Yves here. While I don’t view the narrative versus reality approach as novel as this author would have you believe (this is bread and butter for contrarian investors), it is a useful exercise to articulate conventional wisdom, here about bank crises, and sanity test it. Bonus points for the caliber of writing.

By Nicholas Mangee, Research Associate, Program on Knightian Uncertainty Economics (KUE); Associate Professor of Finance, Parker College of Business at Georgia Southern University. Originally published at the Institute for New Economic Thinking website

A new field of economics explores the role of narratives in driving financial markets and the broader economy. Many studies in narrative economics utilize textual news analytics to gauge the importance and spread of various topics and terms reported in the popular press and searched for on the internet. The idea is that stories of human interest, if visceral and viral enough, permeate investor forecasts and distort stock price movements away from intrinsic, or fundamental, values. Consequently, narratives under these accounts are presumed to be behavioral. Put differently, narratives are synonymous with irrationality. Treating story threads as non-fundamental factors, however, fails to recognize the natural and necessary role they play in making sense of uncertainty-laden environments, such as the recent regional banking crisis.

However, not all accounts of narrative dynamics in financial markets presume irrationality. In a recent study published in INET’s book series with Cambridge University Press, How Novelty and Narratives Drive the Stock Market: Black Swans, Animal Spirits and Scapegoats, I advance a fundamentals-based view of market narratives. This hinges on the frequency of non-repetitive events – think corporate bankruptcies, legal issues, political elections, or armed conflicts – and the instability they cause in relationships driving stock returns and volatility. Unforeseeable changes from such events force investors to contextualize information when forecasting earnings and discount rates in ways that reach far beyond hard data and cold calculation. One key finding is that periods with the most unscheduled events and highest narrative intensity align with formal breakpoints in traditional stock return relationships. Consider the regional banking crisis of 2023 as motivation for, what the books dubs, the Novelty-Narrative-Hypothesis (NNH).

Every banking crisis has its own overarching narratives and coincidental streams of various sub-narratives that course through the marketplace day to day. Even the most cursory observer can attest that narratives are inextricably tethered to major news events. From shocks to banks’ balance sheets, to private-sector shake-ups, to regulator responses, each financial calamity is uniquely shaped by events that, while they may be categorically similar, are not perfect replicas of the past. NNH implies that unscheduled events cause market instability and require investors to interpret as best they can the actual process driving outcomes. In doing so, individuals rely on narratives and other non-stochastic tools to make sense of novelty’s meaning for the future. The recent collapse of Silicon Valley Bank, Signature Bank, and First Republic Bank is no exception.

Overarching narratives are mentally sticky and follow news events like a mutating shadow feeding on each twist and turn of new information. Consider the following narratives relating to the regional banking crisis of 2023.

Narrative 1: Lax oversight of regional banks and low rates encourage rapid growth and overleveraging to fund mortgage origination and Treasury acquisition. In the early stages of the 2020 pandemic, as interest rates were slashed to the (near) zero-lower-bound by the Federal Reserve, many regional bank balance sheets grew rapidly. For instance, the total debt of Silicon Valley Bank (SVB) increased 92 and 174 percent from 2020-2021 and 2021-2022, respectively. Commensurate with peer institutions, much of the onboarded debt financed the acquisition of mortgage loans and Treasury securities. The music stopped in 2023.

Narrative 2: Wealthy mortgage holders panic as low-cost lenders’ losses trigger exodus of uninsured deposits – regional bank run leads to collapse. Indeed, banks have held huge balance sheet losses on Treasury securities as rates increased, hurting their ability to cover deposit outflow. Researchers estimate $1.7 trillion dollars in banks’ unrealized losses for 2022. The combination of asset devaluation and deposit outflow crippled the most exposed banks.

