By Nicole M. Foss, co-editor of The Automatic Earth, where she writes under the name Stoneleigh. She runs the Agri-Energy Producers’ Association of Ontario, where she has focused on farm-based biogas projects and grid connections for renewable energy. While living in the UK she was a Research Fellow at the Oxford Institute for Energy Studies, where she specialized in nuclear safety in Eastern Europe and the Former Soviet Union, and conducted research into electricity policy at the EU level. Originally posted at The Automatic Earth

Countries caught in the grip of financial crisis, with austerity measures compounding their problems, are continually being told to follow Iceland’s example. The assumption is that if a state can disregard the claims of the banking sector, it can address the threat of financial crisis relatively painlessly and get back to ‘normal’ quite quickly. Iceland is held up as an example, but the situation is actually far more complex. As such, it is worth exploring the situation in Iceland in all its complexity. It is an example in some sense, but not necessarily in ways which are transferable. It does, however, illustrate a number of lessons for post-bubble economies, and there will be many of those over the next few years.

Iceland, which achieved independence from Denmark in 1944, was once a relatively poor country of primary producers – fishermen and farmers – but it reinvented itself in the era of globalization under its longest serving Prime Minister, Davíd Oddsson:

It was Oddsson who engineered Iceland’s biggest move since NATO: its 1994 membership in a free-trade zone called the European Economic Area. Oddsson then put in place a comprehensive economic-transformation program that included tax cuts, large-scale privatization, and a big leap into international finance. He deregulated the state-dominated banking sector in the mid-1990s, and in 2001 he changed currency policy to allow the króna to float freely rather than have it fixed against a basket of currencies including the dollar. In 2002 he privatized the banks. When he stepped down as Prime Minister in 2004, he did a stint as Foreign Minister before becoming governor of the central bank in 2005.

The economy expanded and diversified in many ways, attracting ecotourists, moving into new technologies, taking advantage of its abundance of renewable to expand manufacturing and developing a more comprehensive service sector. It became a highly internationalized economy, with the means to import goods from all over the world thanks to a strong currency. With GDP growth running at 4-6% for a number of years, the average family’s wealth increased markedly, with much of it invested in property. As a result, house prices in Iceland saw greater than 10% annual price appreciation from 2003-2007.

The financial sector took off following privatization:

But the principal fuel for Iceland’s boom was finance and, above all, leverage. The country became a giant hedge fund, and once-restrained Icelandic households amassed debts exceeding 220% of disposable income – almost twice the proportion of American consumers.

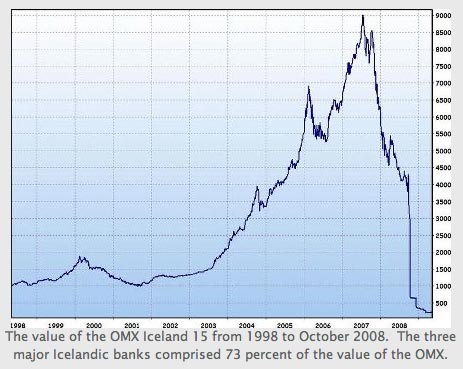

Very large amounts of money were loaned were to the public, allowing them to further bid up the price of property. The fact that many of these loans were denominated in foreign currency (Japanese yen, Swiss francs etc) added currency risk to the resulting speculative mania. Three large banks – Glitnir, Landsbanki and Kaupthing – grew to dwarf the size of the island’s real economy in a financial bubble of unprecedented size (in comparison with a host economy based on only 320,000 people). Total debt to GDP peaked at over 1200%, reflecting the grossly disproportionate nature of the financial sector. This had been a cause for concern at the central bank as far back as 2005, but nothing was done to reign in credit expansion. At the peak of this period of great affluence, the Icelandic population was lauded as the richest people in the world, but it was not to last:

A visitor seeking a sense of how Iceland’s clique of powerful financiers saw themselves before their empire came tumbling down need look no further than Reykjavik’s Harpa concert hall. The extravagant steel and glass structure, which has more seats than London’s Royal Opera House, looks like a futuristic beehive glowing above the grey buildings that make up most of the capital. It was commissioned by Bjorgolfur Gudmundsson, one of the “Icelandic oligarchs” who exploited cheap credit following the aggressive financial deregulation of the early 2000s to create a billion-dollar empire. He set out in 2007 to build a cultural venue to match the country’s new found wealth – but when the global financial crisis hit the next year, and Iceland’s over-leveraged banks collapsed, he went bankrupt, leaving the state to complete the project.

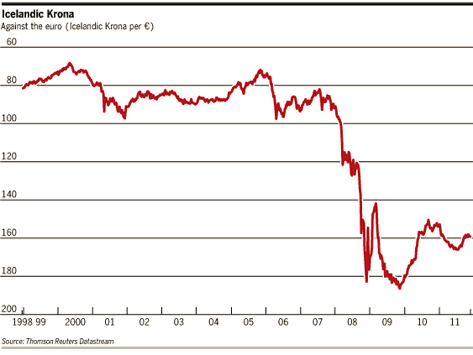

The structural instabilities upon which the illusion of prosperity was based proved fatal in late 2008. Maturity mismatching (issuing short-term debt in order to invest in long term assets) was rife, requiring that short term liabilities be continually rolled over until long term assets matured. Reserve requirements were reduced, increasing the money multiplier. The huge increase in the effective money supply, much of the credit denominated in foreign currencies, combined with a 35% fall in the value of the Icelandic króna relative to the euro, led to substantial price increases – 14% in the year before the system reached its limit. As mortgage principle is typically indexed to CPI in Iceland, this price inflation was compounding the effect of a housing bubble.

The central bank had been attempting to reign in ‘price inflation’ by maintaining interest rates much higher than those in neighbouring jurisdictions. This encouraged overseas investors to hold deposits in Icelandic krónur, leading to an even greater money supply expansion relative to GDP. During the expansion years the stock market made record gains, increasing by a factor of nine between 2001-2007, or a 44% average annual increase for six years in a row. The profitability of the speculative financial sector was so much greater than that of the real economy that resources inexorably shifted away from traditional marine industries towards banking and finance, leading to a great misallocation of capital.

It was clear, to anyone who cared to look, months before the final curtain fell, that Iceland was in a huge bubble and that the over-extended banks were going to fail. We drew readers’ attention to the problems early in 2008, with Fire and Iceland. Icelanders’ status as the richest people in the world was a temporary artifact of the bubble – simply a result of borrowing the most money and therefore temporarily having the most financial freedom to consume. Household debt had reached 213% of disposable income, leaving people highly over-stretched. Real wealth is not built on pathological over-borrowing, but illusory wealth can appear real enough for a time. It can certainly shape people’s perceptions as to what they consider a normal, and deserved, state of affairs.

The country hit a financial brick wall in the fall of 2008, when Iceland’s banks ran into difficulties rolling over the large amount of short term debt, provoking a liquidity crisis. British and Dutch depositors in Landsbanki’s high-yielding internet banking subsidiary, Icesave, also lost confidence and began to withdraw deposits. Unable to call on the central bank as lender of last resort, due to the disproportionate size of the banks in comparison with the $13 billion local economy, all three banks were placed into receivership, defaulting on some $85 billion.

Domestic deposits were guaranteed in full, but overseas internet banking deposits were not protected. These were bailed out by the depositors’ own countries (Britain and the Netherlands), which then attempted to recover the cost from Icelandic taxpayers. The government would have been prepared to sanction this, but by referendum the people overwhelmingly declined to accept public responsibility for the private debts of the banking system. The considerable international pressure to do so, including the freezing of £4 billion of Icelandic assets under anti-terrorism legislation in Britain (Sections 4 and 14 and Schedule 3 of the Anti-terrorism, Crime and Security Act 2001) only made the Icelanders more determined.

