By Robert Ayres, Emeritus Professor of Economics and Political Science and Technology Management at INSEAD, with Michael Olenick and Lu Hao, research fellows at INSEAD

For several weeks, the guest experts on CNBC and Bloomberg News have been talking about the coming tax cut legislation (for corporations) that the Republicans finally seem to have in their grasp. The Bill, as it is currently proposed, will eliminate the insurance mandate for health care and may leave quite a lot of upper middle class salaried people, worse off, especially in high tax states. The sure winners will be the shareholders of multinational corporations and “pass through” enterprises, especially real estate partnerships. The “supply-side” cheerleaders for the plan, both in Congress and the White House (Mnuchin, Cohen, Mulvaney, et al) argue that economic growth be much faster, that it will pay for the cuts, and that wages and salaries will rise, thanks to a burst of new investment.

By contrast, virtually all top economists say that the cuts won’t pay for themselves, that the deficit and the national debt will increase, and that growth will not accelerate. What both sides agree on is that there is around $2.5 trillion in profits sitting out there in overseas banks, mostly in tax havens, just to avoid paying US corporate taxes. Apple, alone, allegedly has $260 billion to bring home, if only Uncle Sam would kindly cut his share. The plan being discussed by the 112th (current) Congress would reduce the corporate tax rate on foreign corporate profits repatriated as dividends.

A “tax holiday” to bring back profits being held overseas was tried by the second Bush administration in 2005 as part of The American Jobs Creation Act (PL 108-357). The tax rate for funds repatriated under the Act was set at 5.25% (a one-time 85% discount on the 35% top US corporate Income tax rate. The corporate promoters and their lobbyists said that 500,000 new jobs would be created in 2 years. Here is what actually happened in 2005[1]. During the next year $299 billion was repatriated by 843 companies (out of 9700 companies that were eligible).Of this amount, $99 billion was repatriated by pharmaceutical companies (32% of the total), $58 billion was repatriated by computers and electronic equipment firms (18%). That compares to around $60 billion per year (on average) of total repatriations of foreign earnings by all companies, during the previous 5 years.

How many new jobs were created? The top 15 repatriating companies reduced their total US employment by 20,931 jobs (about 35%) between 2004 and 2007. (A few companies reported increased employment, but only because of acquisitions. R&D by the top 15 decreased slightly even though six of the top eight were pharmaceutical companies (and those companies are notoriously dependent on R&D). Two academic studies, based on data from the whole spectrum, concluded that repatriation in 2005 had no positive effect on R&D expenditure {Blouin, 2009 #8404;Dharmapala, 2011 #8403}

Use of repatriated funds for share buybacks was explicitly prohibited by the Jobs Creation Act of 2004. But, strangely, share repurchases by 19 major repatriating firms surveyed (including the top 15) increased from $2.2 billion (average) in 2003 to $2.5 billion (average) in 2005 and $5.3 billion (average) in 2007. Share buybacks and executive compensation were the only expenditure category that increased as a result of the repatriations. One study found that, for every $1 of repatriated funds, between 0.60 and $0.92 went into buybacks{Dharmapala, 2011 #8403}. It seems that corporations could – and did– legally use the repatriated funds in the “allowed” areas while moving previously budgeted corporate funds away from those areas (i.e. R&D) to use for the buybacks {Levin, 2011 #8402} p.23, footnote 61. However, it must be acknowledged that buybacks by company were quite variable from year to year between 2002 and 2007; see {Levin, 2011 #8402} Appendix, Table2.

Executive compensation was the other expenditure category that increased dramatically in most of the surveyed corporations. Only one of 19 surveyed (Motorola) reduced executive pay between 2004 and 2007, and that was for other reasons. Collective executive compensation for 19 companies surveyed increased by 35% in the year after the repatriation (from 2005 to 2006), whereas worker compensation increased by only 5%. (Executive pay for the group of 19 decreased slightly from 2006-to 2007, primarily due to an enormous decrease in one company, Hewlett-Packard.

