Submitted by Leo Kolivakis, publisher of Pension Pulse.

I am going to follow-up on my previous post on the perils of linear projections by posting Jonathan Nitzan and Shimshon Bichler’s paper Contours of Crisis III: Systemic Fear and Forward-Looking Finance:

This is the third installment in our series about the current crisis. The first article examined the conventional view that this is a finance-led crisis, a turmoil triggered and exacerbated by “financial excesses.” [Note 1] The second debunked the “mismatch thesis,” the belief that the present crisis is our punishment for letting financial fiction distort economic “reality.” [Note 2] The current paper takes on the notion of the forward-looking investor. According to the conventional creed, investors are forever looking into the future: they discount not profits that have already been earned, but those that they expect to earn. This forward-looking premise lies at the heart of modern finance, and investors usually follow its rituals with religious zeal.

But not always.

Occasionally, capitalism is struck by a systemic crisis, a period in which the very existence of the system is put into question. And when that happens, all bets are off. Capitalists lose sight of the future, and forward-looking finance suddenly collapses.

Takeoff

Consider the current moment.

On the face of it, the capitalist class is finally seeing the light at the end of the tunnel. For a few months now, its analysts, statisticians and public officials are spotting “green shoots” everywhere they look. The snowballing global recession, they say, seems to have slowed down. Managers the world over are purchasing more inputs after a long period of buying less; Asian exporters are beginning to put some factories back to work; raw material prices have stabilized, and some are beginning to rise; bank lending is slowly reviving, and home owners are starting to refinance their mortgages at lower rates; and in the United States, the world’s biggest producer-consumer, initial unemployment claims seem to have peaked and consumers are beginning to loosen their purse strings. But the most important sign comes from the equity market: stock prices are the ultimate barometer of capitalist health, and they are soaring.

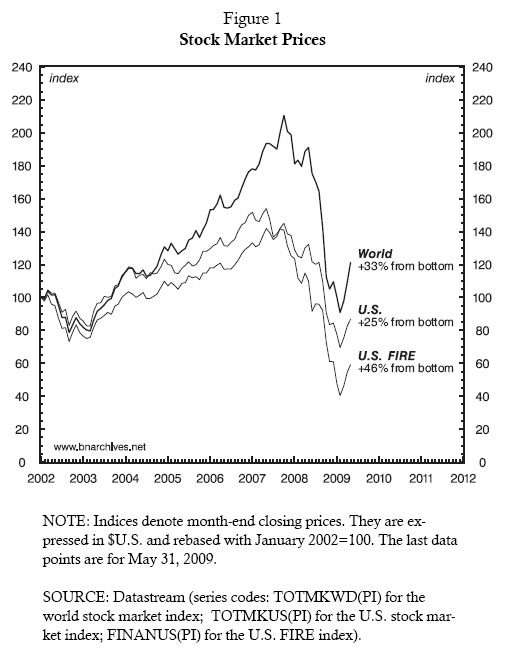

The market takeoff is evident in Figure 1. The chart traces the U.S. dollar price of three key indices—all world equities, U.S. equities, and the equities of the U.S. FIRE sector (finance, insurance and real estate). All three indices show a sharp, synchronized rise. In just three months, from February to May, the world index gained 33%, the U.S. index 25%, and the U.S. FIRE index—previously the most battered of the three—a whopping 46%.

Suddenly, the bulls are everywhere. The greatest returns are usually earned during the initial part of a rally, and no respectable fund manager likes being beaten by a rising average. With the economy apparently bottoming out and with the market having been in a major bear phase for nearly a decade, investors are no longer afraid of losing money; their fear now is not making enough of it. [Note 3] And so arises the specter of “panic buying,” a frenzied attempt to jump on the bandwagon before the really large gains are gone. [Note 4]

Of course, not everyone buys this rosy scenario. Many observers feel that the recent stock market rally is no more than a dead-cat bounce. In the eyes of the pessimists, investors are knee-jerking to a false start. The economic recovery, they say, will be W-shaped, and the market will re-collapse before any real boom can begin. This recession, they warn, is nasty and likely to linger for years.

Forward Looking

Regardless of who is right, though, there is something fundamentally wrong with the debate itself. The current news may be good or bad, revealing or misleading—but, then, investors aren’t supposed to take their cue from the current news in the first place.