The immediate consequences for the Icelandic economy were severe. The banks had accounted for almost three quarters of the value of the Icelandic stock exchange, and with these shares set to zero, and the contingent contagion, the market capitalization of the index plummeted by over 90% (relative to the 18 July 2007 peak). The economy promptly went into recession, with GDP contracting significantly in real terms. Unemployment more than tripled, albeit from a low level, and many workers had either their pay or working hours reduced. The króna fell sharply, raising the cost of imported goods upon which the country had become dependent. The burden of the large amount of debt denominated in foreign currencies, or indexed to CPI, rose enormously. In the following two years the economy would go on to contract by some 10%. After four years, people were still facing a approximately a 25% loss in earnings, while attempting to manage debts which had doubled.

Capital Controls:

Iceland became the first industrial country since Britain in 1976 to receive an IMF loan, with additional funds provided by other nordic countries. The loans came with strings attached in the form of capital controls to support the currency. A free-floating exchange rate had become far too much of a liability:

For countries with a minor-league currency (every currency except for the US dollar, the euro and the yen), an open capital account will always be a mixed blessing. The joys of an open capital account – the undoubted benefits from decoupling domestic capital formation from national saving and from unrestricted international portfolio diversification and risk trading – cannot be enjoyed without the pain; the risk of its domestic financial institutions, capital markets, non-financial enterprises, consumers and public finances becoming the flotsam and jetsam on massive and mindless killer waves propelled by an out-of-control global financial storm.

Capital controls are an imperfect stop-gap measure to take pressure off the currency, slow the speed of a financial crisis by damping down extreme fluctuations, and allow attention to be focused on stabilizing the economy. However, they distort relative values in a non-transparent way, undermining trust in an economy through the maintenance of an artificial exchange rate. This can lead to a risk premium being imposed on loans and investments. They generate incentives to circumvent them, and over time the political control, and potential for favouritism, that they create can lead to corruption, or the perception of corruption. Hence they are intended to be temporary. Once in place it can be very difficult to remove them without experiencing a renewed crisis of confidence, but while they endure they create on going economic dislocations that can have significant effects on the real economy:

In an interview on the news program Spegillinn on RÚV’s radio station Rás 2 yesterday, CEO of CCP Hilmar Veigar Pétursson talked about how the currency restrictions, or capital controls, are obstructing his company. CCP’s employees in Iceland who get paid in foreign currency can neither withdraw their money in foreign currency nor transfer it to foreign accounts, he explained. The company itself is barred from trading with a foreign bank because of the currency restrictions, he added, Icelandic banks are too small for such a large company—but they shouldn’t be any larger. When asked whether this means CCP will relocate its headquarters, Pétursson replied, “Let’s hope for the best.” The currency restrictions should have been lifted by now, according to schedule, and hopefully it will happen in the near future, he added.

Capital controls were originally mandated until August 2012, but the central bank, in its spring 2012 Capital Account Liberalisation Strategy report, recommended that they remain in place until 2015. Controls were in fact tightened at that time, as foreign investors had been circumventing them while the country was still vulnerable to a liquidity crisis:

The strengthening is mainly in the form of including certain payments from the receiverships of the old banks. Repayments of bonds in the ownership of foreigners are also included. It doesn’t matter if the bonds are issued by private or public enterprises. Recently, foreigners have been moving into the bonds on the short end of the maturity, waiting to be able to get repaid in order to get their funds out of the country. Also, since there is a difference of the value of the Icelandic krona is 30-40% (or thereabouts) between the Icelandic currency market and outside it, there is a massive incentive to buy krona outside the economy, bring it to Iceland, buy bonds with short maturity, wait for the day of repayment and get paid according to the exchange rate in Iceland. One has to make hefty losses for the gamble not to be profitable.

Other forms of circumvention are more difficult to prevent. It is unclear, for instance, the extent to which exporters chose not to repatriate their foreign exchange earnings. Others may purchase expensive, yet small and portable, items at home and resell them abroad in order to obtain foreign currency. A form of ‘arms race’ can develop, with a downward spiral of new regulations and innovative ways round them. That way typically lies corruption. Ultimately, capital controls undermine confidence in a currency to its long term detriment, hence the view that they should be removed as soon as practicable.

Capital controls can become addictive for governments, however. With the possibility of investment overseas removed, investors, including pension funds, must look for opportunities at home where choices are very limited. Their consequent purchase of government bonds allows the government to finance its budget deficit, reducing pressure to cut deficit spending. Real estate investments made as one of a limited range of options provide artificial price support to the housing market, maintaining the illusion of greater value than would normally exist, both for the property itself and for the loan used to purchase it, reducing write-downs of what might otherwise be bad debt. Support for the property market also amounts to support for property tax revenues, again strengthening the government’s position. Removing these measures subsequently can be very risky, as relative values can adjust quickly to the downside when allowed to do so, and government revenues could be hard hit in a short space of time.

When capital controls were imposed in Iceland in the 1930s, they were not removed until 1993 – an indication of just how difficult it can be to back away from this type of policy response. The reality on the ground in Iceland is a major curtailment of freedom for both companies and individuals. Almost all currency transactions require explicit permission from the central bank. Firms seeking to invest abroad require permission to do so, and this is rarely granted. Individuals are not allowed to invest abroad at all. They require permission from the central bank for foreign travel, as access to foreign currency is very tightly controlled. The purchase of foreign currency within Iceland is restricted, and Icelanders are required to deposit any new foreign currency they received with an Icelandic bank. There is a strict limit of €2,150 on cash for foreign travel, with citizens expected to convert anything left over back into krónur on their return. Icelanders are only limitedly permitted to support relatives studying abroad. Those who might wish to emigrate would not have the freedom to bring their assets with them.

Currency Options and Sovereignty:

The concern is that with capital controls in place, there is no real way to increase investment, and without investment unemployment will remain high and disposable income low. It has been suggested that one way out of this dilemma would be for Iceland to give up the króna in favour of another currency. As a very small currency with relatively few users, the króna was always volatile. This complicates life for businesses by reducing economic visibility. The increased risk translates into higher interest rates, burdening the economy. However, adopting another currency would come at a high price in terms of loss of sovereignty and loss of any control over monetary policy. The alternative of introducing a currency board and pegging the króna to another currency at a fixed exchange rate would be possible, but currency pegs tend not to fare well in periods of instability, as they provide a tempting target for speculative attack.

In the immediate aftermath of the crisis, Iceland considered joining the European Union and adopting the euro, on the grounds that this would lower interest rates, increase capital investment, labour productivity and trade, as well as possibly lowering prices (due to the ability to directly compare prices with European countries). Joining the EU would come with consequences in the form of loss of control over fishing rights – a very sensitive issue in Iceland – hence there were discussions about the possibility of adopting the single currency without joining the EU. However, since then the eurozone has experienced its own structural problems, dampening enthusiasm for Iceland to join that sphere of influence.

Other possibilities noted were for Iceland to join either the Norwegian or Canadian currencies. The latter option, somewhat surprisingly, appears to have achieved some serious consideration. Arguments in favour of adopting the Canadian dollar include stability, liquidity, similar business cycles between resource exporting countries and ‘Arctic sovereignty’ (increasing clout on the Arctic Council). Part of the attraction arises from historical connections between the two countries:

In a 45-year period from 1870 to 1914, up to a quarter of the Icelandic population moved to North America, most of them going to Canada, where they founded “New Iceland” on the shores of Lake Winnipeg in 1875, as an independent state. In 1887 this colony joined Manitoba and the capital of New Iceland, Gimli, retains strong connections to Iceland. The diaspora in Canada is called West-Icelanders.

However, abandoning the króna would come at a price:

“The Bank of Canada and the embassy declined to comment, but the Canadian official says, “I think they only heard what they wanted to hear.” If Iceland ditched its currency, it wouldn’t have control over monetary policy to boost the economy, leaving layoffs as the primary way to deal with downturns. That’s tricky in Iceland. “It’s a very closed, tight-knit system,” says the official. “Everybody is somebody’s second cousin.” The devalued króna is also a key reason the country is crawling out of its hole: exports, predominately fish, are cheap.”

