Yves here. John Helmer argues that Russia’s lithium reserves not only are considerably larger than those of Australia, depicted at the lithium-richest country in some Western tallies, and with lower production costs than Australia, comparable to those of South American players. That has implications….

By John Helmer, the longest continuously serving foreign correspondent in Russia, and the only western journalist to direct his own bureau independent of single national or commercial ties. Helmer has also been a professor of political science, and an advisor to government heads in Greece, the United States, and Asia. He is the first and only member of a US presidential administration (Jimmy Carter) to establish himself in Russia. Originally published at Dances with Bears

In January of this year the United States Geological Service (USGS) reported the reserves of the nine leading countries in the world which mine lithium, the new fuel to power electric batteries. Chile led, followed by Australia, Argentina, China, and the US which claims to have one million tonnes. Russia was left out of the USGS chart.

Russian sources report its lithium reserves are currently between 3.5 million and 5 million tonnes; that’s at least three times more than the US. The US is also much more limited in its capacity to develop new domestic lithium mines compared to Russia. Bolivia was also omitted from the US Government chart because its reserves were called unproven resources. In fact and in the ground, Bolivia leads the lithium world with 21 million tonnes.

The difference between what USGS reports and what happens next isn’t the distinction in geologists’ terminology between reserves and resources. It’s US Government policy to stop, sabotage and destroy Russia’s ability to meet its lithium requirement from its own, domestic sources, or by importing from friendly countries like Bolivia.

In response, a new plan for combining lithium mining projects in Bolivia and Russia will produce a surplus of Russia’s foreseeable requirement for lithium battery production. But not only that. Allied in technology sharing, investment, trade, and political agreement, the two countries will protect each other in the conservation of the lithium market. If everything goes according to plan, Russia, Bolivia, and the three BRICS states – Argentina, Brazil and China – will dominate the trade in global lithium. They are already discussing the formation of a collective marketing organisation – a lithium OPEC.

Unless the US can stop them.

In the latest official paper issued by the State Department on July 23, “the bilateral relationship between the United States and Bolivia” is “strained. Despite these challenges, the United States maintains a strong and respectful relationship with the Bolivian people, with whom we work to advance human rights, entrepreneurship, and cultural and educational initiatives…However, the United States remains concerned by anti-democratic actions and the politicization of the legal system.”

This is how the lithium war is starting.

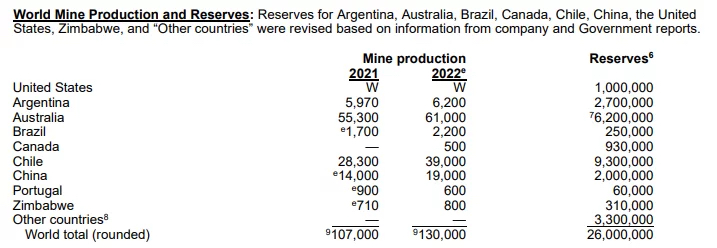

Washington’s version of the world’s lithium table looks like this:

