Due to having competing obligations, your truly is being more curt about the wobbles in financial stocks than is ideal.

As we wrote yesterday, the small but high profile Silvergate Bank is liquidating and said it will make depositors whole. Nevertheless, an actual bank, as opposed to crypto exchange, shuttering (particularly with fraud investigations in the wings) has focused a few minds.

The crypto collapse has been triggered by Fed interest rate rises. Many of these inexperienced players managed their dollar investments poorly, and got caught (as even many banks have) with too many exposures to bond/loan maturities that dropped meaningfully as short term interest rates rose. The yield curve has gotten even steeper due to the central bank making even more hawkish noises better-than-the-Fed-wanted economic data came in. That would worsen losses at financial firms that wrong-footed their exposures.

And of course coins have fallen in values, some coins are pretty much dead, and crypto business is down generally.

That lead Silicon Valley Bank, which is a bank to many tech players, including crypto firms, to decide it needed to hunker down. It decided to strengthen its balance sheet while the getting appeared to be good while also announcing a plan to shrink its deposits (actually pretend it was choosing to shrink its deposits; the more accurate presentation would be that it would reduce overheads in light of its projected contraction in deposits).

As a very good piece in TechCrunch explains in detail, the meltdown at Silicon Valley Bank is a self inflicted wound. Yes, investor and depositors were rattled by the fundraising coinciding with the Silvergate implosion. But what apparently triggered the bank run was the CEO doing an absolutely terrible job on a conference call and triggering panic. Then when some big depositors were told there would be delays in getting their funds transferred, the stampede began.

We’re also cross-posting Wolf Richter’s post on Silicon Valley Bank for you car crash fans.

A source tell us that it wasn’t just the crypto/tech industry depression that had Silicon Valley Bank management worried:

They wrote the fund-level subscription line on a very large portion of small to midsized institutional PE funds, which appears to be a driver to some degree of their liquidity crunch.

Subscription lines, aka subscription credit lines, are loans to private equity funds. This is an additional layer of leverage on top of the lending provided to the companies they buy. These lines are secured not by those companies but by the uncalled capital of the investors in the funds. It was once seen as inconceivable that these investors might default, since they would lose their existing investment in that fund. But perhaps that risk is looking real for funds with weak investor and/or doggy portfolios (like ones with too many bad tech bets).

But let us go back to the ultimate cause. The Fed has known since before the 2014 taper tantrum that it has kept rates too low for too long. It took Covid-induced supply chain disruptions and labor market tightness and sanctions blowback to generate too much inflation. The government has been unwilling to do the heavy lifting to address at least some of these bottlenecks. We also have the not-trivial problem of companies admitting they are price-gouging because inflation in visible sectors like food makes other price rises look warranted when they aren’t. Jawboning, excess profits taxes, bans on stock buybacks could help but nothing like that has even been attempted, Instead the government has relied on the heavy hand of the Fed.

Unfortunately, the Fed will have to really kill the economy to bring demand for workers down enough to make the central bank happy, particularly since the Administration is pulling in the other direction by spending on job-reshoring schemes like the Chips Act and the Inflation Reduction Act.

It was damage to banks that forced Volcker to relent on his interest rate rises to the moon: their huge losses on their credit card portfolios and Latin American loans. Crypto-related damage isn’t enough to hurt the banking industry in a big way. But the recent short term interest rate increases were abrupt and large. Could enough banks be leaking below the water line to force the Fed to back off?

By Wolf Richter. Originally published at Wolf Street

SVB Financial, which owns Silicon Valley Bank, the 16th largest bank in the US with $210 billion in assets, came out with some fascinating announcements late yesterday and early today about shoring up its balance sheet and liquidity.

