Yves here. Thomas Neuburger delves into the question of what happens to seemingly ever-levitating US real estate prices when they run into the problem of non-existent or very costly insurance.

By Thomas Neuburger. Originally published at God’s Spies

The Woolsey fire burns a home near Malibu Lake in Malibu, Calif., Friday, Nov. 9, 2018. AP Photo/Ringo H.W. Chiu

If the contrived flow of water should somehow just stop, California’s economy, which was worth about a trillion dollars as the new millennium dawned, would implode like a neutron star.

—Marc Reisner, A Dangerous Place, quoted here

Insurance, the Stuff of Life

Much of first-world life and its stability revolve around insurance.

We already know the hell the under–health-insured go through. That crisis is on us now, has been for a while, and no one with power, at least in the U.S., dares to address it.

The donor class, especially the health care queens and kings, would put out the eyes of anyone with power who did, and send them to live in the wilderness — Kentucky, perhaps. Or Maine. (By those with power I don’t mean Bernie Sanders. He’s not a decider. I mean Joe Biden and those who hold the real reins in our houses of Congress.)

But more than our health depends upon good insurance. Our homes as well — the shelter that keeps us from living in forests and longhouses and tipis; that which keeps most of us urban, in other words — depends on the ability to insure against destruction.

So imagine if you lived in a state in which home and property insurance was unavailable. What would you do? Most, I think, would move to another state. The rest would shelter in place, go uninsured.

Is that outcome likely? Let’s take a look.

The Day of the Uninsured

The day when whole states will go uninsured is approaching. Many pick California for its many wildfires as an early candidate, and for very good reason.

A structure and a motorcycle burn at an RV park during the Woolsey Fire in Malibu, California, November 10, 2018. Kyle Grillot /The Washington Post/Getty Images

But California is big and varied, and several disasters would have to accumulate there — water shortages; massive fires, especially where rich people live, like Malibu Canyon; earthquakes; collapse of the water table; and more — before the state became uninhabitable. It will, but maybe not soon.