Facing catastrophic loan losses and mass deposit outflow, SVB failed on March 10. All eyes then shifted toward First Republic, the beloved bank of the rich and famous. On March 16, First Republic Bank received a private sector lifeline of 30 billion dollars to stem the bleeding. This was not enough. The bank’s stock plummeted 85 percent from March 8 through March 23. Wealthy depositors, once wooed by low-interest mortgages and attractive savings rates, had little reason to stay with the bank considering such a large proportion of their committed funds (above 250,000 dollars) would be uninsured by the FDIC. Over 100 billion dollars in cash outflow was reported in First Republic’s April 24 earnings release. The FDIC took control of First Republic on May 1 in order to broker its sale to JP Morgan Chase, the largest US bank. The FDIC agreed to share in loan losses. The deal protected depositors but wiped out virtually all shareholder wealth.

Narrative 3: The economy is giving highly mixed signals. Unlike previous banking crises, systemic risk is not what this turmoil was about. Contagion was not obvious. In fact, while three regional banks have collapsed this year, other banks have reported strong earnings. Bank of America crushed Q1 estimates. Wells Fargo, Goldman Sachs, Citigroup, JP Morgan, and Morgan Stanley, too, surprised above. Other areas of the economy have painted nuanced pictures as well. The technology sector had sparkling earnings reports, ranging from Google to Microsoft. America’s industry leaders, especially those with high domestic exposure, performed well. Amazon, Pepsico, GE, Raytheon, Mcdonald’s, and Chipotle joined the earnings parade. As of May 5, roughly 79 percent of companies reporting beat Q1 EPS estimates. But simultaneously, private sector layoffs continued: 3M, Accenture, Amazon, Google, Microsoft, Meta, Disney, Dell, Philips, Salesforce, Ericsson, BuzzFeed, Lyft, Whole Foods, LinkedIn, Deloitte, and others, joined the labor cuts in 2023.

Narrative 4: The Federal Reserve is weighing a possible end to months of monetary tightening. The Federal Reserve, too, must interpret available information and contextualize its meaning. The Fed’s conundrum: wage-inflation, home-inflation. There is a deficit of home-sellers who do not want to lose their low-interest mortgages. Consumer prices are falling but remain stubbornly high at 4.9 percent year-over-year for April. Though the FOMC increased rates a quarter percent in their March meeting, Federal Reserve Chair Jerome Powell cited a possible end to hikes. In attempts to pivot the banking crisis narrative, Powell stated on May 3 that the banking system is “sound and resilient.” Try not to hear echoes of Hank Paulson’s speech to the G7 in Tokyo on February 9, 2008. These forms of narratives must reflect fundamental factors since they are based on statements by policy officials.

Narrative 5: Policymakers and the nation’s largest banks are exacerbating the too-big-too-fail problem. With their continued willingness and ability to subsume the balance sheets of failed banks, it is now the size, and thus market power and concentration, of JP Morgan, stacked with over three trillion dollars in assets, that is driving yet another narrative: too-big-to-fail. And although regulations prohibit any bank from holding more than ten percent of total deposit liabilities outstanding system-wide, JP Morgan, as a private-sector buyer of last resort, was allowed to eclipse that ceiling.