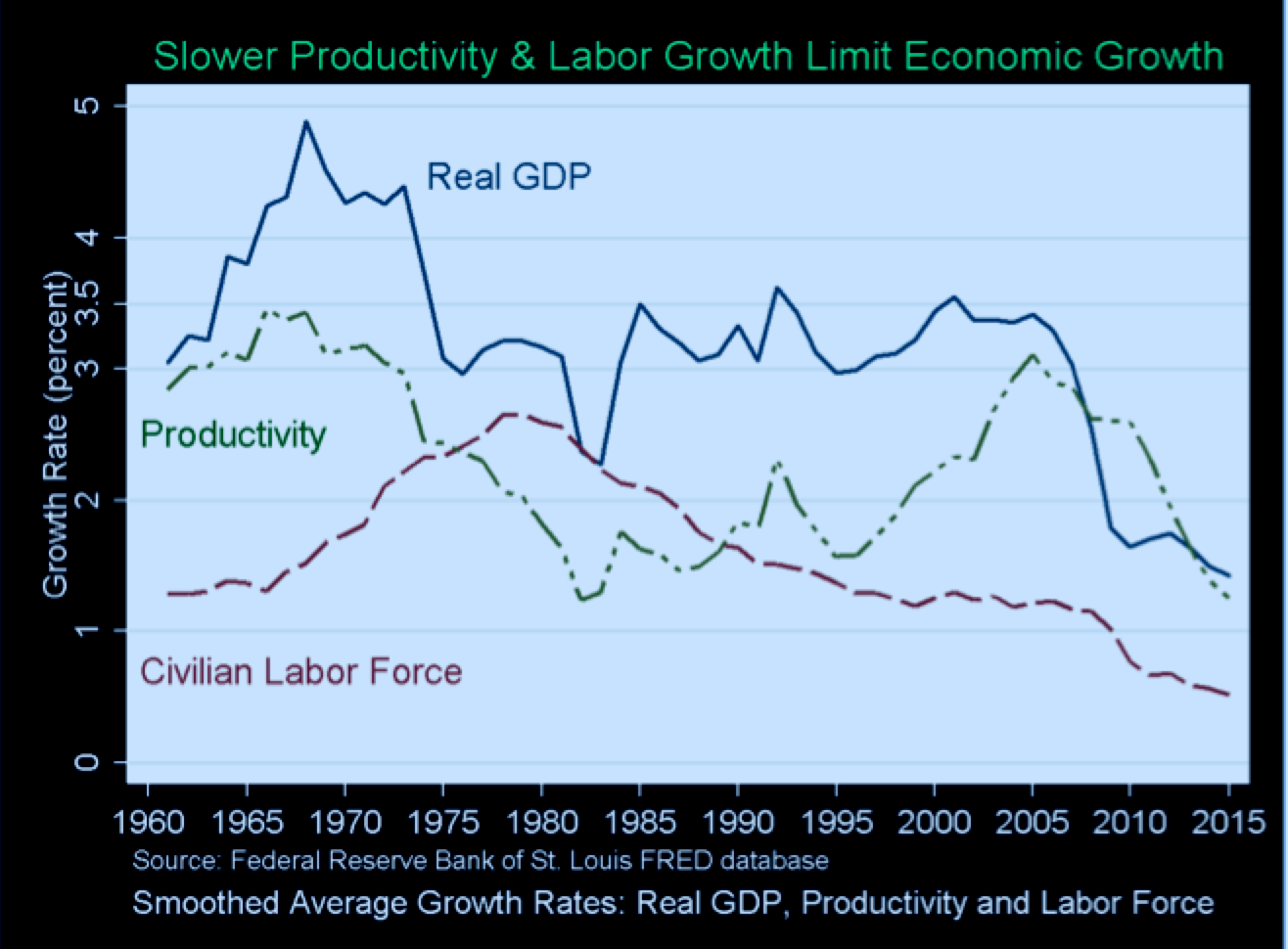

Did GDP growth accelerate after the 2005 Bush tax holiday and other Bush tax cuts? It did not. In fact, the rate of US growth fell sharply. The chart below (from the St. Louis Federal Reserve Bank) tells the story. GDP growth peaked at 4.8 % p.a. in 1967. That peak (driven by spending borrowed money during the Viet Nam War) kicked off a persistent inflation. Real economic growth stayed near 4.5 percent from 1965 until 1973, after the first “oil shock”, and then started to fall partly due to oil price increases. Economic growth still hovered around 3.1% p.a. through the rest of the 1970s. That period was stopped by Paul Volker’s “inflation killer” interest rate spike in the spring of 1983. But the rate of productivity growth fell steadily from the in 1965-67 to a low in 1982-3. That interest rate spike in 1982 caused a deep but short recession in the US (and an economic crisis in Latin America). There was a rapid recovery due to falling interest rates and very low oil prices in 1985-86 (but attributed by all Republicans – but very few economists — to Reagan’s tax cuts).

