By Lambert Strether of Corrente.

Spoiler: I don’t think so. CSR stands for Cost Sharing Reduction, and one of the ways Trump has sabotaged — or, depending on the outcomes of the Alexander-Murray bill, threatened to sabotage — ObamaCare is by threatening to cut them. From the White House Press Secretary:

Based on guidance from the Department of Justice, the Department of Health and Human Services has concluded that there is no appropriation for cost-sharing reduction payments to insurance companies under Obamacare. In light of this analysis, the Government cannot lawfully make the cost-sharing reduction payments. The United States House of Representatives sued the previous administration in Federal court for making these payments without such an appropriation, and the court agreed that the payments were not lawful.

The effect could be to throw the ObamaCare marketplace into chaos, and hurt poor people. Business Insider:

The payments were introduced by the ACA to help offset the cost to insurers of offering affordable plans to poor Americans. Insurers have repeatedly warned that if the payments were cut off, they would be forced to raise premiums to make up the financial loss.

“Raise premiums…” But how? And what happens then? Some states, including California, seem to have managed to dodge the CSR cut bullet by manipulating the prices of ObamaCare’s Silver plan. Timothy Jost, Health Affairs (October 13):

The effect of CSR payment termination, however, will depend heavily on how insurers deal with the change. In several states, including California, insurers have anticipated the termination and have already loaded the lost payments into their on-exchange silver plans. In other states, however, insurers have to date been instructed to assume that the payments will be made, or have been given no instructions whatsoever. In these states, the change is likely to cause considerable confusion. Insurers will have to refile their rates and will likely not be able to do so before open enrollment begins in three weeks. For more on the different responses insurers may have take, see here.

(Other potential states: “California, Connecticut, Florida, Idaho, North Carolina and Pennsylvania.”) Let’s unpack that phrase “loaded the lost payments” a little. The idea for this manipulation — there’s really no other word for it — seems to have been explained first in Kaiser Health News back on April 17, 2017:

Any systematic increase in premiums for silver marketplace plans (including the benchmark plan) would increase the size of premium tax credits. The increased tax credits would completely cover the increased premium for subsidized enrollees covered through the benchmark plan and cushion the effect for enrollees signed up for more expensive silver plans. Enrollees who apply their tax credits to other tiers of plans (i.e., bronze, gold, and platinum) would also receive increased premium tax credits even though they do not qualify for reduced cost-sharing and the underlying premiums in their plans might not increase at all.

We estimate that the increased cost to the federal government of higher premium tax credits would actually be 23% more than the savings from eliminating cost-sharing reduction payments. For fiscal year 2018, that would result in a net increase in federal costs of $2.3 billion. Extrapolating to the 10-year budget window (2018-2027) using CBO’s projection of CSR payments, the federal government would end up spending $31 billion more if the payments end.

This assumes that insurers would be willing to stay in the market if CSR payments are eliminated.

The key insight is that ObamaCare subsidies are indexed to the price of the Silver benchmark plan (“The second lowest cost Silver plan in a state is used as the benchmark plan when determining subsidies”) and so if the price of the Silver benchmark plan goes up, the tax credits to the “customers” go up too, so the cost to them can net out to zero, or even better.

(Note that Sarah Kliff at Vox on May 15, ACA Signups on July 31, the CBO in August 2017, and Jonathan Cohn at HuffPo on October 15 all present variations of this basic idea which they seem to have independently arrived at. This should not be taken as a criticism of any of these sources, but as an indicator of the insane complexity of ObamaCare.) Sarah Kliff gives the clearest, because simplest, explanation of how this would look to the insurer and the customer:

Trump announces he won’t fund the CSR payments in 2018, so I [that is, the insurer] need to raise my premiums to cover that loss. [Here comes the manipulaton.] I jack up the price of my silver plan to $120, but don’t change the price of the bronze or gold plans, because the subsidies don’t apply there.

One of my [sic] enrollees earns $17,820 (150 percent of the poverty line). Under Obamacare, the government will give her a subsidy big enough that she needs to only spend 4 percent of her income — $60 each month — on a premium for a silver plan.

In 2017, this person got a $40 subsidy to afford my $100 plan. In 2018, she’ll get a $60 subsidy to ensure her monthly payment stays the same.

But this enrollee doesn’t have to stay in the silver plan. She could take her new, bigger subsidy and use it to help afford the $140 gold plan. Or she could buy the $60 bronze plan and pay nothing out of pocket at all.

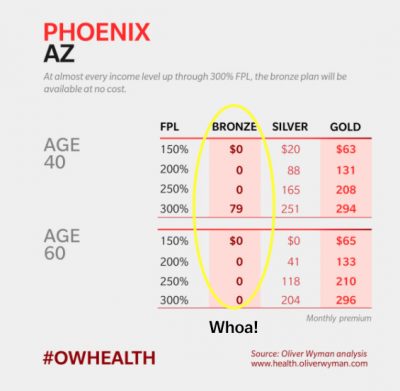

Here’s how Cliff’s source at management consulting firm Oliver Wyman envisaged the result, after jacking up the price of the silve plan, and how it would look to “consumers” in Phoenix, AZ:

The Silver Switcharoo

Sounds great, but I see a few problems.