WORLD LITHIUM PRODUCTION AND RESERVES, ACCORDING TO THE US GEOLOGICAL SERVICE

Source: US Geological Survey January 2023

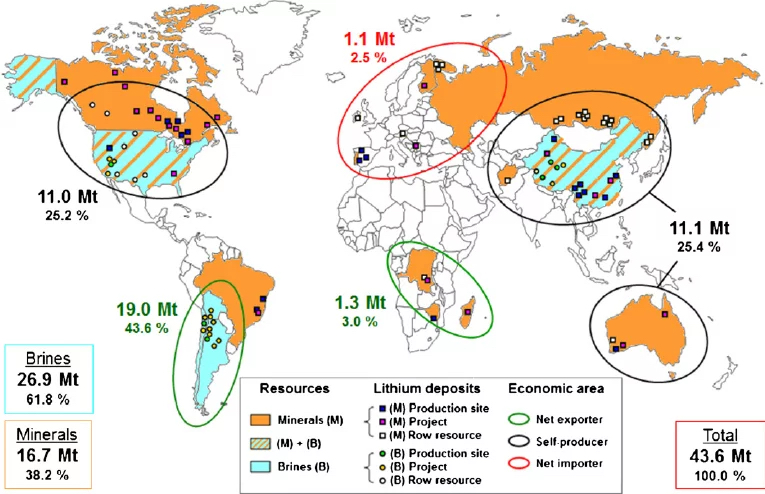

In its footnote to the table, the USGS adds: “identified lithium resources in other countries have been revised to 86 million tons. Identified lithium resources are distributed as follows: Bolivia, 21 million tons; Argentina, 20 million tons; Chile, 11 million tons; Australia, 7.9 million tons; China, 6.8 million tons; Germany, 3.2 million tons; Congo (Kinshasa), 3 million tons; Canada, 2.9 million tons; Mexico, 1.7 million tons; Czechia, 1.3 million tons; Serbia, 1.2 million tons; Russia, 1 million tons; Peru, 880,000 tons; Mali, 840,000 tons; Brazil, 730,000 tons; Zimbabwe, 690,000 tons; Spain, 320,000 tons; Portugal, 270,000 tons; Namibia; 230,000 tons; Ghana, 180,000 tons; Finland, 68,000 tons; Austria, 60,000 tons; and Kazakhstan, 50,000 tons.”

The US is the only country in the table to try to keep secret its production of lithium. “W” in the table, according to the USGS, stands for “withheld to avoid disclosing company proprietary data. — Zero.” In fact, there are at least three publicly listed US lithium miners, and they are required by law to report their lithium results several times each year.

Albemarle Corporation, for example, sells its shares on the New York Stock Exchange on release of quarterly production and financial reports from the company’s lithium projects in the US (Silver Peak, Nevada, and Kings Mountain, North Carolina), and in Australia, Chile, and China. For example, in 2022 the company reports it produced 34,000 tons of lithium carbonate equivalent (LCE); but just 2,000 tons of this aggregate were mined in the US. Because US lithium consumption is so heavily dependent on foreign imports, Albemarle has just announced Pentagon funding for mining equipment to reopen the mothballed Kings Mountain mine in North Carolina. This follows a US Energy Department grant of a year ago to construct a lithium concentration plant at the mine. Altogether, US Government funding to revive Kings Mountain currently exceeds a quarter of a billion dollars.

According to Vygon Consulting, a Moscow analytical company specializing in rare metals, Russia’s reserves are far greater, exceeding Australia, the US, and China on the USGS table, with a cost of production for ore deposits that is lower than the Australian and North American mines, and a brine extraction cost comparable to the South Americans. By 2040, Vygon is projecting annual Russian production of 600,000 tonnes of lithium – a volume which will turn into exports to the global demand market of roughly half the deficit between supply and demand estimated by then.

This means that for Russia, the strategic defence and security requirement for lithium can be met quickly so that import dependence can be ended by 2025. On the other hand, for the longer term in economic war planning against the US and Australia, there is domestic competition for state support of new projects between the established state combines like Rosatom, Gazprom, and Rosneft; the established oligarch miners like Norilsk Nickel and Alrosa; new commercial enterprises; and between regions from Dagestan in the west to Murmansk in the north and Irkutsk and Yakutia in the east.

Confidence in defeating the Americans is an open secret in Moscow; who will benefit domestically between the state companies and the oligarchs is a closed secret because it has yet to be decided.

There has been no lithium mining in Russia since 1997 when mining at the Zavitinsky deposit in Krasnoyarsk stopped. The reason is that there has been no demand at a price for the metal to make mining of proven reserves and develop fresh resources profitable enough. Imports were cheap and supply reliable until 2022. Chile and Argentina then stopped exporting to Russia; several African states halted exports of the raw mineral and required processing plants to be established instead.

Lithium is a rare metal, not because it is scarce but because it is widely distributed at low concentrations in various mineral compounds and salts in the earth’s crust, in seawater, and in oil and gas fields. Because Russia dominates the world in the last of these, its potential capacity for extracting lithium is considerable. Russia’s oil and gas producers have worked this out. So has the US Government.

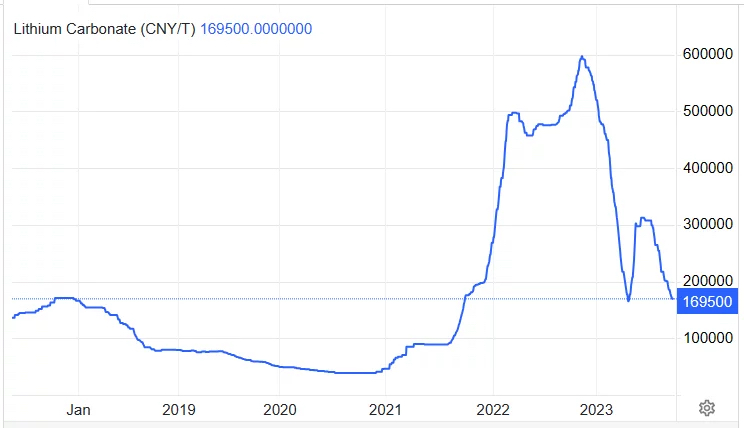

Low concentration usually means high cost of production. The abrupt surge in price to peak at about $90,000 per tonne in 2022 reflected the dramatic change in international supply, demand and mine profitability calculations. Although the latest investment bank forecasts and stock market projections indicate the price in global trade will continue to decline, the cost of production will remain at a level at which new investment in lithium source extraction will be profitable.