To trade assets on the basis of today’s statistics is to be backward looking. It is to be retrospective rather than predictive, to react rather than initiate, to trail rather than lead. It puts investors at the tail end of social dynamics.

Needless to say, such behavior is entirely improper.

According to the sacred annals of modern finance, formalized a century ago by Irving Fisher and popularized during the Great Depression by Benjamin Graham and David Dodd, asset prices are forward looking: “The value of a common stock,” dictate Graham and Dodd in their 1934 immortal doorstopper, “depends entirely upon what it will earn in the future.” [Note 5]

These lines were written against the backdrop of the 1920s. The roaring stock market and the accompanying optimism ushered in by the end of the First World War offered a fertile breeding ground for “new-era theories,” especially in the land of limitless possibilities. The principles of discounting gained adherents, and soon enough past profits became passé. They no longer mattered for the stock market. From now on, declared the gurus of finance, one should view the markets “from the standpoint of eternity, rather than day-to-day.” [Note 6] Looking forward, the only thing that counted was the future trend of earnings.

This forward-looking emphasis—the notion that asset prices discount the deep future—is now sacrosanct. Over the past half-century, this view has been published and republished in millions of articles and monographs, reproduced endlessly in finance textbooks, embedded deeply in computer models and hardwired into pocket calculators. Every accountant, analyst and capitalist accepts it as an article of faith. It is beyond dispute.

But, then, if asset prices depend on the future trend of earnings, why worry about the present recession, no matter how deep?

The Twist

Every investor is conditioned to know that crises come and go with remarkable regularity and that recession always gives way to expansion, so what’s the point of following the latest news on green shoots, commodity prices, or the actions and inactions of purchasing managers and policy makers? Although these immediate news items may be important for journalists, politicians and even economists, their impact on the long-term trend of profit is negligible—so why should they be of any concern to dominant capitalists and their prescient analysts?

And, sure enough, most of time the latter don’t seem to care.

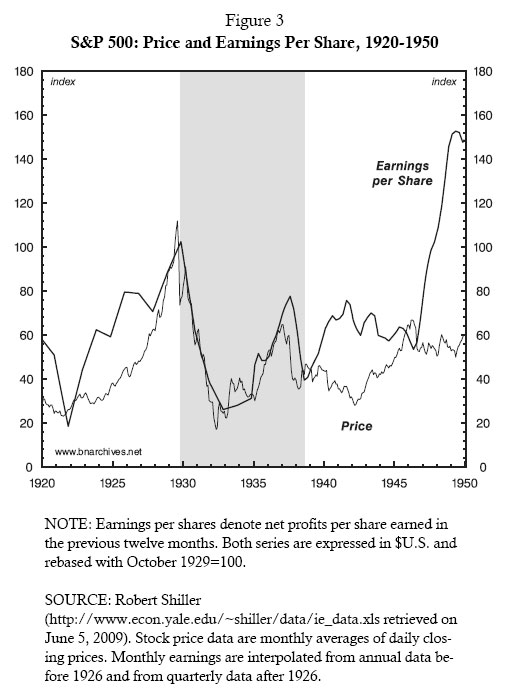

Figure 2 shows the relationship between the dollar price and dollar earnings per share of the S&P 500, a group representing the largest listed corporations in the United States. The series are monthly, with price calculated as the monthly average of daily closings, and earnings per share computed as the average for the past 12 months (both series are normalized, with September 1929=100). The data go back to the 1910s and are plotted against a logarithmic scale to facilitate visual inspection. [Note 7]

(click on figure to enlarge)

Now, if one takes a century-long view, equity prices seem to move more or less together with earnings per share. But from a shorter perspective, the fit is very loose and often negative. The chart shows that the variations of the two series are usually out of sync, that their magnitudes are often very different, and that there are extended periods during which they move in opposite directions.

Theorists of finance don’t consider this loose association problematic. On the contrary, they see it as fully consistent with their basic model. According to this model, investors price an asset by discounting the future profits the asset is expected to generate. In this ritual, investors set the price of the asset—say a share of Microsoft—as equal to the ratio between what they expect Microsoft’s future profits to be on the one hand, and the rate of return they wish those profits to represent on the other. For instance, if investors expect ownership of a Microsoft share to generate a perpetual profit stream of $100 annually, and if they want this stream to represent a 20% rate of return, then they would be willing to pay for the share (or demand to be paid) a price of $500 (=$100/0.2). [Note 8]

Obviously, prices set in this manner should bear little or no relationship to the current level of profit. There are three reasons for the dissociation.

