Yves here. Since the financial media is covering the continuing meltdown of the ruble intensely, we thought it would be helpful to add some information that seems to be missing from most reporting. This post by Jacques Sapir from the 14th (hat tip Michael Hudson) provides important detail on the importance of oil to the Russian economy (far less than typically depicted, although it is the biggest source of foreign exchange), the impact of the fall of the ruble and oil prices on the domestic budgets, and the odds of a Russian default. Note that Sapir is sanguine on the default front and does not see a rerun of 1998 in the offing, by virtue of of Russia having large foreign currency reserves. Note that Menzie Chinn of Econbrowser differs, and uses a chart from the Economist to make his point:

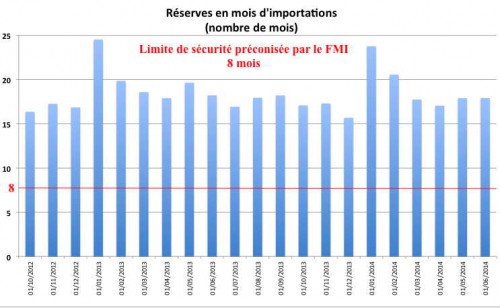

In addition, observers did not take into sufficient account the fact that much of Russian forex reserves are to varying degrees illiquid…

In other words, reserves useful for defending the currency against speculative attacks are more like $200 billion than $400 billion.

And it’s telling to see what a difference a few days makes. This article was penned before the failed Russian emergency rate hike to 17%.

By Jacques Sapir, director of studies at École des Hautes Études en Sciences Sociales in Paris, and head of the Centre d’Étude des Modes d’Industrialisation (CEMI-EHESS). He specializes in the economy of Russia, and teaches at the Moscow School of Economics. Originally published at RussEurope. Translation by Anne-Marie de Grazia

he sharp depreciation undergone by the Rouble during these past weeks relates to two main factors: a peak in the reimbursement of loans by Russian companies, but also the sharp drop in the price of oil. There is still a third factor to be included in the picture: speculation. It applies to the ruble and to the oil price as well.

It can be verified in the following table which carries the different values in the exchange rates since the beginning of the present year. One notices by the way that the exchange rate, after depreciating until mid-March, re-appreciated until July 2014 before undergoing a sharp depreciation during the Fall :

Table 1

Evolution of exchange rates as an index.

|

Roubles for 1 Dollar |

Roubles for 1 Euro |

Roubles for 100JPYen |

Roubles for 1000 KR Won |

Roubles for 1 Fr Suisse |

Roubles for 1 BPD |

|

|

29/01/2014 |

106,00% |

105,10% |

108,30% |

103,70% |

105,00% |

106,80% |

|

15/03/2014 |

112,20% |

112,70% |

115,70% |

110,40% |

113,80% |

113,00% |

|

09/07/2014 |

105,40% |

103,90% |

108,70% |

110,00% |

104,80% |

109,50% |

|

01/10/2014 |

120,60% |

110,90% |

115,60% |

120,70% |

112,60% |

118,90% |

|

12/11/2014 |

140,70% |

126,60% |

127,40% |

135,60% |

129,00% |

135,20% |

|

26/11/2014 |

137,71% |

124,02% |

122,52% |

130,81% |

126,48% |

130,91% |

|

04/12/2014 |

166,52% |

149,29% |

146,48% |

158,11% |

151,79% |

157,78% |

|

09/12/2014 |

163,23% |

145,21% |

141,14% |

154,04% |

147,77% |

153,88% |

One can see the extremely big fall between November 26 and December 4, followed by stabilization. Against all currencies, the Rouble appreciated slightly between December 4th and 9th. Also, the gap between the exchange rate against the dollar and the exchange rate against other currencies is considerable. This can be explained by the size of the repayments to which the Russian companies (banks as well as industrial companies) had to proceed during this period. They needed to buy dollars, which destabilized the currency market on which the dollar was getting rare because of the sanctions.

