Lambert here: Note the pervasive lack of agency: “[T]he intergenerational income and wealth divide has increased,” and so forth; one might almost imagine some sort of “divide and conquer” strategy were in play. And it does look like immigration would really be helpful, if the premise of “integenerational transfer” is accepted.

By Pia Hüttl, Affiliate Fellow at Bruegel, Karen E. Wilson, Senior Fellow at Bruegel, and Guntram B. Wolff, Director of Bruegel. Originally published at Breugel.

During seven years of economic crisis, the intergenerational income and wealth divide has increased in many European Union countries. This paper reviews the pension reforms implemented by several countries and it provides policy recommendations to address the intergenerational divide.

Highlights

- During the economic and financial crisis, the divide between young and old in the European Union increased in terms of economic well-being and allocation of resources by governments. As youth unemployment and youth poverty rates increased, government spending shifted away from education, families and children towards pensioners.

- To address the sustainability of pension systems, some countries implemented pension reforms. We analysed changes to benefit ratios, meaning the ratio of the income of pensioners to the income of the active working population, and found that reforms often favoured current over future pensioners, increasing the intergenerational divide.

- We recommend reforms in three areas to address the intergenerational divide: improving European macroeconomic management, restoring fairness in government spending so the young are not disadvantaged, and pension reforms that share the burden fairly between generations.

1. The emergence of an intergenerational divide

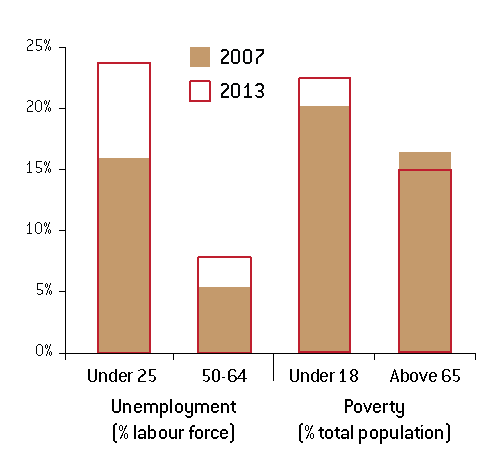

During seven years of economic crisis, the intergenerational income and wealth divide has increased in many European Union countries. In the bloc as a whole, young people on average have become significantly poorer, while poverty among pensioners has been reduced (Figure 1). Unemployment among the under-25s has risen notably while older workers (aged 5-64) have been less affected (Figure 2). While this pattern has been particularly pronounced in southern Europe, it can also be observed for the European Union as a whole.

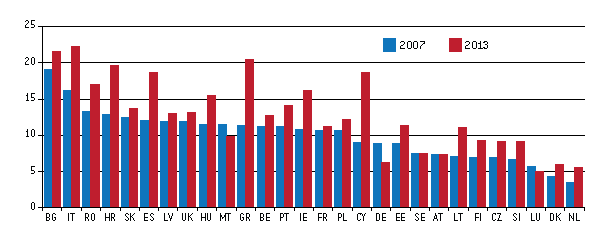

In the EU as a whole, unemployment in the 15-24 age group increased by 7.8 percentage points between 2007 and 2013, peaking at 23.7 percent in 2013, while unemployment among older workers in the 50-64 age group increased somewhat less, by 2.4 percentage points to 7.8 percent in 2013. A more precise measure of forced inactivity of young people is the ‘not in employment, education or training’ (NEET) rate, which varies significantly between countries. In the countries most hit by the crisis (Cyprus, Greece, Ireland, Italy and Spain), the NEET rate increased by more than 7 percentage points between 2007 and 2013, peaking at over 20 percent in Greece and Italy (Figure 2). By contrast, the NEET rate declined in Germany in the same period, from 8.9 to 6.3 percent.

Figure 1: Pre and post-crisis material deprivation rate and unemployment rate in the EU

Source: Bruegel based on Eurostat. Note: The material deprivation rate is defined as the enforced inability (rather than the choice not) to pay for at least three of: unexpected expenses; a one-week annual holiday away from home; a meal involving meat, chicken or fish every second day; adequate heating; durable goods such as washing machines, colour televisions, telephones or cars; or being confronted with payment arrears.

Figure 2: 15-24 year olds not in employment, education or training (%)

Source: Eurostat.