First, the solution — following ACA Signup’s ingenious post, we’ll call it the “Silver Switcharoo” — is complicated and hard to communicate. If you don’t believe me, you try reading those links. I guarantee you won’t be reading them only once, and you’ll notice the tax on your time.

Second, the Silver Switcharoo assumes that all health care “consumers” are “smart shoppers.” That’s not true. From the NBER: “We find no evidence of consumers learning to price shop after two years in high-deductible coverage.” Granted, that’s health services, not health insurance, but talk to anyone who’s cobbled together some sort of coverage plan, and you will see they are very reluctant to risk changing.

Third, your true “smart shoppers” may simply pay the penalty regardless. Again the NBER: “[E]ven under the most optimistic assumptions, close to half of the formerly uninsured (especially those with higher incomes) experience both higher financial burden and lower estimated welfare” after purchasing Silver or Bronze Plans. Will this population react to the headline price, or the net after subsidy? I’m guessing the former.

Fourth, all of these approaches, though well-intentioned, assume (though not, to its credit, ACA signups) that the administration will remain passive, and not counterpunch to the price manipulation. One obvious thing they could try is controlling the navigator curricula and marketing materials to avoid mentioning the Silver Switcharoo at all. A second obvious way, for the states that rely on the Federal Exchange, would be to make the UI/UX for the Silver Switcharoo hard to use. No reason the site has to look as nice as Oliver Wyman’s screen dump! And the Trump administration being the Trump administration, I’m sure there are cruder methods that could be employed. I mean, is the Administration really going to spend $2.3 billion on a program it wants to dismantle because California thinks it’s a good idea?

Finally, the Silver Switcharoo is proof, if more proof were needed, that ObamaCare is random with respect to jurisdiction in its coverage. If you live in California, Connecticut, Florida, Idaho, North Carolina or Pennsylvania, you might be on the train to Happyville. Otherwise, you’re going to Pain City! So let us dispense, once and for all, with the delusion that ObamaCare is universal, or even fair.

In summary, the well-intentioned and intelligent health care wonks who have fought their way through the complexity of ObamaCare’s marketplace to invent the Silver Switcharoo remind me of the Ptolemaic astronomers, who sought to “save the phenomena” by adding more and more epicycles. Simple, rugged, proven single payer: Why can’t we like Copernicus and put health care and the patient at the center of our system, instead of the market?

My father has sold small group health insurance, as a general agent, for my entire lifetime. I’ve grown up with this stuff and *I* find it challenging to compare plans and price shop. I’m college educated and work in the “knowledge economy”.

What possible hope does anyone without that background have?

A tax on citizens’ time indeed. The entire system is as perverse as the primacy of markets is pervasive.

I sold such plans and I completely agree. Also, ~40% of those 65 and older don’t have internet access. When I comparison shop for Medicare supplements and Part D plans, the internet is invaluable for comparing plans based on relevant variables. How one might do this effectively without internet access is beyond comprehension.

Thanks for both of your comments, based on actually having been in this line of work.

Yet again the NC commentariat rules.

Here’s how the Illinois insurance commissioner did it; apparently there are “over two dozen states” that have worked out a similar fix (probably in collaboration with one another over the summer).

It’s totally insane, of course – the complexity of the system is self-defeating even for the most technologically literate and healthcare savvy. An absolutely perfect example of the power of information asymmetry.

“A tax on citizens’ time indeed…”

You have no idea (well not you personally).

My wife and I have spent dozens of hours over the last 2-3 years just trying to understand our status vis a vis ACA coverage. And that’s a conservative estimate.

Now, our case seems to be fairly particular. What I mean is the particulars of our situation have led to us consistently finding “the hidden joints” of the contraption that is the ACA. I don’t have time right now to give a full explanation, but I will say that no less than 5-6 times we’ve tried to get a determination on questions re: coverage and other associated issues to discover that neither Healthcare.gov reps nor the insurance companies’ reps know the answer–and, even better, a few cases where there appears to be no established determination or precedent whatsoever. Yes, literally no one can answer the question. Kafka would be genuinely envious of the encounters I’ve had.

Point being, the insurance companies and the .gov marketplace do not understand or know how to navigate this system beyond its most basic functions. What hope does the average goof have? It’s an absolute Byzantine waking nightmare and without radical overhaul and simplification I fully expect it to collapse on itself–aided, of course, by the thousands of political liars and corporate rent-seekers who use it for their own purposes.

I won’t even bother to address the fact that it’s nothing more than just catastrophic coverage for us ($6,500 deductible) and thus really just a bit of psychological ointment that we are paying monthly premiums for.

That’s not health insurance. That’s death’s door insurance. Just this side of life insurance in terms of what has to happen for it to pay out.

North Carolinians have gotten our notice from NC BCBS and it’s ugly insane increases. They are throwing us off our pre-ACA plans onto the ACA. Rates going up 100-300 %.

THIS appears to be how NC BCBS is funding the ACA this year — on the backs of the middle class kicked off their semi-affordable “private” plans and into exorbitant premiums.

Mine went up 120% — from $650/month to $1430/month.

