Patient readers: One more cross-post while the Internet is out in the Third World country where Yves currently resides. I am to ask if UK readers, especially Colonel Smithers, agree with Murphy’s thesis. –lambert

By Richard Murphy, a chartered accountant and a political economist. He has been described by the Guardian newspaper as an “anti-poverty campaigner and tax expert”. He is Professor of Practice in International Political Economy at City University, London and Director of Tax Research UK. He is a non-executive director of Cambridge Econometrics. He is a member of the Progressive Economy Forum. Originally published at Tax Research UK

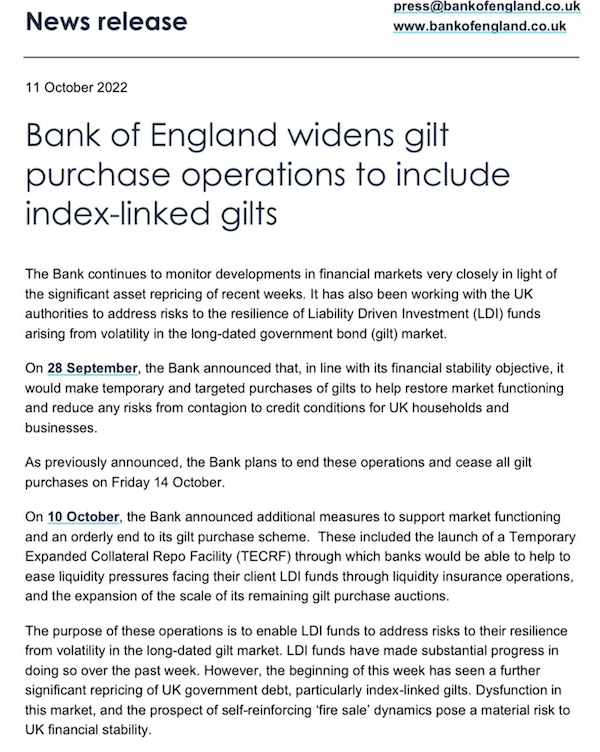

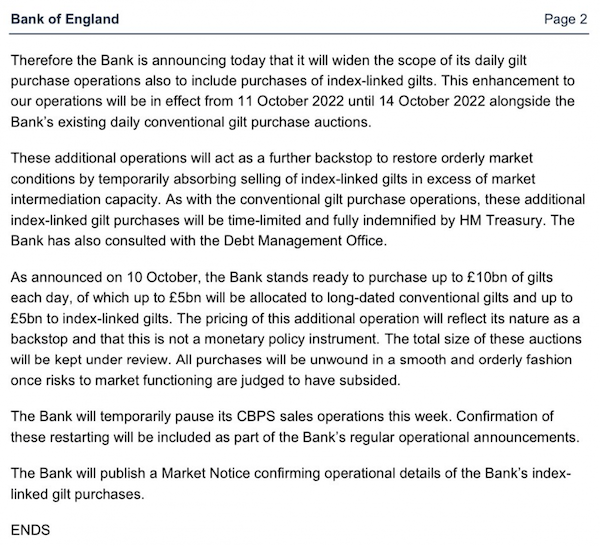

A pile of commentators have appeared on this blog over the last day or so telling me that the interventions by the Bank of England in financial markets are in no way related to pension funds and do not benefit them. Many have been deleted for their tone. A few I have posted to make clear just how wrong they are.

Why are they wrong? Because they look at what the Bank is doing by buying gilts through a QE process and say that this does not directly help the funds. It does instead provide liquidity to conventional (and now index-linked) gilt markets. So, they claim that pension funds do not get direct help.

Why do I disagree with them? Because the crisis has been caused by illiquidity in markets caused by gilt sales by pension funds desperate to sell assets to cover calls for collateral cover.

What is the aim of the intervention? It is to take away the need for those urgent sales by funds at what are likely to be undervaluations.

Do the pension funds benefit as a result? Of course, they do. But it’s not direct, and so those criticising me say I have got it all wrong.

So what is going on here? That’s easy to explain. Those who are criticising are looking at what is happening as economists do. They see market interventions as a result of which pension funds need not sell so they say pension funds are not involved. As a political economist, I ask why the intervention is happening, which is so that the pension fund may either not sell, or may do so in an orderly fashion with smaller losses, and so, of course, the pension fund gains.

Which approach is more useful? That is the political economist, of course, because they answer the real questions in life.

