I thought readers would have fun taking apart a reply by the Thomas Curry, the Comptroller of the Currency, to some written questions posed by Elizabeth Warren after a July 11 Senate Banking Committee hearing on systemic risk.

In fairness, the letter is a mixed bag rather than a complete train wreck. Curry’s answers to Warren’s questions 3 (on what more might be done to address too big to fail) and 4 (on proposed changes in leverage ratios) are basically earnest defenses of current initiatives, and top bureaucrats have to carry that sort of water. Curry is in the middle of trying to change the culture of a way too bank friendly regulator, and my guess is he does not want to stick his neck too far on policy until he’s made more progress on that front. But his answers to questions on derivatives are cringe-making.

Nevertheless, this letter illustrates the degree to which the OCC relies on rationales that are, or look like, they came straight from the banks.

I’ll just go through the first two questions, although I encourage you to look at the reply to Question 8 (on p. 14) as similarly shred-worthy. 5-7 aren’t so great either.

While the OCC does analyze some risk metrics on an ongoing basis, they rely on VaR, which is widely considered to be a comparatively crude and unsophisticated measurement (it’s useful in combination with other tools, but not as the primary gauge). They look at the level and quality of collateral posted and also track credit derivative exposure on a net basis by counterparty. This great primer by Lisa Pollack tells you why that understates risk. You must read it because it has lovely finance geek-porn like this:

Remember at the top in the first table we said that we had to assume the CDS were “fungible” to net them off against each other like we did?

Well, they are fungible if the credit event is a non-restructuring one, e.g. bankruptcy or failure to pay. But if the credit event is a restructuring then you’re going to have different buckets according to the tenor of the contract.

So the OCC is basically using a few simple and not at all stringent measures of risk to look at derivative risk. Ergo anything it says on this front must be taken with a fistful of salt.

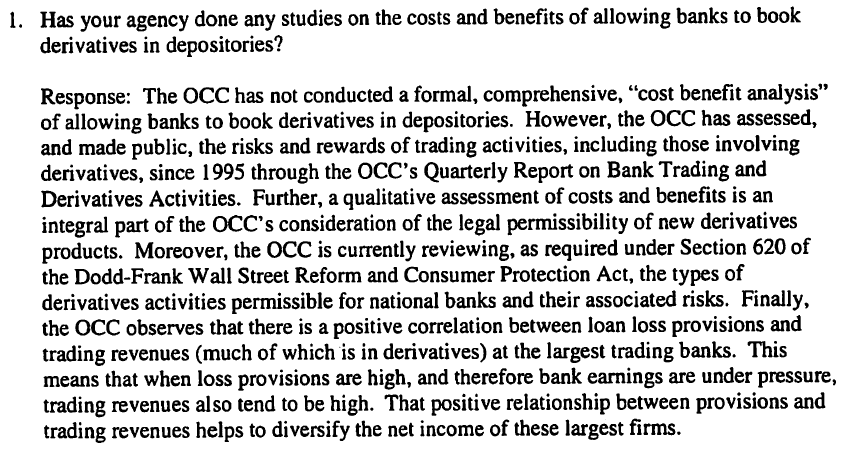

And notice the formulation of the reply. Curry does say, foursquare, that the OCC has not done a cost benefit study but then argues that they monitor the “risks” and rewards, so we should trust that they are on top of things. But his rationale for allowing banks to park derivative exposures is “they increase earnings, since we’ve been measuring them, when banks have needed to make bigger loss reserves.” I’d like to know how true that statement would be if you took September and October 2008 out of the picture, when it took multiple bailouts (the halting of a run on repo via guaranteeing money market funds, the multiple bailouts of AIG that led to its CDS counterparties taking no losses). From a taxpayer standpoint, the case for putting risky derivatives in a depositary to allow banks to make riskier loans (they’d have to be more prudent otherwise in the manner Curry suggests, using derivatives to offset expected loan losses) is weak; it’s basically that these not necessarily socially advantageous activities might help reduce the cost of the socially valuable ones. Plus a correlation is hardly convincing, and since 2012, we’ve seen a move to a “risk on-risk off” trading pattern, which suggests Curry’s correlation may no longer be operative.