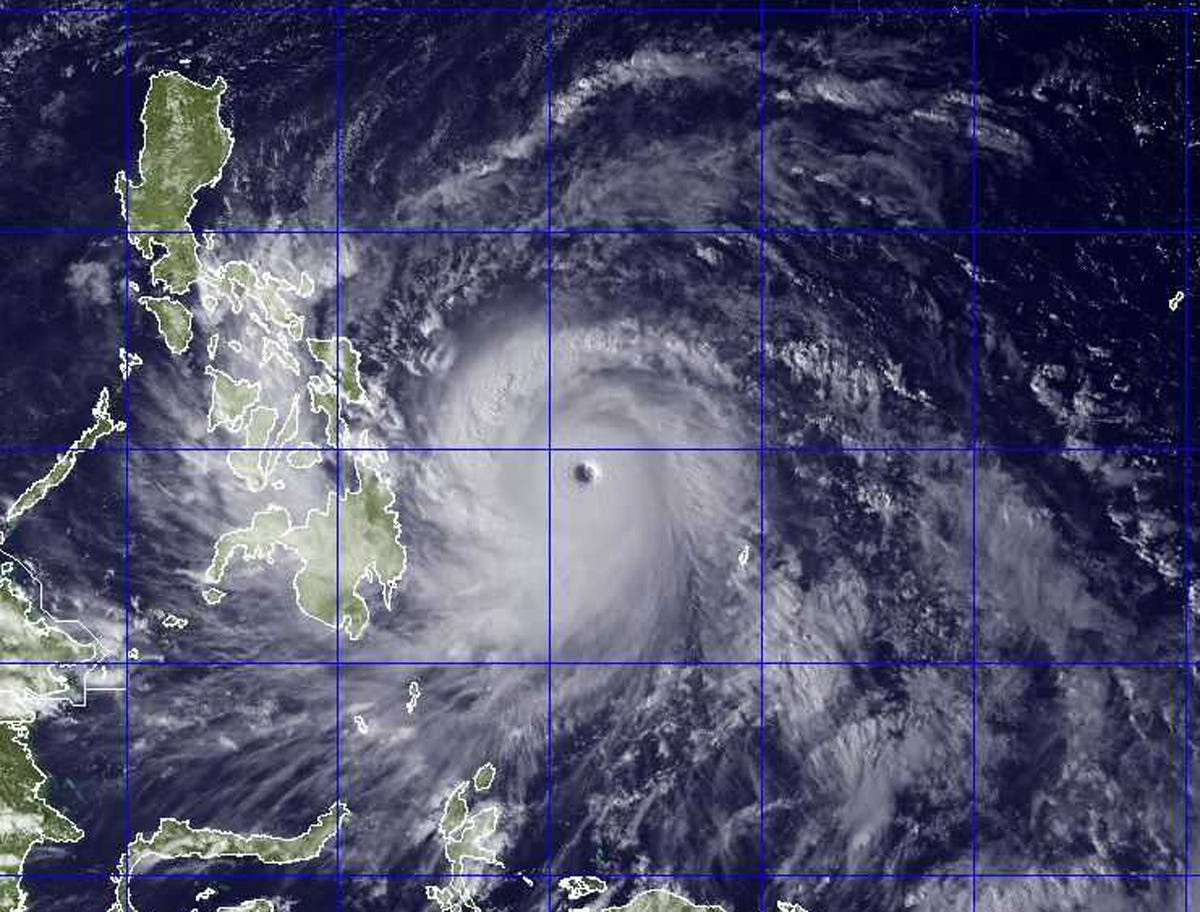

Florida is a different story. There a Typhoon Haiyan–type event could make coastal and inland real estate disappear, leaving the rest uninsurable, all in a day.

Image provided by the US Naval Research Lab. Government forecasters said Thursday that Typhoon Haiyan was packing sustained winds of 225 kilometers (140 miles) per hour and ferocious gusts of 260 kph (162 mph) and could pick up strength before it slams into the eastern Philippine province of Eastern Samar on Friday. AP PHOTO/US NAVAL RESEARCH LAB

That day could be tomorrow, or any day you like. Atlantic hurricane season is June though November, but hurricanes occur outside of that window as well.