Restructuring and ‘Recovery’:

In the aftermath of the banking collapse, the three failed banks were divided into old and new components. The new banks serving the domestic market were recapitalized, at a cost of some 25% of GDP, and granted the guaranteed domestic deposit base. Two are now owned by their foreign creditors, while the Icelandic state holds majority ownership of the third. Within the country, banking services continued uninterrupted. The old banks were left primarily with estates composed of distressed assets and the foreign debts destined for liquidation.

Iceland was sued in the European Free trade Association court (E-16/11, EFTA Surveillance Authority v. Iceland) by the governments of the United Kingdom and the Netherlands over its default on the Icesave deposits, leaving the country in a state of uncertain limbo over the level of government debt. If the case had gone against the country, between 6-13% of GDP would have been added overnight (some 335 billion krónur in principle and interest according to IMF estimates). However, in early 2013 the court ruled in Iceland’s favour, setting an important precedent that governments in the European Economic Area (EEA) are not liable to cover the cross-border depositor guarantee obligations of their banks. This is seen as a factor favouring currency stability, and, as such, an foundational element for the eventual removal of capital controls. It also means Icelanders can be spared some of the crippling austerity measures already imposed, and still to come, in countries that did offer a public guarantee for private banking debt.

In 2010 the government declared foreign-currency-indexed mortgages to be illegal, as the crash of the króna had caused the value of these loans to skyrocket, often to far beyond what people were capable of paying. Government also facilitated the write down of a portion of mortgage debt, but only to 110% of property value, meaning that the large number of people in negative equity did not fall, but the extent of their indebtedness was reduced. Foreign currency indexed loans had been attractive to many as the interest rate on these was lower than on króna-denominated mortgages, but after indexed mortgages were banned, banks retroactively set interest rates higher from the beginning of the loan, claiming back payments for the difference. This is being challenged in the courts. In the meantime, the household debt burden remained stubbornly high – 270% of disposable income by the end of 2010 (compared to 217% prior to the banking collapse). Indexing to CPI has been upheld by the Supreme Court, meaning that rising prices are greatly diminishing the effect of debt relief.

Iceland’s three year IMF programme came to an end in August 2011, with 3% growth for the year as a whole. In early 2012 its government bonds were promoted back to investment grade by the ratings agencies, albeit on the lowest rung of the ladder (BBB-minus up from BB-plus). June saw a return to the international capital markets, with a US$1 billion 10-year bond offering at 5%. This was used for early repayment of emergency loans of $483.7 million from the IMF and €674 million to Nordic nations, for loans maturing between 2013 and 2018. With growth accelerating, Iceland plans further early repayments.

The country has proven to be an interesting test case for a set of policy options opposite to those employed in the struggling periphery of the eurozone. Rather than bailing out the banks and imposing austerity to the extent that the European periphery did, Iceland has attempted to protect its welfare state during the period of crisis. The agreement with the IMF involved postponing cuts for a year, then imposing both tax increases (corporation tax increased to 18% from 12%, increased income tax and VAT and also a wealth tax) and spending cuts simultaneously, rather than favouring primarily spending cuts as was done in countries like Ireland.

Cuts there have been, and these, as always, have hit the poor the hardest. The pension system has been raided and healthcare provision has been scaled back, with sharply increased co-payments required. However, public systems in Iceland still function enviably well in comparison with many parts of the world. Targeted household debt relief, even as limitedly practiced in Iceland, mitigated the impact that debt overhang, and consequent household deleveraging, would otherwise have had on aggregate demand. This helped to keep unemployment relatively low by international comparison. The IMF is now considering the experience in formulating its plans.

The effect of a currency devaluation on exports has been very significant. Because exports constitute 59% of GDP, and they are now very competitively priced, employment in exporting industries, notably fishing, has received considerable support:

“This is probably one of our best years,” said Arnthor Einarsson, a fisherman readying his boat for his next catch as seagulls circle huge piles of fishing nets on a rocky peninsula about one hour south of the capital Reykjavik.

Only a few years ago, a banking boom in which the sector’s assets grew to 10 times the country’s GDP lured many of Iceland’s 320,000 population from traditional industries into the world of finance, where returns to speculation were far higher than returns in the real economy. Fisherman got into banking and sailors speculated on booming real estate. Those heady days have gone. Gas-guzzling Land Rovers have been replaced with fuel-efficient Volkswagens, a sign perhaps of a more sober consumer mood in which economic growth is based on a steady expansion of exports rather than flash-in-the-pan speculation.

Despite the higher expenses for equipment and fuel, which must be paid in foreign currency, the sharply falling cost of labour makes the business far more attractive:

Before the currency collapse, an Icelandic fish plant on average paid workers the equivalent of nearly €20 an hour, said Sigurgeir Kristgeirsson, chief executive of VSV, one of Vestmannaeyjar’s two big fishing companies. “Now it is close to 10 euros an hour,” Mr. Kristgeirsson said, over a dinner of garlicky langoustines and immaculately white cod. “That is a driving force of our profit line.”

It is also driving jobs. VSV now employs 365 people, up from 276 in 2010, a big jump for a town of 4,200 people. Plant workers earn around €10 an hour, but fishermen, who earn a percentage of the catch, do far better: the equivalent of €60,000 a year or more for a deckhand. One captain in VSV’s fleet made €243,000 last year.

Healthier corporate profits mean more investment. Mr. Palsson, who started working langoustines at age 10, opened the Godthaab i Nof fish plant with four partners a decade ago. In 2005, when the krona was at its peak, it lost money every month, he said. “From that time to 2008, nobody wanted to work fish,” he said. Now that money is rolling in, he and his partners have invested 220 million kronur, nearly $2 million, to take over a failing plant at the edge of town that dries heads and bones for shipment to Nigeria, where they are used for soup.

Now in 2013, optimism abounds, in Iceland as in many other places. There is a widespread sense of relief, stemming from the perception that the global financial crisis is over and recovery is underway. Looking beneath the surface though yields a different picture. Perceptions are not always realistic or correct, and an optimistic gloss can be covering up a more troubling set of fundaments:

Today, a visitor to Reykjavik would have no idea this happened. Range Rovers, which became a popular status symbol, still bulldoze their way through the narrow streets. A sparkling performing arts centre under construction when the crisis hit opened this summer to rave reviews in the international press. And though McDonald’s abandonment of Iceland in 2009 was mildly humiliating, a local fast-food chain moved right in to its three locations….

….But calling this a recovery might get you branded by Icelanders as “very 2007,” a term coined after the crash to describe an overly optimistic view or something ostentatious, like those Range Rovers. Look closely at Reykjavik, and you’ll see a gleaming office tower completed when the banks imploded is half empty. A local economist estimates the country has the highest office vacancy rate outside of Ireland….

….While the country dredges up the past to seek closure, it also has to think about how to fill the void once assumed by the banking industry. It became a huge presence starting around 2003, paying fat salaries and providing a reason for the young, educated workforce not to go abroad. For now, Iceland has returned to its roots: fishing and aluminium production.

It has been a sobering experience:

“Did Icelanders have an identity crisis? Yes,” said Egill Helgason, one of Iceland’s best-known television commentators. “They thought they were financial wizards, but it was all an illusion … Now it’s back to books, music, and well, fish.”

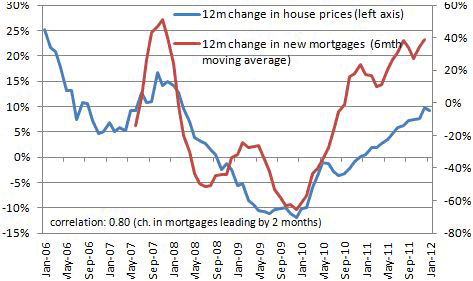

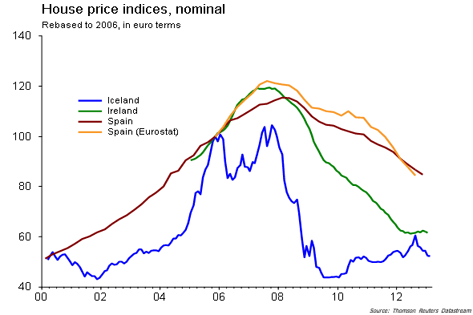

The fundamental reason for the surge in house prices in Iceland is not the economic recovery but the expansion of new mortgages, i.e. debt. Those new mortgages spur the economic growth since the debt creation becomes somebody’s income (first the seller’s and then who ever gets the money from him as he spends it). In the meanwhile, investment is lagging and furthermore, 60,000 households (40% of the total, year end 2010) are in negative equity on their balance sheet. None of those 60,000 households are thinking of speculating in the property market in at the moment, I presume, since they are busy paying down their debts.