The sanctions war against Russia, both to cut off imports and stop exports, leaves no choice for Russia but to restart domestic lithium deposits; create new ones; protect the security and stability of supply from traditional import sources in South America; and develop new methods for trade and price control to defeat US sanctions.

TRAJECTORY OF THE LITHIUM PRICE, 2018-2023

Source: https://tradingeconomics.com/commodity/lithium

Converting the Chinese yuan (CNY) price to US dollars, the current value is $23,730. For more analysis of how the lithium market will develop over the next five years, and the impact on nickel and cobalt, in which Russia is already the dominant global supplier, click on this Goldman Sachs forecast for a steady downward trend in the price of lithium and nickel.

In Russian metallurgy, lithium is used to deoxidize and increase the ductility and strength of alloys. In optics it is used to make glasses to protect against ultraviolet rays. In addition, lithium is used in nuclear power engineering to obtain a radioactive isotope of hydrogen, tritium. There are many military industrial applications. By far the biggest civil application for lithium is in the production of lithium-ion batteries for use in electric vehicles and solar panels.

Until last year Russia imported about 9,000 tonnes of lithium (lithium carbonate equivalent, LCE) per annum from Chile, Argentina and Bolivia. Together, their salt flats from which lithium is extracted are known as the lithium triangle.

Note that Bolivia is landlocked and the lowest-cost transportation route for the raw mineral is by rail westward to the Chilean north coast. The Bolivian government is also planning to process lithium and produce lithium batteries in-country with Chinese investment. Source: https://ubique.americangeo.org/

According to Vygon Consulting of Moscow, about 24% of the world's lithium resources are concentrated in Bolivia, Argentina comes second with 23%, and Chile third with 13%. In the triangle with current extraction technology, cost of lithium production is optimum for western mining company profit calculations. However, Chinese companies are planning to invest in low-cost extraction in Zimbabwe; domestic Russian extraction costs at the oil and gasfields will also be comparatively low.

By 2025 the state nuclear energy conglomerate Rosatom is planning to start extraction and processing of lithium from brines in the crater lake of Pastos Grandesin southwestern Bolivia; by 2027 output will reach planned volume of 27,000 tonnes at an estimated production cost of $4,000 per tonne. The investment outlay for Rosatom, through its Uranium One subsidiary, will be $600 million.

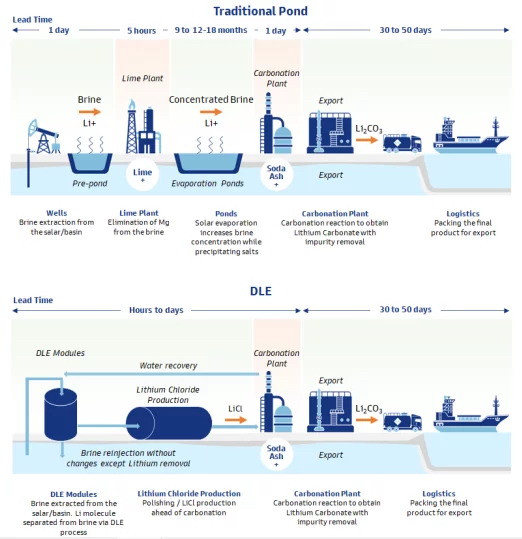

The Russian technology to be used will be a variant of what is known in the west as sorption or direct lithium extraction (DLE).

HOW EXTRACTION OF LITHIUM WORKS

Source: https://www.goldmansachs.com/

Rosatom needs the lithium to produce automobile batteries at a plant being built now in Kaliningrad. This factory will start rolling out 50,000 electric vehicles per year by the end of 2025. Russian sources estimate the plant will consume about 360 tonnes of LCE annually. In planning for this project “an important factor is that the leftwing Bolivian government looks like a more reliable partner in the circumstances, so the choice of Bolivia to launch a lithium mining project seems logical,” says Igor Chausov, an analyst with the Center for Power-Engineering Systems of the Future, Energinet. “Lithium delivery will be carried out, apparently, first by rail through Chile, then by sea.”

