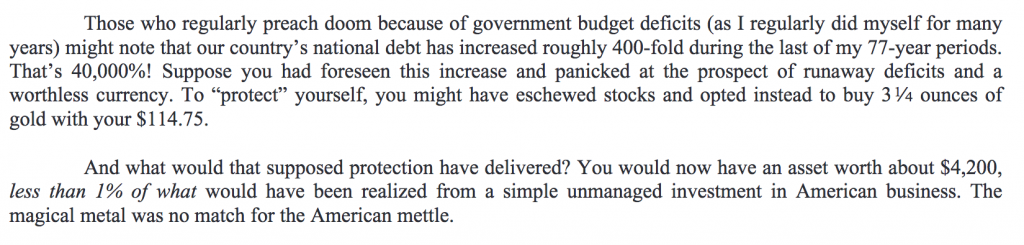

Warren Buffett admitted he was wrong about deficits. Wish he had figured this out before 2009, when the Obama Administration was afraid of launching a big enough stimulus package. From his annual shareholders’ letter:

Sadly aside from Axios, I don’t seen this point getting the attention it deserves. But maybe too many heads would explode were that to happen.

And to the extent the Twitterverse has taken notice, it’s goldbugs and Bitcoin fans up in arms that Buffett has dissed a non-prodcutive, non dollar asset.

In fact, Buffett could have gone further in terms of recognizing the necessity of Federal deficits when companies are under-investing, as they have been doing chronically since the early 1980s. But his becoming an official agnostic is a big step in the right direction.

For a longer-form explanation, see this section of a post we wrote with Rob Parenteau in 2010:

A series of disappointing data releases in recent weeks, including flagging consumer confidence and meager private sector job growth, is leading more and more experts to worry that the recession in the US and abroad is coming back. At the same time, many policymakers, particularly in the Eurozone, are slashing government budgets, which they contend will lower debt levels, and thereby restore investor confidence, reduce interest rates, and promote growth.

Yet many miss the fact that fiscal deficits are a nearly inevitable result of actions by corporations and households. Failure to understand these dynamics and address root causes is sure to make a bad situation worse.

Unbeknownst to most commentators, corporations in the US and many advanced economies have been underinvesting for some time.

The normal state of affairs is for households to save for large purchases, retirement and emergencies, and for businesses to tap those savings via borrowings or equity investments to help fund the expansion of their businesses.

But many economies have abandoned that pattern. For instance, IMF and World Bank studies found a reduced reinvestment rate of profits in many Asian nations following the 1998 crisis. Similarly, a 2005 JPMorgan report noted with concern that since 2002, US corporations on average ran a net financial surplus of 1.7 percent of GDP, which contrasted with an average deficit of 1.2 percent of GDP for the preceding forty years. Companies as a whole historically ran fiscal surpluses, meaning in aggregate they saved rather than expanded, in economic downturns, not expansion phases.

The big culprit in America is that public companies are obsessed with quarterly earnings. Investing in future growth often reduces profits short term. The enterprise has to spend money, say on additional staff or extra marketing, before any new revenues come in the door. And for bolder initiatives like developing new products, the up front costs can be considerable (marketing research, product design, prototype development, legal expenses associated with patents, lining up contractors). Thus a fall in business investment short circuits a major driver of growth in capitalist economies.

Companies, while claiming they maximize shareholder value, increasingly prefer to pay their executives exorbitant bonuses, or issue special dividends to shareholders, or engage in financial speculation. They turn their backs on the traditional role of a capitalist – to find and exploit profitable opportunities to expand his activities

Some may argue that lower investment rates are the result of poor prospects, but the data does not support that view. Corporate profits have risen as a share of GDP since the early 1980s, reaching unprecedented levels right before the global financial crisis took hold. Even now, US profit margins are nearly two thirds of the way back to their prior cyclical high, despite a subpar recovery.

What happens when corporations on balance are saving, and households in aggregate try to save too? Families and individuals typically tighten their belts and bolster their bank accounts in bad times; the tendency is even more acute now, since many are trying to pay down borrowings, which is a form of saving,

If households and corporations are both saving, it must be balanced by the other two sectors of the economy, the government sector and the import/expert secto. In other words, the foreign and government sectors must spend more cash than they are taking in. In lay terms, that means running a trade surplus and having the government incur budget deficits.