First, since the price is determined on the basis of future earnings, there is no inherent reason for it to be correlated with profits that have already been earned. And that is just for starters. Note that future earnings, by their very nature, cannot be known with certainty and are forever conjectural. For this reason, investors discount not the profits they will earn, but the profits they expect to earn. In the case of Microsoft above, for example, investors can easily misjudge the perpetual future flow of earnings per share to be $50 or $400, instead of the eventual $100; this error will in turn cause them to price the company’s stock at $250 or $2000, respectively (=50/0.2 or 400/0.2); and since profit expectations are rather open ended, the effect is to further widen the disparity between price on the one hand and current earnings on the other.

Second, a given level of expected earnings can generate any number of asset prices, depending on the discount rate of return. For instance, if the discount rate for Microsoft in our example were 10% (rather than 20%), the stock price would double to $1,000 (=$100/0.1). Now, the discount rate changes constantly—partly because of variations in the overall rate of interest and partly in response to changing perceptions of risk specific to the particular equity in question. And since in and of themselves these changes are unrelated to current earnings, the effect is to further reduce the correlation.

Finally, investors are not always able to follow the rituals of finance with sufficient precision. Regardless of how hard they try, their computations are constantly thrown off by various market “imperfections,” government “intervention” and other such diseases; and sometimes, particularly when the investors get excited, the calculations can even become “irrational,” god forbid. Now, since neither the miscalculations nor the irrationality are correlated with current profits, the result is to loosen the fit even more.

So if we adhere to the scriptures of finance, we should expect to see no systematic association between equity prices and current profits. And given that most investors obey the scriptures—including the allowed imperfections and irrationalities—their actions tend to validate the “theory.”

But not always.

Looking Backward

Figure 2 shows two clear exceptions to the rule: the first occurred during the 1930s, the second during the 2000s. In both periods, which the chart shadows for easier visualization, equity prices moved together—and tightly so—with current earnings.

Needless to say, this tight correlation is a gross violation of conventional, forward-looking finance. In fact, the violation is far worse than it seems.

Note that, despite their name, monthly earnings per share represent profits that were earned not during the current month, but during the previous twelve months. This measurement convention means that, during the 1930s, and again during the 2000s, investors committed a cardinal sin. They priced assets based not on future earnings, and not even on current earnings, but on past earnings!

What caused this sharp departure from conventional practice? Why would investors suddenly abandon their convenient forward-looking ceremony and instead take their cue from the dead past? Why give up the predictive powers of precise positivism in favor of poor historicism?

Systemic Fear

In our view, the reason is systemic fear.

Systemic fear has little to do with the habitual apprehension that constantly punctures capitalist greed. Business as usual is always uncertain, and investors are forever fearful about profit. They are concerned that earnings may not rise as quickly as they hope or that they might fall, that volatility will increase or that interest rates will rise. But these fears, no matter how intense, are self-contained. They concern the level and pattern of profit, not its existence.

Occasionally, though, there arises a very different and far deeper type of fear: the terrifying thought that profit might cease to exist. This latter fear is associated with systemic crisis—that is, with periods during which the very future of capitalism is put into question. It is what Hegel meant when he spoke of the bondsman’s “fear of death”:

For this consciousness [of the capitalist bound to the steering wheel of a megamachine gone wild] was not in peril and fear for this element or that [such as falling profit or rising volatility], nor for this or that moment of time [like a sharp market correction or a declaration of war], it was afraid for its entire being; it felt the fear of death, the sovereign master [the ultimate wrath of the ruled]. It has been in that experience melted to its inmost soul, has trembled throughout its every fibre, and all that was fixed and steadfast has quaked within it [will capitalism survive?] [Note 9]

The first time capitalists were gripped by such systemic terror was during the Great Depression of the 1930s. The second time is right now.

The 1930s

Let’s examine each of these periods more closely, beginning with the 1930s.