An alternative to salt flat brine extraction is hard rock mining. This not only means reviving mothballed mines like Kings Mountain in North Carolina and Zavatinsky in Krasnoyarsk. It also means opening new hardrock deposits like Kolmozerskoye in the Murmansk region. Russian sources currently believe this holds the largest volume of undeveloped reserves in the country; it has been under consideration for several years, but the lithium price takeoff and the war have accelerated planning. A partnership has been announced between Rosatom and Norilsk Nickel, owned by Vladimir Potanin, to accelerate the project.

According to Vasily Danilov, an analyst at Veles Capital, the target date for first output has been 2030. “Given the significant financial and expert resources of Norilsk Nickel, the start of commercial lithium production may begin earlier.” Click to read the Rosatom summary of February 2023.

In Dagestan, the local government is lobbying for federal budget support to start mining of three large lithium deposits and the construction of processing facilities. According to Alibek Alkhasov, director of the Institute of Geothermal and Renewable Energy Problems, a branch of the Joint Institute of High Temperatures of the Russian Academy of Sciences, the Institute has studied 92 deposits with industrial lithium content in the North Caucasus over the past 40 years, 55 of which are located in Dagestan. “The Berikeyskoye, Yuzhno-Sukhokumskoye and Tarumovskoye deposits make it possible not only to fully meet Russia’s needs for lithium carbonate, but also to export it to other countries,” Alkhasov has said.

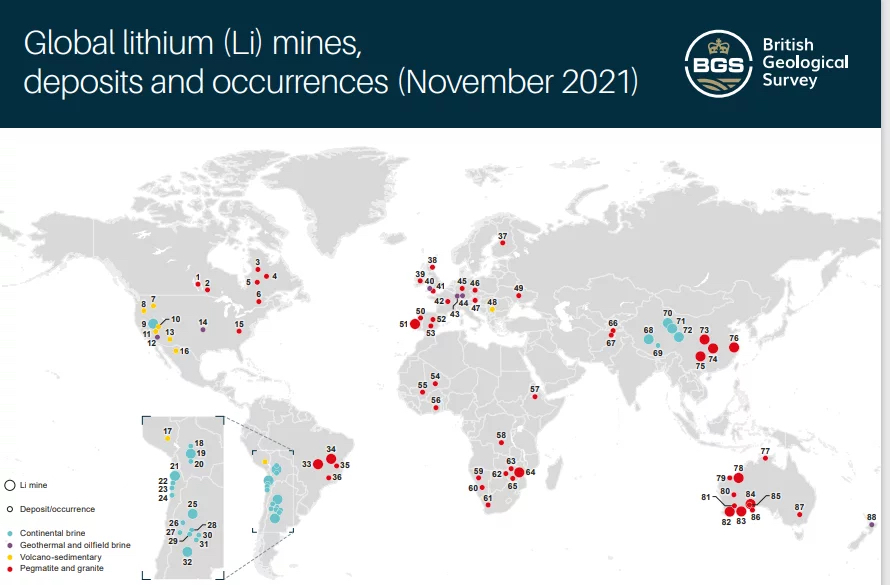

A current and comprehensive map of Russian lithium deposits is not available. The British Geological Survey map for the world omitted Russia entirely. A much earlier global review of 2012 identified the Kolmozerskoye hardrock deposit in Murmansk and brine deposits in southeastern Siberia.

Click on source to enlarge detail and read the key to each identified deposit.

Source: https://www.researchgate.net

The federal Ministry of Industry and Trade has announced its support for the revival of the Zavitinsky deposit in Krasnoyarsk, but this will be limited to recovery of lithium from the old mine’s waste dumps. Production will materialise quite quickly.

Also relatively swift will be the extraction of lithium from brines in Gazprom’s Kovykta gasfields in Irkutsk. Since 2021 Gazprom has been working on a single experimental well; Moscow sources say production there will start in 2025, possibly sooner. Other oil and gasfield sources currently being prospected for lithium projects include the Lena-Tunguska area in the Ural-Volga region and in the North Caucasus. Rosneft, Gazpromneft, LUKOIL and Tatneft are the established producing companies there.

Also bidding for state budget and financing from Gazprom and Rosneft are other regions of eastern Siberia, both for brine extraction and for concentration plants. Soviet geologists identified prospective sources of lithium a generation ago, but the international lithium price, cost of production, and commercial profitability calculations stopped development until now, regional experts say. The US war against both Russia and China, as well as regime change plotting against Bolivia, have transformed the strategic thinking across Russia, and opened for the first time the possibility (and profitability) of Russia as a major lithium exporter to defeat the hostile state alliance.