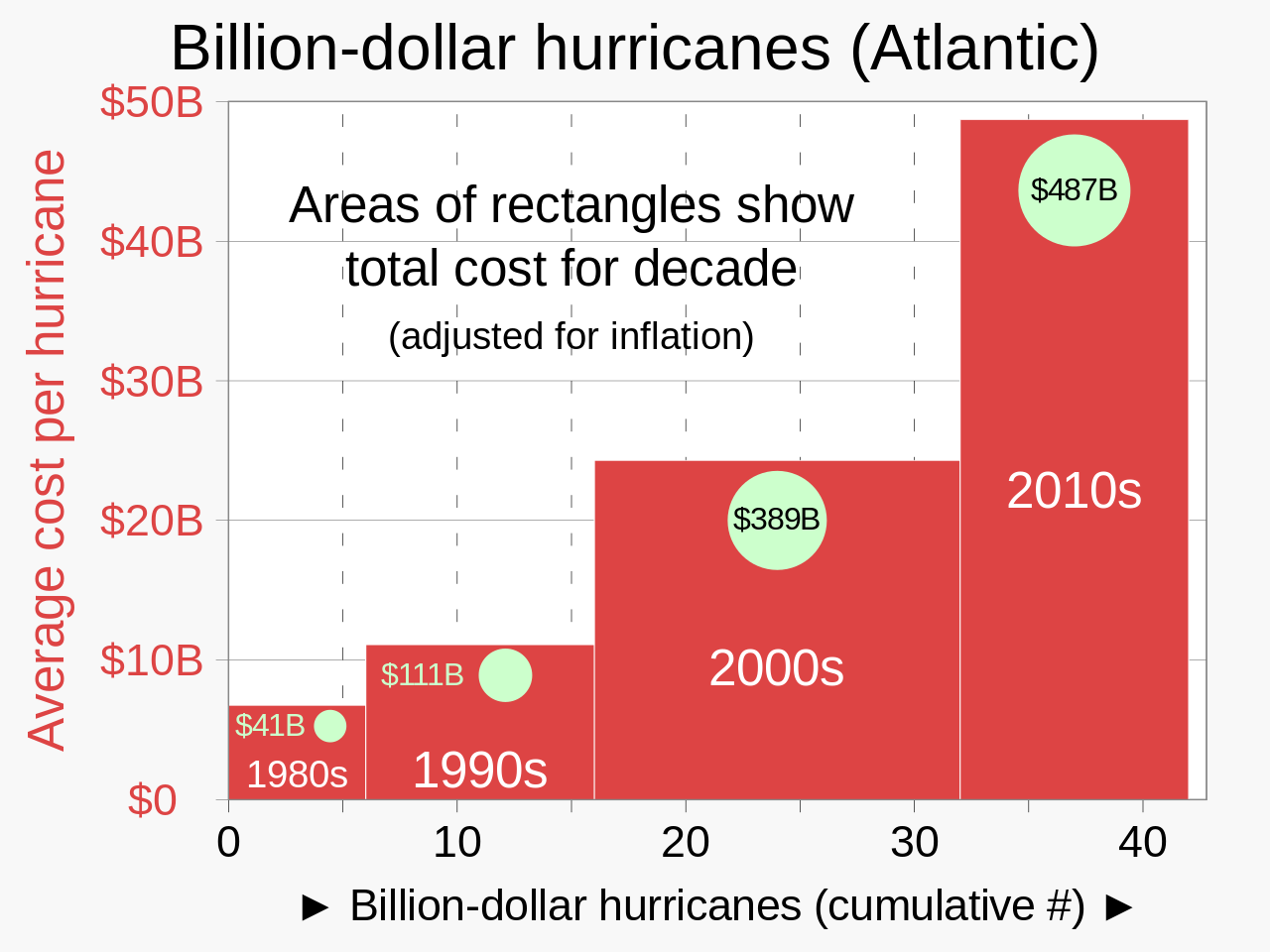

Not only does the chance of a major hurricane increase by the year, but the costs are increasing as well.

The number of $1 billion Atlantic hurricanes almost doubled from the 1980s to the 2010s, and inflation-adjusted costs have increased more than elevenfold. The increases have been attributed to climate change and to greater numbers of people moving to coastal areas. Source: Wikipedia

But you knew that, right? You knew that global warming is accelerating, and the odds of avoiding frequent and large-scale disasters grows slim by the year.

Insurance Costs Are Already Increasing

The cost of insuring a home or business location — indeed, a livelihood — grows naturally greater as the likelihood of disaster increases, until at some point insurance just disappears.

So, how safe are we who live in the dangerous states? Bloomberg Green took a look at the state of insurance by state:

US Home Insurance Premiums May Hit a Record This Year, Report Warns

The average premium for US homeowners insurance is expected to hit $2,522 this year, up 6% from the end of 2023. Premiums in Florida will approach $12,000.

Not a good headline. The article goes on (my emphasis):

In the 1980s, the country experienced about three disasters a year that caused damages of at least $1 billion each. In the 2010s, that climbed to 13 per year, according to the National Oceanic and Atmospheric Administration. Last year, the US endured a record 28 weather and climate disasters that caused at least $1 billion in damages each.

Responding to climate-induced threats, a growing number of insurance companies are pulling out of California and Florida, where those impacts are frequently felt. To fill the gap, state “insurers of last resort” are absorbing trillions of dollars in risk.

“It’s possible that the highest-risk areas will become uninsurable,” says Betsy Stella, vice president of carrier management and operations at Insurify.

About California, as the article notes, the exodus has already started:

State Farm General Insurance Co. will cut about 72,000 policies in California beginning in July, the latest move by the state’s biggest insurer to cope with growing risks from wildfires and other natural disasters.

The move comes just nine months after State Farm announced plans to stop issuing new coverage in the most populous US state. …

State Farm cited the company’s financial health as the reason for the cuts. Expect other insurers in other states to reach the same conclusion as disasters accumulate.

About Florida, Bloomberg states: “Homeowners in Florida, who already pay the highest rates of home insurance in the country, are expected to see another 7% increase this year — bringing the state average to $11,759, more than four times the national average.”

Anecdotally, one Florida resident I know said her homeowner’s insurance went from $3,000 to $14,000 in just six years. Where this will end should be obvious.