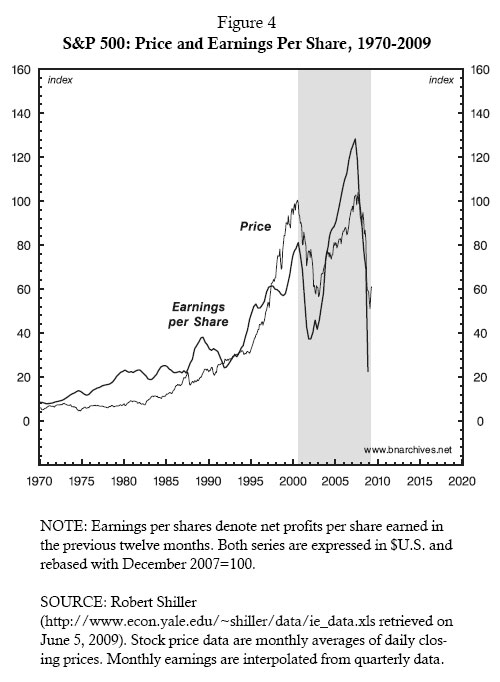

Figure 3 “magnifies” the data from Figure 2. It focuses specifically on the period from the early 1920s to the end of the 1940s, with the shaded area denoting the period of systemic crisis. For ease of comparison, the two series are rebased with October 1929=100 and plotted against an arithmetic scale.

(click on figure to enlarge)

The data show that, during the happy 1920s, stock prices moved rather independently of earnings, exactly as Graham and Dodd’s “new-era theory” decreed. But once the stock market crashed in 1929 and the Great Depression began, the “new-era theory” broke down: the two series, instead of moving independently of each other, suddenly converged and remained tightly locked for nearly a decade.

Both series fell in tandem throughout the 1930-32 period, and then rose in tandem from 1933 to 1936—charting what initially looked like a V-shaped recovery. But the hopeful V soon became a disheartening W. In 1937, a new downturn began, and the two series, which briefly decoupled, again converged in a free fall. It was only in 1939, after a decade of frustration, that the two series again diverged and that the new-era theorists could breathe a sigh of relief.

The political-economic background of the period requires little elaboration. During much of the 1930s, the United States, along with the rest of the world, was mired in a systemic crisis. The very existence of capitalism was at stake, with liberalism fighting for its life against both communism and fascism.

Few felt certain that capitalism would survive, and many—including some of the system’s leading advocates—feared its imminent demise. In this context, the “future trend of earnings” was no longer a very meaningful concept, and there was little point in extrapolating, let alone quantifying, its growth rate.

There was no anchor ahead. All that was solid melted into air, all that was holy was profaned.

And so, in despair, forward-looking investors found themselves latching onto the only “real” thing they could see: the past.

Like the Aymara Indians of South America, they suddenly realized that the future was behind them. [Note 10]

Their assets still represented a claim over the future, but the only way to price that future was to look backward, to what the assets had already earned.

The pricing anomaly ended in 1939. Suddenly, the disorder dissipated, optimism re-emerged and history could again be forgotten. The onset of the Second World War and the boom that ensued sent profit soaring. And the capitalists, cajoled by the apparent efficacy of the new welfare-warfare state, regained their confidence. They abandoned the stale past, returned to their forward-looking rituals and resumed the discounting of expected future earnings.

The 2000s

This situation lasted for sixty years. During that period, capitalism went through many ups and downs, and there was the occasional scare that sent markets reeling. But none of the jolts was serious enough to evoke the Hegelian fear of death. At no point was the existence of the system itself in doubt. It was business as usual, with greed and fear easily incorporated into future earnings projections and risk calculations. The financial model seemed to work like clockwork.

But in 2000, the machine stopped. The threat of a new systemic crisis suddenly loomed large, and the specter of backward-looking pricing, having been dormant for decades, returned to haunt the markets.