The speculators are more likely to be high net-financial-wealth holders, looking for income and yield on their financial assets. The nominal yield on the rental market is around 7-9%, depending on which part of Reykjavik we’re talking about. Unindexed mortgages carry 5-7% interest rates. If you have the net-cash to cover the need for equity, leveraging it up with a mortgage only “makes sense”.The money that is spurring the growth of the Icelandic economy is therefore not coming from investment in capital assets and the subsequent production of goods and services, but speculation with properties.

Newly created mortgages are driving the property market in Iceland, as they do in other countries. The resulting income from debt-creation is what is then spurring economic growth, but not investment in real capital.

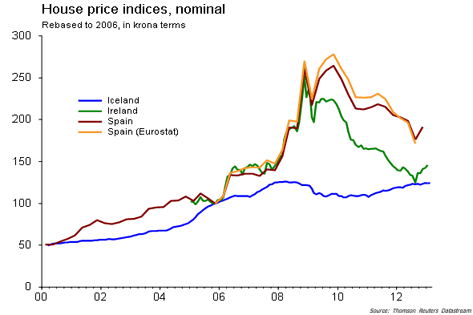

The so-called ‘Icelandic miracle’ recovery is not quite so simple. Creating a new debt ponzi scheme does not constitute a sustainable basis for recovery. The consequence of taking that path – another round of painful future losses – is quite predictable. This time a larger percentage of those losses are going to be felt domestically, given the indebtedness of the population and the extent of negative equity. A housing bubble collapse will affect people far more personally and immediately than a banking collapse where the losses were largely borne by foreigners.

In terms of international purchasing power, Icelanders are very much poorer than they were, due to the collapse of the króna. For instance, the housing prices that show such a strong rebound denominated in króna look very different in euros. The large devaluation (an option not available to struggling eurozone countries) has made labour and exports more competitive. Combined with allowing the banks to fail (with the majority of the losses taken by foreigners), rather than bailing them out at public expense, it has allowed Iceland to stem what could otherwise have been a fatal financial hemorrhage. Given that people judge their situation in terms of nominal wages in local currency, rather than in relation to global purchasing power, the situation is perceived differently than in the troubled countries of the eurozone, and therefore the consequences are different. There banks were bailed out by the taxpayer, leading to government debt. A currency devaluation to boost competitiveness is not possible under the single currency. The resulting ‘internal devaluation’ through austerity is far more painful and far less politically acceptable than Iceland’s “money illusion”.

Calling to Account:

During the months following the banking collapse, there was public rage at the handling of the crisis. The Kitchenware Revolution, so-called because of the banging of pots and pans by thousands of protestors outside the Alþingi (parliament), disrupted governance. In a city with a population of 120,000 people, some protests attracted 10,000 demonstrators. The government of Prime Minister Geir Haarde and his Independence Party was forced to resign in January 2009, more than two years before the end of his electoral mandate. The task of navigating the aftermath of crisis fell to his successor, Social Democrat Jóhanna Sigurðardóttir.

In 2012, Haarde was acquitted by the specially convened Landsdómur criminal court of impeachments in Reykjavik of gross negligence, of failure to prevent the contagion from spreading to the internationally, by not insisting that Icelandic banks ringfence their overseas operations and of failing to act upon the government’s 2006 report on financial stability. He was, however, convicted of failing to keep his cabinet informed of major developments during the 2008 crisis period. Haarde was the first individual to stand trial at the 15-judge court, created in 1905 to hear any charges brought against ministers on matters of accountability. The court set no punishment and allowed for his legal expenses to be covered, in a judgment reflecting a common view that one person should not shoulder the blame for a systemic failure:

Vilhjalmur Arnason, a philosophy professor at Iceland University who worked on the [Special Investigation Commission Report], described the exercise as “very important for reasons of justice and for reconciliation” in a society traumatized by a crash so severe that it threatened to capsize the country. But, he added, bankers alone were not responsible, as “the whole society was so intoxicated” by values that put profit ahead of morality, the law and even common sense…..

….”There is cohesive guilt, because only so much anger can be directed at the bankers,” he said. “It’s like looking in the mirror and asking ‘did I do that’? It comes back to haunt us.”

Other convictions have been obtained, but sentences are typically very short. More than 120 people are under investigation for possible financial crimes, with over a hundred cases opened, and the special prosecutor’s office has grown from five staff to over a hundred investigators, lawyers and financial experts. Most recently, tougher sentences were handed down to four former executives of Kaupthing, who had been accused of concealing that a Qatari Sheikh had purchased a 5.1% stake in the bank with money illegally lent by the bank itself. Among the four are Hreidar Mar Sigurdsson, former chief executive, and Sigurdur Einarsson, former chairman of the board, who received the longest sentences for financial fraud to date (five and a half years and five years respectively). The other two received sentences of three years and three and half years. Their legal costs alone will run into millions of dollars. Another case against Kaupthing is pending.

An indictment has also been issued against corporate raider, and arguable the principle architect of the ponzi banking expansion, Jón Ásgeir Jóhannesson (click for short video documentary).

Prosecuting financial crime is a significant challenge, especially in a small country where almost everyone in Reykjavik has personal connections with people in banking and finance. The first advertisement for the job of special prosecutor received no applicants, and in a second round an outsider with no personal connections in the capital had to be urged to apply. The process is slow and results do not reflect how seriously the public views the offences committed, leading to considerable frustration in a country which holds bankers in lower esteem than drug dealers:

As chief of police in a tiny fishing town for 11 years, Olafur Hauksson developed what he thought was a basic understanding of the criminal mind. The typical lawbreaker, he said, recalling his many encounters with small-time criminals, “clearly knows that he crossed the line” and generally sees “the difference between right and wrong.” Today, the burly, 48-year-old former policeman is struggling with a very different sort of suspect. Reassigned to Reykjavik, the Icelandic capital, to lead what has become one of the world’s most sweeping investigation into the bankers whose actions contributed to the global financial crisis in 2008, Mr. Hauksson now faces suspects who “are not aware of when they crossed the line” and “defend their actions every step of the way.”….

….Mr. Hauksson said he was frustrated by the slow pace but thought it vital that his office scrupulously follow legal procedure. “Revenge is not something we want as our main driver in this process. Our work must be proper today and be seen as proper in the future,” he said. Part of the difficulty in prosecuting bankers, he said, is that the law is often unclear on what constitutes a criminal offence in high finance. “Greed is not a crime,” he noted. “But the question is: where does greed lead?”

Mr. Hauksson said it was often easy to show that bankers violated their own internal rules for lending and other activities, but “as in all cases involving theft or fraud, the most difficult thing is proving intent.” And there are the bankers themselves. Those who have been brought in for questioning often bristle at being asked to account for their actions. “They are not used to being questioned. These people are not used to finding themselves in this situation,” Mr. Hauksson said. They also hire expensive lawyers.

As for the fortunes of the Icelandic oligarchs, it is not clear at all that bankers are generally being held to account in a meaningful way for the consequences of their actions:

Thor Bjorgolfsson was part-owner of Landsbanki, the island’s second-biggest lender by assets until its collapse in 2008. He was also Iceland’s first billionaire and its richest man. He lives in a multimillion-pound house in west London with his wife and three children and still owns a private jet, although it is up for sale. He refuses to disclose his current wealth. Mr Bjorgolfsson still leads Novator Partners, a London-based investment firm, sits on several boards and holds shares in companies including Actavis, a Swiss drugmaker, and CCP, an Icelandic computer games company. His representative says any dividends from his shares, or future gains from their sale, will go towards settling debts to creditors following Landsbanki’s decline…

….Perhaps the most famous “Viking raider” is Jon Asgeir Johannesson, who bought chunks of the UK high street through Baugur, his investment company. He owned stakes in groups such as toy store Hamleys, House of Fraser department stores, Iceland Foods supermarkets and fashion retailer Oasis. Mr Johannesson now estimates his own wealth to be about $2m, down from more than $1bn before the crisis. He is being sued by Glitnir, the third-biggest lender until its 2008 collapse, in which he was the biggest shareholder. The bank lent him much of the cash for his acquisitions. But in a recent interview with Bloomberg, he said he was planning to return to the UK and build a “little kingdom” once his legal troubles subside.