Material deprivation rates are typically higher for young people than for those aged 65 or over (Figure 1). In 2007, 20 percent of young people below the age of 18 were materially deprived, compared to 16 percent of people aged over 65. As with the NEET rates, there are major differences between countries. While less than 10 percent of young people faced poverty in Denmark, Finland and Sweden in 2007 (the proportion is even smaller for older people), more than 20 percent of young and old people were materially deprived in Cyprus, Greece and Portugal. In Latvia, Hungary and Poland about 40 percent of young people were poor.Figure 2: 15-24 year olds not in employment, education or training (%)

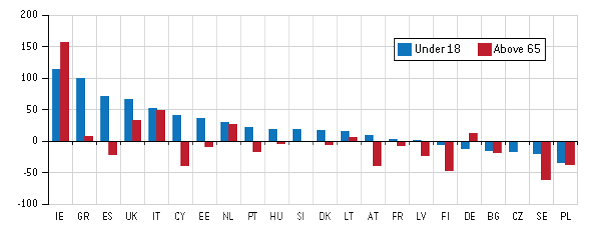

Figure 3 shows the percentage change per country in the material deprivation rate during the crisis (2007-13). The rate increased substantially more for the young compared to the old, especially in the countries hit most by the crisis (except Ireland), meaning that already high levels before the crisis in those countries were exacerbated. Only Italy and to a lesser extent the United Kingdom experienced deteriorating ratios for both the young and old. By contrast, Finland and Sweden, with low levels to start with, saw their respective material deprivation rates decline for both young and old people over the same period. The same is valid for Poland1.

Figure 3: Change in material deprivation rate (2007-13, %)

Source: Bruegel based on Eurostat.

Overall, a worrying picture emerges. First, poverty indicators have shown the emergence of an intergenerational divide, especially in crisis-hit southern Europe. Second, unemployment has become a major concern, with young people hit hardest during the crisis in the most stressed countries. Surges in youth unemployment and youth poverty are particularly worrying because they have long-lasting effects on productivity and potential growth, marking young people for their lifetimes, reducing their productivity and often excluding them from the labour market for an extended period of time (Bell and Blanchflower, 2010; Arulampalam, 2001; Gregg and Tominey, 2005). Youth unemployment and poverty also have negative effects on fertility rates and demographics, possibly because of increased income uncertainty related to unemployment and subsequent decisions to delay starting a family (Kreyenfeld and Andersson, 2014; Currie and Schwandt, 2014). The cost for the EU of a large proportion of NEETs is therefore much greater than the immediate short-term loss of foregone economic activity (Darvas and Wolff, 2014).

2. Key drivers of the intergenerational divide

The intergenerational divide that has emerged during the crisis has been driven by three important policy developments. The first is macroeconomic management. Unemployment responds to the business cycle, but youth unemployment reacts much more strongly to recessions than total unemployment. This is in part because younger workers disproportionately are on temporary contracts (Boeri, 2011). Other factors also matter, such as the difficulty for young people to prove their skills in recessionary periods when they are looking for work. Therefore, the intergenerational divide typically grows in times of recession. Second, structural changes to government spending are important. Fiscal consolidation measures in the EU during the crisis led to an increase in poverty rates (Darvas and Tschekassin, 2015). This raises the question of whether government spending has become less favourable for the young, increasing the share of materially deprived young people. Third, pension system reforms are hugely important for intergenerational equity. In the following, we deal with each of the three issues in turn.

Macroeconomic management

In times of crisis, generally speaking, the public sector steps in to smooth the impact of adverse developments, through automatic welfare policies (such as unemployment benefits), progressive taxation and discretionary policies such as investment programmes. Automatic stabilisers were broadly at work in the EU during the financial crisis in 2008 and 2009. However, during the sovereign debt crisis, budgets became constrained in some countries and they arguably cut government spending more quickly than would have been advisable from a stabilisation point of view. This substantially aggravated the recessions in those countries and increased unemployment and youth unemployment (Darvas and Wolff, 2014). In terms of investment, Darvas and Barbiero (2014) found that gross public investment declined in the EU during the European debt crisis, and even collapsed in the most vulnerable countries, exaggerating the output fall.