Productivity started to recover (but unevenly) in the 1980s to another peak in 2005. Most economists attribute this upward trend in productivity to the penetration of computers and digital technology. But, perhaps surprisingly, the internet revolution that began in the 1990s, has not resulted in measurable productivity gains. N.B. Growth still hovered around the 3 % p.a. level between 1986 until 2005. It actually peaked at just over 3.5% in 1992 and again in 2001 (right after the Dot.Com stock-market crash). After the crash there was a very mild recession. In 2003 the Fed, under Chairman Greenspan, responded with a series of interest rate cuts, intended to stimulate growth. That mild recession stimulated George Bush and the Republican Congress to try, once again, the “supply-side” theory {Stockman, 2013 #8291}. The American Jobs Creation Act of 2004, was supposed to bring back a lot of capital sitting in banks overseas to escape US Corporate Income taxes and induce another Reaganesque growth spurt. But, instead, after 2005 economic growth fell sharply from 3% p.a. in 2005 through 2006 and 2007 to around 1.5 % p.a. in 2008-9. There was no acceleration of growth until the first “green shoots” in 2016, when unemployment finally dipped below 5%

Figure 1: Productivity & the labor force

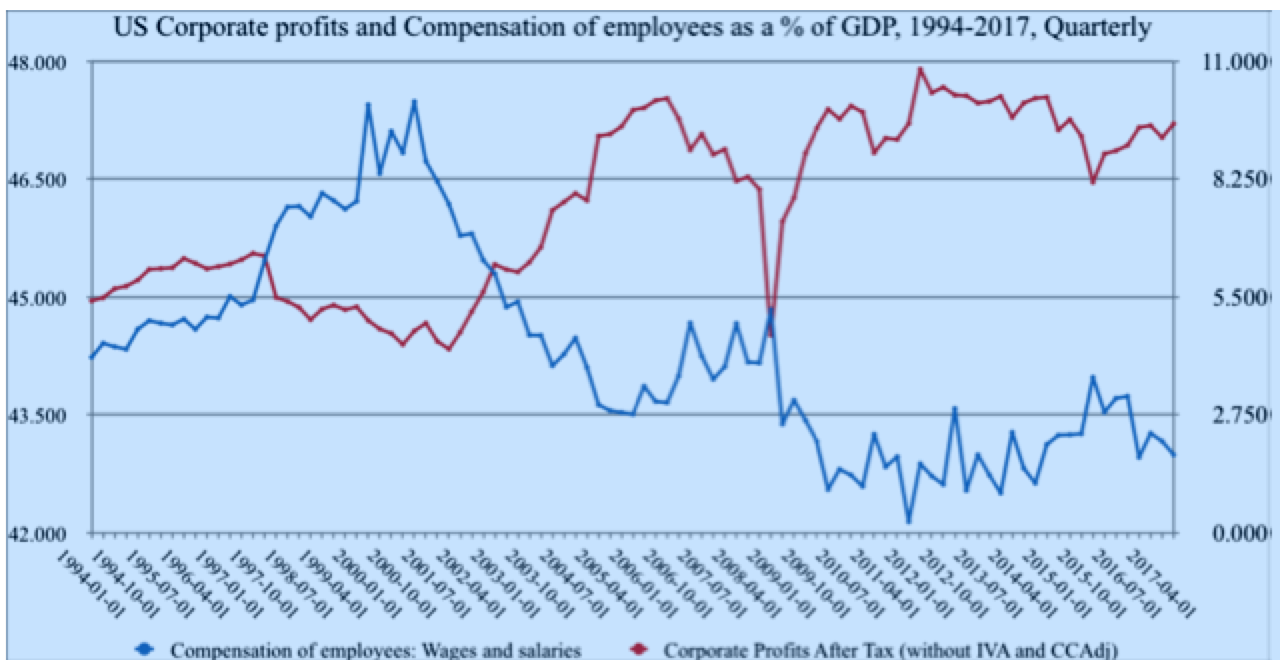

Now I come to the crux of the matter. Corporate profits are currently at an all-time high, in absolute terms. Most market watchers expect to see even higher corporate profts next year, even without the proposed tax cut. Of course the economy has grown, too, but as a fraction of GDP, corporate profits after taxes (red) have increased from 4.5% of GDP in 2001 to more than 9% of GDP in 2017. Meanwhile salaries and wages (blue) have declined as a fraction of GDP, from about 47 % of GDP in 1994 to 43% of GDP in 2017. The relationship is not perfectly symmetric over long periods, but since 2001 most of the dollars added to corporate profits have almost literally come out of the pockets of employees. The notion that future increases in corporate profits will simultaneousl add to employee paychecks is contrary to both experience and logic.

There is more to be said about economic growth,of course. Economic growth is driven by investment, after some lag-time. Money for investment comes either from the current profits of businesses, or from savings from salaries and wages of workers (including the highly paid executives), or from corporate (or government) borrowing against future profits. There is no other possibility. The historical evidence tells us that borrowing against future expected profits is the primary (and increasing) source of investment capital.

Figure 2: Corporate profits & compensation

But beware: the legacy of past borrowing to invest in past economic growth remains in the form of existing debt. Existing corporate and government debt – consisting mostly of long-term bonds — is being paid off constantly at rates of interest set when the bond was sold. Consumer debt, on the other hand, consists mostly (70%) of home mortgages, plus some education debt and short-term credit-card debt. Some past US government borrowing was used to finance Federal, State and municipal budget deficits. Investment in new productive capacity (“bricks and mortar”) is financed by corporate profits or borrowing (selling bonds). Finally, there is financial debt, mostly by banks, hedge funds and rivate equity groups, enabling companies to buy other companies.