Politics and Constitution Building

In the run up to 2008, the Independence Party had dominated Icelandic politics for nearly twenty years. Following the resignation of the Haarde government in January 2009, a ruling coalition between the Social Democratic Alliance, the Left-Green Movement, the Progressive Party and the Liberal Party was asked to form a government, under the leadership of Jóhanna Sigurðardóttir, Iceland’s longest serving member of parliament. The coalition was then formally elected in April, with a parliamentary majority. The first issue was discussion of the repayment of $5.3 billion in losses from the Icesave debacle. The government’s position was put to a national referendum was rejected by over 90% of the population. A second agreement with foreign creditors was made, but the president, Ólafur Ragnar Grímsson, refused to sign it, and it too failed on referendum.

The coalition sought to involve the population, which had been extensively demonstrating and lobbying for a substantial change of governance, in the process of creating a new constitution. Between the government and a citizens’ group referred to as ‘the Anthill’, a National Forum was organized in late 2009, with 1500 people invited to participate in the assembly, the majority of whom were chosen at random from the national population registry. The Forum, convened in mid 2010, proceeded, with much public involvement, to elect twenty-five members to a constitutional council. The constitution-writing process was conducted entirely in public, with a global observation and commenting involvement in a form of social-media-based crowd-sourcing model. The process was not without its critics.

The draft, comprised of 114 articles divided into 9 chapters, was presented to the Al?ingi in mid 2011, with a strong emphasis on open government, transparency and accountability, and also public ownership of natural resources. A one-person-one-vote system was to be introduced, which would effectively reduce the power of the rural vote, and with it the influence of the powerful fishing vessel owners. The parliament voted in favour of putting the new constitution to a national referendum, which approved the document, albeit with a low turnout among voters. This low turnout allowed opponents of constitutional reform to question the legitimacy of the vote.

Changes to the constitution are required to be passed by two successive parliaments either side of an election, hence the coalition introduced it in the spring of 2013. Political opposition in the Alþingi was considerable, particularly among the political allies of well connected and traditionally favoured special interest groups, notably the fishing vessel owners, whose power rested on the previous allocation, by high-placed friends, of fishing quota on highly advantageous terms. Constitutionally protected public ownership of natural resources threatened this power base. Parliamentary manoeuvres were conducted in order to thwart passage of the bill, with one pro-constitution member of parliament comparing trying to make progress in parliament to “trying to file her income tax return with monkeys at the kitchen table”. A successful filibuster by the opposition parties prevented the passage of the bill prior to the election in April 2013. Jóhanna Sigurðardóttir called the day the constitution bill died as her saddest day in parliament in thirty-five years.

The government had reason to be concerned about their fortunes in the run up to the April election. The previous October had seen street protests, in an echo of the movement that had forced the previous government to resign. The people were dissatisfied that their lives remained heavily impacted by the crisis, blaming the government for a litany of failures, including prioritizing the IMF over the welfare of the population. Some dissident parliamentarians from the Left-Green party denounced the actions of their own ruling coalition as being incompatible with their founding principles, and others left the party altogether.

The coalition was soundly defeated in the largest reversal by any government since Icelandic independence in 1944, losing half their seats in the Al?ingi. The Independence Party, in coalition with the Progressives, were elected with a small majority, and Progressive Party leader Sigmundur Davíð Gunnlaugsson is the new Prime Minister. Debt relief was promptly organized for fishing quota owners, and multinational owners of aluminium smelters are hopeful that environmental controls on geothermal power developments will be eased. As the old power structures are revived, crony capitalism appears poised to make a return, with economic and environmental priorities in conflict:

We now have three aluminium smelters in Iceland belonging to multinational corporations. They get power at a fraction of the rate that regular citizens of this country have to pay. That includes greenhouse farmers, who nevertheless are trying hard to maintain some level of sustainability in this country. The vast majority of the wealth generated by smelters is exported abroad, of course. And heavy industry wreaks havoc on our nature. The previous government, with the Left-Greens in the Environment Ministry, did a very good job of protecting many areas that were pegged for power harnessing. Now that the IP/PP are back, all that looks likely to change. Indeed, Century Aluminum, which is just jonesing to start up a new smelter on the Reykjanes peninsula, said last week that they are putting a lot of hope in the new government. Incidentally, the power for that smelter doesn’t exist, which means boreholes all over Reykjanes as they try to harness steam to power it. And it would not surprise me if the new government tried to kick-start the economy by attracting yet another smelter.

Fringe parties and protest groups attracted serious attention. The Pirate Party (described as “a disparate group of hackers, anarchists and digital rights campaigners”) actually won three (out of sixty-three) parliamentary seats:

The Pirate Party was built in Sweden in 2006 by hackers and freespeech activists hoping to fight the flood of online censorship bills being enacted in the name of preventing “piracy”. It is now a global movement, with branches in 60 countries and 250 elected representatives, including two members of the European Parliament. Its demographic is young, educated and precariously employed, mostly in programming, with a taste for lots of black clothing. “I’m a Pirate in my heart,” says Jón Thór Ólafsson, 36, one of the movement’s leading candidates. “The Pirates are for freedom and direct democracy. That means that people have the right to participate in decisions that affect them. It changes the rules of the game, and those who have been benefiting from playing the game aren’t very happy about changing the rules.

The constitution is effectively dead. The electoral platform of the new coalition rested on “correcting household debt burdens” through mortgage debt relief. This promise was made doubly popular by the Prime Minister’s pledge to provide this debt relief from frozen foreign investments, despite the longer term threat this may pose to the króna if capital controls are ever to be lifted. While they remain in place, investment will be limited, and companies and skilled professionals will continue to leave the country. (Two percent of the population has already emigrated, and many more are considering doing so.)

The longer term considerations matter less, however, than the short term popularity of debt relief. 150 billion krónur is to be eliminated, through a combination of outright cancellation (80 billion krónur) and allowing, and incentivizing, people to use their tax-free pension savings to pay down household debt (70 billion krónur). The measures will be paid for through taxation of the estates of the old banks, in other words with foreign funds trapped behind capital controls. Short term impact is all that can be expected from debt relief under circumstances where mortgage debt continues to be indexed to CPI, and CPI is continuing to rise on economic and currency weakness. For the time being the ponzi scheme continues, after being bought a little more time with other people’s money. A concern is that current debt relief could encourage further debt expansion down the line, in the expectation that it too will be written down.

Clearly the previous coalition had failed to meet public expectations, but those expectations were patently unrealistic:

Iceland’s response to the financial crisis has been taken as a model for how a country should react to a dramatic economic shock. However, international observers should also take note of our country’s recent election result. Despite guiding the country through a difficult but impressive recovery, the governing parties were ousted. The parties that were blamed for the financial crisis won a slim majority. This raises a fundamental question: in our age of austerity and slower growth, can politicians maintain popularity without the proceeds of a bubble economy? Put differently: can any politician meet the unrealistic expectations of Europe’s voters?

Unfortunately the problem was that there were no solutions that could have avoided the pain people continue to face, no matter who was in power, and any government trying to do anything under circumstances of inflated expectations, copious spending priorities and very little money is going to upset almost everyone. When anger and fear are in control, and the there are inevitably going to be far more losers than winners, whatever one does tends to be seen in a negative light, even if it was the best possible action under the circumstances. Nothing within the scope of what is actually possible looks like success to anyone.