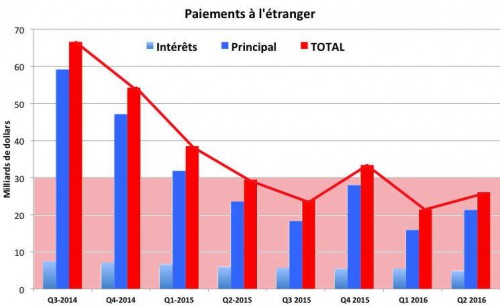

It seems that Russian companies and banks, faced with considerable loan payments to be made in December, have massively bought dollars, which made the Rouble go down during the first days of December. On a market where, as an effect of American sanctions, dollar liquidities are rare, this would explain the spectacular, yet not dramatic evolution of the past days. As far as the flux of reimbursements is concerned, it will decrease considerably come January 2015 (chart 1).

Chart 1(a) and (b)

Foreign payments in billion USD

(b)

Quarterly reimbursements with the limit of quarterly trade surplus (pink zone)

Source: Central Bank of Russia

We must now examine the reason for the drop in oil prices.

A Drop of a Political Nature?

Multiple indications show this drop as being of a political nature. Some OPEC leaders have alluded to a possible speculation too. It is known that huge quantities of “paper-Oil” were in some Banks books and that these banks were going “short” on this trade. But, still, there is quite clearly a political bias in this speculation.

An attempt by the United States to destabilize Russia is often conjectured. Such an attempt may have occurred, but reality is much more complex. One must know that the threshold of profitability for the new sources of fossil fuels lies at 70 USD a barrel for oil sands (mostly exploited in Canada) and at 65 USD the barrel for shale oil. With an oil price that could hit below 60 USD a barrel, the OPEC countries are actually attacking the North American oil industry. Besides, it is significant that the large Russian oil companies, Rosneft, Loukoil, remain fairly silent about the present evolution of prices. One may well ask if there is not a tacit understanding between Saudi Arabia and Russia to evict, or at least to set limits to, a new actor on the fossil fuel market.

But this attack could have other consequences. The shale oil and gas sector has developed on loans covering 80% to 90% of the investment costs. These could make out over 300 billions in liabilities for American banks. These debts inevitably turn into “dubious loans” (or “non performing loans”) from the moment that one descends significantly below the threshold of profitability. But banks have, as a matter of course, securitized this loans, by emitting CDS’s in which these loans act as collateral. If we are stuck too long with a price that is too low, one cannot exclude a new financial crisis in the American banking system. We notice moreover that the potential risk hovering over the shale oil industry has already been anticipated in part, for operating licences in the United States have gone down 50% during the third quarter of 2014. We can therefore conclude that if oil prices maintain themselves at a very low level until next June, we will probably witness a blood bath in the shale oil industry, with very grave consequences for the banks. I point out in passing that the estimate of 65 USD as a threshold of profitability is an estimate given in oil industry circles, based on the technical conditions of extraction. It does not include financial costs. We can therefore expect the American government to blow the whistle to put an end to the price drop no later than the end of this winter, if it doesn’t want to have a major crisis on its hands. But extracted volumes will go down, too. Production in the United States, after experiencing a peak at the beginning of 2015, should go down significantly during the second semester of 2015. This means that we can expect a new rise in prices during the second semester of 2015, probably in the direction of 70-75 USD the barrel.

This is Not a Replay of 1998

This poses no problem to Russia, whose reserves are such at present (450 billion dollars just for the Central Bank) that it can face an important drop in prices, albeit of a limited duration. One must note also that the repayment of loans by Russian companies for 2015 does not exceed 120 billion dollars. This remains far below the reserves of the Central Bank of Russia as well as of those of the finance ministry. Should it turn out to be necessary, these companies will find among the state actors the money which they need to repay their loans. But this would then imply an extension of the authority of the State over the economy. Yet, in no case should it lead to a “default,” as in 1998, neither of the State (which is very little in debt, and whose debts are essentially held by Russian actors, such as Sberbank) nor of the private sector, which is in fact in possession of vast assets in dollars and which is therefore solvent in the long term. The question of short term liquidity being manageable by way of an appeal to the public sector. The very idea of Russia getting struck into the same crisis pattern than in August 1998 sounds very, very strange. This is probably another case of ideology-driven statements, or ones made by people with no information at all on the actual situation of current Russia.