And how do I know I am right? The Bank of England says so. Take these comments from the Bank of England issued this morning as they extend this emergency programme as evidence:

LDI activity is essentially only by pension funds.

Those seeking to make similar comments again today will be deleted.

All getting a little close to home.

Omg

82%

There’s no rationale for that kind of allocation.

Except: The UK govt guaranteed those pensions.

Oops: the pension funds need to make margin calls!

Oops the Treasury needs to make those margin call

Oops: the gilt market is f@#

As the late,great chalmers johnson used to remind us;

To ask the question is to answer it,

The exposure of the 5000 or so most valued professionals seems to be patent in this document.

I would place a bet that they would do.

Can I just check, is that 82% in that asset class, or 82% with Legal and General? The bit of the article that is not paywalled seemed to indicate the latter rather than the former.

Thank you, Lambert, especially for the shout out.

Murphy is correct, especially his focus on the political motivation and bringing political economy back into public discourse.

The Bank of England is bailing out pension funds, from the chancellor’s incompetence, the mismanagent of pension schemes, not just those engaged in liability driven investments and something going back decades, and the lack of oversight of investment firms / funds and migration of risk, especially, credit by regulators, again something going back decades.

In March 2021, the Bank warned about liquidity management by funds, especially open ended funds, and stressed the need for better product, risk and fund governance, but little was done, especially as the priority was for the Bank to support the covid stricken economy.

The worst affected firms are Legal & General, as Paul states above, BlackRock and Insight.

There’s worse to come.

Thank you, Colonel Smithers.

One wonders if the focus on pensions and the middle classes’ financial hopes for a comfortable retirement during their working years was an empty promise. Not a happy thought, if it’s true.

Another factor at risk here, getting little attention that I’ve seen so far

https://www.ifre.com/story/3544414/derivatives-clearing-exacerbated-ldi-cash-crunch-yrp11f0qrn

One of the key post GFC safety mechanisms, centralized Clearinghouse for derivatives (CCP) is being put to the test here.

Both the Pension funds themselves and the health of the CCPs are the drivers behind the Golt market bailout.

A cascading failure of the CCP on the entire derivates market would be catastrophic, and sudden.

Thank you and very well said, Michael. If matters continue to spin out of control, I reckon we will look at 2008 fondly.

Indeed

And I’d like to be proved wrong.

A quibble tho:

L&G aren’t the most exposed.

It’s bigger than them

And the dream will be over.

The empty tower of babel after the land of cockaigne.

Thanks, Bruegel, you could have warned us.

Immanuel Wallerstein did try to keep the flame.

.

There is an FTAlphaville post on clearinghouses’ role in this today.

The post has some pretty heated comments but it is seemingly agreed that the clearinghouse’s current margin system has exacerbated things (amount of margic vs uncleared practice, only takes cash not specie).

https://www.ft.com/content/e694e5e7-5b96-43a7-8909-2b35ad3e8d4b

The pension funds are simply going to double down on all risky bets. The Bank of England is guaranteeing all their losses. Not a regulator in sight! Just a big sugar daddy.

Does that come as a surprise?

There was a blogpost which I am having trouble finding again saying that the real problem is not the headline movement in gilt yields but the uneven distribution of the damage among the pension funds:

– the major pension funds (single schemes with big asset bases, probably running bespoke LDI programmes) were squeezed but stable

– some LDI funds in which multiple small pension funds had invested were being taken to the cleaners and some of them had dropped to zero NAV as a result of yields spiking and therefore bond portfolio values tanking, having to sell the best tanked bonds for cash to meet margin calls, and being structurally leveraged (this part I am bit hazy on but essentially the LDI scheme is implemented synthetically as a swap between two parties’ different cash flows rather than by holding physical gilts because the synthetic route is cheaper (and, like all structured products, deadlier) and by implementing it more cheaply, the LDI fund managers would make more money but this results in the LDI fund being effectively leveraged up to 7x….

– the real scandal being the counterparties to the gilt sales (remember, folks, finance is a zero-sum game) because these are thought to be the investment bank LDI desks taking their clients to the cleaners because they smell blood

So the net result is a lot of the more marginal pension schemes just found their LDI fund investments toasted by the investment banks. Not a good look.

To make it worse, apparently the large pension schemes are UK tax-resident but most of the LDI funds are offshore

I will try to find the link to post.

Pensions were the great promise to the now retiring generation as a financial guarantee for their life long hard work.