The composition of government spending

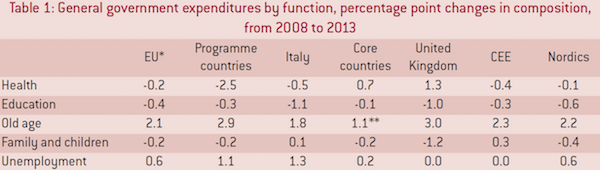

Table 1 shows the percentage point change in the composition of government spending in the EU from 2008 to 2013. Unsurprisingly, Greece, Ireland and Portugal, which experienced the sharpest fiscal consolidation in the euro area, and Italy saw unemployment expenditure increase substantially as a share of total expenditure as their unemployment rates soared. Spending on health grew in importance in the core countries (see Table 1 for definitions) and the United Kingdom, while it fell substantially in the programme countries, on the back of fiscal consolidation measures. The share of spending on education decreased slightly in the EU overall and fell substantially in the UK and Italy. The UK and the programme countries reduced their spending on families and children. By contrast, pensioners were the main beneficiaries of fiscal adjustments. Spending on this category increased in all countries and exceeded the EU average in the UK, the programme countries and, to a lesser extent, central and eastern European countries2. The composition of government spending therefore shifted from families and children and education towards pensioners, entrenching the intergenerational divide.

Pension reforms

Government expenditure on pensions can increase because pensions are considered to be more difficult to change than other benefits from a political point of view. Several member states introduced pension reforms during the crisis. Such reforms can benefit current pensioners at the expense of future generations or vice versa. The most important pension reforms happened in the stressed countries, especially in Greece, Italy, Portugal and Spain, because the crisis highlighted that their pension systems were not sustainable. From an intergenerational perspective, these reforms typically aim at increasing the sustainability of pension systems by reducing implicit debt obligations, and should therefore favour the young and future generations. In general, a successful reform should increase sustainability while not compromising adequacy of future pensions.

Moreover, all of this has to be understood in the context of rising EU life expectancy and declining fertility, which represent major challenges to future pension and health systems. The European Commission’s Ageing Report (2015) states that the EU will move from four working-age people per person over 65 today to about two working-age people in 2040. This will affect both revenue and spending: there will be less revenue because of the shrinking working-age population, and more spending because of higher costs for pensions, health and long-term care. To address these challenges, several EU member states have enlarged the role of pre-funded, privately managed schemes as opposed to the prevailing statutory, public, pay-as-you-go schemes (OECD, 2014)3. There are, however, clear limits to what such schemes can achieve.

To see to what extent the intergenerational divide has been affected by reforms in the crisis years, we carried out an analysis of changes to benefit ratios, meaning the ratio of the income of pensioners to the income of the active working population (Box 1) Pension reforms that do not affect intergenerational equity should leave the benefit ratio unchanged. We considered (a) how the current benefit ratio changed over the crisis period, (b) how the 2060 benefit ratio changed over the same period and (c) how the relationship between the two ratios has changed. It is the latter that best captures the ongoing intergenerational changes in the pension system.

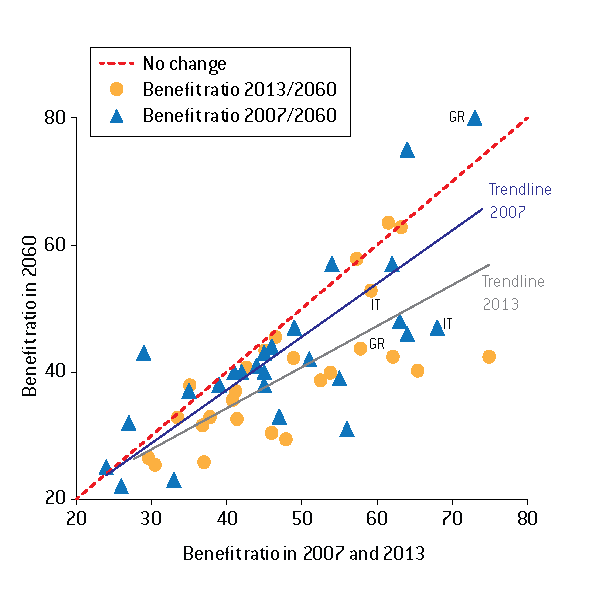

Figure 4 compares the benefit ratios in 2007 and forecasts for 2060 to their current counterparts, the 2013 benefit ratios and their respective 2060 forecasts4. In 2060, current 20-year olds will be approaching or already in retirement, making it a useful year to discern the effect of current reforms on today’s young. A perfectly equitable pension scheme should safeguard the benefit ratio for those that will retire in or around 2060, keeping it the same as the current ratio.

Figure 4: All pensions benefit ratio, 2007/2060 and 2013/2060 (%)

Source: Bruegel based on European Commission Ageing Report (2009 and 2015 edition). Note: the benefit ratios take into account both private and public schemes.

