By Delusional Economics, who is determined to cleanse the daily flow of vested interests propaganda to produce a balanced counterpoint. Cross posted from MacroBusiness

As I’ve been covering over the last few months the data coming out of Europe of late has been slowly getting better, and last nights’ PMI continued the trend.

Eurozone stabilises as PMI hits one-and-a-half year high

• Flash Eurozone PMI Composite Output Index at 50.4 (48.7 in June).18-month high.

• Flash Eurozone Services PMI Activity Index at 49.6 (48.3 in June). 18-month high.

• Flash Eurozone Manufacturing PMI at 50.1 (48.8 in June). 24-month high.

• Flash Eurozone Manufacturing PMI Output Index at 52.3 (49.8 in June). 25-month high.The Markit Eurozone PMI Composite Output Index rose above the 50.0 no-change level in July for the first time since January 2012, according to the flash estimate. The PMI rose for the fourth successive month, up from 48.7 in June to 50.4.

Manufacturers reported the largest monthly increase in output since June 2011, registering an expansion for the first time since February of last year. Service sector activity meanwhile fell only marginally, recording the smallest decline in the current 18-month sequence and showing signs of stabilising after the marked rates of decline seen earlier in the year.

New orders fell only marginally during the month, registering the smallest decline since August 2011. The rate of loss of new orders has now eased for four straight months, helping the rate of decline in backlogs of work ease to the slowest for nearly two years in July.

New orders for manufactured goods rose for the first time since May 2011, buoyed by a slight increase in new export orders. Incoming new business in the service sector meanwhile continued to decline, although the drop was the smallest seen since March of last year.

The easing in the rate of loss of new business was a factor helping drive expectations for service sector business growth in the year ahead to the highest since April.

….

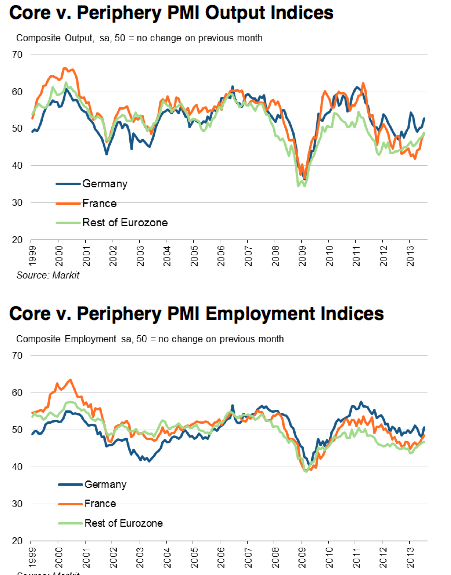

By country, output rose at the fastest rate for five months in Germany. Service sector growth hit a five-month high while manufacturers reported the steepest monthly increase in output since February of last year. Overall job creation hit the highest since March.In France, the rate of decline eased to the slowest seen since output began falling in March 2012. This was buoyed by a return to growth in manufacturing, which reported the largest rise in production for 17 months. The service sector meanwhile saw the smallest downturn in activity for 11 months. Employment fell across both sectors, though to the weakest extent since April 2012.

So, again, some goods news , but let’s not get ahead of ourselves here. If you’ve been reading along for any length of time you will know much of this new found competitiveness in many European nations is because they have squashed down internal demand making themselves more competitive by lowering wages and standards of living, which has included large increases in unemployment. One of the key issues I have talked about since I started covering the Eurozone is that this particular strategy is mutually exclusive with the idea that existing debts, serviced by pre-existing higher wages, were ever going to be paid back.

Obviously, much of the economic and political elite in Europe weren’t too keen to address this particular issue as it would have required banking systems across the region to realise actual losses on their balance-sheets, something that is on-going. So instead the Eurozone went on a campaign of “extend and pretend” in hope that somehow, at some time in the future, the economy would pickup and all would be well again. Of course, the fiscal policies of the zone have made this particular issue even harder to address so, as the economic slump has continued, the ability for debts to be serviced has worsened and now, in many cases pushed onto sovereign balance-sheets, debt to economic output ratios have reached alarming levels.

