The mortgage beat has been quiet of late, but I must confess to being remiss in writing up two recent losses suffered by MERS. One of the big reasons that MERS has taken comparatively few losses in court is that it has often settled cases where it looked like it might lose.

Today, we’ll deal with the higher-profile one, that of a filing by the Montgomery County recorder in Pennsylvania, Nancy Becker, for herself and on behalf of all county recorders, against MERS, in Federal court. The basis of the suit was that MERS had violated a state law that required that conveyances of real property be recorded in county recorder of deeds’ offices. Becker argues, in effect, that the mortgage (the lien against the property) and the note (the borrower IOU) were inseparable, and that trying to treat the note as separate and exempt from the recording requirement was a “willful and negligent” violation of statute. She sought, among other things, that MERS be required to record mortgage transfers and that it be found to have engaged in unjust enrichment.

MERS has won suits filed by recorders in other states, but the flip side is that MERS suffered a major loss in Oregon, which has a state recording statute.

Even though the court accepted the premise that notes could be transferred readily, which was one of the legs of the argument MERS advanced as to why it did not need to record mortgages, it rejected the notion that it meant mortgages weren’t subject to the state recording law. The judge cited decisions from 1848 and 1850 and pointed out:

These holdings remain undisturbed despite the passage of more than 150 years and thus the underlying purpose behind the Pennsylvania recording acts remains clear – to provide notice to the public of the identities of those who hold an interest in real estate as well as notice of the true nature of the transaction on record…And in 1852, it was determined that the assignment of mortgages also fell within the recording acts…in 1863, the Pennsylvania legislature first decreed that such recording be mandatory.

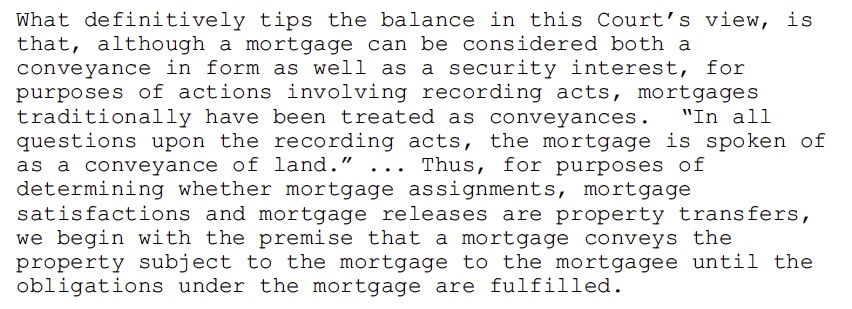

The judge pointed out that there were nevertheless competing legal theories and decisions on both sides until a Pennsylvania Supreme Court case in 2004, Pines v. Farrell, which focuses on the issue of whether a mortgage constituted a property transfer. Here is the key section:

The judge also found MERS could be held responsible for damages:

We likewise reject the proposition that MERS is not subject to liability because it is only an agent for its member-lenders. Indeed, as a general matter, an “agent” is a “person authorized by another (principal) to act for or in place of him; one intrusted with another’s business.

As Georgetown law professor, Adam Levitin, said succinctly by e-mail, “MERS hasn’t lost a case like this before.” Damages are to be awarded in a jury trial. Note that this case did not decide the validity of mortgages in the MERS system, but you can be sure that borrower attorneys are planning to file a boatload of cases on the back of this decision.

This case is certain to be appealed. Not only is MERS facing a possibility of a very costly award, but this also increases the odds of suits in state where title does not pass to the borrower until the mortgage is paid off in full (aka “title theory states“) and state law requires that property transfers be recorded. While this decision seems promising, and is carefully argued, Tom Cox, the Maine attorney who made robosigining a national issue, thought that the appeals court would be likely to certify the MERS question to the Pennsylvania Supreme Court, which could very well reverse the district court decision. So keep the champagne on ice for now.

118-Memorandum-and-Order-dated-6-30-14-00122979

Memorandum and Order dated 6-30-14 (00122979)

119-Order-re-Summary-Judgment-6-30-14-00122980

Order re Summary Judgment 6-30-14 (00122980)

Thank you, Yves, for posting on this important case. It is depressing that county recorders apparently agree to settle cases with MERS. I doubt that any of the millions of people whose lives have been destroyed by mortgage fraud ever benefit from those financial settlements. Perhaps it is foolish to hope that MERS will lose on appeal, but yet I do.

Mortgage Electronic Registration System (MERS) not MERS (Middle East respiratory syndrome (MERS).

hehehe

They’re both deadly.

How dare the peasants question Covington & Burling’s handiwork?