Therefore, when both domestic households and the corporate sector are saving at the same time, then you need to have a VERY large trade surplus, a very large government deficit, or some combination of the two. There is no other way to square this circle – anyone who tries to tell you otherwise does not understand double entry book keeping, which the West has used for at least the last five centuries with some success.

And what if a government embarks on an austerity program in the face of private sector efforts to deleverage? Income growth will stall, and if the austerity program is large or sustained long enough, falling household wages and business profits can result.

That result might not sound bad, since lower wages and prices would make US goods more competitive abroad. But in economies suffering from a debt hangover, as incomes fall, it becomes even harder to make payments on outstanding loans. Defaults and bankruptcies cascade through the financial system, leading to even more reluctance to borrow and lend. In other words, the result of Austerian fiscal policies, is deflation – falling wages and prices – which can easily snowball into a depression.

One has to wonder if Buffett’s newfound indifference to deficits comes from the fact that he expects some big bubbles to pop soon.

This is not good. Are all these corporations hoping that when the wheels fall off the economy the next time, that they can ask the government for another Greenspan put? Combine the lack of investment in themselves by corporations with the degradation of the country’s infrastructure and that is one deep pit that the economy could find itself in next time. A big worry too is not only the amount of money & resources being spent on research & development but also which sectors of the economy are investing in it and whether it translates well into the general economy. Here is a page that talks about world R & D-

https://www.visualcapitalist.com/global-leaders-r-d-spending/

In growing up I use to think that the so-called “Robber Barons” of the late 19th/early 20th century that I read about were pretty bad in their behaviour – people such as J.P. Morgan, Andrew Carnegie, Andrew W. Mellon and John D. Rockefeller. Make no mistake, they were on the whole people that behaved badly but compared to today’s business captains of industry at least they built things. You are talking about industries, railways, ports, shipping, etc and after their power had waned, all this infrastructure was all there. What will today’s Robber Barons leave behind them?

What will today’s Robber Barons leave behind them?

– they leave in their trails: homeless people from forclosures, debt slaves, drug deaths, death from weapons, diabetes and obesity from crap food, absence of privacy of the data of your life, elderly people lying in their own excrements for days in provatized elderly care, pupils not learning anything in privatized schools, infrastructure that is crumbling etc

No, no!

Deficit spending lifts all boats, particularly those of wage earners. The Greenspan put helps first and foremost the owners of financial assets, and the trickle-down goes first to their service providers.

Sorry to leave Warren’s epiphany in the dust, but I don’t think deficit hawkery is limited to gold bugs and ideologues. I don’t think I’ve heard a single politician utter, “deficits don’t matter”, since that renowned lefty Dick Cheney did. I believe that these broadly-held deficit fears are driven mostly by the scale of the national debt, and a visceral “how will we ever pay this all off,” among the gullible and their mentors. Perhaps if the U.S. government accepted that there is little if any inflationary difference between covering deficits with debt (T-bonds) or government emissions (printing), they could grossly reduce the debt via printing while maintaining the stable store of value provided by T-bonds. It seems to me that global financial giants, not elected or selected fiscal and monetary leaders control U.S. fiscal and monetary policies. They maintain that power through influence (lobbying) and credential-driven fear mongering (e.g. “Ocasio-Cortez is an economic illiterate” screamed the headline). Meanwhile, aside from a small cadre of colleges, thinking outside the neo-classical or neo-liberal boxes brands one as “not serious,” or even “a kook.” I would very much like to hear our left-leaning pols argue that deficit fears are not founded and should not prevent the nation from doing what needs to be done.

Deficit spending lifts all boats, particularly those of wage earners.

Seriously?

Postage stamps went up 20% the other day. Stamps are a good indicator of actual inflation. (which is always “under the target”).

Min wage people did not get the memo.

Oh come on. Postage prices have everything to do with the manufactured crisis at the Postal Service due to bogus accounting for their pension obligations. We’ve featured articles on this quite a few times.

And minimum wages are being increased in quite a few states and cities after many many years of being static.

The fact that deficit spending helps workers does not mean that the level of deficit spending is high enough.

I think you may have a wrong Buffet quote there – it’s about fees. An appropriate one for CalPERS, but maybe not deficits?

vlade is right – putting in the quote about deficits would be better!

