Think it’s scandalous that the average 2014 pay of the CEOs of the 500 biggest companies was 373 times that of the typical worker, as the AFL-CIO reported? You aren’t scandalized enough. Their take home pay, which is reported in the bowels of SEC filings, as opposed to the Summary Compensation Table that the AFL-CIO, along with most analysts and reporters rely on, was a stunning 949 times that of the average worker in 2014.

How did this massive disparity come about, and why is the SEC on the side of such gross understatement?

An important new paper by William Lazonick and Matt Hopkins, which is recapped in detail in The Atlantic, explains this gaping disparity. The culprit is the differences in the approach used to measure stock-related compensation, which is the bulk of top executive pay.

The widely-used, readily accessible pay reports in the SEC-mandated Summary Compensation Table uses an approach called “estimated fair value” (ESV), which is a Black-Scholes options value based method. That may sound technical and therefore be presumed to be accurate, but Black-Scholes models are based on all sorts of efficient markets assumptions, namely, that everyone has the same access to information, which is clearly not operative with CEOs. Not only do corporate insiders have an information advantage, but CEOs can and do take active steps to boost stock prices, like engaging in buybacks, and they have advanced knowledge of when those programs are to be announced. So it should come as no surprise that CEOs can time when they execute their option on when to sell stock far better than an ordinary investor. And that’s confirmed by the results shown in the obscure Option Exercises and Stock Vested table, which is based on “actual realized gains” or ARG. And this is a real, hard dollar figure. Per the Atlantic story:

ARG is a figure that permits the calculation of senior executives’ actual take-home pay—the number they report in their personal-income tax filings with the Internal Revenue Service.

