity in 2016—despite projections that sales will continue to be challenged. [..] “The players tend to build more capacity in hopes of maintaining, or hopefully, gain market share. Overcapacity is here to stay.”

These are mere examples. Similar developments are undoubtedly taking place in many other sectors of the Chinese economy (how about construction?!). China has for example started dumping its overproduction of steel and aluminum on world markets, which makes the rest of the world, let’s say, skittish. The US is levying a 236% import tax on -some- China steel. The UK sees its remaining steel industry vanish. All US aluminum smelters are at risk of closure in 2016.

The flipside, the inevitable hangover, that China will wake up to sooner rather than later, is the debt that its real growth, and then it’s fantasy growth, has been based on. We already dealt extensively with the difference between ‘official’ and real growth numbers, let’s leave that topic alone this time around.

Though we can throw this in. Goldman Sachs recently said that even if the official Beijing growth numbers were right -which nobody believes anymore- ”Chinese credit growth is still running at roughly double the rate of GDP growth”. And even if credit growth may appear to be slowing a little, though we’d have to know the shadow banking numbers to gauge that (and we don’t), that hangover is still looming large:

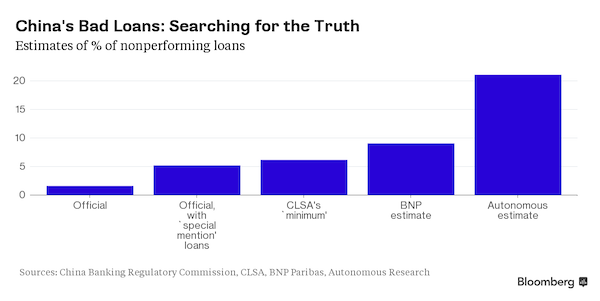

China Bad Loans Estimated At 20% Or Higher vs Official 1.5%

[..] While the analysts interviewed for this story differ in their approaches to calculating likely levels of soured credit, their conclusion is the same: The official 1.5% bad-loan estimate is way too low.

Charlene Chu [..] and her colleagues at Autonomous Research in Hong Kong take a top-down approach. They estimate how much money is being wasted after the nation began getting smaller and smaller economic returns on its credit from 2008. Their assessment is informed by data from economies such as Japan that have gone though similar debt explosions. While traditional bank loans are not Chu’s prime focus – she looks at the wider picture, including shadow banking – she says her work suggests that nonperforming loans may be at 20% to 21%, or even higher.

The Bank for International Settlements cautioned in September that China’s credit to gross domestic product ratio indicates an increasing risk of a banking crisis in coming years. “A financial crisis is by no means preordained, but if losses don’t manifest in financial sector losses, they will do so via slowing growth and deflation, as they did in Japan,” said Chu. “China is confronting a massive debt problem, the scale of which the world has never seen.”

Looking at the producer price graph, we see that the downfall started at least 44 months ago, and that 52 months is just as good an assumption. And we know that debt rose 50% or more since the downfall started. That does put things in a different perspective, doesn’t it? (Probably) the majority of pundits and experts will still insist on a soft landing at worst.

But for those who don’t, please consider the overwhelming amount of deflationary forces that is being unleashed on the world as all that debt goes sour. As the part of that debt that was leveraged vanishes into thin air.

It’s ironic to see that it’s at this very point in time that the IMF (Christine Lagarde seems eager to take responsibility) seeks to include the yuan in its SDR basket. Xi Jinping’s power over the exchange rate can only be diminished by such a move, and we’re not at all sure he realizes to what extent that is true. Chinese politics are built on hubris, and that goes only so far when you free float but don’t deliver.

To summarize, do you remember what you were doing -and thinking- in mid-2011 and/or early 2012? Because that’s when this whole process started. Not this year, and not last year.

China’s producers couldn’t get the prices they wanted anymore, as early as 4 years ago, and that’s where deflationary forces came in. No matter how much extra credit/debt was injected into the money supply, the spending side started to stutter. It never recovered.

http://www.bloomberg.com/news/articles/2015-11-20/china-cracks-64-billion-underground-bank-moving-money-abroad

Too that I would add –

http://www.bloomberg.com/news/articles/2015-11-17/fear-spreads-in-china-finance-amid-unprecedented-arrests-probes

Unpacking using a convo at another site –

WOW – HOLY SHIT !!!

$1 Trillion in corporate debt ?!!

United States Corporate debt has DOUBLED since the GFC and now stands as the single greatest threat to GFC MKII

$10 Trillion in lending to corporations for MERGERS and STOCK BUY BACK alone…….thanks to lending from QE via the Fed Reserve.

But yeah – China has $1 Trillion – blow me down with an atomized feather…..can we get some more CHINA PORN on here STAT – seriously lacking.