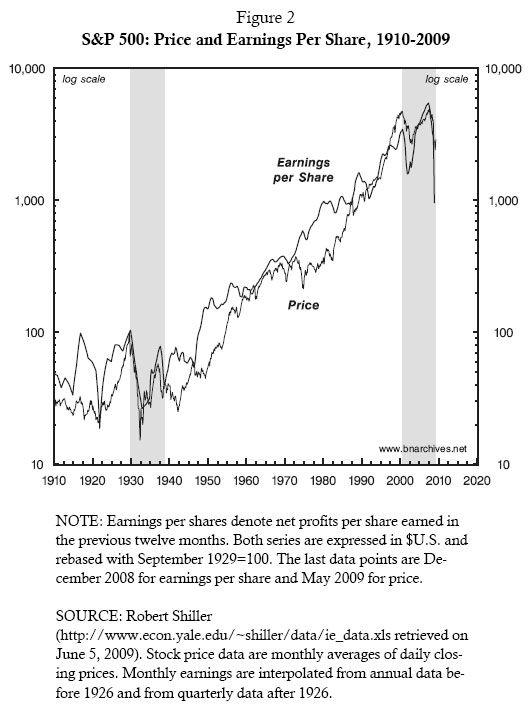

Figure 4 displays price and earnings per share data from 1970 to the present, with the shaded area denoting a period of systemic crisis (the two series again are rebased—this time with December 2007=100—and graphed against an arithmetic scale).

(click on figure to enlarge)

As the figure shows, until the early 2000s both series trended upwards. But in line with the “new-era theory” (which by now had become mainstream finance), the short term correlation between them remained loose and often negative. During that period, earnings have gone through several sharp declines. For instance, in the end-of-communism crisis of 1989-1991 they dropped 37%, and following the emerging markets scare of 1997-1998 they fell 6%—yet in both cases stock prices continued to soar. And conversely, in 1972-1974 earnings increased by 42%, while prices dropped by 43%; similarly, at the end of 1987 earnings increased by 14% while prices dropped by 27% (the latter divergences are seen more clearly on the logarithmic plot of Figure 2).

All in all, then, investors seemed perfectly happy to obey the theory. Throughout the period, they ignored the ephemeral present in favor of the eternal future.

But in 2000, they suddenly lost their forward-looking vision. The dotcom crash and the end of the “new economy,” together with the collapse of the Twin Towers and the onset of an “infinite war on terror,” signaled the beginning of a new era of uncertainty. Analysts started to debate the end of the Washington Consensus, strategists deliberated over the decline of the “American Empire,” and culturalists lamented the demise of the “global village.”

It is true that, initially, nobody was seriously contemplating the “end of capitalism.” But capitalists nonetheless started to grow wary. This was no longer business as usual, and the trajectory of future profits, which in previous decades had appeared neatly bounded and relatively easy to project, suddenly looked murky.

And so, once again, the capitalists found themselves with their backs to the future. Instead of projecting the earning trend looking forward, they began to watch earnings as they unfolded and discount their past declines.

By the middle of 2002, the crisis finally ended. Earnings staged a massive, V shaped recovery and, over the next five years, rose by nearly 350%. And yet, despite the surge, capitalists still found the future hard to envisage. The earnings boom certainly was real enough—but so were its limits. In the United States, the national income share of corporate profits was hitting record highs, so the prospect for further redistribution in favor of capitalists seemed increasingly dim. And those who pinned their hopes on “real” growth were running into doomsday scenarios of “peak oil” and “climate tipping.”

With the future looking disheartening at best, capitalists preferred to keep their eyes on the past. Share prices started to rise only in October 2002, a full six months after the earnings upswing began, and they continued to increase in tandem with profits (albeit at a lower rate) for the next five years.

And then all hell broke loose.

All Bets are Off

The contours of the current crisis are still unfolding, but one thing seems clear enough: the capitalist class has lost its self-confidence.

“Uncertainty is the only certain thing in this crisis,” bemoan the editors of the Financial Times. As of today, nobody knows what is going to happen:

[A] dense fog of confusion has . . . descended, obscuring where we are—falling fast, slowly, bumping along the bottom, or finally turning the corner. . . . Economies are behaving unpredictably and will continue to do so. The instability is both cause and consequence of the great uncertainty that has been spreading out from the financial markets. Fearful and confused, people react erratically to changing news, reinforcing confused market behavour. It doesn’t help that our economic theories were constructed for a different world. Most models depict economies close to equilibrium. . . . And unlike what most models assume, prices are not properly clearing all markets. . . . [etc. etc.] [Note 11]