So, existing debt is what financed past wars, past budget or trade deficits and past investments in economic growth. Existing debt is being paid off, year by year, just as mortgage debt is paid off over time, by corporate , municipal or private borrowers. But the cost of debt service comes out of current income. A debtor may decide to accelerate her payments, so as to reduce the current debt service load. But debt repayment in the absence of increased income, means there will be less money available for new investment. This truism applies at all levels. If we (as a nation) decide to pay off the existing national debt faster there will be less money for other government services, including new capital investment, such as infra-structure repairs and upgrades. That means slower growth.

The essential point is that faster economic growth requires more investment. That, in turn, necessarily implies more – not less – borrowing. Corporate leaders who want to pay less in taxes, are proposing to cut government revenues, resulting in austerity: reduced services or more borrowing to fill the budget gap, or both. Can the gap be filled by spending cuts? If the spending cuts come out of social services, such as health care and pensions – which is what most Republicans advocate – it means that people now depending on those services will have less income, even if they also pay a little less in income taxes.

To complicate the situation further, the Federal Reserve Bank (FRB) is now (2017) starting to sell back into the bond-market the several trilliond dollars of securities (government and corporate bonds) that it bought during the three periods of “quantitative easing” (QE). When that QE policy was in effect, the FRB was effectively under-writing the commercial banks capital reserves (by giving them cash to buy other securities to maintain their reserves) and, thus enable them to make more loans to businesses. But now that US unemployment is close to 4% p.a. the FRB has started to reverse this “easing” policy i.e. to resell the bonds it bought a few years ago. To buy them back, the banks will have less money available to lend to small businesses. What was a “tailwind” a few years ago is now a “headwind”.

In summary, there is no evidence that cutting corporate taxes will result in increased investment in “bricks and mortar” projects, to make useful products, or in R&D. That did not happen after the 2005 tax holiday, and the financial incentives that operated then are still in place. The money brought back from overseas in 2018 or 2019 will mostly be spent on share buybacks, executive compensation and dividends to shareholders. The buybacks will drive up share prices further and accelerate the current “bull market” in corporate equities. The end result will be another euphoric “bubble”, comparable to the ones in 1929 and 1999. When retail investors borrow money to buy stocks, on margin, the end is near. After such a bubble comes the inevitable crash, when the small “mom and pop” investors get hurt the most. And the next crash will be very painful. One can only hope that it will be painful enough to encourage and allow some fundamental changes in the current forms and structures of capitalism, starting with election reform.

