Yves here. Normally we don’t watch economic tea leaves too closely and prefer to focus on broader trends. However, as we’ve discussed, the Fed is trying to tackle inflation via its usual method of raising interest rates to increase unemployment. That might have made sense in the 1970s, when labor had a lot of bargaining power and many employers had COLAs (Cost of Living Adjustments) to pay.

But as quite a few analysts have show, our current inflation is not due to too much demand or wage pressure on prices. Instead, it’s caused by different supply issues over time (high energy prices earlier on; continued commodity price pressure and supply chain hiccups due to Russia sanctions; Covid reducing the number who can work full time) and “greedflation,” companies increasing prices not because their costs have risen much but because they can.

Perversely, Wall Street is hoping for signs like this of a worsening economy, since that would mean the Fed would hopefully soon stop tightening and even consider easing, which would buoy asset prices. See Wolf Richter for a long-form treatment in But What If We Don’t Get a Recession in 2023? That Would Be a Bummer for Wall Street.

By New Deal democrat. Originally published at Angry Bear

The important data this week will include new home sales tomorrow, Q1 GDP and initial jobless claims on Thursday, and most importantly of all (imo) real personal income and spending, along with real manufacturing and trade sales on Friday.

In the meantime, today let me take another look at a significant coincident indicator, income tax withholding payments, because the situation has changed in the past week.

Tax withholding payments have for years been employed as a proxy for jobs. Unfortunately, there’s no monthly or quarterly data published on FRED. The best representation is annual data from 1947 to 2020. Below I show the YoY% change in that annual data, adjusted for inflation, compared with the YoY% change (*3 for scale) in monthly nonfarm payrolls:

Because of a quirk in FRED graphing, it appears that jobs lag tax payments, but that’s just a byproduct of comparing monthly vs. annual data. Had I used annual payroll averages, the peaks and troughs would match exactly (but the jobs data would be less fine-grained). The bottom line is that, while the two haven’t matched exactly, especially in the 1980s, typically the increases and decreases move in tandem.

Turning to the present, last week I cited to the California Department of Revenue, showing that tax payments in that State had declined steeply compared with the prior fiscal year during the last four months of 2022, before stabilizing during the first three months of this year.

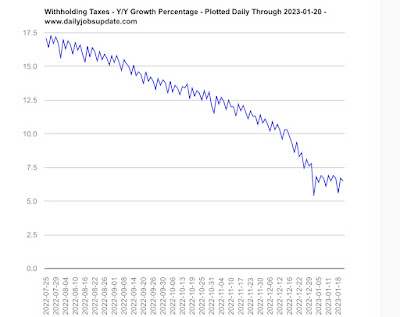

For the nation as a whole Matt Trivisonno has the YoY data, measuring the entire 365 day total of tax withholding vs. the entire previous 365 days, and has a public graph with a 3 month delay. Here’s his latest:

Like the California graph, it shows a steep deceleration during 2022, which had been as high as +21% YoY in March, down to only about +6% by the end of December. Thereafter through January, the YoY data stabilizes.

Indeed, by my own calculations, for the first three months of fiscal 2023 ending December 31, withholding tax payments were only up +1.2% YoY. But for Q2 they rebounded sharply, up +5.4% YoY.

But in the last 10 days they have stumbled. For the first 14 withholding days in April, payments are down -3.4%, $189.7 Billion vs. $196.3 Billion one year ago. For the last 4 weeks as a whole, withholding payments are down -5.0%, $270.2 Billion vs. $284.5 Billion.

What is notable about that, in addition to including the April 18 deadline for payment of taxes this year, is that the CA Department of Revenue had suggested that the late 2022 stumble was due to stock market declines meaning that stock options hadn’t vested.

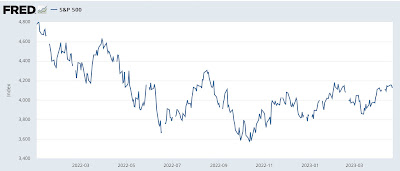

Well, since last October the stock market has rallied, and last week was very close to an 8 month high:

Only a short term shortfall at this point, and of course it could reverse by the end of the month, but if stock options are vesting and withholding payments are still down, even before accounting for inflation, that suggests renewed trouble in the jobs market.

Gotta wonder if the job losses are from AI and not related to interest rates.

AI/ChatGPT-like software (outside of call center stuff) is not that good—–yet.

And (anecdotally….my experience and some others) the official ChatGPT seems to have self-throttled its capabilities over its various updates, seriously—even for paid subscribers.

Interesting. Thanks for posting. One stat I’ve been looking at is Employment Level – Part-Time for Economic Reasons, All Industries (via FRED).

Almost back to its most recent peak of August last year.

One thing worth noting is that CA is particularly tech-heavy and that sector has been hit harder than the broader economy.

The IRS changed the withholding tables this year and all of my payroll clients are seeing slightly larger paychecks from reduced Income Tax withholding. (None of them have stock options.)

This means that quarterly withholding payments will be naturally lower for the FY23 second quarter reported in April than the FY23 first quarter reported in January. In addition, there are holiday hires and year end bonuses to consider that will increase payments for the last calendar quarter of 2022.

Nevertheless, I agree that there is trouble in the job market. Anecdotally, I am still seeing plenty of signs offering jobs. There’s even a very popular sports bar near me that can’t get enough servers and they offer full benefits, including health insurance and retirement, which is rare in the restaurant business.