To the second question. I found the reply to be remarkable:

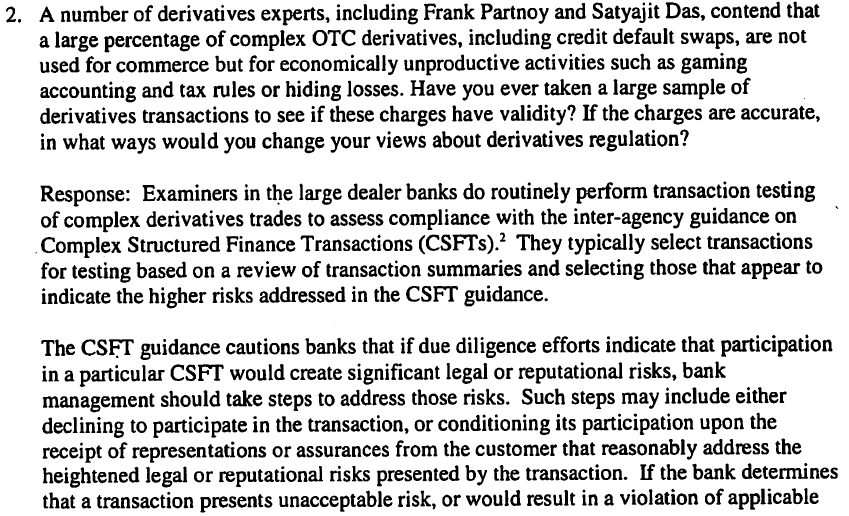

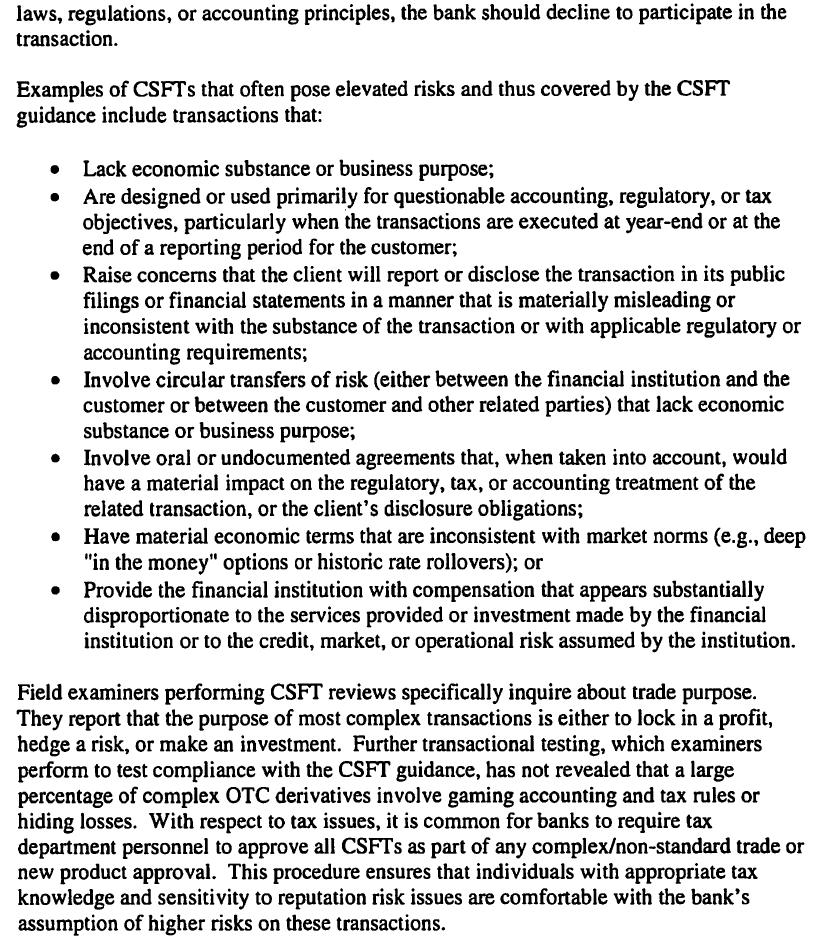

So, shorter: “We have guidelines that tell banks not to take too many risks or do other bad things with derivatives. The banks are supposed to behave, but we also look at a sample of transactions that look sus to us. We ask the banks why they did these trades. They give us good explanations. We also still look at some trades a bit more and we don’t find anything wrong. We don’t do tax, so we make the banks have special tax people look at those transactions to make sure the bank is not doing something so terrible that Matt Taibbi might write about it, assuming he ever could figure it out.”

I asked Satyajit Das for his comment. His reply:

I am flattered to have been mentioned in despatches in Comptroller’s Curry’s response to Senator Warren’s questions about the use of derivatives.

