Yves here. As readers no doubt recognize, when official forecasts are this dire, the odds are non-trivial that reality will be markedly worse. And what do airlines do with all those airplanes in the meantime?

Also note how fat this tail is proving to be compared to historical examples of “ZOMG Bad!”

By Wolf Richter, editor at Wolf Street. Originally published at Wolf Street

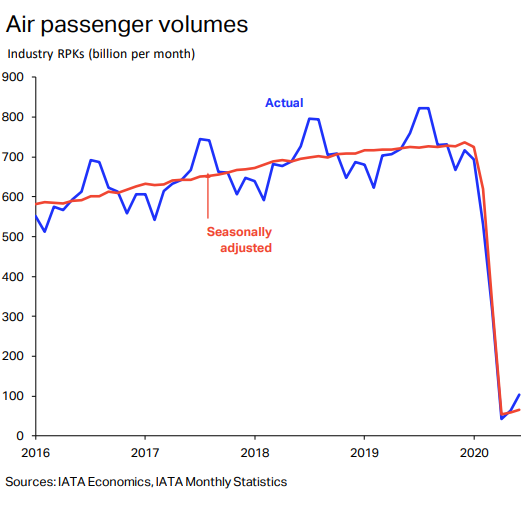

Globally and industry-wide, a measure of business for airlines, “revenue passenger-kilometers” (RPKs), in June was still down -86.5% compared to June last year, but a smidgen less bad than in May (-91.0%), according to the IATA’s newly released analysis. By comparison, during the six months following the 9/11 attacks – “considered to be the most severe aviation crisis prior to 2020” – revenue-passenger kilometers declined by 12% (the next three charts below via © International Air Transport Association, available on IATA Economics).

Passenger volume. Worldwide, the recovery, so to speak, occurred mostly in domestic air travel, which in June was down -67.6% compared to June last year, an improvement from May (-78.4%).

But international air passenger volume in June was still down -96.8% from June last year, and only a minuscule 1.5 percentage points up from May (-98.3%), which had been as close to zero traffic as you can get without actually reaching zero.

International flights have been handicapped by travel restrictions many countries have still in place. Even if people wanted to fly to some distant destinations either on business or vacation, they might not be able to, or would have to subject themselves to long quarantine periods, coming and going, making shorter trips practically impossible.

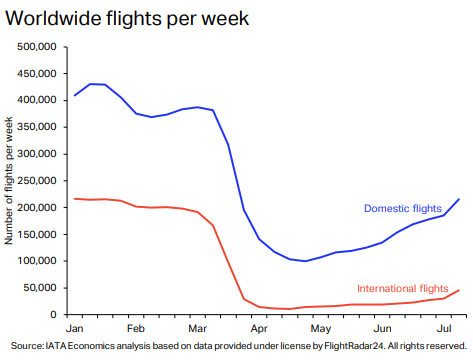

The number of flights on domestic routes worldwide rose in June and into July but remained down by about half from January pre-Covid. The number of flights on international routes ticked up in late June and into July as the EU’s Schengen Area lifted border-crossing restrictions, but remained dreadfully low:

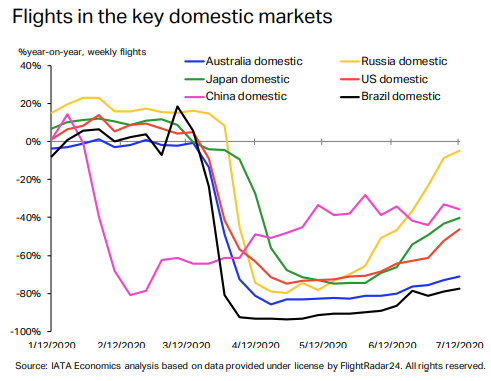

By country, the number of domestic flights recovered more in some countries than in others. In Russia, local carriers resumed all of their domestic flights in June, and in terms of the number of flights, air traffic by mid-July was nearly back to normal (yellow line). Chinese airlines started to add domestic flights in late March, but then renewed outbreaks occurred, which has put the recovery of flights into a holding pattern since May. US airlines were adding flights in May and June for summer travel season (red line):