This sentiment is echoed in numerous publications and speeches, academic and popular. “The whole intellectual edifice . . . collapsed in the summer of last year,” concedes former Fed Chairman Alan Greenspan. [Note 12] “[T]he pillars of faith on which this new financial capitalism were built have all but collapsed,” observes Gillian Tett in a special Financial Times series on the future of capitalism, and that collapse, she concludes, “has left everyone from finance minister or central banker to small investor or pension holder bereft of an intellectual compass, dazed and confused.” [Note 13] And with no intellectual compass to rely on, confesses Bank of England Governor Mervyn King, “[J]udging the balance of influences on the economy” becomes “extraordinary difficult.” [Note 14]

But perhaps the clearest evidence for this loss of confidence is the “fear of death indicator”: the persistence of a backward-looking stock market.

As Figure 4 shows, since their 2007 peak, earnings have fallen by 80%—a drop comparable to the earning collapse in the first three years of the Great Depression depicted in Figure 3. If capitalism is here to stay, this must be the mother of all investment opportunities. As the system recovers, profits are bound to rebound—and, from their current lows, the rise could be spectacular indeed.

A shrewd academic would probably have developed this apparent “anomaly” into a full-blown mechanized model, complete with a universal taxonomy of “fear-of-death” eras, a menu that alerts investors when to switch and reswitch between forward- and backward-looking postures, and an easy to follow list of “how to profit” from both. And judging by what is on sale in the analysis market, this model could end up having plenty of paying followers.

We prefer to forego this investment opportunity and instead keep our speculations tentative and free. It seems to us that some investors must be feeling the greedy itch of an overly discounted market, and that this itch may explain the recent rise in equity prices shown in Figure 1. But for most investors, all bets are still off. This is a period of systemic crisis, a social upheaval in which the very future of capitalism is in question. And as long as capitalists continue to doubt their own future, they are likely to remain dubious of the models that describe this future and hesitant to apply the pricing rituals that these models dictate. [Note 15]

Capitalism may survive this upheaval, as it survived the Great Depression. But its continuation may well entail a significant transformation—one that restructures both the architecture of power and the ideology of the powerful.

This is the transformation capitalists are eagerly waiting for. And until this transformation gets under way, backward-looking prices seem here to stay.

End Notes:

1. Shimshon Bichler and Jonathan Nitzan, Contours of Crisis: Plus ça change, plus c’est pareil?, Dollars & Sense, December 31, 2008.

2. Shimshon Bichler and Jonathan Nitzan, Contours of Crisis II: Fiction and Reality, Dollars & Sense, April 28, 2009.

3. Given the extent of the crash, some strategists started to speak of an imminent bull run already in late 2008. But the bulk of the pack remained in watchful waiting, and it is only now, after the market had finally turned, that run-of-the-mill analysts claim they have anticipated it all along. For a historical examination of major bear markets and subsequent bull runs, see our Contours of Crisis: Plus ça change, plus c’est pareil?.

4. “A long-unheard phrase was on the lips of many equity traders during this week’s market rally—panic buying. Even after two months of steady gains for stocks, there were few signs of investor fatigue—indeed, the overriding sense was the fear of being left behind. . . . ‘You could say there was an element of panic about it—there were a lot of underweight players driving the market higher out there,’ said Tony Betts, senior sales trader at CMC Markets in London. ‘We clearly reached a situation where the bears felt they had suffered enough punishment’“ (Dave Shellock, Investors Willing to Dive Back into the Fray, Financial Times, May 8, 2009).

5. The quote is from Benjamin Graham and David L. Dodd, Security Analysis, 1st ed. (New York and London: Whittlesey House McGraw-Hill Book Company Inc., 1934), p. 307-9. Fisher’s analysis of present value is articulated in The Rate of Interest. Its Nature, Determination and Relation to Economic Phenomena (New York: The Macmillan Company, 1907).

6. Benjamin Graham quoted in Jason Zweig, Be Inversely Emotional, Not Unemotional, The Wall Street Journal, May 26, 2009, p. 28.

7. A logarithmic scale amplifies the variations of a series when its values are small and compresses these variations when the values are large. This property makes it easier to visualize exponential growth (note that the numbers on the scale jump by multiples of 10).