The image of a Russian default continues to haunt the minds, when the situation is actually quite different at present, as shown by the ample currency reserves. But one may ask if this default of 1998, in which American banks and European banks generally lost a lot of money, is not still being « reproached » to Russia. As a matter of fact, this default allowed Russia to save itself from the depressionist trap in which it had found itself since 1992. It was the founding act of the economic renewal, and of course also of the political renaissance, of the country. We remember the decision of the then Prime-Minister, Evguenny PRIMAKOV, to send Russian paratroopers to protect Serbian populations at the time of the intervention of NATO in Kosovo. One can see in this a first adumbration of the “return of Russia” which is at present embodied by Vladimir Putin, and which has still not been admitted by the ruling circles of the United States and their satellites in Europe.

Russia is not an Oil State.

These realities are systematically ignored by publicists which are popularizing an image of Russia as an « oil state. » In doing so, they forget the important fact that the sector of fossil fuels represents only 11% of GDP. Granted that it weighs more heavily in exports. But this translates in fact a variation of the relative price of oil products in relation to other goods, not a phenomenon of volume. A fairly simple example will show this.

Let’s take the case of a simplified export structure, distinguishing volumes and prices, and considering that at the beginning of the period (T) the level of these prices (calculated in USD) is equal to 100.

Situation at T

|

Volume |

Price |

|

| Commodities |

100 |

100 |

| Agriccultural goods |

20 |

100 |

| Manufactured goods |

30 |

100 |

| Weapons and equipement |

20 |

100 |

If we calculate the share of each category of goods in the total exports we obtain the following picture of the country’s exports:

|

Base price (T) |

|

| Commodities |

58,8% |

| Agricultural goods |

11,8% |

| Manufactured goods |

17,6% |

| Weapons and equipments |

11,8% |

For this price structure, commodities (which are considered here as representative of oil) play a decisive role in exports. Let’s now suppose that at T+1 the prices of commodities increase by 30% in relation to the base price, other prices remaining unchanged, and that at T+2, these prices diminish by 50% (always in relation to base price), other prices remaining unchanged. The product distribution of the exports of the country would then be as follows:

|

T Base Price |

T+1 Increase in commodity prices of 030% |

T+2 Decrease of 50% |

|

| Commodities |

58,8% |

65,0% |

41,7% |

| Agricultural goods |

11,8% |

10,0% |

16,7% |

| Manufactured goods |

17,6% |

15,0% |

25,0% |

| Weapons & equipement |

11,8% |

10,0% |

16,7% |

We can see immediately that the share of commodities in the exports fluctuates massively with the movement of prices. The image rendered by the analysis of the structure of Russian exports reflects in reality the movement of relative prices as determined in the short term by the movement of the absolute prices for commodities (i.e. for oil). A more exact analysis would consider the number of Russian workers working towards for these exports. If one considers that the base productiveness of a worker in the fossil fuels sector is at the instant (T) (and therefore at the price of T), 2.5 times superior to the productiveness of a worker in the sector of weapons and equipment, 3 times superior to a worker in the sector of manufactured goods and 5 times superior to the one of a worker in the agricultural sector, the real share of these sectors in exports turns out very differently:

| Sectors |

Value (T) |

Share in work |

Share in value |

| Commodities |

10000 |

29,4% |

58,8% |

| Agricultural goods |

2000 |

29,4% |

11,8% |

| Manufactured goods |

3000 |

26,5% |

17,6% |

| Weapons & equipments |

2000 |

14,7% |

11,8% |

We see that the effects of relative prices can skew in a very considerable way the reality of the structure of an economy. It is particularly important to keep this in mind when one is reasoning about a country which, like Russia, is both a producer of commodities AND of industrial goods.

Back to the Ruble

We notice that the strong depreciation of the Rouble corresponds to a peak in repayments, but that the situation will loosen up in early 2015. It is sure therefore that the exchange rate will reverse its tendency in the first semester of 2015. The question is, up to what point? If the Rouble stabilizes around 50 roubles for 1 USD, inflation will be strong next year and could reach 12%. If we witness a rise in oil prices and the Rouble stabilizes around 40-42 roubles for 1 USD, the inflation rate could amount to merely 10%. Still, this implies that the Central Bank of Russia keep an eye on such establishments which could be tempted to speculate on the exchange rate, dragging it farther down than it should normally be. Explicit threats were made by President Putin at the occasion of his declaration of general policies before the chambers of parliament on December 4th. However spectacular it has been, the depreciation of the Rouble by no means puts into question the financial stability of Russia. The trade balance remains in excess, with an amount outstanding of 10 billion dollars a month. This is largely sufficient to face up to coming payments. The budget is actually profiting from this depreciation, which should allow the government to spend a little bit more in 2015.