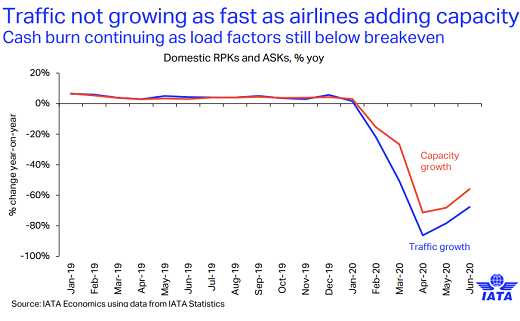

Industry-wide capacity has been slashed radically starting in February, as airlines tried to grapple with the collapse in air-travel demand. Then, from the low in April, airlines started to add some capacity. In June, industry-wide capacity, as measured in available seat-kilometers (ASKs) was still down -80.1% from June last year, but a slight improvement from May (-86%).

Airlines have been adding capacity on domestic flights (red line) faster than air travel has grown (blue line), widening the gap and contributing to the cash burn (the next two charts below via IATA’s Presentation, © International Air Transport Association, available on IATA Economics):

The industrywide passenger load factor – the percentage of available seats filled – remained at an all-time low in June, at 57.6%, down by 26.8 percentage points from June last year, despite the aggressive reductions in capacity in February, March, and April.

Every region but Latin America experienced record low load factors in June. Latin America experienced its record low in May (54%), which rose to 66.6% in June. In North America, 52.4% of the seats were filled, in Europe, 55.5%, in Asia Pacific, which includes China, 63.8%. The load factor of Africa’s airlines plunged to 16%.

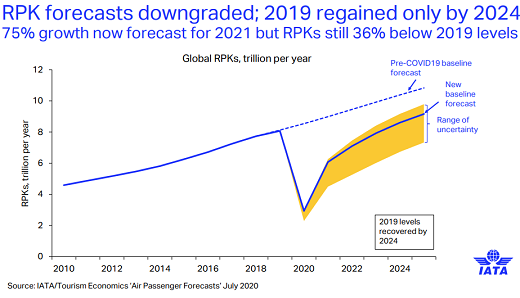

The IATA forecasts a funny-looking V-shaped recovery in revenue passenger-kilometers (RPKs) which sees the 2019 level of 8 trillion RPKs to be “regained only by 2024”:

The data for the IATA report reaches into mid-July. But in July, renewed outbreaks in the US have started to hit the air travel recovery in the US, and since early July, major US airlines started warning about renewed declines in ticket sales.

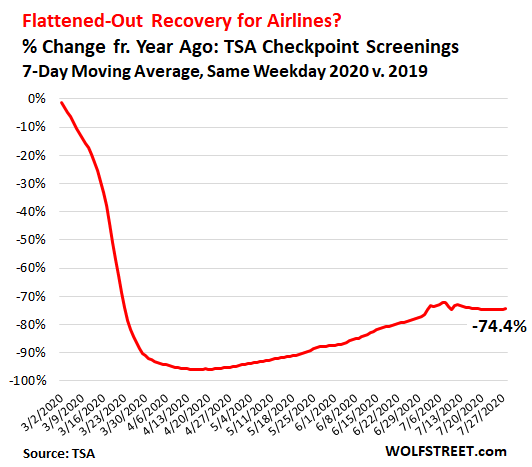

TSA checkpoint screenings, which measure on a daily basis the number of people entering into the security zones at US airports, were down -78.0% yesterday (Tuesday) compared to Tuesday in the same week last year, according to TSA data this morning. This was the biggest year-over-year decline since June 28.

The seven-day moving average, which smoothens out the day-to-day volatility but by definition lags a few days behind, has edged down from its “peak” in early July and has now been essentially flat for July, with the recovery of passenger volume having started to backpedal slowly since early July:

In the greater picture, I’m not sure how significant this is, but its reported in the Irish business papers (aircraft leasing is a huge industry here), that a number of airlines are doing sale and leaseback deals on their existing aircraft. I can only guess but that these deals are far more favourable for the leasing companies for the airlines, which is another way of saying that even if there is a full recovery in (say) 2 years time, many airlines will find their cost base far higher in the longer term because of deals they’ve struck this year.