8. The practical computation, of course, could be far more complicated, but the basic relationship between expected profits and the discount rate of return is always present. For a detailed critical examination of discounting, see Jonathan Nitzan and Shimshon Bichler, Capital as Power. A Study of Order and Creorder (London and New York: Routledge, 2009), Ch. 11.

9. Georg Wilhelm Friedrich Hegel, The Phenomenology of Mind, translated with an introduction and notes by J. B. Baillie, 2nd Revised ed. (London and New York: George Allen & Unwin and Humanities Press, 1807 [1971]), p. 237, emphases and contemporary parallels added.

10. The Aymara language, spoken by Indians in Southern Peru and Northern Chile, reverses the directional-temporal order of most languages. It treats the known past as being “in front of us” and the unknown future as lying “behind us.” To test this inverted perception, just look up at the stars: ahead of you’ll see nothing but the past (see Rafael E. Núñez, and Eve Sweetser, With the Future Behind Them: Convergent Evidence from Aymara Language and Gesture in the Crosslinguistic Comparison of Spatial Construals of Time, Cognitive Science: A Multidisciplinary Journal, 2006, Vol. 30, No. 3, pp. 401-450).

11. Editors, Sound and Fury in the World Economy, Financial Times, May 16, 2009, p. 6.

12. Edmund L. Andrews, Greenspan Concedes Error on Regulation, New York Times, October 23, 2008, p. 1.

13. Gillian Tett, Lost Through Destructive Creation, FT Series: Future of Capitalism, Financial Times, March 10, 2009, p. 9.

14. Editors, Sound and Fury in the World Economy, Financial Times, May 16, 2009, p. 6.

15. Note that the latest earnings-per-share reading in Figure 4 is for December 2008, whereas the most recent price datum is for May 2009. This gap means that the early 2009 increase in prices could end up being correlated with a yet-to-be reported rise in current earnings. . . .

The great uncertainty among capitalists can be easily gauged by the sharp drop-off in business investment across OECD economies. But is there really a fundamental shift going on right now or is this the normal cyclical response to a severe and synchronized global downturn?

Moreover, I would argue the crisis in capitalism has been simmering for a long time and the ‘great transformation’ will boil over when global pension tension reaches a breaking point. In many ways, we have already reached the breaking point. Entire industries are in upheaval and along with them the retirement security of millions of workers and retirees.

Governments will respond by extending the amortization period on pension solvency rules, but this is a short-term fix, not a viable long-term solution.

There will be great social, political and economic transformation in the next twenty years. What remains to be determined is whether the “new capitalism” will be based on old principles or more inclusive and more humane principles that will benefit a greater proportion of the world’s population.

More animal spirits. Why don't we use reductionism and say it's due to adrenaline; or rather, that the earth is finite and capitalism with its unlimited growth model will destroy it.

I agree w the thesis as it applied in the 1930s. The past decade was nothing like the '30s. Only the past year was in term of FUD: fear, uncertainty and doubt.

What happened this decade was probably unprecedented market manipulation PLUS the fact that long-term interest rates were so stable (Greenspan's 'conundrum'), so the discount rate/PE ratio didn't change much.

Thanks for this article.

An article once again proving that this site and its associated contributers sites are truely outstanding.

I have two criticisms of this article. One, it is non-sensical. And two, it longwinded being so.

It lost me almost from the beginning.

"The second [article] debunked the “mismatch thesis,” the belief that the present crisis is our punishment for letting financial fiction distort economic “reality.”

Yes, we can't let reality get in the way of finance. I mean how much more reductionist can it be that if the market goes up, this is ipso facto evidence of forward looking and if it goes down, then investors must be backward looking. Why not junk the superfluous theoretical structure and just say: Market go up, good; market go down, bad.

For an article that discounts history, it spends an inordinate amount of time examining it. It seems the main point of this article is that we should forget history because history might inform us that there is a cliff up ahead. This might cause us to rethink our headlong rush and engender feelings of fear and death. How much better to go over the cliff with a positive attitude than to consider our position and maybe avoid the cliff altogether.

Yeah this is a really interesting article..

There's good reason to think that capitalism is tapped out in the G7 bloc. The public and private debt levels of these countries indicate it.

Thanks Leo, Always enjoy your posts.