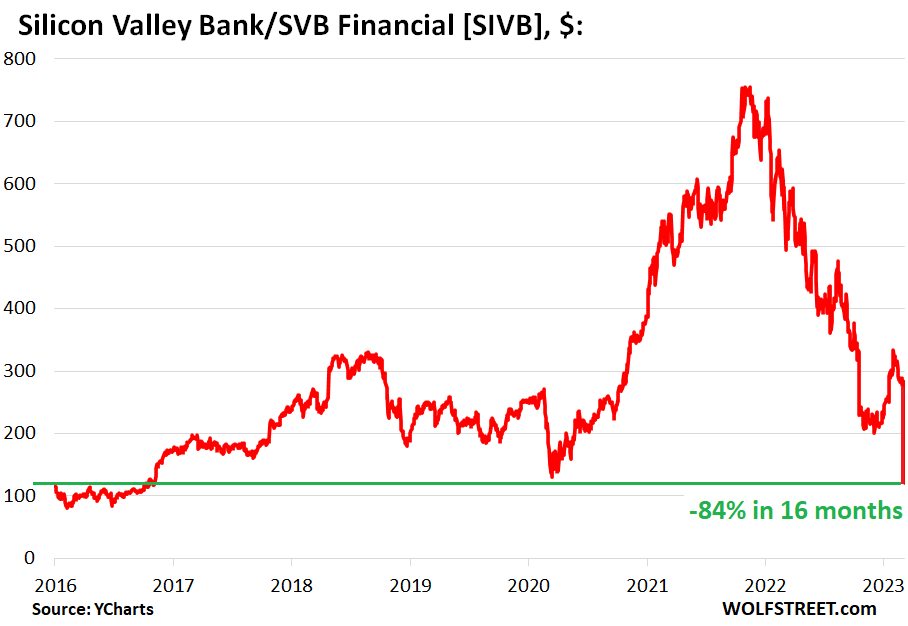

After having already plunged 65% in a series of breath-taking dives, and dead-cat bounces from their startup-and-crypto consensual-hallucination peak in November 2021, shares of SVB Financial [SIVB] kathoomphed so far today another 55%, to around $119 at the moment, the lowest since 2016, and are now down 84% from the November 2021 high, thereby getting inducted into my pantheon of Imploded Stocks. [Update: SIVB closed at $106, -60%; now trading at $85 afterhours, -69% in total for the day; updated chart in the comments. This is just stunning].

The 84% plunge from the high already exceeds SVB’s Dotcom Bust plunge of 77% from September 2000 through October 2002 (my discussion in July of this SVB phenomenon) The Dotcom Bust was a horrible creature for Silicon Valley, and SVB Financial is another indication that this current bust – we still have to come up with an appropriate name – promises to outdo the Dotcom Bust.

Silicon Valley Bank is heavily involved with all aspects of the startup scene. And the startup scene – across all sectors, from biotech to crypto, and across all stages, from early-stage outfits to companies that already went public – is getting the rug pulled out from under it by the collapse of consensual hallucination.

It had to happen some day anyway. It always does sooner or later. But now the end of easy money, after years of central-bank money printing and interest rate repression, is getting blamed, including by SVB Financial.

Get More Equity Capital

SVB said in a series of filings with the SEC late yesterday and today that it would raise $2.25 billion in equity capital in a three-pronged approach that is heavily dilutive for existing stockholders:

- A public stock offering of $1.25 billion of common shares;

- A private sale of $500 million of “depositary shares” to General Atlantic, a growth equity firm, which happens to be a “longstanding client of SVB”;

- And the sale of $500 million of mandatory convertible preferred shares.

Get Lots of Liquidity

SVB said that it was “repositioning” its balance sheet by having sold all of its $21 billion in available-for-sale securities, and that it booked a staggering loss of $1.8 billion on those sales in Q1 – so Q1 earnings are going to be a massive loss.

It said that it would place the proceeds in short-term securities and on deposit at the Fed to earn the higher short-term rates and improve its liquidity.

In addition, “to further strengthen balance sheet liquidity,” it said it would double its “term borrowings from $15 billion to $30 billion and hedge these borrowings to mitigate higher funding costs in the future.”