Periods of contraction consume the politicians who attempt to lead through them, and who therefore preside over comprehensively dashed expectations. The electorate uses its votes to express anger at hardship and austerity, punishing the politicians they associate with the the tough decisions that had to be made. The Icelandic government could not give the people what they wanted, which was essentially to be the richest people in the world again, and quickly too. People get used to advantageous circumstances very rapidly, and come to see their good fortune as the new normal, or as a baseline from which things should only improve further.

Unfortunately, at the peak of a bubble, the only way to go is down, and the larger the bubble, the larger the correction. The political task of guiding recovery is made very much more difficult by being unable to hold power for long enough in a democracy to see through the measures that need to be taken. Failure to do so has a tendency to deliver power right back into the hands of the bubble architects and established elites, who happen be the least likely to want to move away from established power structures. These are votes cast, by association, for the memory of life at the peak of the bubble, not for a new future based on different governance principles. As such, further disappointment is guaranteed. Over the long life of a major financial crisis, the entire political elite can be consumed in successive waves.

The Icelandic bubble was exceptionally large in comparison with its host economy, suggesting that the period of adjustment back towards what has traditionally been normal for Iceland will be long and very painful. The country is far closer to the beginning of this trend change than to the end, despite the fairytale recovery portrayed in the mainstream media. At this point, the ‘recovery’ is merely a counter trend bounce within a larger downtrend, and that downtrend is very likely to be amplified significantly once the global context shifts in the same direction, as it appears poised to do. At a global level we have a very similar predicament, but on a much larger scale, that Iceland found itself in just prior to the crash of 2008. The lessons Iceland is painfully learning are ones many more of us will be experiencing over the next few years:

The Iceland of the future seems set to be a quieter place than in the first decade of the 21st century. It will, perhaps, be less about power and ambition – and less worthy of the kind of opera that might be performed at the Harpa.

“All this used to be filled with private jets,” says Mr Johannsson, with a sweeping gesture towards the empty runway overlooked from his corner office at Icelandair’s headquarters in Reykjavik’s domestic airport. “But it was easy when you are spending other people’s money,” he says. “Now we work with real things – with fish and with tourists.”

This article addresses just one of the many issues discussed in Nicole Foss’ new video presentation, Facing the Future, co-presented with Laurence Boomert and available from the Automatic Earth Store. Get your copy now, be much better prepared for 2014, and support The Automatic Earth in the process!

Wow!

The neoliberal roller coaster. What fun! Massive current account deficits and a real estate bubble to boot!

Well one things for sure: the party’s great while it lasts.

But the hangover, which Argentina can also attest to, is a real b*tch.

And Seasons Greetings from Britain, Europe’s new Bubble King.

A housing boom, increasing household debt, an influx of ForEx looking for yield (in the aforementioned housing sector), no industrial strategy (apart from, erm, housing).

We are having a fine old time of it here.

What could possibly go wrong ?

(okay, all of the outcomes listed in gruesome forensic detail in the above feature; but as the population can attest to, who is interested in reading through a 5,000 word article of doom and gloom when it’s a case of “party on dudes !”)

Groan.

I am surprised at the Foss take on Iceland.

With too much focus on the financial aspect of Icelandic activities.

She states Iceland is not investing in productive capital but I am not sure quite what Iceland can invest in !!

Greenhouses to grow Bananas ???

Perhaps a Tram (cheap electricity) for the capital along Bergens model but thats it really.

It has the most unique energy balance in the world and certainly quite different from entrepot Europe,

It burns almost zero fuel oil and no gas for residential & local commercial use – its quite unique even if we compare it to Hydro rich Norway or Nuclear heavy France.

Also It is NOT A MEMBER OF THE IEA – which partially explains why it has such a wise energy policy.

What most striking is its use of Diesel fuel – more diesel is used for fishing then its road transport

In Ireland 10 times as much diesel is used for road transport relative to both agriculture and fishing combined.

We can see now that Ireland is merely a euro area capital dumping ground.

But peripheral countries of the Euro have a advantage in this respect.

If we never needed the cars then we don’t need the cars……….

The old trading towns of Ireland – be it Cork or Waterford have seen a quite unnecessary decline in population simply because the Evil Euro which only can survive via credit rather then money expansion.

Creating a sort of credit nuclear blast wave out beyond the ancient walled centers of these agricultural trading towns.

The Irish PMs idea of exporting Irish beef to Asia so that we can afford BMWs will never ever work.

But we must accept that the financial industry advising the puppet states of Europe don’t intend on it working……ever…….

We are now all aware of the Euros evil plans.

To create extreme local scarcity via various mechanisms be it monetary malice or the new population plantations – all so as to drive pointless trade which the financial sector can easily capture via very long & absurd supply chains.

Whats the biggest banana republic in Europe ?

http://www.youtube.com/watch?v=NiuHQyPLzTI

A message of Winter Scarcity from An Taoiseach……..

(never quite sure if this guy is a comedian or not)

Although he reminds me a bit of Alan Ladd of the 1950s Cowboy films….

“Shane SHANE ”

http://www.youtube.com/watch?v=lNffPgaE1Yc

Me thinks he has been listening to Dutch energy economists………..with skin in the game of getting a yield off of symbolic tokens.

Its the highly populated core which depends on the periphery….its not as we have been told.

Their life support systems is almost entirely based on Usury

If you think a while. Try to figure out what he is really talking about.

That’s very very scary.

@Otter

The way to attack these traitors is to ask simple questions ……

And keep asking the simple questions.

Such as what is the purpose of a economy ?

If the purpose of the economy is to produce goods that can be consumed then we can agree on that.

If the purpose of a economy is to pay external debt then…………Heuston we have a problem………..as the products then exported and reimported as concentrated capital items via consequent capital flows generally cannot be consumed by wages or state benefits.

The surplus & unused products (generally capital goods ) depreciate over time.

This depreciation is expressed as either wage deflation , tax increases or product inflation( its all the same really)

I have a major problem with Foss here.

“Capital controls can become addictive for governments, however. With the possibility of investment overseas removed, investors, including pension funds, must look for opportunities at home where choices are very limited. Their consequent purchase of government bonds allows the government to finance its budget deficit, reducing pressure to cut deficit spending. Real estate investments made as one of a limited range of options provide artificial price support to the housing market, maintaining the illusion of greater value than would normally exist, both for the property itself and for the loan used to purchase it, reducing write-downs of what might otherwise be bad debt. Support for the property market also amounts to support for property tax revenues, again strengthening the government’s position. Removing these measures subsequently can be very risky, as relative values can adjust quickly to the downside when allowed to do so, and government revenues could be hard hit in a short space of time.”

Its not really a artificial price support.

The economy is merely not global – it is more closed.

Iceland produces all of its non transport energy – in this kind of closed economy that surplus must be expressed by consumption unless interest is being extracted for external players.

People have the dosh as domestic Industry has provided them with enough surplus energy to purchase domestic goods.

The fish can be used to buy oil which Iceland cannot produce.

I think she is also missing something vital.

The world economy is being run by a criminal cabal.

You don’t really want to go there.

In the real world of real domestic economies Belgium may convert or shut down it modern CCGT turbines and convert to more primitive but more dynamic OCGTs because of renewables erratic load production…..

You just can’t make this stuff up.

http://www.argusmedia.com/pages/NewsBody.aspx?id=846349&menu=yes

These guys supposedly expected CCGTs to preform base load functions (not really , it was and is the greatest scam of them all)

I am saying this because Irelands electricity production is showing major declines over these past few months…….much greater then seen over the last 3 or 4 years of depression.

The interest that we pay merely goes to the core so that they can buy the gas and not us – the banking idea (perhaps it was only a idea) was to have balanced trade was it not ?

NOT.

Yves thinks the periphery will run out of oil if or when they go national & default

But fails to see the possible complex dynamics if ALL OF THE PERIPHERY gives the finger.

We live in a oil standard rather then a Gold standard world.

Already we can see a major car boom happening in England as a result of non consumption of oil in the periphery.

What people fail to realize is that -IT IS ALL THE CORE CAN DO….as it has rejected physiocracy for free trade long long ago.