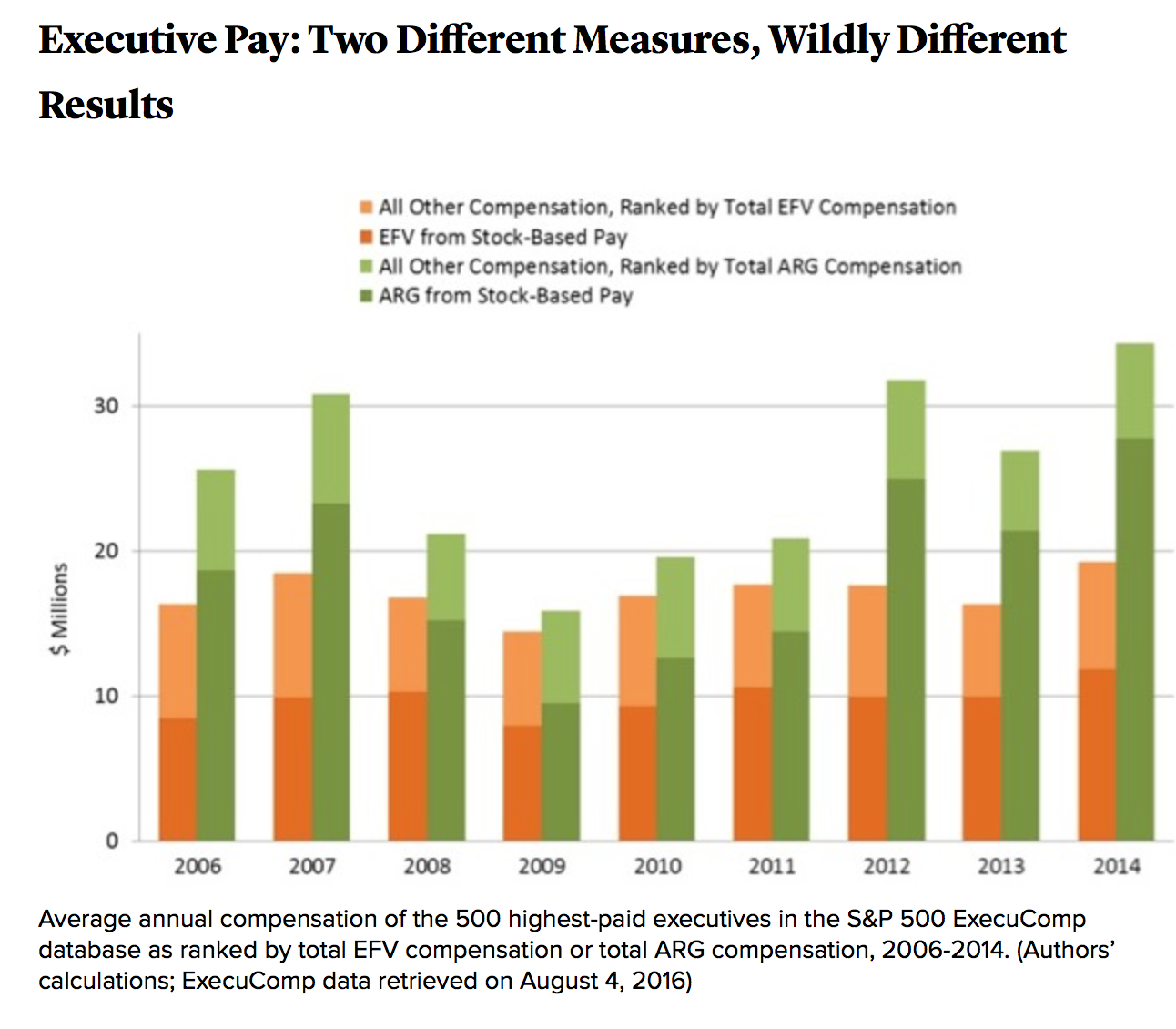

Moreover, the disparity in favor of ARG is consistent over recent years:

As the authors explain in the Atlantic:

EFV tends to understate ARG because its estimation methods, which seek to value stock-based pay in advance of realized gains, fail to capture actual stock-price increases and the timing of realized gains. In the case of stock options, the mathematical models, known as Black-Scholes-Merton, that are used to generate EFV assume that stock-price changes are distributed such that one should expect lots of small changes but very few large changes in stock prices. EFV is recorded as compensation in the year in which shares in an option vest, using the grant-date stock price in the estimation model. But, in timing the exercise of the options and generating ARG, executives are on the lookout for large stock-price increases, which will be driven by some combination of innovation, speculation, and manipulation. Black-Scholes-Merton-type models capture none of these three drivers of the stock market, whereas top executives can to some extent influence all of them.

The underlying paper gives examples of how large the differences can be. For instance (emphasis original):

One dramatic example of this difference between fair-value and realized-gains measures is the total compensation of John C. Martin, CEO of Gilead Sciences, a drug company that has been in the public spotlight since 2013 because of the extraordinarily high prices of its Sovaldi/Harvoni medicines for Hepatitis-C.

Based on the sales of these drugs, Gilead’s revenues soared from a two-year total of $20.9 billion in 2012 and 2013 to $57.5 billion in 2014 and 2015, while the company’s profits escalated from $5.7 billion to $30.2 billion. Gilead’s stock price tripled during 2014 and 2015, boosted not only by its monopoly pricing of Sovaldi/Harvoni, but also by $15.3 billion in stock buybacks…..

In an op-ed entitled “Gilead’s greed that kills,” economist Jeffrey Sachs accurately describesGilead as a company “driven by unquenchable greed,” and goes on to say that “Gilead CEO John C. Martin took home a reported $19 million in [2014] compensation –the spoils of untrammeled greed.” But the figure of $19.0 million, which is reported as Martin’s total 2014 compensation in the Summary Compensation Table of Gilead’s proxy statement, includes the estimated fair-value measures of Martin’s stock

-based pay, not his realized gains.In 2014 Martin actually took home $192.8 million, and in 2015, when his estimated fair-value pay was $18.8 million, his actual take-home pay was $232.0 million. From 1996 through 2015, as Gilead’s CEO, Martin’s estimated fair-value compensation totaled $209 million but his actual realized-gains compensation totaled $1,001 million, of which 82 percent came from stock options and 13 percent from stock awards. Gilead’s drug-pricing policies and its stock buybacks helped Martin extractthis massive stock-based pay. If $19 million in annual compensation can be called “the spoils of untrammeled greed,” what should we call the $193 million and $232 million that the Gilead CEO

was actually paid in 2014 and 2015?

Why is the SEC giving pride of place in shareholder reports to what Lazonick and Hopkins correctly call a mismeasure of executive pay? Historically, disclosure on compensation covered only cash amounts. In 1994, the agency implemented the Summary Compensation Table which included other pay elements. Companies also had to report ARG from exercised stock options.

So far, not so terrible. But in the 1990s, tech companies used options and stock awards for employees of all levels as a recruitment tool, and this practice became even more popular in the dot-com era. These options were dilutive, and investors wanted to measure their impact. The FASB latched upon EFV as a good estimate for the cost of these grants. But as we’ve discussed, this wasn’t a good technique for senior executives, who are uniquely able to identify windows when the stock price is trading at unusually attractive levels and take advantage of that. As Lazonick and Hopkins stress, “… the FASB would probably not have implemented EFV for reporting stock-option compensation expenses in 10-K filings.” Yet the agency has declared this dodgy metric as “the cornerstone of the SEC’s required disclosure on executive compensation” when it revised its Summary Compensation Table in 2006. And as the authors lament in the Atlantic:

Sadly, the SEC’s rules about corporate disclosure are moving in the wrong direction. Next year, as mandated by the Dodd-Frank Act of 2010, the SEC’s Pay Ratio Disclosure Rule will go into effect, requiring companies to publish the ratio of their CEO’s pay to that of their median employee’s. However, the SEC instructs companies to report these ratios using EFV measures of executive pay, not ARG measures—furthering the systematic underestimation of U.S. income inequality.