Not Just Florida

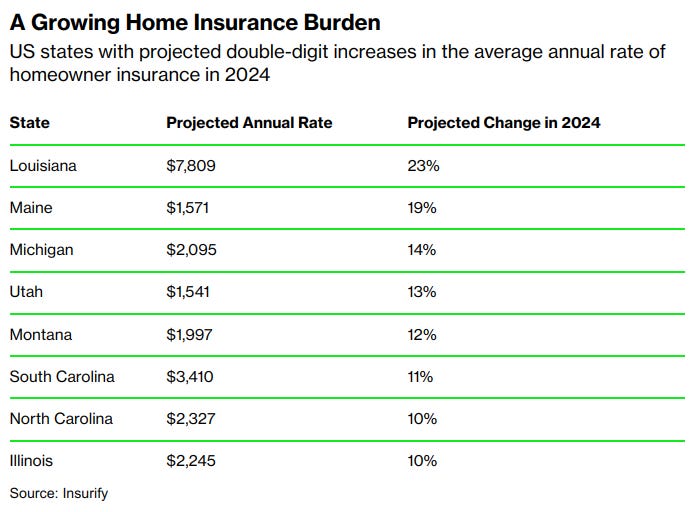

Seven states, none of them Florida, will see double-digit homeowner insurance rate increases.

Says Bloomberg:

For states with rising premiums, Insurify’s researchers largely point the finger at the increase in natural catastrophes. According to AccuWeather, the US can expect an “explosive” hurricane season this year, with the potential for as many as 25 named storms between June and November, compared with about 14 on average. Meanwhile, sea-level rise and other adverse climate impacts are catching up with historically low-risk states like Maine.

Something else to anticipate.

Time to Consider a Change?

The good news is this: the worst hasn’t happened yet, even in states where bad things tend to occur. There’s time to leave before everyone leaves before you, and you’re left selling to no one who wants to buy.

The bad news is obvious: for many, a world without insurance is in the cards. The numbers vary, but according to NOAA, about 40% of Americans live in coastal counties.

NOAA estimates that if U.S. coastal counties were their own country, they’d be third in world GDP. All of which will be lost, sooner or later, to sudden disaster or eventually, sea level rise. You can count on insurance companies to pull out of those areas ahead of those liabilities having occurred.

A world without insurance. Time to plan now?

Crikey. We see it here in Australia already.

Our house insurance (mandated by the bank to insure their mortgaged property, obviously) is now $48 a week. That’s only $AU but that is what we use here and it equates to the average US figure in the article.

We had massive bushfires here in 2019/20. All insurance has skyrocketed since then.

Michael Hudson’s thought on the FIRE sector rents are a real thing with us. But, in an area like this or a lot of other places in NSW to go without insurance seems suicidally risky.

Many homes in the North of the state have been flooded three times in two years. They are uninsurable now.

A big problem indeed.

Yep. Up in Townsville, after the last cyclone our house insurance went to $5,000 / year. Down in Brisbane after the 2022 floods, house insurance was $4,000 / yr. We just don’t insure anymore. Our plan is ‘stay off the low ground and pray’.

Even if your attemps to to find the least impacted personal living site are successful, the community-at-large (you) will be affected by these disasters.

In a coastal community the sewage treatment plants are mostly along the coast and will be inoperative with sea level rise. An expensive home up in the hills will still see extreme value loss without dependable sanitary services.

Exactly juno mas. And yet our (Aus) Local and State Governments seem tunnel-vision focused on hyper-accelerating tourism and fleecing those older folk leaving the cities to “live the good life” in new coastal developments. Not that the Insurance lobby would have much clout at State and indeed Federal Gov’t levels, mind you. Cough cough.

I can see California the state stepping in as “insurance provider” of last resort, ostensibly to lower the cost of insurance, but instead the funds will be redirected to that big hole at the center of California’s finances. But no worries, one big earthquake, and the Federal government will bail California out.

Speaking of earthquakes… aren’t you in Taiwan?

I am indeed in Taiwan. The earthquake was very scary and even until now I can still feel the aftershocks affecting the building where I live :( Given the magnitude of the earthquake though, I feel Taiwan has done very well. It’s very sad that some people lost their lives in the incident, but I think had this happened in the US, you can expect a much higher number of casualties.

It’s prohibitively expensive to purchase insurance that covers earthquakes in California already. Almost no one buys it. The “insurance” is that mortgages in the state are no-recourse, meaning that after the earthquake, a whole bunch of people will default on their mortgages and leave the lenders with the rubble.

Even in Recourse states, the debt is still dischargeable in bankruptcy which means the lenders (or the Federal Government) will ultimately be holding the bag

California’s state (fire) insurance is roughly double the private sector’s cost. Still…there’s often no alternative if the conventional insurers cancel.