Russia will therefore remain one of the least indebted countries in the world, which is not necessarily an advantage and goes to show that, provided it takes up debts internally, the country wields over a strong potential for investment and development.

btw, Federal Reserve basic capital ratio is 1.26%.

Russian Central Bank ratio is 12.5%.

appreciate the post Yves.

Anyone else noticing Bloomberg has whipped itself up into a frenzy lately? They seem to have gone beyond mere anti-Putin propaganda into the realm of the truly delusional. I guess they think giving their readers a taste of 1890’s style jingoism sells ads. Maybe they’ll drum up support for bombing Canada next.

It really pays to avoid U.S. media these days. I fear for what 2015 is going to bring.

I agree Chris. I get most of my current affairs info from a relatively small handful of blogs and an even more select few newspapers. When I watch the US networks — and now even Bloomberg is in the same category as the rest of ’em — I have to put my brain into a special operating environment which filters the words and the pictures into a sort-of demilitarised zone (to use some IT security jargon) from which I can then unpack the messaging (whether overt, as in the coverage is what it purports to be or whether there’s something else behind it masquerading), the messenger and what the transactions might be between them.

Even previously trustworthy sources (e.g. the BBC, PBS) I now have to view with a little suspicion. Dare I say that the Real News Network and maybe C-SPAN are some of the last vestiges of old-school integrity left.

I’ve crossed PBS off my list of trustworthy media sources. This morning on NPR they had a blurb on the TRIA getting sent to Davey Jones locker by the Senate. There was no objective discussion of the pros/cons of the bill, nor any mention of the fact that Jeb Hensarling (R) had poisoned the bill with a non-germane amendment that would have further gutted Dodd-Frank.

Instead they brought on a Chamber of Commerce shill to whine and bemoan the taxpayer-backstopped insurance programs’ demise. The interviewer let this go mostly unchallenged, with no reference to the shenanigans of Hensarling and others (Schumer) who refused to strip out the Dodd-Frank amendment.

Also this morning, the anchor called Putin’s governance “reckless “. It’s the only channel I can get on the ranch and I only listen to it in the shower. Listening to NPR is a waste of time except to know what the regime talking points are.

Yes, the Nice Polite Republicans (NPR) continually display they are just another faithful organ of the Politboro, total silence on the gutting of ERISA protections, the Wall St Cromnibus coup, and certainly they’re as quick to demonize Putin as anyone. Here’s a question: why, precisely, the urgency to brand Putin as our latest Worst Guy In The World (following in the hallowed footsteps of Mossadegh, Arbenz, Fidel Castro, Ho Chi Minh, Allende, Noriega, Ahmadinejad, Saddam, Gaddafi, Assad)? Maybe not enough money to be made just peacefully trading with him (as he is doing with China and India)? It’s not enough to trade and grow ourselves, we need to economically destroy any countries trying to do the same? Oops, we’re all connected: Step 1. Obtain firearm; Step 2. Locate foot; Step 3. Pull trigger.

MM

“It’s the only channel I can get on the ranch and I only listen to it in the shower.”

Most radio stations of note, (and plenty not of note) have online digital broadcasts (web radio/internet radio) available.

I happen to use http://wiki.slimdevices.com/index.php/Internet_radio because this is the platform I wirelessly broadcast media at home –but you can go online and search “internet radio” or “web radio” and the world is your oyster media-wise, As well you can buy a dedicated portable radio very inexpensively that loads as a device on a home (ranch) network wireless connection.

For that matter, w a 4G phone and a modest internet connection connection, it will function as an excellent digital tuner/video link.

http://www.cnet.com/products/metra-aip-av5v-ipad-iphone-ipod-audio-video-charging-cable-composite-video-audio/ for the iphone alternative,

The key consideration (for fidelity) is these cables use the signal “line out” rather than the earphone jack, so the crappy volume control circuit on the phone, which slaughters the dB response, is taken out of the loop.