Reply

skippy

November 20, 2015 at 8:15 pm

I wonder which country’s consumers are the most tapped out…

Then which country still has some remnants of Laws enforced….

http://www.bloomberg.com/news/articles/2015-11-17/fear-spreads-in-china-finance-amid-unprecedented-arrests-probes

Loved this bit – “The authorities’ goal is to root out practices such as insider trading as part of China’s anti-corruption campaign, and a desire by “some in the political leadership to find scapegoats to blame” for the market crash, according to Barry Naughton, a professor of Chinese economy at the University of California in San Diego.”

So who is Berry…. eh… wellie that would be a Hayekian… rim shot…

Skippy…. sadly in America they are more interested in brand image than the fundamentals of sovereign law…

———–

Skippy… hate to say it but as noted above… which country has the capacity for its citizens to either take on more debt or service it… and at the end of the day to what point….

Then which country still has some remnants of Laws enforced….

From one of your links.

Policy makers say “now we’re innovating, so you can all come in — using high-frequency trading, hedging, whatever — to play in our markets,” Gao Xiqing, a former vice chairman of the China Securities Regulatory Commission, told a forum in Beijing on Nov. 6. “A few days later, you say no, the rules we made are not right, there are problems with your trading, and we’re putting you in jail for a while first.”

The “Law” is whatever we say it is, whenever we want. Humpty Dumpty would be proud.

Looking from the outside in, China seems to be a total madhouse destined for a hard crash landing, economically speaking. Or, they can save themselves by building another 65 million empty concrete shells. Put those destitute concrete plants, back to work!

As opposed to here in the US where the golden rule is inviolable: he with the gold makes the rules….

You say that like its a bad thingy….

Skippy… whom said learning is fundamental to our capacity to cope with future social-ecological change. But how do we stimulate the ‘right’ kind of learning, and …

Skippy, are you aware of the short-term, rip-off, money grubbing, lack of morals (even Scrooge had some) of Chinese? (I hear you on the porn thing. Most of my cultural exposure was through girlfriends.)

What I learned in Asia was that enormous inflows of cash from exports to the West can paper over the largest problems. No tht Jpan and Korea are suffering the global game to the bottom, they are also starting to look like the U.S.: anemic growth, widening inequality, plummeting living standards.

The only ‘better’ thing about asia is that its elites have nationalist tendencies that induce them to try to build -up the country (in addition to their profits).

We shouldn’t be too surprised at falling commodity prices.

Using raw materials to make real things is all very 20th Century, financial engineering is the stuff of the 21st Century.

When Capitalism reaches its zenith, everyone will be an investor and no one will be doing anything.

Central Bank inflated asset bubbles will provide for all.

The biggest market in the world today is derivatives, money making money without a useful product or service in sight.

With the market in derivatives being ten times larger than global GDP we can see that making useful products and providing useful services is nearly irrelevant even today.

We are nearly there.

“When Capitalism reaches its zenith, everyone will be an investor and no one will be doing anything.”

+1000

Ah, that glorious day when we’re all rich, rich, RICHer than Midas from interest, dividends, and rents!!!

Just to amuse myself, I intend to be a dog poop scooper – and pick up some pocket change of 1 million dollars a poop…

Money making money.

Be careful.

It’s like ‘light seeking light doth light of light beguile.’

Money seeking money and money will be of money beguiled.

Your Brent chart only goes to Jan 2015 – a disgraceful manipulation of the data. Is this factual news or polemic?

The graph data extends beyond the hashmarks and the price is now around 15% below the low of Jan’15. Makes the case stronger, as far as I can tell.

Who cares about Brent when transport is going poof….

This problem of debt vs income seems to reflect the ongoing financialization (extraction, not to be confused with financing) of the global economy rather than a focus on capital development of people and the social and productive infrastructure.

I liked how Wray and Mazzucato linked the two in their Mack the Turtle analogy.

“Underlying all of this financialization was the homeowner’s income—something like Dr. Seuss’s King Yertle the Turtle—with layer upon layer of financial instruments, all of which were supported by Mack the turtle’s mortgage payments. The system collapsed because Mack fell delinquent on payments he could not possibly have met: the house was overpriced (and the mortgage could have been for more than 100% of the price!), the mortgage terms were too unfavorable, the fees collected by all the links in the home mortgage finance food chain were too large, Mack had to take a cut of pay and hours as the economy slowed, and the late fees piled up (fraudulently, in many cases as mortgage servicers “lost” payments). The “new model” was inefficient (too many fingers in the pie, all of them extracting value), highly risky (often Ponzi finance from the beginning with reverse amortization), and critically dependent on rising home prices. Even leaving aside the pervasive fraud, the model was diametrically opposed to the public interest, that is, the promotion of the capital development of the economy. It left behind whole neighborhoods of abandoned homes as well as new home developments that could not be sold.”

Mission Oriented Finance

Interesting, the supposition here is that China is heading for a depression similar to the Great Depression.