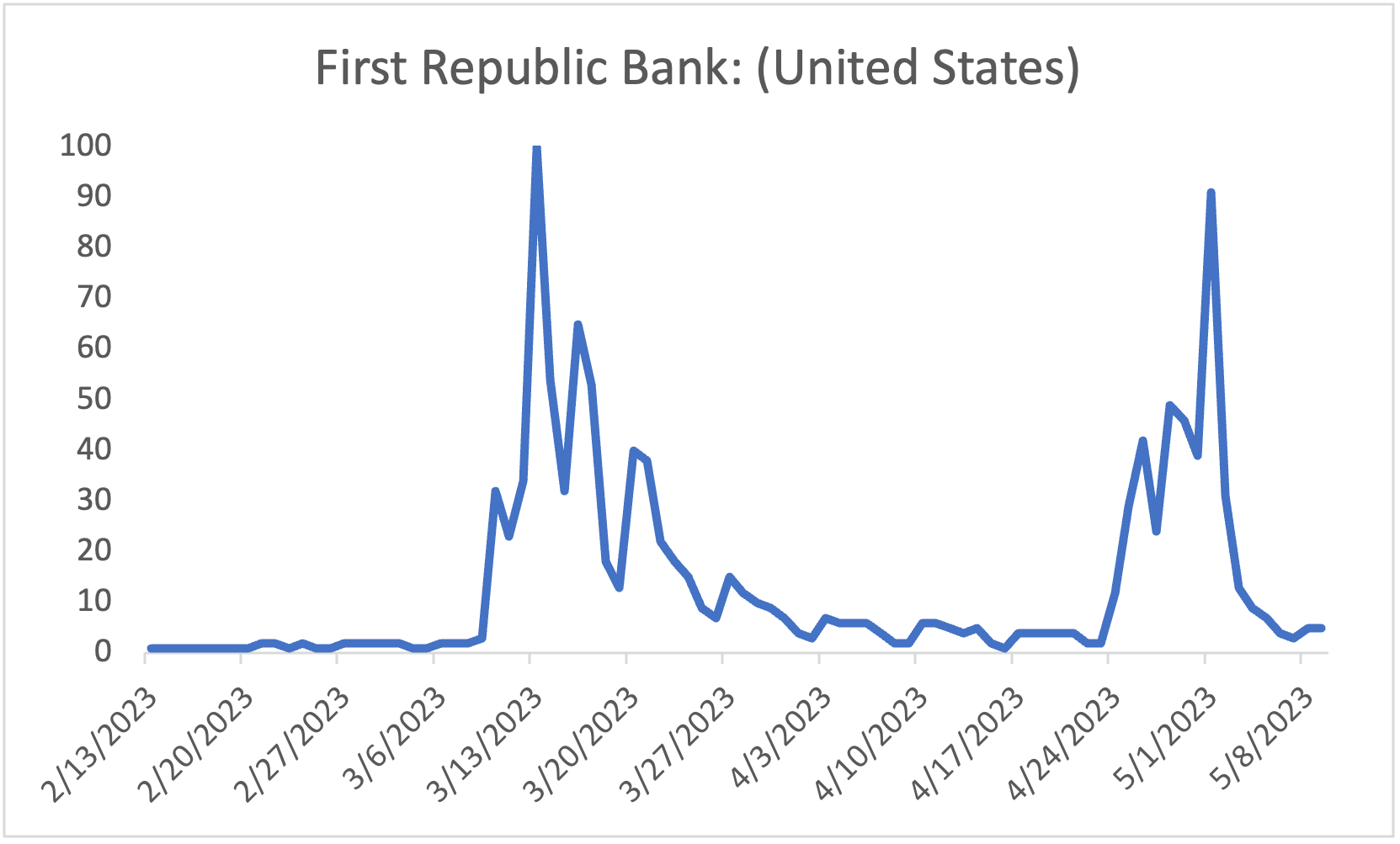

Is there evidence that narratives are involved in news interpretations? Consider the Google Trends internet search interest for “First Republic Bank” plotted below for the 90 days spanning February 13 through May 9 of 2023. Dates with the highest spikes in search interest surround notable events connected to the bank, but also to the regional banking industry. The first spike occurs on March 13, days after the SVB failure. The second spike occurring on May 1 aligns with the FDIC’s takeover of First Republic. In both instances, however, there are asymmetric increases in search interest surrounding the events. When SVB failed, there was more search interest for First Republic following the news. In the second instance, there was greater search interest preceding the news. One interpretation is that narrative dynamics are both part expectational and part interpretation. That is, narratives are rationally present both ex-ante and ex-post as individuals attempt to make sense of novelty, instability, and uncertainty.