Yes, I e-mailed some people about this with screenshots of the Bloomberg landing page. Really shocking.

“You supply the charts, and I’ll supply the war.”

And now little bro Bush is huffing and puffing about USA needing a strong leader…

Duck and cover, people, duck and cover…

Has the Dollar blindly walked into a trap…???….. The view from Russia…

“Rouble vs. Dollar Games – From a Perspective of a Russian Businessman

Only the lazy are not writing about this subject today. But everyone for some reason is looking in the wrong direction. Let me explain:

– Our country has a stock of dollars

– The currency of our country – roubles – is held by other countries

– We – Russia – are planning to sell oil for roubles in the future

– Everyone who buys oil from us in the future will have to look for these roubles to buy oil

– The harder it is to look for them, the more expensive they will be

Naturally, the task is simple – we need to drop the rouble to the bottom, and then buy all the roubles that we can, giving away the dollars that are no longer needed and not guaranteed by anything. This will help concentrate all of the roubles inside the country and to assign their price independently, while holding and releasing more money to the market.”

A view from Russia….

“Rouble vs. Dollar Games – From a Perspective of a Russian Businessman

Only the lazy are not writing about this subject today. But everyone for some reason is looking in the wrong direction. Let me explain:

– Our country has a stock of dollars

– The currency of our country – roubles – is held by other countries

– We – Russia – are planning to sell oil for roubles in the future

– Everyone who buys oil from us in the future will have to look for these roubles to buy oil

– The harder it is to look for them, the more expensive they will be

Naturally, the task is simple – we need to drop the rouble to the bottom, and then buy all the roubles that we can, giving away the dollars that are no longer needed and not guaranteed by anything. This will help concentrate all of the roubles inside the country and to assign their price independently, while holding and releasing more money to the market.”

fortruss.blogspot.com/2014/12/rouble-vs-dollar-games-from-perspective.html

Russia certainly seems strong enough to use the rouble as a true sovereign currency employing domestic labor. But it should be being used to diversify into solar and wind etc and trying to keep the carbon in the ground.

“”Coal is a natural sponge that absorbs many substances dissolved in groundwater, from uranium to cadmium and mercury. The Earth’s capacity to absorb the filthy byproducts of global capitalism’s voracious metabolism is maxing out partly due to the allure of free market logic that usurped so much intellectual life in the late 1980s and 1990s.

The 1970s was a time when intervening directly in the market to prevent harm was still regarded as a sensible policy action. Confronted with unassailable evidence of a grave collective problem, politicians across the political spectrum still asked themselves: “What can we do to stop it?” (Not: “How can we develop complex financial mechanisms to help the market fix it for us?”)””. (This Changes Everything)

Solar PV is a gigantic boondoggle at present and for the foreseeable future.

Wind is also in this category.

Yes, there are small regions where these technologies can be marginally useable, but neither is in any way fit for base load in modern societies.

The greatest irony of these technologies is that they actually cause carbon emissions to increase rather than decrease – by forcing ever more inefficient operation of fossil fuel backup.

There is a conclusion here – but nobody wants to make it. We have to go back to more primitive means of production. Manpower anyone?

… we got lotsa people who could become worth their weight in gold

http://www.lowtechmagazine.com/2010/03/history-of-human-powered-cranes.html

Hey, we can build Human powered treadmill cranes out of carbon fiber! HAHAHA!

A Study by Mark Z. Jacobson and Mark A. Delucchi at the U of Calif, Davis detailed a road map for 100% of the world’s energy for all purposes could be supplied by wind, water and solar resources by as early as 2030. The plan includes not only power generation but also transportation as well as heating and cooling.

Univ of Melbourne: 60% solar, 40% wind electricity system in 10 years

US NOAA: cost-effective wind and solar 60% of US electricity by 2030

US DOE: wind, solar, and other currently available green technologies could meet 80% of American’s electricity needs by 2050.

Denmark has 40% of its electricity coming from renewables, mostly wind.

These goals depend on how strongly we push for them and push against the current fossil fuel regime.