Insurers are the most financially capable of lobbying for significant climate policies, but a focus on short-term profits hamstrings an otherwise potent opponent of carbon emissions.

Yes. California FAIR plan is basically natural disaster insurance only, but excludes flood and earthquake for which you need separate policies. It doesn’t cover liability at all. And as noted above, it is more expensive.

One can ask how effective insurance companies could ever be in lobbying for limiting carbon emissions.

Too many lifestyles would have to be changed, less driving, smaller homes, lower consumption, less development.

If state/local and federal governments are reluctant to force change, having one industry lobbying to limit climate changing emissions while other industries (real estate, tourism, petrochemical) lobbying against any changes seems a poor use of insurance company influence..

In a sense, insurance companies, via increased premiums are making a “lobbying” statement.

Having insurance companies spending money to lobby for climate policies could result in no changes and higher premiums to cover the lobbying costs.

California Earthquake Authority has offered insurance for quite a while, haven’t ever bought it. Florida Hurricane Catastrophe Fund is another state-controlled insurance program. Here in HI there was a major problem after Iniki, resulting state creating Hawaii Hurricane Relief Fund. After things settled down, the legislature raided it to pay for other things. Rates are up this year; told due to re-insurance costs from Lahaina and 25 other major events nation-wide last year.

Re ‘A structure and a motorcycle burn at an RV park during the Woolsey Fire in Malibu, California’

I think that you will find that that is the Ghost Rider’s bike just parked there. Regardless. In looking over this situation it is obvious that there will be areas that will become uninsurable. That being the case, it is likely that the best way to do it is by looking at the facts for each county for fires, floods, tornadoes, etc. Yes, there are some 3,000 counties plus but there would be little sense denying flood insurance to several counties in a region only to include the one county in the middle that is on a high elevation. Real estate prices will go up in counties where you can still get insurance and would drop in places where there is none. So wealthier people will buy up the former which will leaves the later to poorer people because markets.

Now I am going to get even more cynical here. You will find that there will be a problem with wealthy people who insist on having their homes in risky locations like here-

https://www.latimes.com/california/story/2024-02-14/multimillion-homes-teetering-on-edge-of-cliff-overlooking-ocean-following-heavy-rain

And let us not forget The Hamptons with it’s very low elevation to the sea making it undefendable for future flooding. They will demand that they be insured and everybody knows that wealthy people have their lawyers at number one on their speed dial. So what I am saying is that insurance corporations may deny insurance to any number of counties and use the savings of the payouts to make sure that those wealthy people still have their insurance for their own properties, no matter how risky they are.

Loved that nod to “Ghost Rider”!

Your comment about flooding reminded me of all the paper shuffling back and forth across the table when we purchased our current property 20 years ago. The lawyer when sliding one particular sheet over to us commented:” this is probably the most important one, it says you are not in any floodplains according to surveys and the maps.”

I chuckled then but who knew this many years later after what has happened in recent years in Vermont.

I would guess that as the climate shifts, that a lot of those info sheets will have to be updated. Ideally, you should be able to go to the website of a County, look through the menus until you find one for historical flood maps & topographical surveys, and then check them out as they are superimposed over a modern map. Can’t see my own Council here in Oz ever doing that as too many interests want to see those maps buried.

Well the lower pasture below is floodplain and about 60 feet lower than my house site. All I can say is if my house gets flooded, God help everyone and everything in existence for the next 180/200 miles south to where the Connecticut Rivers dumps into the ocean.

But, there’s always a first for everything in this world of change.

And as you say there are certainly flood maps being redrawn all over the place.

In most counties in California you can go on country GIS systems and do exactly that plus many other things that reference data geospatially.

One of the few ways our local tax dollars actually benefit the citizenry.

Had a co-worker whose house in VT was “not in a flood plain.” Don’t remember which storm it was in the early 2000’s but the water in the brook across the street from her house rose 48 feet and flooded her house. The insurance company would not pay the claim, and she could not afford to make the repairs. I think she was able to take advantage of a FEMA buyout, otherwise she would have had to just walk away from it.

Sorry to read that about your friend. It’s been horrible what has happened to so many the last few years. . And in a State like ours which already has limited housing stock it’s tough to find new shelter.