Just spitballing, but I wonder if in a few years time we’ll see the established players who survive under additional pressure from a combination of debts along with competition from a new generation of discount airlines taking advantage of a host of unwanted second hand aircraft to undercut their costs. If fuel costs stay low, the advantage of flying new generation, more fuel efficient aircraft may well be undercut.

Whichever way you look at it, those airlines which can’t throw themselves to the mercy of massive government bailouts are toast.

That makes me wonder: where do the lease companies get their capital from, to buy those aircraft? It’s not like they are in a good position at the moment. Their customers are going bankrupt, demand for their product has collapsed and their balance sheet is mostly aircraft – which used to be seen as predictable assets, but probably not right now.

The leasing companies rarely have much of a problem getting cash because (unlike most airlines), nearly all their investment is in tangible and fungible products (i.e. aircraft). So at least in the short term, they are in a much better position than airlines. But obviously in the longer term, if there is a huge surplus of aircraft floating around, then they may end up like second hand car dealers in the middle of a deep recession.

But some may well be calculating that they’ll end up the long term winners, especially if major airlines simply can’t raise capital for new aircraft, then they’ll have to rely more on the leasing companies. Plus, the sale and leaseback model may end up being very profitable for them.

If I was to make a wild guess, in a few years we could see a wave of debt free new discount airlines being formed using cheap used aircraft to take what exists of market share away from established names. The leasing companies could be the midwives of these airlines. Ryanair, one of the worlds biggest discount airlines, came about this way in the recession of the late 1980’s – the ‘Ryan’ of Ryanair was Tony Ryan, the owner of a leasing company who thought it would be a good idea to use surplus 737’s in his stocks as a side business to undercut what he saw as sleepy national airlines.

Kindly correct me on this if I’m being ignorant, but I thought that used car prices go up in recession, because new cars are less affordable, and new car pricing tends not to erode.

It varies, some get their funds from selling bonds using their high credit-rating and some might even have the cash just lying around waiting to be lent out (very few, if any). The exact funding differs between the different companies, there is probably a mix of long-term and short-term bonds.

A story from the Irish state broadcaster:

https://www.rte.ie/news/business/2020/0704/1151391-covid-19-crisis-or-opportunity-for-aircraft-leasing/

One quote from the article:

And directly afterwards then this:

The whole article might be worth a read. There is one named leasing company in the article so reading up on that one might give an indication of how the aircraft-leasing companies obtain their funding.

Possibly the weaker ones will go under leaving the stronger ones with better odds of surviving, the article ends with: “Only time will tell”

What tends to be forgotten is that airlines themselves are simply providers of services to get people from A to B, and so only one part of a complex and tightly-integrated process. Unless both the desire to travel and the practical possibility of travelling exist, they have no market. This applies even at the most banal level: “let’s go and get pissed in Prague this weekend!” OK, but you need not only cheap and frequent flights to Prague, you need cheap hotels where they speak English, cheap restaurants ditto, cheap and reliable transport from the airport, something to do in-between bouts of getting pissed, and, of course, an environment which will enable you to, um, have fun. If one of those things disappears or becomes too expensive, then it doesn’t matter how safe and cheap the airlines are. The same is true on a larger scale with business travel, which depends on a very large and complex (not to say costly) infrastructure, some of which may be about to disappear. Airlines are a very complex, high-cost, part of an international travel web, but they are only part, and dependent on other elements which are much more vulnerable.

And I’d add to all that the cultural aspects of rapid travel. Its not really so long ago that people flew either for business (a very small minority of business people), or for their annual holiday. The notion of flying for weekends away or having your wedding in an exotic location, or to see a London show or whatever, was entirely alien, even to pretty well off people. But its now entirely normal – a few months ago one of the cleaners in my office was telling me how sad she was that she couldn’t have her annual easter break in Spain this year. For people under 40, hopping on a plane is no different from catching a bus.