[1] Our main source is the 78 page Majority Staff Report of the Permanent Subcommittee on Investigations, United States Senate {Levin, 2011 #8402}. We also refer to the report of the Congressional Research Service (CRS) {Marples, 2011 #8400}

Lately I,ve been reading analysis like this, and other recent political developments in the US with horror. I pretty much agree with the conclusion of this article and I find the words elected revealing:

The author does not say that “democratic institutions” starting with the election system should be reformed. He says that “capitalism structures” including elections should be reformed. Wow! This is for me one of the most blunt recognitions I´ve read on how democracy has been downgraded to an instrument of capital.

I think this goes back to the market as an unparalleled information processor.

Consumerism is the modern version of Utilitarianism. And corporations as “persons” is a big part of the collective feedback. As consumers, we can only effect the result thru our happiness (consumer spending). More happiness, more consumer spending.

What gooses this system, is credit. We use banks as intermediaries in the feedback loop, for both individual and corporate persons. And nobody has ever understood the exponential function, or very little credit would be used. Instead we have “irrational exuberance”.

No wonder classical “rational actor” economic models fail. The actual system depends on irrationality. This analysis is “macro” … and hence flawed by the miscorrelation of poorly modeled and badly counted measures. Outside of “micro”, we don’t know what we are talking about.

Consumerism seems to endlessly generate more desire than happiness.

Adam Curtis BBC documentary;

“The Century of Self”

https://www.youtube.com/watch?v=eJ3RzGoQC4s

This is a last grab for cash/donations from big donors and ultimately the grand bargain. They push hard before they get tossed in the midterms. i like to listen to Washington Journal to put myself to sleep, many conservatives are angry. Pretty soon all of the USA will be Kansas, Greece or Cyprus.

https://www.youtube.com/watch?v=zfyEhAc7K_I

This could cheer people up, so funny

Having failed to eliminate Medicare, Medicaid, and Social Security by conventional means, Republicans sought to intentionally increase the deficit with this tax bill so they can turn around and say “sorry but we can’t afford it” and gut these programs accordingly.

Perhaps I’m being overly cynical here–maybe they actually believe their own B.S. about tax cuts–but I do wonder sometimes.

…not at all “cynical”, Louis…it’s quite simply more “Shock Doctrine-Rise of Disaster Capitalism”:

https://www.youtube.com/watch?v=hA736oK9FPg

(parallel Klein’s documentation of Sept. 11, 1973, Milton Friedman “Chicago Boys” takeover of Chilean economy-exploitation under U.S. puppet dictator (convicted war criminal) Pinochet…)

Very clear, although I have a couple of questions about underlying postulates, or maybe assumptions — at any rate they are statements

1.) “That peak (driven by spending borrowed money during the Viet Nam War) kicked off a persistent inflation.” Is this consumer, corporate or government borrowing? What for, and why borrowed? Why, for that matter, during the VN war?

and

2.) “To buy them back, the banks will have less money available to lend to small businesses.” Since banks can and do create money with keystrokes, if I have that correct, then reluctance to lend to small businesses would be a matter of bank policy, not necessity — same as now.

Johnson’s Great Society was trying to use “functional finance” to bring about full employment and with it improved living standards for the bottom tiers of society. At the same time, trying to avoid Kennedy style bullets to the brain, LBJ gave the MIC everything it wanted. The confidence that comes with prosperity fueled a real popular resistance to the VN war that grew out of the Civil Rights movement. The latter had been an LBJ ambition, the former a concession to reality from his perspective.

When Nixon took over, the engine of functional finance was subverting the Bretton Woods semi-gold standard arrangements and when Nixon ended Bretton Woods, in a fit of pique erstwhile gold importers who happened to be oil exporters formed OPEC. This real demand side shock precipitated a cost push inflation that wasn’t corrected until the natural gas market was deregulated. By that time, inflation had been normalized into contract language for both labor and commerce and took on a self fulfilling form as CPInflation caused contract escalation clauses to to kick in and cost of living clauses in labor contracts to do the same.