Another interesting thing about many flood maps is some also have marked for “100 year floods”, etc.

yet many are arguing we now have a 100 year floods 3 years in a row in some areas. I don’t know how all that is resolved on maps going forward other than maybe what was 100 year floods should get promoted to possibly annual occurrences, which would be a monumental change.

The problem is worse than this implies. We are increasing risk concentration in the most CAT prone areas and rising property values are a double edged sword.

Curiously, many of these states are epicenters for deregulation. Imagine what would happen if they allowed insurance rates to be set where insurers actually need them to be.

And, this same ideology (religion) says don’t subsidize and bail people out. Well, it is a question of when, not if, a major storm hits a high density coastline and we have a +$100bn insured event. Who pays then?

I recall reading that insurance has been a pretty profitable racket. Also that with a potent lobby, insurers can tune their risks and profits by doing stuff like creating small risk pools by incorporating many places out of nationwide operations, then walking out of the “losing” business areas.

Seems to me this is fundamentally about whether there is an “us” in the political economy, or if it will be thieves, winners and losers all the way down.

My county has written a “resiliency plan” that does not seem to have much planning on how to elevate the sea level sewage, water and power utilities. My home is in an evacuation and inundation zone, at 18 feet above high water. I’m 78 years old and hope to die of age before the SHTF. I uncharitably hope that the looters who have gotten filthy rich off building the vulnerabilities that now threaten us mopes get zapped first. But I’m realist enough to expect that the psychonarcissists will of course emerge from the cesspit of catastrophe smelling like roses.

Is there an “us” in the US? Or anywhere else? Lacking that, what hope is there for this bunch of naked apes?

And I have this feeling that maybe when it comes to social support, there are models for healthier economic activity, like in Islamic ideals of banking and finance. https://www.investopedia.com/articles/07/islamic_investing.asp

You would think with premiums like 12,000 a year that …. you could build a totally hardened home with on site supplies and energy systems.

I have always wanted to build a real stanchion of a home with wave and hurricane resistance down on Hatteras – Invite the news media in for on coast coverage of a hurricane

Like this?

https://web.archive.org/web/20170912034534/http://www.townandcountrymag.com/leisure/travel-guide/a12223036/ernest-hemingway-house-cats-hurricane-irma/

Loved that link! I volunteer to move to Key West and live in that house and take care of those cats.

The site also had a story about how talking to our pets is a sign of intelligence. I feel so validated.

Best of luck when the wind and the waves kick up and it isn’t hurricane season. When it comes to that island and also Ocracoke island, there isn’t much for engineering to do if the water is high enough to wreck the best laid plans…in this case asphalt. And since I grew up 100 miles inland from Manteo or Nags head, there just isn’t enough money or insurance for such a home my two cents. Build it inland if you must.

https://www.cbs17.com/news/north-carolina-news/key-highway-closes-at-nc-outer-banks-amid-flood-warning-waves-up-to-15-feet/

The good news is this: the worst hasn’t happened yet, even in states where bad things tend to occur. There’s time to leave before everyone leaves before you, and you’re left selling to no one who wants to buy. This sentence departs reality in terms of being a solution. The idea that you can move out of harm’s way seems a stretch. Selective too, if one considers economic strata. Destructive in a me first good luck everybody else sense. Yet there’s no denying it does seem predictive. Not looking forward to the days when everyone’s a nomad.

I’ve got some lots in Erie, Pa. for sale.

There’s never been a better time to buy and they’re going fast!!

Okay, bad humor aside, Dan Gilbert, the chief of Quicken and owner of the Cleveland Cavaliers, has been buying up tons of property in and around Detroit for years, and I sometimes wonder if, at least in the back of his mind, it’s a potential climate play. There’s a lotta room for infill in Great Lakes cities, and the infrastructure is already in place.

M Dawg Political Consulting, Prediction Markets and Specialty Grifts, LLC (A Duke DeGuise Company) is currently seeking Limited Partners for this once-in-a-millenium opportunity!

Actually Atlanta looks like a good spot in terms of climate safety. Whoever located this town when it was founded knew what they were doing, and we are next door to Florida. People think of the city as a backwater. Then they get here and find out how lovely it is, in terms of weather and a beautiful canopy forest that blankets the city, and then they stay. I say this with chagrin, as this is my home town. So I hate to think of how big this city will get, and how much of the charm of this lovely habitat will be lost when that happens.