In 2013, Denmark, most continental welfare states and the United Kingdom were close to the 45 degree line and can therefore be considered to have relatively equitable pension systems. All other countries were below the 45 degree line, indicating a bias towards today’s pensioners, resulting from a smaller future benefit ratio compared to today’s ratio.

Analysing how the ratio has changed during the crisis allows us to track the impact of pension reforms and other factors on the intergenerational justice of the pension system6. Compared to 2007/2060 benefit ratios, the countries most under stress from the crisis reduced their 2013/2060 benefit ratios. Greece moved from a benefit ratio biased towards future generations in 2007 towards a benefit ratio that favours current pensioners (also highlighted in Figure 4). Spain and Cyprus moved from a more-or-less balanced position in 2007 to a system biased in favour of current pensioners, while Portugal increased its benefit ratio for both current and future pensioners, not changing the burden-sharing between generations in a significant way. Meanwhile, Belgium did not change its position, while Austria curtailed entitlements for current pensioners, moving closer to the 45 degree line. Germany reduced its 2013/2060 benefit ratio compared to 2007/2060 for both current and future pensioners, not changing the bias towards current pensioners significantly.

Denmark moved towards a more just intergenerational burden-sharing, by reducing the benefit ratio of future pensioners, while Sweden reduced entitlements for current and future pensioners, without improving its position. Romania and Hungary moved from balanced burden-sharing to significantly favouring current pensioners, while Bulgaria and Poland curtailed entitlements for both current and future pensioners, not affecting their intergenerational burden-sharing. A notable and important exception is Italy: compared to its 2007/2060 benefit ratio, its ratio for 2013/2060 marked the greatest shift among EU countries towards a more just intergenerational position. Italy achieved sustainability in its pension system not by cutting the future benefit ratio, but by reducing the current benefit ratio, thus improving intergenerational burden-sharing (see the Annex for more details).

This analysis suggests that overall entitlements have been curtailed in many countries to address sustainability questions, but the burden seems not to have been shared equally, favouring current over future pensioners, especially in crisis-hit southern Europe (Italy being an exception).

3. Ways forward: Policies to address the intergenerational divide

Measures to address the intergenerational divide could include policies against youth unemployment, rebalancing spending and more equal burden-sharing between generations in pension scheme designs.

One of the biggest legacies of the crisis is high youth unemployment. Bentolila et al (2010) and Boeri (2011) argue that the tw o-tier system with ultra-secure permanent workers and vulnerable temporary workers (who are often the young entering the labour market) is a major factor behind the high rate of job losses among younger workers during recessions. It also suggests a possible solution: labour market reforms that allow for graded job security as workers acquire tenure. However, such reforms are unlikely to yield significant job benefits in a situation of depressed demand. Other measures to counteract youth unemployment, such as the Youth Guarantee7, are a step in the right direction but are hardly adequate as a counterweight to national policies; in addition, the European Court of Auditors has questioned the adequacy of such policies8.

Beyond such structural measures, adequate macroeconomic policies are important in order to prevent a significant increase in unemployment. In the context of the euro-area crisis, some sort of shock absorber on the euro-area level could have helped mitigate the adverse impact on the economices of member states. In the short term, we are sceptical about creating major European stabilisation functions such as a European unemployment insurance scheme (Claeys et al, 2014). Such measures, such as the euro-area unemployment insurance scheme proposed by former European commissioner Laszlo Andor, could prove effective but would require an extraordinary effort to create harmonised European labour market legislation.

Instead, for the euro area we would recommend an enhanced, symmetric and binding policy coordination framework for fiscal policy, as outlined in Sapir and Wolff (2015). The main reason we advocate this step is that 98 percent of EU government spending is national. Macroeconomic stabilisation therefore works through national budgets. It is of central importance that national public finance is cautiously managed in good times, in order to have enough fiscal leeway in bad times. However, a system relying exclusively on national policies would be inadequate for the monetary union for two reasons: Irresponsible fiscal policy can have substantial cross-border spillover effects; and the sum of national fiscal deficits does not add up to an adequate fiscal stance for the euro area as a whole. A deeper coordination framework that is binding in exceptional times should therefore be created, to prevent unsustainable fiscal policies, while it should ensure that countries provide adequate stabilisation for the area as a whole.

For countries outside the euro area, fiscal policy, monetary policy and the exchange-rate channel should play their full role in mitigating shocks.