They can therefore only burn oil using their OWN entrepot products….that is eat their own tail rather then their neighbours.

If the Periphery decides to pour oil down the throats of London & Amsterdam the financial capitals will experience a modern Marcus Licinius Crassus moment.

Its not likely to happen in Ireland.

But it is possible I guess in Spain or Italy.

Once people in these countries realize that it is the cars which are killing them the core is dead.

Wow I thought Foss got this

I was wrong I guess.

Foss cannot get her head around the most obvious kernel of truth learned from the economic crisis.

Most of the worlds trade is not needed.

It simply used to pay off debt as the function of a capitalist economy is NOT TO CREATE USABLE GOODS AND SERVICES.

Watch Ireland and its “leader” for all that is needed to be known about such matters as Ireland is a sort of anti economy.

http://www.youtube.com/watch?v=JCt98ousNTw

If Europes entrepot is destroyed we in less populated parts of the world may well enjoy a time of great bounty and freetime although the bankers will no doubt try to press some military or indeed all of the military buttons.

Not too impressed with John Looke like monetary stats.

I would bet a considerable wad of EUROS the mean Icelander has a much better standard of living then the mean Irelander.

The Mean Irelander is “free to choose” but typically has not enough tokens to choose.

if we look at the consumption of oil products (which is more or less divorced from the alumina hydro and geo energy) Iceland has a very different ( & growing again) visage.

Y2011 data

http://www.iea.org/stats/WebGraphs/ICELAND1.pdf

Ireland however

http://www.iea.org/stats/WebGraphs/IRELAND1.pdf

(the recent 2012 figure is now just 6,000~ktoe !!!)

A default on the core of Europe is to capture the oil that entrepot Europe wastes on its value added products.

We have no energy crisis as such.

Its a crisis of non local production / distribution & consumption as global trade is structured around the payment of interest rather then serving real final (wage or benefit based) demand.

We should all be so lucky as to be second cousins. Our dear country is just a hateful cauldron where the scum is regularly discarded. Icelanders, in spite of their predicament, make a minimum wage of @15$/hour – down from 25! Interesting that foreign money trapped in Krona has to go somewhere – and that is back into real estate. The end of this essay sounds a lot like TINA – predicting a very long “downtrend.” Very good information but I am left with the uneasy feeling that money and economies are so poorly understood, perhaps intentionally by the people who gain from confusion, that nobody is even bothering to come up with an alternative to capital flows, international trade, environmental destruction and debt enslavement. Why not?

The author seems to be misrepresenting Iceland household borrowings at 220 percent of income. Just as the Federal Reserve Board includes hedge funds and other “pirates” borrowings as household borrowings, one can easily guess that this number represents the “pirates” borrowings.

Anyone who privatized banks in Iceland should be in jail, not commended. Believing that corporate raiders and pillagers create true value is just Hollywood publicity phlegm. Yes, if you believe that US financial corporations truly were earning 40 percent of corporate profits at the peak bubble, then you can believe these “pirates” were doing something besides theft.

I can guess that a vast majority of pounds and euros invested in savings accounts in Iceland were relent out not to Icelanders but to the European robber banks. Same thing happened in Ireland, German bank sets up shop, self detonates trading Euro Securities, NOT investing in Ireland, and the Irish people are left to pay for the theft.

“I can guess that a vast majority of pounds and euros invested in savings accounts in Iceland were relent out not to Icelanders but to the European robber banks”

They bolted out of Iceland leaving fleets of Range Rovers behind them.

I have great affection for Iceland and the Icelanders. ~310,000 of the nicest people you’ll ever meet.

An aspect of Iceland that fascinates me is that they pull off a country w/ a population less than Cincinnati and a land mass less than Kentucky.

Due to scale and the peculiarities of it’s economy using it as too literal of a model for anywhere else has its limitations.

Aluminum (a surrogate for geothermal power) is their highest value export followed by fish. The mostly heredity land owners (farms) are the traditional center of gravity of power in the country.

Beautiful farms. An interesting peculiarity is that the land owners also own the rivers and streams and their content as it flows through there property. A consequence of this is that these segments of flowing water may be far more financially productive due to fishing leases than the surrounding farm’s inherent agricultural value –to the tune of high US$ six figure incomes.

Property owners may operate fishing lodges, or simply put up their piece of river in leases to special entitles that aggregate them and resell fish rights. As a perspective, a stay at one of these lodges can be $5,000+/day.

Back during Bush rev.1 term he would fish there and do deals.. A fellow I know that was an Icelandic national US Embassy employee, also a avid fisherman took Geo Shultz and him during some negotiation deal and acted as a fishing guide in the hinterland, In classic Pretorian Guard excess, the SS was reduced to using their Blackhawk Helicopter to spot for fish.

http://www.cio.com/article/740458/Why_RMS_Built_Its_Cloud_Environment_in_Iceland

Icelanders are state of the art experts for geothermal power related activates from congen to District Heating and Hydronic systems hot water heating systems.

Cool product::

http://www.apartmenttherapy.com/blush-radiator-by-thorunn-arna-43175

So yes, from up thread Iceland does have a very unique energy balance and “product mix” that drives their economy.

EUROPES DASH FOR GAS IS OVER – if I were Iceland I would wish to slowly walk away from the Euro train wreck and I would not build my economic hopes on potential tourism from this black hole of Euro entropy.

Taken from the IEAs energy stats of OECD countries

Electricity outputs from Nat gas (note the following is not efficiency gains , IT IS A LOSS OF PRODUCTION)

OECD Europe expressed in (GWh)

1990 : 167,533

1995 : 264,761

2000 : 511,619

2008 : 868,605

2009 : 814,034 (first wobble)

2010 : 845,754 (recovery ?)

2011 : 786,143 (second decline phase)

2012 : 664,587 (massive structural decline)

Remember the dash for gas was a high quality fuel race – the fulcrum on which Euro “growth” has been touted….in reality it was merely a massive extraction via the mechanism of interest from the real economy as New Nuclear was denied funds so as to aid consumption in the financial capitals of the world.

The “Irish growth strategy” ……..the last thing Ireland needs is “growth”

http://www.finance.gov.ie/documents/publications/reports/2013/mtesfin2013.pdf

Growth of bank credit will be catastrophic as before

Irelands strategy Is to export its wealth and import labour further reducing the energy used per person.

Any “growth” will drastically increase the population again which will further increase the stress on the society as the society is not “cohesive” as stated – it has become atomized since the 1970s and EU entry….starting with the global banks dumping heroin into Dublin , turning the capital into a living hellhole.

Therefore GDP numbers will rise but consumption per person will tank even further.

If you subtract the possible future capital dumping (we send surplus exports to the core and receive items which we cannot really use without massive depreciation) via cars etc etc the real end use (life support) energy consumption will soon reach Edwardian levels for the mean worker.

Growth will cause a rise in the retirement age , not a decrease.

What have I missed ?

Industrialization was a labour saving experiment was it not ?

Not.

Be very afraid , very afraid when banks escape the danger zone.

Then much of the population can be safely wiped out without a loss on the books.

Wow Wow Wow

I can’t believe this FT piece was linked in the above article

http://blogs.ft.com/ft-long-short/2013/03/13/europes-house-price-bubbles-iceland-ireland-and-spain-updated/

First of all he makes a elementary omission.

“imports virtually everything it needs other than fish and electricity” – forgot one little thingy – Nat gas it imports no Nat gas.

In Irelands case its our biggest fuel import after oil.

You see the financial sector is deeply tied to the criminal dash for gas as it is a means of controlling nations & former nations.

He then talks of cars as if vast numbers of them were important to national economies – they are not , they are important to the oil monetary cartel based in London and Amsterdam as it is a very easy way of controlling Euro area scarcity in their interests.

Car consumption is wasted end use consumption.

He then talks about the supposed money illusion but never states that Euro area workers lost big time after Euro introduction as Euro inflation (or tax increases) on domestic &social goods exploded.

The Irish Pub trade went into immediate dramatic decline after 2002 with a slow burn destruction since 1979.