What’s hard to compete with is the dollar amount of carbon still in the ground even though it’s becoming even more devastating to the environment to get it out such as fracking, tar sands, deep water drilling, arctic drilling etc. (ibid)

These goals depend on how… successful we are at developing an efficient scalable method for storing MW worth of power from intermittent sources, otherwise the conventional sources have to remain available as pointed out by c1ue. Presently something like ~20% ( from memory) of grid power can be supplanted by intermittent sources. Its an issue of storage and distribution as much as anything.

Good point. These sort of problems are why we need an ‘Apollo’ project of state funding of significant projects. The private sector doesn’t have the funds or long term outlook necessary for this type of innovation. It’s also important to nurture this process. Fossil fuels have the advantage of a system already in place (and their own set of ‘subsidies’) and renewables need to be subsidized to get a foothold. We need to realize the importance of getting this foothold to insure clean air to breath among other aspects of climate destruction. This nurturing includes things like states agreeing to pay an established price for these renewable outputs to get them going. Various free trade agreements can make this sort of nurturing of vital innovation illegal if it interferes with profits of established fossil fuel companies.

http://www.triplepundit.com/2014/09/storage-solutions-wind-solar-energy/

Sustainable Renewable Energy Storage: Are We There Yet?

9/5/14

Debbie Fletcher

Energy storage potential

Wind turbines and photovoltaic installations now produce enough energy to sustain themselves. However, there is an issue in that both types of technology require extra, large-scale infrastructure to store the energy so that it is available on demand and not just when it’s windy or sunny. A study by a team of Stanford researchers concluded that the wind industry will be able to afford to invest in these large-scale technologies and remain sustainable, while the solar industry will find it more difficult due to the extra energy required to produce photovoltaic panels.

The viability of storage systems for renewable energy sources like wind and solar is already beginning to be put to the test in the real world. According to a recent article in the Globe and Mail, Ontario’s Independent Electricity System Operator (IESO) has recently commissioned five companies to build 12 demonstration models which will capture and release energy, thereby accommodating the power fluctuations associated with renewable energy sources. The technologies being tested include batteries, hydrogen storage and kinetic flywheels. The IESO hope that these storage systems will not only allow renewable energy systems to be incorporated into the power system but will also help to balance supply.

A recent article on Clean Technica gives examples of how storage technologies are also progressing elsewhere: The Pacific Northwest National Laboratory has been working to bring down the cost of Sodium-β (beta) batteries, which are considered by many as having the potential for widespread energy storage but have always been limited by their relatively high cost. However, PNNL’s latest research has helped to decrease the cost and improve the operating life of the battery using a new liquid metal alloy, which could be a hugely significant step for the renewable industry.

I completely disagree. Baseload is a concept peddled to the public by utilities that want to make investment in renewables impossible. Utilities operate on a profit model (most have shareholders) not a scientific one so they feed the public a great deal of BS to maintain their bottom line. We have been using pretty much the same power distribution/production model for over 75 years. It hasn’t changed because utilities don’t want to change it not because current technology makes the change infeasible. See the following:

http://cleantechnica.com/2014/08/08/rmi-blows-lid-baseload-power-myth-video/

http://decarbonisesa.com/2014/09/14/the-myth-of-the-myth-of-baseload/

http://www.kentucky.com/2011/07/12/1809690_the-myth-of-baseload.html?rh=1

There are countless more from technical papers, research and the like, please refer to them through a search if you want more information.

Baseload does not have to be met via single plant distribution. Power can be effectively transported at great distances (1000 km or more) with minimal losses on demand (“on demand” is the key point here, it is a distribution/load based system that would be used with Renewables). The only issue is distribution. If your grid is set to accommodate so called “baseload” plants then “baseload” plants are essential. If your grid is set up to accommodate a large portfolio of renewable energy sources then demand can be met in much the same way except it is based on grid load.

Being owned as profit seeking entities, consider why utilities operate on the baseload principle. It is predictable. They know how much coal/gas/uranium they use, when they use it and change comes slowly, and the power distribution model/culture conforms to this principle.

As always we have to consider sustainability. Large (i.e. baseload) coal or combined cycle natural gas plants are going to be pretty difficult to operate once we run out of economically viable oil, and unless all that coal and natural gas are going to be extracted/pumped, transported, etc. by way of coal/gas plant generated electricity/battery storage we are going to have some major problems with the “baseload” system. Renewables won’t work because we won’t let them. It has absolutely nothing to do with an inability to meet demand (“baseload”). That myth has to die.