However, I am unable to understand the responses, which in their vagueness surpass even the responses given by derivative/ structured product sales persons to clients. Clearly, regulatory capture extends to linguistics.

As I understand it the Comptroller’s staff asks the bank if they are doing trades for a legitimate reason. The examiners rely on the bank’s own summary and responses. Apparently, if participation in a particular transaction would create significant legal or reputational risks, bank management should take steps to address those risks. Examiners performing reviews specifically inquire about trade purpose and have reported that the purpose of most complex transactions is either to lock in a profit, hedge a risk, or make an investment – extraordinary. Um, what is the definition of hedge and investment? Author Thomas Pynchon would have recognised the position: “If they can get you to ask the wrong questions then the answers don’t matter.”

Sadly, the real questions are simpler but aren’t being asked or answered.

1. Based on surveys conducted by the Bank of International Settlements (BIS), the global derivative market is around US$600 trillion in notional amount. This is a large increase in size from less than US$10 trillion 20 years ago. The outstanding amount compares to a global gross domestic product (GDP) of around US$60 trillion. While this comparison is not ideal, it begs the questions why volumes should be so high? What is the legitimate reason for this activity?

2. Most of the trading is in simple derivatives not complex ones – like interest rate swaps.

3. Proponents argue that derivatives are used principally for hedging and arbitrage. In this way, they perform an economically useful function aiding capital formation and reallocating risk to those willing and better able to bear them. While they can be used for this purpose, derivatives are now used extensively for speculation; that is, manufacturing risk and creating leverage. The UK FSA Turner Report reached this conclusion.

Ultimately, as German Finance Minister Wolfgang Schäuble stated: “If you want to drain the swamp, then you don’t ask the frogs for their opinion”.

I’m embedding the rest of the answers for your delectation. Those of you who are outside the US or have lived or worked abroad be sure to weigh in on Question 8!

OCC's Tom Curry Response to Elizabeth Warren QFRs 7-11-13

typo?

“global gross domestic product (GDP) of around US$60 billion.”

Fixed, not mine for a change, although I did precisely the same sort the other day!

Senator Carter Glass and Congressman Henry B. Steagall had the specific purpose to prevent activities that would present a “moral hazard” in depository institutions. This “strict supervision” of banks led to the longest period of financial stability in American history broken only when the Savings and Loan banks were deregulated.

It’s incredible, in hindsight, that Clinton, Rubin, Summers, Greenspan, Graham, Leach, and, Blyly did what they did to Glass-Steagall knowing what they knew about our financial history.

It’s even harder to believe we are allowing this kink of activity even after the aftermath of September 15, 2008.

I know its a typo, but drop the word “of” and add a “y” to kink and you would be closer to the reality of the situation. My real concern is the prospect of the Clinton Cabal getting another kick at the can in 2016 with Hillary. They were all following orders and were exceedingly well remunerated for their efforts.

I’m not the least surprised. Either the government complies or no more gravy and the banksters crash the economy sooner rather than later.

Banksters have played this game for centuries. They lost control under FDR and it’s taken them all this time to get it back.

In response to OCC’s Curry comment (Warren introduces Lew’s TBTF statement about – “other options”), is anyone else reading this as a parody of Dean Wormer’s “Delta house is on double secret probation”?

Curry’s Testimony & Assurances

1. “Significantly tougher Capital requirements”

2. “Explicit liquidity requirements”

3. “Heightened expectations for corporate governance”

4. “Provisions of Dodd-Frank will fundamentally alter”

a. How and where risk will be transacted

While I am apt to defer to Yves’ perspective about being careful not to attribute too much negativity to Curry here, I seem to remember Dan Kervick recently wrote about the capital requirement not being a panacea.

Can anyone explain why I should not be picturing the ending to Animal House with Kevin Bacon in the middle of chaotic riot saying ” All is fine, everything is fine?”

It will be interesting to see what excuses are offered after the next/nearing derivative collapse for the failure to reign in that monster.

It will be important to take profits early in that collapse, by its middle/end most of these instruments will be banned. As mentioned in the Spring, Puts are once again being given away. The profits from these can be used for social good. My personal goal is to offer “Bounties for Bankers”- rewards to lower level bankers who can turn in higher level, criminal bankers in exchange for cash. Spring Puts returned 80-1, I encourage those with the previous experience and risk tolerance to “Trade for Justice”. use the system against them until the System collapses from their greed.