The Euro destroyed all domestic commerce in Ireland starting with its real introduction in 1979 which was followed by the dramatic deflation in the 80s.

Beginning to think good old Fosse works for the other side………..

Most days I am reading Naked Capitalism and New Economic Perspectives in parallel and while I know that there is only a bit of overlap, the disconnect can sometimes be a bit jarring, like when I read:

And where would be the problem with that? Iceland, as the post points out, is still sovereign when it comes to issuing its currency, so the state could have just spent the Kronas necessary to complete the project, stimulating the construction sector in the process.

This is just plain wrong: once again, Iceland is sovereign, the government is the issuer of its own currency and it doesn’t need to “sell” bonds to “finance” its spending. There’s absolutely no need for a government issuing its own freely floating currency to reduce its deficits, unless the economy is at capacity and government spending leads to inflation. If 20% deficit are needed for full employment in Iceland to be reached, why shouldn’t the government run this deficit?

So after, as the post points out, the crisis has been caused by the neo-liberal playbook, a deal is made with the point organization of neo-liberalism, and the sacrifice being made consists of impoverishing the vulnerable via regressive taxation and reduced social spending?

So, let me see – from what I understood, the Icelandic banks are bankrupt and effectively state-controlled. This would mean that all mortgages that these banks held are now held by government, which also means that the government could forgive all the loans for which these mortgages were security, without having to “pay” for this debt-forgiveness. In particular, this would mean not swindling people out of their pension savings (although private pension savings are not a good idea anyway, since they take away from aggregate demand and are pointless unless the investment in the infrastructure – nursing homes, medical sector, care personnel – has been made)

I know I sound like a broken record but the fact remains: the Icelandic government is a sovereign currency issuer! If Hilmar Veigar Pétursson needs Kronas, any government-controlled bank can give him a loan as large as needed, although the question comes to my mind why a video game publisher needs such large loans. If he needs foreign currency, I understand the problem but then I wonder again why he needs large loans of foreign currency for business.

All in all, the analysis of this post and the potential solutions it offers, seems entirely couched in neo-liberal think and speak…which I find perplexing since it is exactly this think and speak that created the mess in the first place. How about going into alternative directions? Imagine the last government, instead of playing along with the IMF’s rules, would have put the welfare of the Icelandic population first, engineered debt relief, and spent what was necessary to fill the demand gap – they might just still be in power.

You are missing how large the banking liabilities were , over 11x GDP. No way could they be monetized without creating lots of inflation. Iceland defaulted on foreign bank creditors to be able to pay domestic depositors. MMT can’t solve a mess of this magnitude.

The inability to get foreign currency was very damaging to Iceland. I recall stories at the time of shortages of critical supplies, particularly pharmaceuticals.

Entirely couched is too strong. The piece gets some important things right, focuses on the crux of the matter more than most..

” the people overwhelmingly declined to accept public responsibility for the private debts of the banking system.”

“Rather than bailing out the banks and imposing austerity to the extent that the European periphery did, Iceland has attempted to protect its welfare state during the period of crisis.”

Combined with allowing the banks to fail (with the majority of the losses taken by foreigners), rather than bailing them out at public expense, it has allowed Iceland to stem what could otherwise have been a fatal financial hemorrhage. Given that people judge their situation in terms of nominal wages in local currency, rather than in relation to global purchasing power, the situation is perceived differently than in the troubled countries of the eurozone, and therefore the consequences are different. There banks were bailed out by the taxpayer, leading to government debt.

Not paying debts you don’t owe, not paying debts owed by other entities,even if they are domestic financial institutions, is a fine and traditional path to prosperity. It is not default, and so far, the courts have seen it that way. As far as I can see, the idea of “bailing out banks” for foreign liabilities is the post-1970, post -1980? novelty , merely pretending to a hoary pedigree. Recklessly assuming others’ debts – at the deepest level because of brainwashed mass acceptance of grotesquely illogical “economics”, whose illogic has assumed its most pure, unprecedentedly pure, form in the last few decades – is the road to misery and existential despair, as Ireland is learning.

But the piece contradicts itself, contradicts its good sense with its illogical “free-floating exchange rate had become far too much of a liability:” part that grossly exaggerates the vulnerability of states like Iceland to “global financial storms”. For MMT, the brilliant idea of not paying debts you don’t owe can “solve” messes of even greater magnitude – by not creating them!

Of couse Iceland could have problems stemming from lack of foreign currencies. But keep fishing the fish. Keep running your society on homegrown, cheap geothermal. Maintain a modern, productivity and human welfare enhancing Welfare State. Then what is the real problem? It ain’t there.

She spends quite of text critizing capital controls, but after

“The new banks serving the domestic market were recapitalized, at a cost of some 25% of GDP, and granted the guaranteed domestic deposit base. Two are now owned by their foreign creditors, while the Icelandic state holds majority ownership of the third.”

I searched in vain for a description of how the banking sector has at least been strongly reregulated and for some criticism of the re-privatisation.

Austerity is done after all:

“The agreement with the IMF involved postponing cuts for a year, then imposing both tax increases (corporation tax increased to 18% from 12%, increased income tax and VAT and also a wealth tax) and spending cuts simultaneously, rather than favouring primarily spending cuts as was done in countries like Ireland.

[…]

The pension system has been raided and healthcare provision has been scaled back, with sharply increased co-payments required.”

yet I read no criticism of this at all!

Instead of outright debt relief, people are “allowed” and “incentivized” to

“use their tax-free pension savings to pay down household debt.”

and once again, the only criticism is of how this is only a short term solution and not in how it reduces people’s savings even more.

Even the part on the new constitution is half-hearted. From how she started, this should have been a piece that clearly and loudly makes the case that the Icelandic model is nothing to emulate because it tries to drive out Devil with Beelzebub but instead we read how in a democracy elected governments cannot see the harsh and necessary neo-liberal measures through to the end.

What demand gap ?

What does this really mean ?

So you will have more nurses taking care of old people rather then a family not swamped by pointless work can take care of their own.

Full employment is inhuman.

MMT is Hamster wheel economics.

DoC,

your second point of your response is either naive or in bad faith. While you might be right in terms of pure labor, taking care of a person whose physical and mental abilities are failing when you’re not trained for it, and don’t have the infrastructure is not comparable at all to trained personnel doing this in a nursing home.

Besides, assuming that the elderly person needs to have someone available all day – who would that be? In the past this fell on women (who were not “not swamped by work” by performed hard work without direct renumeration), so is this the arrangement you had in mind?

Regarding your first point:

and at an unemployment rate of 5%, there’s obviously not enough demand to employ several percent of the working age population.

As to “pointless work”, the inhumanity of full employment and hamster wheels, I’d direct you to Mitchell and

(http://bilbo.economicoutlook.net/blog/?p=26396)

but I saw that you’ve already been there.

PS Iceland has reached the limits of its productive capital spend it can actually use in a rational human manner – what more do you want out of people ?

If it increases capital spend it will not have the people to burn it unless you consider it wise to increase the population via external workers…..but what is the point of that from a national democratic perspective ?

How much is enough for yee Keynesian guys ?

He always want more friggin stuff.

MOST PEOPLE LIKE TO SLOW DOWN – go trekking in the Icelandic wilderness , fishing , hunting etc etc…..you know natural human things outside of the Industrial maw.

http://grapevine.is/Home/ReadArticle/In-The-Land-of-Wild-Boys

The Reyjavik Grapevine

In The Land Of The Wild Boys

Based on a 2010 article entitled “Í landi hinna klikkuðu karlmanna.” (“In the Land of the Mad Men”). Translated in part by Haukur S. Magnússon

required reading for MMTers……….the bankers last chance saloon.

https://ia600404.us.archive.org/0/items/fallacyofsuperpr00doug/fallacyofsuperpr00doug_bw.pdf

I think much of the problem is for those who borrowed money in foreign currencies. These loans doubled almost overnight when the value of the krona tanked. I don’t imagine the government owns them. I have read many of them have been bought by vulture capitalists. Did anybody propose the government buying them at prices near what the vultures paid?