Almost as if by 1980 it was clear to economists that the capitalist model could no longer provide the profits necessary to maintain growth, and we got instead trickle-down which was soon corrupted by investors demanding productivity (profits) and the offshoring of all our jobs. Followed by financialization of everything, making even housing a commodity to be traded. Aggressively. The only field left to compete in was investing. Yet all the goods and services required by our society were provided – increasingly by China and other EMs. Pollution was not regulated any more than banking was. In fact they have gone hand-in-glove to create a market economy that serves wealth creation in currency only. It would be nice if the ruble could extract itself from this ratrace. To now stop all this insanity will require an economy based on just about anything but trade and profit. The danger of maintaining a market mentality is that it precludes resolving global warming and pollution; it also continues – requires – inequality; and financialization, which must create a return (whose whole reason for being is to create a return on investment) is incapable of promoting environmental solutions. Oil is just another step down a ladder of decommissioning the market economy. For now it looks like a price war, but oil is actually all but done. The real trick is NOT to replace oil and other industrial commodities with “non-resource tradeables” (financialized instruments) but instead to create a new economy. Not based on trading markets at all. Maybe based on distribution networks and reciprocal credits. Maybe based on the production of “goods” like clean air and water; safe storage of radionuclides; health support systems including nutritious food. You know, the truly valuable things. I wonder if there will be enough runway foam to get there.

I wonder if there will be enough runway foam to get there.

I wouldn’t worry about it. The industrial civilization airliner is already in a flat spin with all engines flamed out and locked up. There won’t be any landing approach requiring a runway. Just a vertical drop and a smoking crater somewhere in the wilderness.

The “good news,” however, is that the market economy has already been pretty much completely replaced by the resplendent new military economy. So much more regal, and so much more efficient! And as long as there’s people, there’s enemies left to be exploited!

There are a lot of ways to get to jet fuel, less so gasoline (more so diesel). Ultimately Gas to Liquid technology can be plugged in the loop using natural gas or biomass feedstock to produce transportation fuels.

http://www.nrel.gov/biomass/

http://en.wikipedia.org/wiki/Gas_to_liquids

http://www.dsm.com/corporate/media/informationcenter-news/2014/09/29-14-first-commercial-scale-cellulosic-ethanol-plant-in-the-united-states-open-for-business.html

pdlane – You are mistaken on how things work. ALL resources and includes FX capital are priced in dollars.

Russia can sell their oil for any currency they want but the PRICE will be established in dollars. If Russia can convince the world that their currency is strong and stable and the Rouble is on par with or more valuable than the dollar and will stay that way, then that will be used to purchase Russian oil and other goods. I don’t see how they could possibly work this but who knows.

Now if we have a big war, Russia wins, and we have a new Bretton-Woods where the Rouble replaces the dollar then the world will be an entirely different place (but not in a good way). Those who say the world will come together and enact a new B-W like agreement eventually anyway, without war, are seriously deluded. IMHO

Just to point out that B-W was after the war, agree that WW III will be what’s required before the system is reset, my view is that historians someday will tell us it has already started. Right now we’re in the Phony War stage, a brief lull after initial hostilities, with the Ukrainian airforce pilot who pulled the trigger on the Malaysian jet as Gavrilo Princip.

One thing is clear. With Russia’s central bank policy rate at 17.00%, while its 10-year government bond yields 14.76%, the ruble yield curve is strongly inverted.

This implies that a harsh recession in 2015 is already baked in the cake for the Russian economy. It also suggests that Russian investors expect high short-term rates to be temporary. That is, the short term rate will likely be cut as the Russian economy weakens.

Russian 10-year is 16.28, reflecting expectations on future inflation.

Bloomberg (Dec. 17th):

http://www.bloomberg.com/news/2014-12-17/ruble-extends-worst-slide-since-1998-as-russia-crisis-worsens.html

————

That was 3 hours ago, presumably near the close of Russian bond trading.

You’re correct, my source is about 20 hours old.

You’re correct, my source is older than the bloomberg article you link.

These forecasts of Russian recession in 2015 aren’t worth much.