I’ve been using the Copernicus “save the phenomena” example to try to explain the bizarre intricacies of Obamacare to some of my fellow Canadians (so I appreciate seeing it here). And it occurred to me that Copernicus didn’t publish his manuscript until after he died….too many powerful interests deeply vested in the existing system…

I tried to make this as simple as possible, but apparently that’s not simple enough (no knock on the readers).

As a political power play, though, I don’t think it’s that complicated; the “Silver Switcharoo” states have thrown out any idea that policy pricing is actuarial, by “loading” everything onto the silver plans so that the insurance companies will profit (and therefore stay in the marketplace). Surely there’s a way to write new regulations or sue in court to prevent that. And as I say, I’m sure cruder methods will come to hand for the Administration, if need be.

And will. Unfortunately neither machinations do much for any of the people who need healthcare not unusable insurance.

I sometimes wonder if even half as much time and effort were spent really attempting to provide access to healthcare as is being spent keeping insurance companies happy and/or keeping up appearances regarding the issue how much improvement we would see in our dismal health statistics, rather than say declining life expectancies.

Actually the only real mystery is how they all think no one sees the reality rather than the sales pitch.

Rhetorically … why are we wasting pixels?

Supposedly a super majority of Americans want single payer.

Spend all those millions and millions of man hours on uniting Americans across wedge-lines to force the dad gum politicians to do the will of the people.

While “we” are bogged down in minutia the status quo continues.

Honestly … years ago when I did my own taxes I wanted to go after the complexity of the tax code based upon it’s damage to my pursuit of happiness.

Nobody wants anybody to die because of a lack of health care.

Nobody wants pharmaceutical companies to get rich off of cancer patients.

Nobody wants the insurance industry to increase the cost of health care by 30% (or more) because of bloated administrative costs, marketing expenses, extravagant executive pay and profits

The idea that neither the Democrats or the Republicans support single payer is enough stand alone proof for me to know that the false dichotomy is the dragon that must be slayed.

Somebody does indeed want to get rich off of other people’s health issues- the people that collect the payments. They, claiming horsehockey like “maximized shareholder value”, will charge as much as they can for as little care as they can get away with. Out all makes perfect sense when you look at it from their (despicable) perspective.

A supermajority of very interested billionaires and their sock-puppet politicians like the current system just fine, thanks.

Even a unanimous citizenry in favor of single payer will not trump (pardon the pun) the very interested billionaires.

Time to abandon those two useless and bought parties and start organizing around another party who gives a damn about ordinary folks and effectively run government to serve you the people and deliver services in the publics interest instead of the oligarchs. Perhaps the SOCIAL democrats or the Greens.

If you think it’s complicated choosing a plan, wait until you actually have to use it.

Having spent considerable years overseas, moving back to the States, signing up for “silver” and having a hospital stay, I am completely convinced the USA is one of the worst countries in the world. The insanity of trying to get these bills processed and paid is inhumane, and I’m healthy. There is no way someone who is sick could wade their way through this treacle. In network, out of network, co-pays, deductables, duplicate billing, erroneous billing, appeals processes, automated phone calls to explain appeals processes won’t happen for x amount of days, appeals being approved, then not paid, phone automated health advice….. it just goes on and on.

And for the argument that there may be some acceptable level of bureaucracy for the quality of care received, wrong-o. The quality of care I received was sub-standard in every respect. I had to question every diagnosis for days until the proper one was made, which included questioning prescribed drugs that should have been discontinued immediately once the (erroneous) diagnosis changed. This was in a reputable trauma one facility with highly experienced staff. I quite literally had to facilitate communication across departments and staff members. It took multiple days to find a problem that should have been discovered in a few hours with a common test normally done for someone with my symptoms. A test that is also fairly inexpensive, non-invasive and takes 15 minutes. And of course, the answer to every single problem is a prescribed drug. I questioned every drug prescribed and refused to take some of them, like statins,

I have experienced health care first hand in Europe and Asia, and while it’s no panacea, at least we felt like we were being treated like respectable human beings, with transparent, effective results and payment processes. In many cases the quality of care we received was world class.

This country is very, very broken. My wife and I have had multiple conversations about leaving once again. At times it feels as if we are the only ones on the other side of the looking-glass.

Anyways, sorry for the rant. It felt good to get it out…….

No, many of us are on the other side of the looking glass. And our “health care system” is cruel, stupid and very, very expensive.

I don’t know if it will work, but I am researching what other country I could move to and work.

Just as a minor point, the whole thrust of the article here is that even after cancelling the CSR payments the government will be paying as much or more due to insurance companies manipulating rates, but the Trump administration never said that cancelling these payments was about reducing government outlay. The stated reason for the cancellation was that Congress had not authorized funding for them and that paying them was against the law. It had been ruled unlawful by a court, and that ruling is still in force.

So the writer is going to great length to refute a point that the executive branch never made, and is not even attempting to refute the point that the executive branch did make.

I saw the same thing. A quick search concurred.

As much as I despise the client system and administration (the last several, TBH), unauthorized funding appears to be the cause of the cancellation.

Anyone have anything to show otherwise?