Found it, it was a comment to an FT Alphaville article (https://www.ft.com/content/3859dc18-f151-4210-b49e-3ae9a13c3976) by Irish HF Guy:

“The BOE letter explains it was mostly the pooled LDI funds which are outside of the UK and have as investors a lot of small and medium sized DB schemes. I think the larger schemes are okay and can call the large plc sponsor for cash. The pooled LDI funds could not, and it seems they were potentially wiped out from an NAV perspective (which is true is unbelievable). Pension schemes and LDI managers are regulated by The Pensions Regulator (TPR) and the Financial Conduct Authority (FCA). LDI funds themselves are typically based outside the UK.

https://committees.parliament.uk/publications/30136/documents/174584/default/

I also 100% believe that the investment banks trading the other side of this -v- L&G, Schroders, Phoenix, Just Group Plc pillaged them pricing wise in providing liquidity.

Amazing, as usual the small guy takes most of the losses and the larger participants are okay.”

I read the BoE letter and it does indeed say (p4) that some LDI funds were on trajectory to have negative asset value!

Here is another bit of food for thought. Were LDI schemes missold by investment managers to pension scheme trustees if this handbook produced by one such investment manager is an example of the financial sophistication of said trustees?

https://prod.schroders.com/en/sysglobalassets/digital/fiduciary-management/cs1151-ldi-fp-jargon_v7_final.pdf

Eye-opening! It has to define counterparty, liability and nominal interest rate for the audience! Come into my lair said the spider to the fly….

Please pursue that question. Nobody seems to be asking it.

It looks like Orange Country all over, just with Central Bank support at the end.

On Richard Murphy’s article, it is a bit breathless. Is it so wrong that the BoE stepped into prevent disorderly market conditions (or disorderly market participants) wiping out pension savings?

Even if it is wrong, BoE would still doing the right thing for the wrong reason, seizing control of the yield curve. Interest rate rises are not the remedy for commodity inflation….

it wasn’t the interest rate rises per se that the Bank was using to try to save the pension schemes and, thereby, some banks; it was its QE intervention after the disastrous mini-Budget, so-called. Now, Kamikwasi is out of his job. Called back from meetings with the IMF to be sacked. Classy. And now Hunt has taken his job (I hope I’ve spelled his name right.).

Having never heard of LDI b4 as I’ve had no Pension fund experience, it was kind of a hoot to discover its definition.

Since managing future expected liabilities v current asset accumulations + expected returns is Insurance/Pension actuarial 101, I was surprised to learn LDI is even a thing.

Unless you are massively and systematically underfunded, as most pension schemes likely are, I suppose, and until you’re faced with an AIG like situation where mark to market rules (ie derivates clearing ) force you to pay up today for losses you expected to defer into the future, you are sheep to IBs selling you product to cover your incompetence in mismatching your liabilities. The IBs know you’ll need to be bailed out by your govt, as they did w AIG.

DejaVu all over again.

Nobody wants to use the word socialism, but that’s what these bailouts are. Selective socialism in order to protect capitalism from it’s own demise.

May I suggest Professional Socialism?

A lot of 2008 nostalgia here. Profits are the hard earned rewards for risk taking creative financial wizards. Losses are nobody’s fault, like thunderstorms they just happen.

Privatize the profits-Socialize the losses.

Heads I win, tails you lose

Tangentially relevant.

Wanted to post this where it could be caught as I’m always too late in the daily links for comments to be useful.

Here in Australia we have 4 major banks, well known as ‘the big 4’.

Westpac. National Australia Bank (who rebranded to the refreshingly candid NAB.) Commonwealth Bank. And, ANZ (stands for Australian New Zealand Bank)

All got a public bollocking in the Royal Commission on Financial Services a few years ago.

Last night I was speaking with a colleague, a highly respected and potent professional at law. He also provides cutting edge financial services. Masterful reputation. His successes appear on the front page of newspapers and are sometimes the first time a particular success in law has occurred in Australia’s history. (For example, he got a farmers property back 12 months after a court order to repossess it. Never happened in Queensland before.) He is literally feared by the establishment. Naturally he is well informed and connected. He told me yesterday he has a precious metals broker who is also very respected and connected. This broker told my colleague, Westpac and Commonwealth Bank have just approached the Australian Government for a bail out.

And, ANZ are not far behind. That was the verbatim message. Feels like something Yves would appreciate being aware of. Hope you catch this :-) x

Any clue what’s tanked the aussie banks? Real estate hasn’t declined enough to be the culprit has it? The four are definitely still inflating and gouging profits from bubble prices over the ditch here.