They all depend on another forecast – of low oil prices throughout 2015. And these may turn out to be dead wrong.

If the oil price recovers (not impossible – no one foresaw the recent drop; maybe no one is anticipating a possible near term recovery) the economy may even show a positive growth rate in the end.

The events of the last couple of weeks have shown the “markets” at their worst – managing expectations of an unknowable future in a state of total hysteria

You are expressing the standard neoliberal central banker belief.

My question for you is: should a nation which has a positive currency account balance, a debt to GDP which is in the teens, and has full foreign currency reserves to match its foreign currency debt obligations – expect the same actions to have the same consequences as a nation which has a 100% debt to GDP ratio, a negative currency account balance, but no foreign currency issues because all debt is denominated in its own currency?

Equally, whether Russia suffers from a recession isn’t really the issue – the real issue is if the EU’s recession is worse, and more importantly, acceptable to the EU people and government.

I’m not giving you “neoliberal belief,” I’m telling you what happens. The West is trying to break Russia’s banking system, which has dollar liabilities.

Russia itself is forecasting a bad recession for next year. It’s old GDP forecast was for a decline of IIRC 0.8%, which isn’t that bad. As of this week, it raised it to over an over 4.5% contraction.

And what does the comparison with the Eurozone have to do with anything? Russians don’t have EU passports. They can’t readily emigrate.

If you read this site at all, we have not been fans of what the US and its cats’ paws in the Eurozone have been doing. And the Russians have plenty of capacity to take pain. But what happens in a narrow economic sense as a result of the sanctions and the plunge of the ruble is not a matter of debate.

You might note that I haven’t said there won’t be a recession – however, you did not respond to my question on how well the EU and/or the US can hold up their side of the bargain. The possibility of an EU and/or US recession is far from a moot point.

I don’t have any doubt that what’s going on is a financial attack; the question is how successful it will be. While the Russian banking system does have some dollar liabilities – I have not seen any numbers which show that this is a fundamentally insoluble imbalance, especially with Chinese dollar reserves potentially available.

Perhaps you can comment on this since you are saying you know about it.

I’m not sure what you mean by “their part of the bargain”. We’ve regularly decried EU policies as misguided and deflationary. But this isn’t a competition as you imply. US policy has strictly been about the US, and then one can argue pretty persuasively, given the lack of average worker wage gains for decades, about delivering good results to the capitalist classes. The US sees itself as having no obligation to other countries on the economic front. Look at how QE is creating havoc for emerging economies. US policy makers regularly talk about being competitive.

The intent of the Western policies is to damage Russian banks and companies. I didn’t say they’d succeed. I expressed no point of view either way. You keep straw manning what I write.

“their part of the bargain” means is the EU willing to take the economic hit in order to carry through the policies clearly being pushed by the US.

As for straw-man – unclear what you’re talking about since all that was in the previous comment was a question. Which was not answered.

As for how US policies are affecting emerging economies and US consumers – no argument there. That’s also part of the bargain: how long can/will the 99% of the US population accept the crappy economic pie being handed to them in favor of foreign entanglements.

By Russian “investors”, do you mean sowers or predators…builders or plunderers…producers or parasites?

This was intended for Jim.

The reference is to all investors in Russian bonds collectively.

Governments regard financing as essential, whether investors provide it out of altruistic or selfish motivations.

Here is the record of gift contributions to the US Treasury:

http://www.treasurydirect.gov/govt/reports/pd/gift/gift.htm

Thank you for your generous support.

Thank you for your always interesting POV.

“Governments regard financing as essential, whether investors provide it out of altruistic or selfish motivations.”

Motivations are important, especially from the moral imperative perspective. Since you mentioned “Government”, I would be very interested in reading your opinion about its purpose. Is it a collective effort to solve collective problems or enforcement of an authoritarian power structure? I personally tend towards the former but I’m not sure you can legislate morality either way. I do think you can regulate conduct that has proven destructive.

As for debt, I believe Michael Hudson explains it as well as anyone, anywhere at any time.

http://michael-hudson.com/?s=debt

But, um, Russia is selling off its foreign reserves….

I wonder if the author was trampled on his way home from Moscow University by frantic shopppers buying before the dollars are gone.