As you say, this is entirely dependant on a huge, complex set of interrelated processes and infrastructure, ones that are now unravelling at speed. Its very difficult to predict the outcome. Although one interesting little anecdote is that the manager of my local car hire outlet told me that they’ve had a surprising uptick in business over the summer – mostly in the small number of tourists, in addition to locals, deciding to do a traditional driving holiday around the coast of Ireland. This was the typical ‘holiday in Ireland’ 30 years ago, but it’s now become popular again. I think one outcome will be the revival of the long summer holiday, replacing multiple ‘breaks’ over the year. This is probably good news for campsite owners, terrible for anyone with a hotel in a major city.

Hadn’t thought about it in terms that you said but yes, we are talking about an ecology of travel here. Take one component away and the whole system become no longer viable. With a much smaller market for the foreseeable future, I think that we may see an amalgamation of airlines and those that are left will be the ones to receive government support. Yes, so the government will get to pick the winners.

So a country that has an internal and an international airline might combine the two into one entity. And a country that has two or more internal airlines might let them combine into one. They will be monopolies supported and underwritten by their government but that may just what the inevitable result will be. A fair government would ensure that seat prices don’t go sky high as they will be monopolies but that will depend on each country’s government.

“something to do in-between bouts of getting pissed”.

Doesn’t apply. At least not in Prague, based on what I’ve seen. Just one massive round usually started already on the departure airport, ending on the way home from the same airport.

Oh dear, I was afraid you might say that. I was hoping the reality might be slightly better than the accounts I’ve had of it, but evidently not.

Well, some are somewhat better (a friend of mine does a brisk business taking them to a shooting range where they can shoot anything from a handgun to a machine gun. But last year he was getting worried, as a lot of his clientele stopped being young white Brits and become young Brits of ME/Asian descent).

But a lot of them can remember the first pub they were in, and that’s about it. The real problem is that a 0.5l of beer can be as cheap as 20p, and the Brits can’t hold their drink really (I have friends who can do 20 beers a night and walk home, and can do it regularly few times a week. That would kill most British tourists. The trick, apart from lifelong training, is to go slow and steady and eat).

There is very much a ‘get drunk quick’ culture in England as opposed to other drinking countries. Back in the 1990’s a friend of mine worked in research for a major Dutch brewer. He was telling me about how they adjust the same beer for local taste far more than people realise. They found that in England they initially lowered the alcohol content of their beer to around 3.5% to match traditional ales and milds when they entered back in the 1960’s, but gradually increased to 5% and higher in line with demand. But in Ireland, the priority for drinkers was to drink lots of beer while still standing at the end of the night, hence they wanted lower alcohol levels.

I think this is one reason why you see a big difference in the beers sold in big city centre pubs in England – all strong beers, served quickly, whereas when you go to the increasingly rare olderstyle pubs that serve a more traditional drinker, they sell mostly traditional session beers.

Yes, I think people can lose sight of all the moving parts and how they fit together. A good example is the EU opening up to tourists from New Zealand. Anybody in the tourism industry might be forgiven for hearing that and assuming that some actual tourism might result. The small problem is that there’s already a backlog of >1 year to get into New Zealand just considering citizens and residents, and it’s also been announced that people will be charged for their quarantine stay under certain circumstances (tourism would certainly fall into that category). Who would set off on an overseas holiday without knowing when, or if, they might be able to return home? If the current volume of tourism from NZ to the EU is anything above zero at this point, I’d be amazed.

This morning I heard an interesting comment about a big conference later in the year that has gone online. Apparently, a factor in the early decision, previously they indicated they would only announce in August, was that they lost their venue because it has been converted into a temporary Covid19 hospital. As has their second choice venue. And so those conference venues are no longer available for late November. Which means somebody expects the hospitals to be needed then! A sign of how bad this still can get?

I don’t know if anyone else has heard about conference centers new role?

This is another wrinkle in the change of the broader business travel system.

I’ve heard that the models are predicting an early winter crisis if a bad flu season overlaps with a winter wave of Covid. Certainly in Ireland thats what they are preparing for in terms of hospital capacity.

Funny you should mention this, Koldmilk. Look what’s happening down at the Tucson Convention Center:

https://kvoa.com/news/2020/07/21/tucson-convention-center-may-be-used-as-an-alternate-care-site-for-covid-19/