… the refreshingly candid ‘NAB’…

:)

Excuse me for saying the obvious, but if the purpose of the Bank of England is to benefit pensions, would not the most efficient way to do so be to digitally create GBP and deposit them into pension accounts?

Of course it would. Of course that is empirically and indisputably the most effective way the to save pension accounts. That would cut out the ENOURMOUS BLOUT of ravenous financial markets that the Bank of England is currently using, with great inefficiency. Or great efficiency is it’s goal is to support financial systems at the expense of pensions.

So, that means we know with total and complete certainty that what Richard Murphy is totally and completely false and has no idea what he is talking about.

Put another way, the BOE is using financial markets to help pension funds in the same way Obama used insurance corporation to help deliver healthcare.

Q1: Is Social Security considered a pension fund?

A: Believe the answer is No, but of course a lot of seniors think it’s the equivalent. And they vote.

Q2: If it’s not–and I think there’s a very powerful constituency (if that’s the right word) that claims it isn’t–will the Fed/Treasury protect payments to pensioners?

A: No. They’ve been preparing the script for years.

What do you think?

With apologies to Keynes, when the pensions of a country become a by-product of a casino, the job is likely to be ill-done.

If the Bank of England has to bail them out anyway, why have private pension schemes in the first place? Because it’s a grift for spivs and “jobs for the boys” …

Claudia Sahm tweeted on this yesterday:

“Toby Nangle on What We Just Learned From Gilt Market Madness” (via Odd Lots Podcast, omny.fm)

Just under 47 minutes, but worth it.

Toby Nangle is also the author of the FTAlphaville blog that I linked above. It was very good and not 47 minutes long!

Video is so low bandwidth as a medium of instruction – why can the world not be transcribed!

Ha! Sorry! I missed your comment above. I had the free time, so listening wasn’t too bad, but I agree on transcription being very easily consumable as well.

Is the real problem here the LDI approach itself which as a concept feels benign: to match expected cash outflows to the pensioners with projected cash returns via a suitable portfolio strategy. Although I do understand that specific vehicles used for this may create additional risk (as well as nice fees for whomever sold these instruments).

Or is the real issue that rising nominal interest rates are reducing pension asset values, especially those that have a fixed £ return (as traditional bonds typically do). This in itself would worsen the financial position of pension funds. Given that their liabilities are inflation linked based on the promise to the pensioners then I see a double whammy.

The immediate collateral based margin calls and forced bond sales that the Bank is addressing by gilt purchases may just be the immediate symptom of a bigger issue?

I am not very up on specific terminology for all these things, which often obfuscates the underlying drivers (perhaps intentionally) so if anyone understands what is really going on then that would be super helpful.

The issue is “cakeism” ((c) Boris Johnson), I.e. trying to have your cake and eat.

In a defined contribution scheme with new members joining, you can assume an infinite time horizon and you can invest in equities, which on average will deliver you growth in line with the wider economy so, bar some cashflow smoothing, you are matched (just don’t promise guaranteed increases, Equitable Life!). There may be mark-to-market accounting impacts on pension sponsors or simply they did not like the level of contributions required so they closed these defined benefit schemes to new members.

As soon as you close the scheme to new members, your membership is in run-off and your scheme assets need to meet actuarially projected liabilities. The projections depend on bond yields. Holding equities is now risky because your cashflows may not match. Swapping your assets into bonds that have the right repayment profile is less risky.

However, your pension scheme needs to be well funded to do this and still pay out well, especially when yields have been as low as the last decade. Jonathan Ralfe did this for the Boots pension scheme c. 2000 and has dined off his foresight ever since. His pushing others to do it later during ZIRP just locks in low returns.

LDI strictu sensu means this but pension fund sponsors were not willing to over fund the schemes to enable a switch to LDI where the fund held physical bonds and in such quantity that returns were acceptable to pensioners. So the investment banks invented LDI where much less capital is required because the bond cashflows are synthetic: the scheme enters into a swap agreement, buying a cashflow of the required profile from an investment bank in exchange for cash payments to the swap counterparty. The initial cash down is much less, freeing up capital to be invested in higher yielding instruments (equity, investment grade bonds, junk bonds, private equity, real estate, commodities), some of which are illiquid and some of which are liquid and are on stand by as cash equivalents for any short term payment obligations.