Needless to say, the actual riches that CEOs have been able to garner via stock price manipulation via buybacks that since 2006 have consumed more than half of net earnings, as well as the regular use of accounting tricks, have been widely lamented for producing rampant short-termism, looting, and slow liquidation of these enterprises, often masked by acquisitions. This isn’t capitalism, it’s rent extraction by well-placed insiders. Obscuring its true, obscene costs helps keep this diseased system going.

How long before the revolution starts, guillotines and all?

Hey SEC, who’s side are you on?

https://www.youtube.com/watch?v=4IgVfmvbd0I

(silly question, I know, as it’s obviously not ours)

This insane situation has been caused by our leadership/lawyer class as well as political correctness gone wild. I treat a lot of prisoners. Most have Hepatitis C and numerous lawsuits have required the prisons to provide Hep C treatment which costs the taxpayer up to 450,000 per year per patient. What we see over and over is that they get “cured’ and then do more tattoos or anal sex or whatever and get reinfected and then the 450,000 cycle starts over again. This cycle is exactly what we see when they get out as well. I would like to see what proportion of Gilead’s sales are coming from government tax revenues. I would guess it is the majority. That means that the outrageous prices are supported by our lawmakers presumably influenced by these pharmaceutical executives. These unfortunate patients are a wonderful vector allowing these executives to make dynasty creating money. This is just a drop in the bucket but it goes a long way to explaining why the US economy is a disaster for everyone except these rent seekers. I wonder how much the democratic establishment has been paid by Gilead and the other pharma frauds. How far we have come since Fleming, who gave us penicillin without a patent. The numbers in the following article are dated since they are now much higher but https://www.washingtonpost.com/national/health-science/medicare-spent-45-billion-on-new-hepatitis-c-drugs-last-year-data-shows/2015/03/29/66952dde-d32a-11e4-a62f-ee745911a4ff_story.html

Big pharma is #1 in lobbying spend by far.

https://www.opensecrets.org/lobby/top.php?showYear=2016&indexType=i

And further down the list are Health Services, Hospitals and Health Professionals in separate categories!

As Bill Black says, lobbying and campaign contributions produce the highest Return on Investment of any expenditure that can be made.

Why can’t the gov’t negotiate drug prices? and on and on and on……

Excellent reporting Yves.

Regarding Gilead’s rent seeking, Fortune ranks them the 5th most profitable U.S. company ( 2015 annual profits ). Of their $18.1 billion profits, Hepatitis C drugs accounted for $19.1 billion:

http://fortune.com/2016/06/08/fortune-500-most-profitable-companies-2016/

Hepatitis C drugs have driven their profits higher than every other U.S. company in 2015 except Apple, JP Morgan, Berkshire Hathaway, and Wells Fargo. If you’re interested in the sausage-making process of how these drugs are priced, there have been some articles to discuss this:

http://www.bloomberg.com/news/articles/2015-12-10/behind-the-1-000-pill-a-formula-for-profits-inside-gilead

The short version is that Medicare is the biggest U.S. drug purchaser, so Pharmaceutical Companies hire ‘consultants’ to perform detailed Surveys of health insurance and Medicaid plans to determine the maximum “acceptable” price for a drug that will not trigger ( Medicare ) coverage restrictions, which limits Annual Sales of the drug. This is commonly referred to as Access-Optimized Pricing. In this case consultants convince Medicare the maximum “acceptable” drug price is close to the lifetime cost of Hepatitis C treatment before Gilead’s cure was available. This is one reason why revenues can exceed drug development costs by astronomical quantities.

Securing a high priced Medicare ‘rent’ guarantees a government subsidized bump in the CEO’s pay which they are free to under-report to shareholders as discussed in this post.

Felix_47: I agree. But next to leadership/lawyer class do not forget the vast majority of headhunters. Let’s call these group the yay-sayers. You can recognize them based on two features:

1. their charging a fee based on the contract volume of the vacant position to be occupied (instead of charging a fixed fee based on the actual difficulty of a search);

2. they are giving their blessing to whatever explosion in executive income you may imagine. That blessing usually takes the form of a “compensation study” not worth the paper it’s on (sample size? number of selectors? alternative candidate compensation?). Media presence does the trick as well – articles about income benchmarks sell.