Preparing for the Mass Extinction Event Among Startups

“We are taking these actions because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients as they invest in their businesses,” SVB said in one of the filings with the SEC today.

“We expect these actions to better support earnings in a higher-for-longer rate environment, providing the flexibility to support our business, including funding loans, while delivering improved returns for shareholders,” it said.

So this is in preparation for what it sees will come its way in the startup scene after the free-money era ended.

When consensual hallucination collapsed, the IPO and SPAC bubbles collapsed and closed the exit doors for VC investors, so they stopped funding many of these companies. And suddenly, these companies have to survive with what they’ve got, but they’re burning cash like there’s no tomorrow, and they cannot cut costs fast enough, and they cannot get new funding – neither the still private companies from private investors, nor the already publicly traded companies via stock offerings.

“Mass extinction event” is now the term used by the VC community to describe what will happen to the vast majority of startups when they run out of money.

Many of these startups and their founders are clients of SVB across its divisions:

- Silicon Valley Bank: deposit outflow as startups burn cash until it’s gone and they shut down. And some loans may go bad.

- SVB Securities, the investment banking division.

- SVB Capital, the venture capital division.

- SVB Private, the private banking and wealth management division to cater to the (erstwhile?) multi-millionaire or billionaire founders.

All of them have fallen off Cloud 9 in a spectacular manner. And SVB is doing what it can to remain relevant.

Moody’s downgraded SVB Financial and Silicon Valley Bank by one notch. Moody’s report said that this “reflects the deterioration in the bank’s funding, liquidity and profitability, which prompted SVB to announce actions to restructure its balance sheet.”

Moody’s also downgraded the rating outlook from “stable” to “negative,” meaning another downgrade might be next, “reflecting the uncertain macroenvironment and specifically, the potential negative implications for SVB if the declining venture capital investment activity and high cash burn does not subside.”

OK, folks, we need to find an evocative name for this bust, a name that will make it into the annals of history, as did “Dotcom Bust.”

I look forward to a Jim Cramer freakout ala 2007, once again. They know nothing. It will be popcorn worthy for econ nerds, the quantitative inclined and general finance followers ( like myself ) if this is the line to cross for the FED / FOMC to begin to consider pausing.

And as for white knights in 2023, unless there is a looming CEO and idiot like Ken Lewis who famously bought Merrill Lynch for a lofty price, surely any functional major bank that can acquire this institution will be doing the opposite of the aforementioned Mr. Lewis. Investigate first, ask questions and then make an offer to acquire. BTW, thanks for posting as most of us know your list of tasks and duties is over abundant.

There is another lever the Fed seems to be pulling and might also be part of SVB’s actions.

The stress test scenarios this year are particularly severe in a couple of key areas. In the severely adverse scenario, the national house price drop is a 38% decline, and the VIX is projected to go to 70. Both of these are very extreme and rival if not surpass the changes seen in the last 20 years.

The goal seems to be to drive capital requirements up. This is going to hurt some banks. With over $100 billion in assets, SVB will have to submit results, and maybe they saw some scary early numbers.

Should be an interesting couple of months.

In my Internet ramblings I have watched some West Coast v-loggers mention the importance of the looming layoffs in the Silicon Valley Middle Management cohort for their local housing prices.(I believe several of the NC Commenteriat live in and around Silicon Valley. Any sightings “in the wild?”) When Pater and Mater lose their high paying Silicon Valley jobs and can no longer afford the mortgage payments, something has to give. Here, or there, depending where you reside, is a systemic shock to a large segment of the general banking sector for the West Coast; mass defaults on house mortgages in the high rent neighbourhoods. Already shaky banks could be pushed over the edge thuswise.

Let us not even speculate about those poor fools locked into Adjustable Rate Mortgages. The fact that ARMs are now a ‘thing’ again is a telling sign itself. Automatic rate increases as the ARMs follow the Fed interest rate rises will push a lot of those borrowers into penury. The knock on effects could be devastating for some formerly high flying West Coast service economies.