In my understanding, the Great Depression was an implosion of the credit system after a period of over investment in productive capacity. The investors failing to pay the workers enough to buy the extra goods produced. The projected returns never materialised to pay back the debt… Boom!

China could well be headed down that road, there isn’t enough money getting into the pockets of ordinary Chinese that’s for sure. Elites everywhere just can’t bring themselves to give a break for those at the bottom.

China still has implicit state control of the banking sector, they may still have the political will to make any bad debt disappear with the puff of a fountain pen. That option is always available to a sovereign.

Then again they may just realise in time, someone needs to be paid to buy all the junk.

They were counting on us and the Europeans, but we’ve let them down. The race to the bottom erased the global middle class that could buy Chinese consumer products. They specialized in mass production the way agribusiness has here, where the production is not where the consumption is. It’s as if all the pig farmers of North Carolina and corn growers in Iowa woke up one morning and found out that the people of the Eastern Seaboard had all been put on a starvation diet. The economic results in the grain belt would not be pretty. Ditto China.

So the corn growers need to eat more corn, that’s my logic.

Except that China ain’t Iowa, they can create a middle class as big as Europe and US combined.

It’s just anathema for the ruling class to give the little guys a break.

The global glut of oil and other resources can’t just be attributed to rising production in “tight oil”. Somehow the Powers that be are hiding a great deal of economic contraction. If the world economy were growing it would need oil, copper, lead, zinc, wood and wood pulp, gold, and other metals as inputs. What I want to know is the extent of the cover-up, and what the global economy really looks like.

Where were you in 2011? I was here reading NC. One of the Links posted was a graph of the abrupt shutdown of China’s economy – It was a cliffscape. Very long vertical drop off. So dramatic I could hardly believe it and I said I was having trouble catching my breath. Another commenter said it looked like a tsunami. Of exported deflation as it turns out. Things have been extreme since 2007 when the banksters began to fall; 2008 when Lehman crashed (just after the Beijing Olympics, how convenient for China…) and credit shut down. China was doin’ just fine until then. In spite of the irrational mess in global capitalist eonomix. The only way to remedy it was to shut it down I guess. That’s really not very fine-tuned for a system the whole world relies on, is it?

I don’t remember the graph, but I recall posting about something looking like Hokusai’s Wave at Kanagawa.

Was that the comment?

It was probably you Beef.

Related, this Pollyanna-ish laff-riot op-ed from Ross Gittins, the economics editor of the Sydney Morning Herald:

Don’t buy the China doom and gloom stories just yet

Proceeds from the laughable assumption that official China economic numbers ‘may not be as reliable as we’d like’ rather than being ‘persistently and hugely faked,’ (especially during slowdowns) and ignores that the housing-market slowdown and huge unsold-RE-overhang will also necessarily be accompanied by a price crash, hence a huge amount of toxic debt being exposed – really basic boom/bust dynamics. And no demographic boom coming to the rescue, either. (But he does repeatedly invoke the magic ‘service economy boom’ mantra mentioned by Ilargi.) Thankfully most of the commenters rightly take the author to task.

Not too long ago, some here were still not buying the doom and gloom stories.

I don’t have if they have been persuaded otherwise since.

Couple of thoughts:

Firstly, its only China’s buying that stops oil falling even further Sr Ilargi.

Secondly its a Peoples’ Republic – employment must be maintained.

We are not competent to forecast the future yet. Even the weather surprises us. Its also the case that people who do have relevant data are quite likely to convert that into profit rather than share it.

Don’t worry, be happy. It will be OK.

Tangential Friday night funny: What’s in a name?

Received a small airmail parcel today containing some replacement attachments for my Dremel moto-tool … package was addressed from Shenzen, specifically the “Fuming Manufacturing Park”.

It’s the collapse of bonded warehouse copper/aluminum/etc. lending frauds and all that rehypothecation. I don’t think it’s just a problem in end demand. It’s a problem in the derivatives/futures market.

Think Repo 105.

All of the players were massaging their balance sheets.

But it takes cash flow to pay down the stacked debt.

For many of the players, their primary asset is the financial obligations of others…

Players dependent upon export earnings. — Indeed, they need an increase in export earnings.

But their customers — globally — are saturated.

Factories have been built — for markets that can’t absorb their production.

Beijing has so long insulated manufacturers from goofs that we are here.

The edge of the market has been reached, and many will fall over it.

Here is a very good case study for why people are always wrong about economy and markets.

What happen to all the currency manipulators like Paul Krugman?

China has so much hidden debt — off the books — I don’t think anyone knows what their balance sheet really looks like — to include themselves.

Beijing has held the whip hand – demanding additional GDP… come Hell or high water.

Hence, the provincial officials — across the board — saluted and complied.

But to do so, they had to extend credit, permitting every manner of loan dodges.

In a way, they permitted land and buildings to be ‘repoed 105.’

So, they really have learned from the best.

Now, they shall learn from the bust.