Under narrative 4, I get to cynically think about other statements that may not last well. Particularly that the banking system is sound and resilient. I am fairy certain the biggest, gigantic sized banks are in fine shape by all counts. However that leaves many smaller institutions which could be ultimately fine, or not. It’s not just Powell with these profound declarations, Yellen has a few doozies of her own. Below are a few random keepers of premature or as yet finished business, from various realms.

The movie Jaws. “It’s completely safe to go back in the water.”

Bush 43. “Mission Accomplished”

Bernanke. “The subprime crisis is contained.”

Joe Biden*. “America is back …”.

*Pronounced one month after entering office.

#McResistance media: “The Walls Are Closing In!”

It’s always ALL about the narrative.

Everything else is noise.

“”The Fed’s conundrum: wage-inflation, home-inflation. There is a deficit of home-sellers who do not want to lose their low-interest mortgages. Consumer prices are falling but remain stubbornly high at 4.9 percent year-over-year for April.””

Today’s CPI:

“”The shelter index, which jumped 8% annually and 0.6% between April and May, was the largest factor in the monthly increase of core inflation, accounting for over 60% of the total increase. Among the other indexes that rose in May was the index for used cars and trucks, which increased 4.4% for the second straight month, and the index for motor vehicle insurance, which increased 2%, the BLS noted.””

“The technology sector had sparkling earnings reports, ranging from Google to Microsoft. America’s industry leaders, especially those with high domestic exposure, performed well.”

Oh, industry leaders. He must mean ‘monopolies’ and ‘oligopolies’ with absolute pricing power and patent protection. Now there’s a narrative that this fellow apparently missed.

My favorite part of this is his term, “unscheduled events”. If only they had done better scheduling that would fix everything. :-)

The narrative follows profits and big corporations will continue to make obscene amounts of money as long as Americans consume obscene amounts of merchandise. When the shrinking spending class become much smaller than the destitute class corporations will be in trouble.

Definitely not a novel approach, but better late than never for the dismal science I suppose.

Benoit Mandelbrot wrote a book related to this topic nearly 20 years ago now called The (mis)Behavior of Markets. This from the link pretty much sums it up –

“Modern financial theory assumes that prices move randomly in a “normal” range.

But prices are not random, and “normal” does not encompass all price fluctuations.”

The accepted (and wrong) financial theory assumes a normal distribution like you would get when flipping a coin – in other words, an equity has an equal chance of going up or down on any given day. Mandelbrot notes that there are a lot of factors that cause prices to change and if a stock has gone up for example four or five days in a row, it does not follow that the probabality it will go up the next day is another 50% coin flip – it becomes more likely than not to go up again due to the momentum of the past several days, ie the narrative. There are actual people involved in the markets and when Jim Kramer spouts nonsense on the teevee, for better or worse that skews the distribution.

Narrative #6: someone has a startup brewing using Large Language Models to analyze and mediate narratives. Jeez, even I could do this on the side.

https://arxiv.org/abs/2306.06031

https://github.com/AI4Finance-Foundation/FinGPT

Surely – at its root ‘narrative driven behaviour’ is just a new name for ‘herd behaviour’?

Also – is anyone examining the heirachy; that (leaving aside intentional horseplay to mislead the players) ‘reality driven behaviour’ is the antecedent of ‘narrative driven behaviour’? The realists claiming that they have done their own research and if broadcast – for a personal buzz or as an earner – offer their findings to the world.

But always interesting to get AI factored in.

The next squabble amongst the ‘reality driven’ decision makers being which bot to believe; which other bots can be ‘proved’ (whose proof?) to have been programmed to have ‘agenda’s’ ….

Herd behavior

This effect is evident when people do what others are doing instead of using their own information or making independent decisions. The idea of herding has a long history in philosophy and crowd psychology. It is particularly relevant in the domain of finance, where it has been discussed in relation to the collective irrationality of investors, including stock market bubbles …

https://www.behavioraleconomics.com/resources/mini-encyclopedia-of-be/herd-behavior/