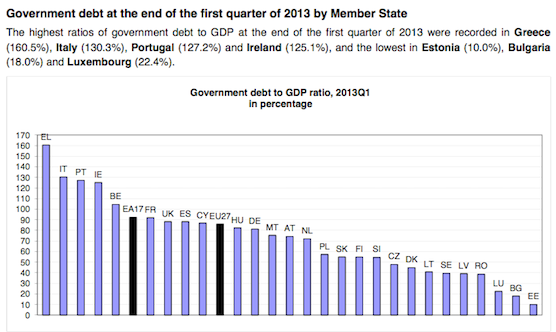

At the end of the first quarter of 2013, the government debt to GDP ratio in the euro area (EA17) stood at 92.2%, compared with 90.6% at the end of the fourth quarter of 2012. In the EU27 the ratio increased from 85.2% to 85.9%. Compared with the first quarter of 2012, the government debt to GDP ratio rose in both the euro area (from 88.2% to 92.2%) and the EU27 (from 83.3% to 85.9%). At the end of the first quarter of 2013, securities other than shares accounted for 77.1% of euro area and for 79.0% of EU27 general government debt. Loans made up 18.4% and 15.9% respectively of government debt. Currency and deposits represented 2.7% of euro area and 3.6% of EU27 government debt.

Due to the involvement of EU governments in financial assistance to certain Member States, and in order to obtain a more complete picture of the evolution of government debt, quarterly data on intergovernmental lending (IGL) is also published. The share of IGL in GDP at the end of the first quarter of 2013 amounted to 2.1% for the euro area and to 1.6% for the EU27

So as you can see , much of the Eurozone periphery continues to be encumbered by unsustainable levels of government sector debt which continues to grow as GDP shrinks. On top of this private sector wealth continues to fall in many nations as the economic slump drives down asset values. The latest house prices from the Netherlands for example.

This latest PMI data does show a broad upturn in economic activity, or at least a slowing of the decline, but as I have discussed previously what is actually required, in the absence of much greater external demand, is larger growth in the periphery while the euro-using creditor nations become greater consumer of goods produced in these regions. The on-going strength of Germany, although good for the Germans, is not good news for the rest of the zone in this regard, and you only have to look at Italy’s situation to realise there are many more hurdles to be overcome before you can call this crisis over:

Italy is heading for an even more severe economic downturn than previously forecast, and will contract by 1.9 percent this year, the country’s central bank said on Wednesday.

In its July bulletin, the Bank of Italy downgraded its 2013 outlook for the country, forecasting a contraction of 1.9 percent, after projecting a 1 percent slump in January. The Italian economy shrunk by 2.4 percent in 2012.

The bank attributed its downgrade to weaker-than-expected economic activity in the first half of the year, following a slowdown in international trade and continued tensions in the credit market.

The move follows a downgrade from credit ratings agency Standard & Poor’s, which earlier this month cut its rating on Italy’s sovereign debt to BBB from BBB-plus, two notches above junk status.

So again, good short terms news, but the underlying macro-level issues remain.

Eurozone Flash PMI report below.

Markit Flash Eurozone PMI July 2013

The big european countries (and most of all germany and france) are pumping up their statistics and most of all their PMIs and “forecasts” to get some how a 0,1% “growth” and the mass media are trying to sell this as very,very good news while the export & retail data show a desaster afterwards.

http://www.flassbeck-economics.de/ifo-in-der-flaute-wieder-keine-bewegung/

The germans dont have any other choice than to insist of “doing fine”.Positive psychology is their last line of defence against a desaster.Actually it is not a big secret that Merkel back in 2008 met with the german media moguls and asked them to hide the truth about the real shape of the german economy and most of all the status of the german banks like deutsche bank and commerzbank which are bankrupt since 2009.

This is no crazy conspiracy theory but an open secret:

http://www.zeit.de/2009/06/Ratlosigkeit/komplettansicht

Who cares about macroeconomics? Isn’t the real plan to keep crushing the population in order to simply declare everyone in default and then just have the banks and the 0.01% take all the assets? Then who will care about the “real” economy?

In other words, extend-and-pretend isn’t just about hiding the banks’ weaknesses; it’s about creating a totalitarian state.

while Japan has done exactly what the empire majority seeking an ever greater share of phantom GDP for entitlements has demanded, declare war on China, again, and increase the number of beds in the ‘shut-in’ rooms to accomodate more zombies.

seems like just yesterday demographics didn’t matter.