The problem with swaps is the margin calls. When gilt yields went up, the value of the payments required from the LDI buyer went up – hugely! These had to be met from selling liquid assets, starting with gilts. This drove prices down and yields higher. A doomloop was born. In extremis, a pension fund could burn through all its cash and cash equivalents on margin calls and have nothing to sell, just illiquid assets (pennies on the pound if sold in a hurry rather than held to maturity) which could not be realised in time and would then default on the swap agreement.

Apparently funds which had enough assets to buy real bonds to construct their LDI portfolio were OK. They would have some nasty mark-to-market losses on the NAV but they would hold the bonds to maturity and pensions would be paid fine (even if the pension sponsor would have to pay in more in the interim to cover the shortfall in accounting terms).

Poorer pension funds which had bought swaps were essentially leveraged up to buy higher yielding illiquid assets and were in trouble. This included some independent asset management funds with multiple pension fund investors, which aim to give small funds access to LDI.

The real problem is the fallacy of debt. Just because you expect it to be serviced and repaid doesn’t mean it will be. So funding and economy with debt and creating a financialised tower of debt relations is just jenga, at some point a block will be removed and the whole tower collapses.

What the world needs in almost all cases and certainly on multi generational timescales like pensions is equity funding. Equity returns to fund participants and equity investment by the funds into the real economy.

Thanks for a comprehensive answer. I think I get it now.

They created swap (or debt) instruments as a sleight of hand to pretend all was well by matching cash flows through holding bonds while hoping to achieve high returns at the same time by holding illiquid assets. Cake and Eatism, as you say.

But that sleight of hand can never be a true substitute for having enough capital to start with, or finding ways to achieve the necessary returns to make it so. The rest is then mechanical. If I own the bonds 100% with no debt and the cashflow of the bonds fully matches my expected future outflows then ultimately it works, and is not a cake and eat it strategy, although as you say the accounting rules may cause drama and my scheme needs to have been super well funded.

But if I am effectively holding the bonds via debt that I have to service then I am in cake and eat it land. The fall in the bond value as yields increase creates a margin call with more cash needed to satisfy the lender. So I have to sell other assets to fund this. These are very same assets that I have been holding in the hope of securing higher returns as part of the “strategy” and this creates the spiral you mention.

I met John Ralfe a few times when he was Treasurer at Boots back in the 90s and I happen to have a deferred Boots pension from the several years I spent there. At the time, his model was seen as very innovative. It is only “safe”, of course if you have the capital required to make it so in the first place. Otherwise, you effectively just create a debt Ponzi scheme.

Agree with you fully on equity. Pretty much everyone who has a defined contribution pension pot (as I have apart from the Boots component) holds the investment as equity, except possibly immediately pre retirement to avoid short term equity dips. Odd that the “experts” are doing something else. How a debt based swap strategy beats just holding equity in the first place and not having bonds at all is not clear, but I am sure the banks had some very convincing arguments. Would not be too surprised if accounting sleight of hand is in there somewhere too.

A few days late on commenting here, and I hate being a nit-picker or pedant, but what are internet comment sections for if not that. And so I’ll contest the thesis at the title of this post. I understand that these pensions engaged in non-vanilla behavior, and due to ZIRP, introduced risk via leverage that exposed them to mark-to-market loses. I understand that the BOEs actions are helping to soften the loses of pension funds to the extent of preserving their existence. But the BOEs actions aren’t a bailout of pensions, they are a bailout of Gilts, of His Majesty’s credit, and of the UK itself. Pensions just happen to be the immediate beneficiary here, at least via headlines because Blackrock has better PR.

The GFC shapes our modern understanding of financial crisis and response, and so the inclination to interpret this action as a “bailout” of bad behavior is strong. And in some sense it is just that, but the bad behavior isn’t the pension funds it’s the UK government’s. Unlike in 2008, the assets getting clobbered aren’t fraudulent securitized loans and their derivatives- private debt on private balance sheets. The bad assets are public debt, level 1 High Quality Liquid Assets. If these are “fraudulent” or just sh*t collateral then they indict the government and its system, those pensions are just idiot victims in the fraudulent scheme that is the UK.

Now as a “modern” western central bank the BOE can buy Gilts to their heart’s content; but QE is just an accounting gimmick on the upside with a socially predatory downside. So rather than take their lumps and try to salvage something of a society they’ve decided to save the “value” of their pieces of paper and send their people to a future of indignity and destitution. As they say in jolly olde, cheers!