The “borrowing” referred to I have to assume is the Federal Budget Deficit which was spent for both guns and butter. Once off Bretton Woods, this was purely an internal policy priority problem, but has been turned into propaganda bugaboo to frighten the children about “THE DEBT!!!” Why LBJ did this was: to end poverty; to not get shot in the head. The end of functional finance was an unintended consequence created by the deliberate efforts of the Powell Memo Consortium.

I agree with your take on the second point: banks will lend when there are creditable borrowers who want to borrow. Not much of that in the cards these days.

A couple of other things run counter to my MMT beliefs.

But it’s present profits that are reduced by debt service. Credit is issued based on expectation of future profits, and those aren’t going to be reduced by present debt repayments The leash between current profits and future borrowing can be very long.

And of course

Treasury and its Central Bank, the FED, being the fount of all money, there can be as much money as they say.

And an aspect of bank reserves I possibly don’t understand:

In my understanding, the reserves are the dollars held in a private bank’s reserve account at the FED. That this balance could be “supported” by spending it down to buy other securities is strange to me.

The objective observations in the article are valuable. Notably the truth about the route the returning money took (enabling other funds to be spent for share buybacks) during the last tax holiday.

Johnson (and Nixon) ran deficits when the economy was already at full employment to pay for the Great Society, the space race (not trivial in terms of cost) and the Vietnam War. Deficit spending when an economy is at full employment is a prescription for creating inflation. Johnson did it before Nixon went off the gold standard, hence it did entail borrowing, as opposed to direct spending accompanied by bond issuance for the convenience of investors who like to hold bonds.

Johnson should have raised taxes but didn’t want to, since it would be depicted by his opponent as taxing to pay for the unpopular Vietnam War (or among the far right, for the Great Society programs).

Yves, Are you now against running deficits? I thought the MMT folks said it doesn’t matter. I’m not seeing match wage inflation out there. I’m in the Software industry. Must of the IT organizations I deal with are still trying to move everything they can off-shore.

No, Yves is not.

Deficit spending is absolutely necessary for addressing unemployment and the aggregate demand shortfall that recessions create.

It is just that deficit spending in times of full employment are a recipe for inflation. Keep in mind that taxes are not about giving the government money. They are about keeping inflation under control.

Spending is dictated by the economic climate of a nation.

Do you really believe we are at full employment?

Figure 2 is an eye-opener! Or is it the coffee???

Some quasi-relevant quotes, mostly from folks whose name starts with “G”:

“Those who cannot remember the past are condemned to repeat it.” George Santayana.

“If history repeats itself, and the unexpected always happens, how incapable must man be of learning from experience.” George Bernard Shaw.

“Every record has been destroyed or falsified, every statue and street building has been renamed, every date has been altered. And the process is continuing day by day and minute by minute. History has stopped. Nothing exists except an endless present in which the party is always right.” George Orwell.

“We learn from history that we do not learn from history.” Georg Wilhelm Friederich Hegel.

“Those who don’t study history are doomed to repeat it. Yet those who DO study history are doomed to stand by helplessly while everyone else repeats it.” Unknown.

Capped off with this:

“A great many people think they are thinking when they are merely rearranging their prejudices.” Walter Lippman.

This time around interest rates will be much closer to zero,allowing less of a bounce when the Fed lowers the rates rapidly. And when the Fed tries quantitative easing by giving money to banks instead of pumping the money into the real economy, more bubbles will be inflated in the assets in which the banks dump their free money. History may not repeat exactly, but it rhymes like an off-color limerick.

I’m 31, so I don’t have a long history with politics and markets, but I’ll be damned if I’m not scared half-to-death. It feels like we’re riding up a ramp that terminates above the grand canyon at 100 mph with no safety harness. Sure markets are going up at the moment, but an enormous correction and crash seem imminent. I don’t know if I’m just experiencing my generations apocalypse worry or if I should heed the the warning signs and personal worry and sell of my individual account and lay low for awhile.