Dimension_size is the big issue, eh? Does capitalism have its limits in a finite closed world ie endless job creation, of products that add value to life and are not destructive in the long term to our selves or the environment.

The all conquering nations are glorified in history, but always slowly decay when pushed to their limits, when opposing forces reach parity to its expansion.

Hyper Individualism can not exceeded the boundary's of a worlds ability to support it, for all individuals. If the top of society lays claim over an increasing disproportionate share of the society's gains, the spread of the gains through out sociality is diminished and in times of calamity badly need recourses can be horded, when their need is at its most.

The tops fear of change has gone on for to long. Badly needed change is forth coming like it or not. The only question I see is how much pain will be required to stimulate it.

skippy…@VG GOLD your set pat, I fear your services is the next bubble to expand.

"Government officials can help defuse the fear and anxiety terrorism has incited in people around the world, said psychologist Pamela Ryan, PhD, managing director of Issues Deliberation America/Australia (IDA), at a Sept. 10 press conference held at the National Press Club in Washington, D.C. IDA, the event sponsor, operates as an independent research group, but collaborates with universities such as the Australian National University and the University of South Australia.

Other speakers at the event underscored the importance of mitigating terror's psychological hold.

"The context of terrorist attacks needs to be narrowed," noted speaker Patrick Boyer, a political scientist and former member of the Canadian Parliament. "No society can sustain constant, generalized fear."http://www.apa.org/monitor/dec04/anxiety.html

Thank you for seeing that the Psyop the non-stop terrorization of America has economic consequences and quite possibly a large role in our current problems.

It will take a generation to undo its effects.

I'm just really stunned at the extraordinarily unbalanced length/quality ratio of this post.

Well said Skippy.

Some of these economists should begin to read ecology.

Start with

Overshoot: The Ecological Basis of Revolutionary Change

and the many papers citing it:

http://scholar.google.com/scholar?q=Overshoot:+The+Ecological+Basis+of+Revolutionary+Change&hl=en

excerpted among other places here online: http://dieoff.org/page15.htm

"… Amid the economic and political events of 1929-32 it was plausible for Americans, unaware of the ecological basis for what was happening, to see all the difficulties of that difficult time as products merely of the failures of the Hoover administration. This attractive oversimplification neglected one fact that should have been obvious: many other nations, over which Mr. Hoover did not preside, were undergoing the same calamity.

For those of radical inclination, it seemed plausible (in the absence of an ecological paradigm) to attribute the dire situation to a failure of "the capitalist system." But socialists believed as ardently as capitalists in the myth of limitlessness. In spite of socialists' commitment to production for use rather than for profit, they were not then (and have not been since) any more cautious than capitalists about adopting the drawdown method. They assumed that socialist-sponsored versions of drawdown could somehow eliminate such "capitalist contradictions" as simultaneous overproduction and abject poverty. They remained just as unconcerned as the capitalists about overshoot. [10]

Conservatives, on the other hand, who were not necessarily misanthropes, found it plausible to whistle in the dark, insisting that prosperity would automatically return if we just waited for the system to adjust itself. They were the Ostriches of their time, holders of the Type V attitude (delineated in Chapter 4). They believed nothing essential had changed from the Age of Exuberance…."

B&N are 'value form theorists'*, right?

So end up conflating things like profit and earnings, value and price,,,and missing the contradictions between, say the nonfinancial and financial brought on by overaccumulation and falling rate of profit in the former, and attempts to compensate for this via increased speculative activities – a pretty basic dynamic which has evidenced time and again since at least the mid 19th c and can be seen as one not-theoretic mismatch, though perhaps not the ones they argue against in CoC II.

One 'value form' argument made in '99 was:

it is a peculiarity of value (as opposed to weight, for instance) that it can only exist in so far as it is measured. Price is its measure. Without money, therefore, value could not exist.

Which leads to all sorts of rentier illusions, some of which I'd brought out in a long post that failed to post but the gist gets down to the evident reality of value created in the processes of production and that such value need not = price nor necessarily dependent upon the existence of money. That the 'beginning and end' of the circuit of production is M does not make that process identical to one of M-M'.

Taking form for substance ignores contradiction, so also motion and leaves explanation to psychology and/or power relations while the real world of capitalism is somewhat more involved.

Brilliant post.