In terms of burden-sharing between generations, we have found that current pensioners have been protected compared to future pensioners (Italy being an exception). Safeguarding a constant benefit ratio over generations by adjusting contribution rates for the working population and benefit levels for pensioners would enable better intergenerational burden-sharing9. This would counteract the limitations of existing fixed-contribution or defined-benefits schemes, under which adjustment would eventually fall only on the younger or on the older generation. Following a Musgrave rule, rising unemployment among the younger generation would mean that the contribution rates for the younger generation rise, but benefits for the older generation would decrease too, to keep the benefit ratio constant. Therefore, both parties ‘lose’ at the same rate, allocating the burden in an equitable way.

However, it is not only pension reforms along the lines outlined above that are needed. As noted by Myles (2002), the aggregate well-being of future generations depends primarily on the quality and quantity of the stock of productive assets (including human and environmental capital) that they inherit or create, and not so much on the design of pension systems. We have shown that during the crisis, social spending on families and children, and on education, was preserved less in the UK and in Italy, and held constant in the countries that faced the highest youth unemployment rates. By contrast, policies aimed at education and child care, one of the pillars of the social investment strategy, could play a major role in addressing the intergenerational divide. Children are the future workforce, and investing in better education and affordable child care will lead to higher levels of productivity and employment (Hemerijck, 2013). Education is also important as a policy measure to reduce income inequality. By increasing access to high-quality education, greater equality of opportunity is fostered, which in turn contributes positively to economic growth (OECD, 2015a). Also, as pointed out by Vandenbroucke and Rinaldi (2015), investing in education and child care can reduce intergenerational gaps.

Overall, we are concerned that the crisis has left a dangerous intergenerational legacy. Addressing this legacy by making the government spending mix fairer for the younger generation while re-establishing intergenerational equity in pension schemes, should be a priority for policymakers throughout much of the European Union.

Very interesting. Unfortunately, I don’t see my country addressing the problem any time soon (even worse, now if, indeed, the present PM-to-be gets to be PM).

two-tier system with ultra-secure permanent workers and vulnerable temporary workers (who are often the young entering the labour market)

Part of the general crapification trend by employers.

Contagion spreads then. Noting like the affects of free trade at work, because jobs, including yours, can be easily outsourced.

This was the famous deal between Reagan and O’Neill to “save Social Security.” People in my age cohort “paid for”[1] a top-up of our parents’ Social Security, and imagined we were “paying” for our own; younger people ended up with progressively worse benefits. And thus a two-tier system was introduced, with predictable divide and conquer effects. Any Social Security reform should eliminate this disparity; it’s unconscionable that people lose dignity in old age because they were born after a certain date.

[1] Federal taxes do not “fund” spending.

If only they had made it illegal to use the pension funds as collateral for government debt.

Nonsense. The collateral for Government Debt is the Government’s powers both to create new money (interest) and to tax.

Debt is money. Interest bearing accounts.

There is nothing stopping the Government for elimination interest bearing accounts (bonds) and by crediting them with credit non-interest bearing accounts (money).

When I see things like this:

Then I know the rest of the conclusions are to be doubted as well.

Leaving out the pensioners of the discussion for a while and instead focus on the ones still in the workforce and then something else might come to light.

The ones who got a job when times were good are (of course) reluctant to give up something for nothing so that the ones currently out of a job can get something. If the ones who got a job when the times were good are ever to give up something then they might have to be offered something in return. That something might be: Give them more free time in return for less hours worked and less pay. That would allow the ones on the outside a chance to get in and all would have stronger bargaining position against employers.

Sadly people still believe that lump of labour is a fallacy. I suppose that belief is a comfort and who’d ever doubt anything that economists claim?

& how easy is it to conclude that there is a lump of labour? Either there is an unlimited number of jobs or there is a limit to the number of jobs. People who claim that lump of labour is a fallacy are actually in effect believing that there is an unlimited number of jobs (paying a living wage). In a finite world there are few unlimited things and I doubt that there are an unlimited number of jobs. If salary is allowed to go to zero then I stand corrected, the number of jobs are then indeed infinite….

You miss the societal dimension. Socialists aim for full employment. Neo-Liberals aim for maximum profits.

What neo-liberals do not understand (or do not want to understand) is the savings by unemployment is offset by the cost of policing.

It is all about the flow of money being created by Government, under socialism it goes to the poore, to be spent, and thus grow the economy, under neo-liberalism new money goes to the rich as debt service by rent, where is is given to the financial sector to “manage” (gamble through bubbles).

This kind of propaganda is a way to prevent people from really seeing the qualities that others possess. It’s just wrong.