Sometimes we forget the function of the regulators in the financial industry. We think, merely because Americans like to fantasize about the political economy, that they are there to protect the public from predatory practices and to think that is absurd and naive. They are there to regulate the industry for the industry–to make sure it thrives and survives. The industry survived and thrives, mission accomplished.

The massive fraud that went on, particularly after 9/11 (no accident that) is and should be a matter for local, state and national AGs and the FBI.

I live in Taiwan, and I consider the payment system rather … quaint.

I admit that I’ve never tried to get a Taiwanese credit card, so I don’t know too much about them. There is a local slang word for young women who load up their credit cards to the limit, but they are not considered normal.

They still use chops here, and having your own chop is required for certain types of bank accounts and financial transactions. Since my financial transactions are pretty simple, I haven’t needed to get a chop, though I know an American student who had to get a chop in order to receive her grant money from the Taiwanese government.

Most payments, at least for individuals, are made in cash, either physical currency or ATM fund transfers. Pretty much all of my payments are made this way – even online purchases. I know that this is normal for online shopping in Taiwan (yes, it’s to use physical currency to pay for online purchases), and that credit cards are a less-used payment option.

I remember, when I was on Nangan (an island with about 5000 residents), there was a European who had only 200 NT (that’s short for ‘New Taiwan Dollar’). He needed to buy a ferry ticket to Keelung, which cost 600 NT. The only ATM on Nangan, of course, was a post office ATM, which only serves Taiwanese bank accounts, so he couldn’t access his European bank account. I lent him the money he needed to get the ferry ticket, and I got paid back in Keelung.

When I went to that post office ATM in Nangan – which is a small island about 10 hours away from Taiwan by ferry – the transaction fee was about 0.02 USD.

While I would not say that Taiwan’s payment system for ordinary folk is innovative or ‘ahead’, it does manage to be pretty low-cost.

Too bad there wasn’t some way to help everyone get debt free so that credit cards never need to be used.

At some level, I think that you WANT a fairly crude measure of risk. Because to some degree, the more sophisticated your measure is, the more ways there are to “game” it. And with the ammounts of money that we’re talking about here, you can rest assured that the banks will try to game it to the maximum degree possible.

VaR is the worst possible type of metric for a regulator, because it explicitly leaves out tail risks, and it’s those tail risks that taxpayers eat.

You are assuming the answer is relying on a better single metric. It isn’t. There is no such thing. That’s like trying to look at human health via your temperature only. You’ll catch some things that way, but miss a ton of others.

You need to use multiple metrics, and I don’t mean 3, and they need to be pretty sound ones. The real issue is the desire to use metrics to replace judgment. You can’t. You need metrics to inform judgment.

Thanks Das for the Schaeuble quote. Indeed, Elizabeth Warren should know better than to ask the frogs these questions. It is a waste of time. I’m beginning to think she’s just an actress. And not even a good one.

Much to consider here. Agree with others’ comments regarding the need to reinstate the Glass-Steagall Act.

The Comptroller’s reply to question number one concerning the positive correlation between the banks’ trading revenues from derivatives speculation and the size of their loan loss provisions is particularly baffling to me. This seems both self evident and far from a cause for celebration.

Based on the charts contained in the OCC’s last published quarterly report on derivatives, aggregate total losses from credit derivatives trading since 2007 at the four largest trading banks, also known as “Too Big To Fails”, dwarf their gains from these speculations over that same time period. Based upon their recent historical losses, speculation by national banks in such contracts should be prohibited IMO. I have previously read elsewhere that derivatives counter-parties have super-priority in bankruptcy proceedings of depository institutions. If so, this activity continues to potentially place bank depositors at risk of loss.

Bilateral netting is a fallacy IMO given the interrelationships between large global financial institutions.

Question Number 7 itself should cause any citizen to pause regarding potential abrogation of national sovereignty and effective repudiation of U.S. law by the banks through international trade agreements. The secrecy in which the terms of the TransPacific Partnership trade agreement and the EU-US trade agreement are being negotiated heightens my concerns in this area.

I question the extent to which these large banks are dictating national economic policy through their derivatives exposures.

“.. I have previously read elsewhere that derivatives counter-parties have super-priority in bankruptcy proceedings of depository institutions.”

You had most probably read that here, or on Credit Slips with Adam Levitin or Anna Gelpern. I think the point reared it’s head in the MF Global meltdown.