I would say; “Get some popcorn ready,” but have you seen the price of popcorn lately?

Everyone stay as safe as your informed Personal Risk Assessment allows.

I wonder also about rents in these areas, especially considering the aggressive investment money buying up real estate to convert into rentals. I don’t have deep understanding but I had been hearing that the investors were making very high cash offers that family buyers couldn’t compete with. It seems like those investors would need to buy all the stock as it comes on to the market to preserve high rents and reduce the hit to the incoming cash flows of their existing properties. If they have tons of cash on hand, maybe that’ll work. But if incomes keep falling, who’s going to pay the high rents?

Maybe the new feudalism won’t be arriving as soon as we thought.

Meanwhile, Bill Ackman who might well have a pile of his own capital tied up in ventures with ties to Silicon Valley Bank (or may have equity or other interests in it – he hasn’t disclosed), had a string of tweets floating the idea that the Fed should bail out the bank (beyond what it would do if it went under and triggered FDIC insurance provisions).

Of course, if saving this bank is such a good investment, then it seems obvious that he should put his money where his mouth it, and cough up some of his billions, perhaps along with his buddies, to make it happen. Otherwise, goodbye bank. Small depositors, if there are any, will be made whole by the FDIC insurance. (The comments on twitter seem to be pretty strongly against him.)

https://www.bloomberg.com/news/articles/2023-03-10/bill-ackman-says-us-should-mull-svb-bailout-as-possible-option

“Crypto-crash” seems like an obvious candidate.

Great minds! I thought of the exact same term.

I wonder if there are any prognostications on how long it might take some of these things, like startups fully burning their money piles, to run their course? In my ignorance I’m thinking 6 months or so for the bulk of it?

A-a-nd boom! The FDIC team shows up.

https://news.bloomberglaw.com/banking-law/silicon-valley-bank-collapses-enters-fdic-receivership

Didn’t even have time to get a good comment thread going.

Yeah following this on the half time show on CNBC. No mention of crypto for those keeping score. Knock on effects of a bank run when the VC investing community tweets out action items ( that is summarizing one investor’s comment on the situation). Capitalists want their deposits back please, on demand, and no amount of George Baileys are sufficient in today’s world.

This all happened very fast. This might enter the listing of Top 5 financial institution failures, but my memory is dodgy on that aspect. Rising interest rates, declining capital levels, sustained cash burn. CNBC anchor Bosa just laid this out.

My guess is the doors at the branches are padlocked and the systems people from both the state and federal regulators are doing their wizardry in double time.

WaMu in 2008 keeps the 1st place spot (307Bn). The Wikipedians are already on it:

https://en.wikipedia.org/wiki/List_of_largest_U.S._bank_failures

It’s interesting that WaMu and SVB are ~ an order of magnitude larger than the 3rd place ‘winner’ (Continental Illinois, back in 1984)

Detail historical info on failures from FDIC: https://www.fdic.gov/bank/historical/bank/

Scale of Continental Illinois v. SVB…

How much would it close the gap to incorporate the significant difference in margin-requirement level and then the (2.9x, somewhat significant) 1984 v 2023 dollar value?

Naïve q: ¿Might it be germane to compare the size of failure adjusting for resources-beyond-margin?

Is Bust3.0 or Bubble3.0 too close to Web3?

I do quite like the sound of Zirpocalypse.

CryPTEQ Crash ?

Sorry, I’m really stupid at this stuff-dumb question: It looked like SVB had invested in BetterUp(the mental health company). Is it possible anything will happen to BetterUp now, any effects there? Like any ripples from SVB’s troubles? Thank you, and again, sorry for the dumb question.

There are no dumb questions, only dumb answers.

The best question might be, how much of a stake in BetterUp did SVB have? Are there other “investors” in the company who can step in to keep the concern going through the ‘disturbance?’

Good luck.

Ah, I see! Thank you, ambrit! That helps my thought process a bit.

Hi to Phyl for me!

How about “Crypto-nightfall”