It looks like you are rigth. But the quote is interesting too!

Can anybody send Buffet’s article to our austerian EU authorities, please?

Oops, fixed. Sometimes the screenshot function puts the most recent image higher up than last in the list.

,,,Little things…mean a lot…

What else is new; even the Buffets of this world, all turn out to be

unfit clowns; some of them know it even if too late!

Monetary Sovereignty has preached deficit spending for 20+ years. Finally, the “Oracle” begins to see the light.

I say “begins,” because it isn’t clear that he truly understands Monetary Sovereignty. But perhaps it’s a start. Now, if only the Committee for a Responsible Federal Budget (CRFB) and all the others of their ilk, would finally just shut up.

What I find interesting is something that doesn’t really mean anything under our current financial aegis, is so upsetting to Warren Buffet.

Says a lot.

Those countries using the euro must remain austerian, because they made the mistake of giving up their Monetary Sovereignty

In that sense, they are like cities, counties, and states. Unlike the U.S. federal government, they do not have the unlimited ability to create their sovereign currency; they have no sovereign currency

In 2010, in a talk at UMKC, I said, “Because of the Euro, no euro nation can control its own money supply. The Euro is the worst economic idea since the recession-era, Smoot-Hawley Tariff. The economies of European nations are doomed by the euro.“.

The euro nations have volunteered to be ruled by the unelected, wealthy, EU bankers.

On a perhaps related tangent, NPR featured a story this weekend about the sorry state of German (!) infrastructure. Deutsche Bahn’s legendary punctuality is now regularly undermined by problems with their trains/bridges etc. Many German customers interviewed apparently appalled by how bad things have gotten. Closing quote even suggested poor on time performance compared to Italy (!)

Responsibility alluded to “black zero” policy i.e. no increase in national deficit.

In hard times households save? Hmmmm! ?More likely they use credit cards. Debt has been on the rise–despite a “growing” economy. Consumer debt grows because wages don’t keep up with productivity.

Businesses are showing profits by driving consumers ever more deeply in debt. Those profits are not being reinvested. Because financialization.

The national debt increases because the overall economy can’t keep up without continuing government infusions.

They only bring up debts when it’s about social policies. Never about military or tax cuts. Or of course their pet aka pork projects.

Gotta say i love professor Keen’s take on government deficits.

That it is effectively what allows corporations to run a profit and the public to pay down their debts.

If he makes the transition to an MMT advocate, I would imagine some pretty tense bridge games between him and Bill Gates.

https://www.theverge.com/2019/2/12/18220756/bill-gates-tax-rate-70-percent-marginal-modern-monetary-theory. “modern monetary theory is ‘crazy talk’”

Knowing Buffett though, he’s only interested in keeping the values of his companies high. In other words, he’s just another Alan Greenspan.

Americans should thank their lucky stars Warren Buffett is not in control of national economic policy because his prescriptions have been wrong, wrong, wrong for years running. I suppose we should be grateful he has finally reversed course, but we should also recognize his track record. Buffett is in part personally responsible for the deindustrialization of America (Berkshire helped to gut furniture manufacturing here) and pretty much the worst person in the world to listen to. But, since he has too much money, and since our nation’s media is owned by rich people and run for rich people, he is handed the biggest possible megaphone to broadcast his destructive ideas.

2009: Months after an unprecedented economic crisis, Buffett weeps about the budget deficit and high levels of inflation. In fact, the U.S. experienced disinflation for a decade. Income and wealth of the lower 90% still have not recovered.

2011: During the peak of the Great Recession, Buffett proposes automatically firing legislators who are in office when the deficit exceeds 3% GDP. MMTers will recognize this proposal as economically illiterate. High school civics students will recognize it as requiring a Constitutional amendment.

2011: Buffett tells Congress that reducing the deficit by $1.5 trillion over ten years isn’t enough.

2012: After multiple years of destructive austerity, Buffett tells the nation that a 2.5% deficit should be sufficient for economic growth. MMTers will recognize this notion as farcical in a country with a massive trade deficit.

I gave up wrestling with Google at this point but I doubt that one shareholder letter can defeat years of NYT op-eds and CNBC interviews when it comes to influencing the nation into bad economic ideas.