-DN

http://www.reuters.com/article/2012/01/20/us-usa-holder-mortgage-idUSTRE80J0PH20120120

Thank you, Yves, for this posting reminding us that the MERS system hasn’t gone away. I’m not a lawyer, and the following may not be pertinent, but I found the New Mexico Supreme Court comments recorded here in a February finding most interesting. Perhaps others who have more facility with these matters can comment on this case:

http://livinglies.wordpress.com/2014/02/18/new-mexico-supreme-court-wipes-out-bank-of-new-york/

“provide notice to the public of the identities of those who hold an interest in real estate as well as notice of the true nature of the transaction on record” C’mon, let’s be reasonable, here. If we did that, how could we get our commissions for slicing and dicing mortgages into CDOs, let alone sell the same property to multiple buyers? It’s like this judge is biased against fraud, or something. What a nut job.

It is not surprising in Montgomery County, where I now live, that there is this turn of events. Not only are the judges siding with the people in regards to their homes, but also, in the matter of credit card law suits to obtain judgements, the county managing judge does not want the various local judges taking on cases from dubious sources. Credit card companies frequently write off bad debt and in amounts too small deemed to be worth pursuing, sell off little more than mailing lists with account numbers to debt collectors. These data dumps wind up phone calling and dunning with local attorney letter heads demands for payment. When actual cases are filed in the local courts around the county, the attorney is usually by themself and gets a default judgement. However, a change in how these credit card cases are being handled resulted in a demand by the judge to see the original note and the assignment of the note in order for an even uncontested claim. This simple request usually defeats all but the most high valued claims pursued by attorneys who are provided with the proper paper work from the the creditor.

It is hard to say just how much it will take to overturn this at the PA Supreme Court level. There are too many people that make a living as a part of the real estate sales business, especially Title Insurance Companies, who may simply refuse to insure clouded titles, killing mortgage loan approvals and blowing up the deal in the process. MERS has to overcome hurdles in PA, with 12 million residents, all who have a claim on the system as it is constituted. From the licensed realtors, to the mortgage brokers, to the appraisers, title insurance companies, the local county officials, all of these people have already been socialized as well as trained to operate a system that provides the right to property are ensured by due process. For MERS to insinuate itself into a large scale state with millions of homeowners and property titles that date back to William Penn Land Grants in the late 1600’s is to promote legal chaos for all of the tiny parcels of homes. Maybe formerly rural and recently urbanized areas, such as the South and Southwest can be rolled over for efficiency but with a long established tradition of due process, the institutional inertia is great.

——————————————————————————————————————–

Zombie Homes: Homeowners vacate and empty out houses before foreclosure is finalized.

http://www.philly.com/philly/classifieds/real_estate/20140706_Zombie_houses_-_vacated_but_not_foreclosed_-_haunt_the_market.html

Yes, the title insurance companies. I’ve been wondering about those. There are many claims that MERS clouds millions of titles, probably depending on state law. I gather the title insurance reviews didn’t check for that. If they start doing that, they’ll make those millions of titles unsaleable until the title is cleared somehow. In short, they could throw the whole real estate business into chaos; and some of them are probably badly exposed if they’ve insured titles that aren’t sound. I’ve seen no one deal with that factor; could be a whole new crash. I’ve no idea what capital stands behind the thousands of local title co’s – does anyone out there know?

This seems like the right place to ask.

Of course over time the title defects clear up as adverse possession laws kick in. In particular if you pay the taxes on the land as well as possess it, the periods tend to be shorter. What Pa will need to do is to put a 4 to 5 year limit if you pay the taxes (as some other states do). In Pa the problem will clear up when 21 years have elapsed, so we are 1/3 of the way there already.

Yeah, making it difficult to foreclose is one thing, but clouding the title is a HUGE kettle of fish.

First American Title Insurance Company is a shareholder of MERSCORP Holding, Inc., parent company of Mortgage Electronic Registration Systems, Inc. (MERS). Stewart Title is also a shareholder. So are Freddie Mac, Fannie Mae, Bank of America, CitiMortgage (merged into CitiBank), Sun Trust and others.

https://www.mersinc.org/about-us/shareholders

The title policies I have reviewed try to use MERS to cover the securitization issues which will surely arise when the mortgage is recorded in the name of MERS. The effort to limit liability through the use of the MERS data base may eventually create liability when the conspiracy to defraud is proved. There is a case pending in Wisconsin state court right now in which First American Title Insurance Company, MERSCORP, MERS and Bank of America are all parties. That case involves a Freddie Mac loan which Bank of America is trying to foreclose in the name of Bank of America.There may be a Freddie Mac class action involving multiple servicers for failure to disclose the real party in interest in hundreds, if not thousands of Wisconsin foreclosures. The title companies could be on the hook for trillions of dollars in claims from homeowners who bought title insurance where MERS appears in the chain of title prior to a foreclosure. All Wisconsin foreclosures in the name of MERS are void under Wisconsin law, which requires the party which holds the Note and is entitled to enforce it to foreclose. MERS did not hold any Notes, loan no money, collected no payments. It merely acted as an agent for undisclosed third parties.

Thanks, rur42 for telling us what MERS is. C’mon Yves!