OTOH, just in the last two decades, the population of immigrants has changed the demographics of the city so much that the old Jim Crow antagonism between the black and white populations has been eclipsed. White flight has moved beyond the counties adjacent to the city which are now majority Asian or Hispanic.

If your insurance is $12,000 a year you’re probably better off going without insurance and putting that money in a high yield savings account each year to cover damages.

What good does an extra 6 percent do if your house is destroyed? Even if you doubled the 12k that’s a fraction of the total cost of a home

And what about the future of tornado alley?

How many inland states does that cover?

And are they doing any refunds of premiums?

Home insurance has gone from $4k per annum to the present $7,200 3 years later after the 2020 Castle & 2021 KNP Fires burned over 250k acres in total, almost all of it in the high country, with no property loss whatsoever here in Tiny Town or any of the Sierra foothill towns, owing perhaps to the firefighters keeping it at bay, and the idea that there aren’t many pine trees in the foothills, its an oak savanna for the most part, and when is the last time you heard of an oak forest going up in flames?

The leaves just smolder unlike oh so combustible pine needles, and oak trees aren’t all that close to one another, not so many fire ladders to contend with, and we don’t really get winds here all that much, according to what the fire chief related.

There are a few fire’y trees in the native population around these parts (i’m looking at you ceanothus cuneatus!) and i’ve tamed their tendrils, as they have a nasty habit of spreading dead limbs on the floor, bad buck brush!

I’m being warmed by the wherewithal for a wildfire by wood that will never contribute to the delinquency of an uncontrolled conflagration, and in terms of insurance policies, honestly, if I were to hire a crew to get rid of the remaining dead wood on the many splendored acres of the all cats and no cattle ranch, it would probably cost me around $14,400 (a couple years of insurance payments) to complete the job i’ve been working at for over a decade, but keep getting stymied by newlydeads which are falling for me at a rate about double of what I can handle, some disassembly required.

But the fact is I enjoy working in the yard and sometimes you gotta show a tree who’s boss, wielding the 18 inch Ryobi 40v chainsaw. It’s a workout parting out dead trees or limbs.

We are nowhere near an earthquake fault, so that isn’t a worry, nor near a flood zone either, so fire is the only threat of Mother Nature’s whims.

I’ve given thought to not having insurance and maybe if I felt confident that on account of 3 of the 4 sides of me as far as neighbors go, have been diligent as well in preparing their land for something wicked this way comes, and say the insurance company wants $10k a year now…

But if I ever give up my insurance and then decide I should have coverage again, it isn’t like anybody is going to take me on as a new customer, that’s the catch 451, er 22.

I believe the Eastern Sierra Fault Zone is near you. Fortunately, single level wood structures are seismic survivable.

Other peoples faults can be an issue, we were in our cabin in Mineral King when the 7.1 2019 Ridgecrest temblor hit, and it felt like a good old LA 5.1 model 50 miles away, no biggie.

The 1906 SF quake set off avalanches in Mineral King Valley that destroyed many cabins there at the time.

p.s.

Look for long established places which were climate change proofed by the locals over thousands of years, such as here. In that stretch there is a couple of quite lengthy droughts of over 200 years and 135 years, which happened starting around 1,000 AD. We are perhaps 32nd in line for water, and then its all wilderness beyond that, not a lot different than back in their day, which had a very similar population base as ours presently.

Was up at the Sherman tree the other day with my brother in law and his kids, and one of the display items off to the side is a cross-cut slab of Giant Sequoia around 2,000 years old, and the evidence is right there in the rings, distinct looking and then all of the sudden, a 2 inch section for the first drought where you can’t make out any individual rings-its just a blur, and then a gap of discernible rings, followed by a 1 1/2 inch blur for the 2nd drought.

To put things in perspective, in the past decade we were only a year or 2 away from one of those horrifying ‘when the water runs out’ stories for the Big Smokes in Cali dependent on somebody else’s water source, in the past couple of brutal droughts which both got bailed out by bountiful winters in the end, got lucky.

Interesting that companies like State Farm are only pulling out of the home insurance market in California. Doesn’t seem to apply to commericial real estate.

Insurance in CA is already at this state. My Homeowners policy here in the desert (not even a tree on my block, was bumped from $800/yr to over $3000 last fall.

Retired now, I had no choice but to self insure.

I just finished reading “Fire Weather” by John Vaillant. I highly reccomend this book even though it may destroy any hope in the future of life on this planet as we understand it.