That Buffett is becoming agnostic about MMT is a constructive development. When Berkshire’s Vice Chairman Charlie “Suck it up and Cope” Munger publicly agrees with him, that will be cause for a tall cool one indeed.

Of course, the concluding sentence of Yves’ piece and memories of post-GFC beneficiaries (how soon we forget) might also have played a role in his conversion. After all, I think about 43% of Berkshire’s ~ $200 billion equities portfolio is in TBTFs’ stocks, with much of the balance in sectors that could also be adversely affected by a deep recession, and that’s setting aside those entities that are wholly owned and operated by Berkshire as subsidiaries.

This is not to say that we should favor subsidies for American corporations that have engaged in aggressive stock buybacks over the past several years to the detriment of R&D, Capex, operating improvements, and their capacity to endure cyclical downturns in the economy. But I don’t believe Berkshire falls into this rather large group.

Running an obscene debt is only possible under two conditions: the country must have a sovereign currency and must be able to largely dictate financial policy to the world. The first will likely always be true, but the second is debatable. The euro might someday be able to challenge the dollar, but the more likely threat is from China after Made in China 2025 becomes reality. For those of you unfamiliar with it, China plans to manufacture 70% of important technology by 2025. Given China’s IP theft and technology transfers (forced or otherwise), China already has a world-class high-speed trainset. Its version of the 737 is in trials. It has started production of NAND, both 3-D and 2-D. It has made real progress in processors. This will have two results. First, China will stop buying from the West, and second, other countries, especially in Asia, will buy China’s products instead of ones from the US or Europe. Add to that Cold War 2.0, with China, Russia, and other countries reconstituting the Second World, only this time with technology that’s not a joke, and the future for the US may not be the same as it once was.

Debt can be excessive, badly structured… but obscene? Rates can be obscene/abusive.

In the very near future, debt will be over $40 trillion, yet GDP will be less than $30 trillion, with China’s financial strength reducing the US ability to obtain favorable interest rates. Then you too will term the debt obscene.

Yeah, not sure why debts can’t be obscene. If something is structured as debt, in the first place the lender is expecting to be paid back i.e. the borrower will need to show some debt servicing capacity. If that capacity is somehow damaged, debt can get obscene super fast.

once this idea goes mainstream , and deficits are the cure all for everything…

guess who will get all the cash from the printing presses.

Buffet may have said as much around 2009. See apendix 7 on this new economic perspectives post. It’s an image and I’m on my phone otherwise I’d type it out. But it’s along the lines of ‘we print out own money we can’t go bankrupt like Greece. Stupid Eurozone countries have to their sovereignty. ‘

http://neweconomicperspectives.org/2019/02/what-you-need-to-know-about-the-22-trillion-national-debt-the-alternative-interview.html

I think it is neoconservative and neoliberal thought that’s “informed” politicians’ economic understanding – such as it is – since Reagan. The neoliberal model apparently insists on government austerity during deep recession, judging from govt’s reaction to the great financial crisis of 2008.

I went back and reread Philip Pilkingon’s 2011 essay on the Austrian (not austerian) school economists’ theories. These two paras now stand out as relevant to what NC has been saying about the flimsey intellectual underpinnings of government’s justification for austerity. Govt premised its reasons on faulty economic theories.

In short, they [the Austrians] postulated a theory and then when confronted with the inconsistencies of the theory when it was applied to any practical ventures they simply threw up their arms and claimed that such inconsistency showed just how true theory was and how much we should respect it. The knowledge that the theory imparted then became, in a very real sense, Divine, in that we meagre humans would never be able to grasp it and instead should simply bow down in front of the Great Being that possessed this knowledge – that is: the Market.

…

The Austrians were never quite content with the chicanery and political posturing that they had passed off as scientific debate. As alluded to above, their theories about market prices were forged in the debates with those who advocated a socilialistic planned economy. Being ideological to the core, the Austrians were, for a while at least, perfectly content with saying that while no economist could say anything worthwhile about price determination – and thus, any attempt at a socialist planned economy would be doomed to fail because there could be no perfectly informed coven of evil socialist economists who could administer it – they were still happy with the airy theory of market prices that they had just poked such a large hole in.

https://www.nakedcapitalism.com/2011/12/philip-pilkington-libertarianism-and-the-leap-of-faith-%e2%80%93-the-origins-of-a-political-cult.html