It is currently estimated that by 2030 that the hardrock sources of lithium in Russia will be producing 68,000 tonnes of LCE annually, roughly three times more than the estimated domestic demand requirement. The output capacity of the brine extraction sources is much greater – by 2030, 56,000 tonnes per annum; by 2035, 206,000 tonnes.

According to a commentary published in Vzglyad last week, “the growth of the share of electric vehicles, the emergence of electric airplanes and electric-powered ships will change transport around the world. And if today Russia’s international influence is partly based on its role in OPEC+ as one of the leading oil exporters, then in the future we can think about a comparable role in the economy of tomorrow – the economy ‘with lithium blood’… In these conditions, the winners will be those in whose hands the most effective technologies will be. Effective both from the point of view of direct costs and from the point of view of the environment, which minimizes indirect costs allocated for environmental protection measures.”

“Russian companies have unique advantages which can be implemented in the production of lithium. If we talk about the distant future, it is worth paying attention to the recent statement of several Latin American countries about the desire to create a lithium OPEC to reduce market volatility. An example of the classic OPEC+ is in front of their eyes. At some point, this will move on to practical plane. Steps are being taken now so that in time Russia can enter this new international cartel as one of the leading countries.”

NOTE: Because of the war conditions, no Russian source agreed to respond directly to questions.

Recent news claimed a 3 million ton Lithium reserve found in Nevada. Do you think this news is just part of a propaganda war?

You’re talking about the Thacker Pass area and the McDermitt caldera, where a rabid pack of lithium (and uranium) miners and speculators have descended. I suspect what is going on is Lithium Americas is trying to bump up its stock prices AND set the stage for going back on its past statements that it would NOT mine up in the Montana Mountains above Thacker Pass. The Montana Mountains are a Sage-grouse stronghold. The cultural values that have caused huge tribal resistance over lithium mining at Thacker Pass extend across the caldera landscape. Many of the news stories reporting on the recent paper and the “big find” did not say that its lead author was a Lithium Americas executive. This article provides some perspective on part of what is going on. https://www.nevadacurrent.com/2023/09/22/report-of-giant-lithium-find-underscores-need-for-less-sloppy-permitting-conservationist-says/ . The huge flurry of news stores, some of which appeared planted, seem aimed also at breaking environmentalist and tribal resistance. That won’t work at this point, because so many eyes are now on the innumerable biological, cultural and other values of the caldera .

“Environmentalist and tribal resistance” is one major reason “the US is also much more limited in its capacity to develop new domestic lithium mines compared to Russia.”

A number of states (led by California) have passed laws requiring that all new vehicles being sold be 100% electric by 2035, and this will require vastly more lithium that the US currently produces. If we don’t mine more from Thacker Pass, from where shall we get it? Are we just going to import it all? [Note that importing lithium effectively asks other countries to tear up their own environments so that we can keep our own environment pristine.]

Perhaps we learn to make do with less? Maybe more public transportation and fewer cars? I know, I know, that’s crazy talk…

Lithium is only the current way to power EVs. Sodium and other batteries will give lithium a major challenge because they are cheaper. VW counterpart, JAC, has introduced the first EV running on a sodium battery. It is first generation, so the specs aren’t great:

https://jacmotors.co.za/jac-motors-unveils-worlds-first-sodium-ion-battery-vehicle/

https://www.youtube.com/watch?v=UVplZS6Gqwc

#TYVM

even if one hand-waves all the environment litigation and self-boasting by people trying to raise capital, the US still needs the processing infrastructure to make lithium carbonate and other lithium compounds.

There is essentially zero processing infrastructure in the US and a whole other set of environmental litigation that will start when someone announces a lithium carbonate plant in small town X.

If you think fracking is bad, wait until lithium comes to town.

You always have to be very careful about reports like that, as there is a lot of money to be made by hyping up discoveries. There are many factors involved in making any mineral reserve viable – most obviously transport infrastructure – so all reports (including the ones on Russia’s reserves) should be taken with a large pinch of salt. Just as an example – the maps above indicate a large orebody in Ireland – and indeed there is a very large and well studied one south of Dublin. But for all sorts of reasons, its highly unlikely to be mined.

The big thing nobody is mentioning though (although the industry is well aware of it), is that we’ve just seen the first effective sodium-ion batteries come on the market – they have the potential to completely undercut projected demand for lithium