Last time I checked, 75% of executive positions in the US were filled with the help of headhunters. So yes. This type of headhunters are to executive compensation what risk rating agencies are to financial products. But the former are more important than the latter when looking at income discrepancies and the rise of feudalism.

OBSCENE!!!

Spanish saying: “lo bueno, si breve, dos veces bueno”

Google translation: “the good, if brief, twice good”

My own;”Good stuff, briefly expressed, twice the good”

wow. You last para is spot-on. The 1992 law about stock options was, I think, supposed to align managements’ interest more closely with investors, on the theory that closer alignment with investors would produce stronger companies. That alignment, however, isn’t with actual companies real interests. (outside of share price.)

Thanks for this post.

This post illustrates the degree to which executive pay in large corporations has become so objectionably obscene and vulgar.

These executives are part of the basket of irredeemable deplorables of TPTB in our society. (Killary Killington & Donald Dummkopf also fit within this basket.)

I couldn’t finish eating my breakfast this morning while reading this post.

Pure pornography! Yves, your site well deserves its name!

Actually, whole of the disclosure requirements of the U.S. sucks. They disclose very limited information and that too in a very confusing manner. Sadly, most of the investors doesn’t care about such things as far as share price remains high because nowadays they intend to hold shares for a very short term.

You betcha!

Given the choice between reporting, like, ya know,, an actual number, and some estimated ‘value’ requiring complex mathmatical models, which would you expect them to prefer?

“Really, its very complicated, you wouldn’t understand”, they tell me.

Why don’t we put a cap on multiples of average salary. For example, let’s say the average salary is $65K and the cap is 40. The most the CEO or anyone else can make is $2.6m.

Somehow our planet did just fine back when the multiple hardly went over 20.

I always go back to a field analogy. At what point, do we recognize, (and legislate away), the positive absurdity of thinking that one man can do the work of 370?

It’s so dangerous that we’re in a world of such extraordinary information and transportation technologies. This allows the CEO to exist in a universe so far removed from the workforce or manufacturing base (when it applies). If businesses were still in villages and regions, we’d have seen a guillotine by now.

You are right; it’s way too depressing to read about the problem without immediately thinking about a solution.

But these people are already too powerful for direct countermeasures. We are already in a feudal environment where income caps will probably fail as soon as anyone will try to implement them. People who earn 900 times the average salary will not simply sit still and wait for their opposition to organize. They will use their money to bribe, split, criminalize and discredit whoever gets in their way. Or worse.

But if wealth is the problem, it is also the solution. Employee-owned companies (EOC) are the one way out of quite a few other quagmires we got ourselves into. EOCs aim at increasing the wealth of their employees and have strict caps on the min-max span of incomes within their structures (max cap is usually at 5-8 times the min income). There are numerous legal forms under which a company can organize as such (ESOP, coop, etc. but most other can give itself a structure accordingly). And if there is one thing for sure: they are more profitable than their direct competition, without being a silver bullet (they do declare insolvency, even if certain interest groups would like to make you believe otherwise).

My concern is that “wealth” redistribution isn’t really possible or moral. I consider it ex post facto. So, I think the only route is income/gains. Can’t change the past, but can change the future.

I like the EOC idea, but who’s going to start them and how? We’ve got Credit Unions, but they don’t seem to be gaining any traction on banks. For a small business starting out, who’s going to be the ultimate decision maker? (I need to educate myself more on EOC’s and perhaps I’ll find the answer.)

The real problem is that nothing can really change so long as we’ve got millions of “temporarily embarrassed millionaires” running around. No guillotines with them around.

You’re right, the only route is income/gains, not “wealth” in the proper sense of the word. It is a long-term strategy, and/but it is working. If you live in the US, ESOPs are the fastest growing form of EOCs (not coops, surprisingly). That’s where I suggest you can start reading. The Cleveland Model is a practical functioning example. There are also organizations like BALLE. The only book I know from a worker-owner is “The Company We Keep”.

Europe is a mixed picture. EOCs are huge in Denmark and Scandinavia. You probably have read about the largest coop worldwide, Mondragon (Spain). Greece’s Syriza based their economic plattform on them before winning the election (and abandoned them afterwards, for all I know.) The list can go on.

The extreme inequality in salaries reminds me the famous video showing that monkeys fed with different fruits also have a sense of justice. The fact that this is not uniquely human shows that the sense of justice is evolutionary relevant and migth favour the survival of the species as a group rather than the individual approach. The fact that these guys seem to regard the competitive advantage of the individual as superior achievement, while their are benefiting from the strength of the group (the companies they manage, and the strength of the whole society) is so contradictory, and the double morale they apply is so obvious, it could be considered a mental disorder. Monkeys are more judicious…

Fantastic comment.

Collabiarators with HELLIARY !