They redid the fire maps a couple of years ago and my house’s classification changed. My home insurance went from $2900 to $6600 in one year and this year is $7200.

I also got added to the annual fire inspection list and get to pay an additional $150/yr in property tax for the privilege.

Why is any form of insurance privatized, profit-driven? For many years tax-based Medicare-for-All has met with wide public approval. No mystery why we don’t have it.

When there are gigenormous disasters state and Federal resources are brought to bear. Privatized insurance cannot do what needs to be done.

All insurance should be socialized. No one should profit from others’ misery.

My insurance is through a mutual insurance entity. I don’t think the “profit” aspect is that big a part of the cost.

One can imagine that this “socialized” insurance would be gamed by real estate developers to build in high hazard regions.

This could be a massive “Privatize profits, socialize losses” gift to many who would be quick to profit from it.

Isn’t this already the case with US government subsidized flood insurance?

Yes it is. As always socialization is such a bad idea, exactly like in healthcare. People knowingly build and sell house in horrible zones and m0r0ns oopsie buyers knowingly buy them, and they cry fowl when shit happens.

Missing from this discussion is that a mortgage loan requires that the borrower carry insurance on their property.

I’ve noticed that over the past dozen years or so that mortgages that I’ve taken out got sold to companies that seemed to be quite interested in peddling me insurance — and even more interested in threatening to force-place their over-priced policy on the property at the slightest whiff that a premium hadn’t been paid well in advance.

Watch for foreclosures.

Indeed. Hard not to conclude that financing real estate will no longer be available for the serfs. Yet that busts up the liar loans grift, so maybe not. Or perhaps this just moves the predatory financing crowd higher up the food chain. Won’t they find themselves already there? Somebody’s gonna lose some turf.

The now-outlawed Liar’s Loan grift was all about generating Foreclosure Futures. While I do believe that homeowners insurance has become under-priced and under-reserved due to wildland encroachment and climate risk, insurance cancellation is the latest iteration of Foreclosure Futures.

It’s the same model as Private Equity: leveraged asset-stripping and rent extraction. Mortgage originators and servicers used the marks to pass-through subprime lending from the Treasury via TBTF banks. When the mark inevitably defaults they scoop-up the property on the cheap, while skimming fees all around. Now they can rent it back to the marks and the cash keeps flowing in.

Admittedly a bit of an over-simplification — but a likely understatement of the layers of grift by our rentier caste. Insurance requirements are simply becoming another way to bleed-out the mark before foreclosing on the property.

A lender that sounds like Bells Fraudco was a master at forced-placed insurance scams. One such scam they would play a shell game of change their P.O. Box address of where the proof on insurance would go against the homeowner’s agent.

Perhaps a stupid question: how does anyone get a mortgage to buy a house without insurance?

Cash.

Americans collectively insist on living in plywood boxes, and even most new apartment buildings are plywood boxes, and then are shocked, shocked when the inevitable happens. Insane.

And yes, one cement building can burn down, but something like the Camp Fire is much less likely. Cement can also get flooded, but a total mildewed loss?

Yes, construction here is a *JOKE*.

A lot of people can’t sell their homes because they locked in low rates. If they can’t afford insurance, and the mortgage requires it, what do they do?

what if the prevailing materials of housing structures changed?

Then that land that had those stick built wooden homes that got trashed were replaced with intelligently engineered and OVERbuilt homes made of some old/new materials like aerated concrete that are inherently safer from fire, and water, and rot, and bugs…. and can be equipped to deal with seismic shifts too.

Built into a hill to benefit the thermal mass of the earth…. of just built above the water peril zone… and covered with dirt for the same effect… maybe?

What if the investment was intended to provide long term housing… instead of just lasting decades… maybe the return on investment could pay off for double or triple that time or more with a useable dwelling? I hope my house lasts a couple hundred years…. and whomever is alive then can still find comfort and peace and sanctuary….

Which is not to say all the lame brained places to build houses shouldn’t be returned back to nature.

Back in the glory days of the Nonpartisan League of North Dakota (1915 – 1920 or so), crop insurance became socialized – run by the state, along with a state bank and several other things farmers needed. The Nonpartisan League was so successful, the idea spread throughout the West – eventually to be absorbed by the Progressive Movement. But worth looking at again.

Planning is socialism.