Well, this is starting to get the feel of a bad soap opera, which is not helpful to Citi (never a good sign when I leave my computer on a Sunday afternoon and find multiple news updates when I return. This may not be full crisis mode, but it is certainly not a good sign).

It speaks of a badly organized process, which makes perfect sense, given the fact set. Citi has apparently gone from denying anything is amiss to talking with the government about assistance. That was predictable. But despite the fact that Citi clearly cannot be permitted to go under (not that we are there yet, mind you, but the longer Citi flails about, the more concerns start to escalate), the reaction from DC to Ciit’s appeals appears less than enthusiastic. That in turn is probably due to mixed messages from Citi and lack of clarity as to how much it might need and why.

Of course, if you are Vikram Pandit and in denial that real trouble is possible, you are probably going to have difficulty coming up with a realistic figure as to how bad bad could get. And the very last thing the officialdom wants is another AIG, where an initial commitment turns into a black hole.

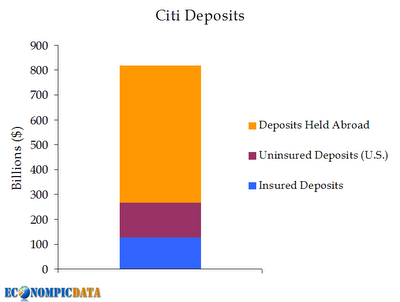

Felix Salmon and Econompic (hat tip reader ndk) summarizes the fundamental risk to the bank, text from Felix, chart from Econompic:

As of June 30, Citigroup had a whopping $820 billion in total deposits — but its estimated insured deposits were only $126 billion, and fully $554 billion — yes, well over half a trillion dollars — was held abroad.

So we have depositors who are at risk if anything bad happens, and a bank with a $2.2 trillion balance sheet with an additional $1.2 trillion of off balance sheet exposures. The typical big firm l problem of lack of transparency is amplified by the global nature of Citi’s business and the OBS component.

According to the Wall Street Journal, talks with the Treasury Department had focused on creating a bad bank for dodgy Citi assets:

Citigroup Inc. is nearing agreement with U.S. government officials to create a structure that would house some of the financial giant’s risky assets, according to people familiar with the situation.

While the discussions remain fluid and might not result in an agreement, talks were progressing Sunday toward creation of what would essentially be a “bad bank.” That structure would help Citigroup cleanse its balance sheet of billions of dollars in potentially toxic assets, these people said.

The bad bank also might absorb assets from Citigroup’s off-balance-sheet entities, which hold $1.23 trillion…

Under the terms being discussed, Citigroup would agree to absorb losses on assets covered by the agreement up to a certain threshold. The federal government would cover losses beyond that level, people familiar with the matter said. One person said the new entity is expected to hold about $50 billion of assets…..

One rescue structure under consideration would resemble part of the $150 billion bailout plan that the government struck with AIG in November as part of a restructuring of the previous bailout. Two vehicles, funded largely by as much as $52.5 billion in government money, were created to take on risks from some of AIG’s souring assets, including exposure to credit derivatives.

$50 billion of dud assets is smaller than some observers had thought the bank might need to clean up.

But CNBC (hat tip reader Dwight via Calculated Risk) reported in the afternoon that the government it not exactly keen:

Sources with knowledge of the deal say government officials are now getting cold feet over the plan to buy the troubled assets from Citigroup.

Situation is still fluid and people close to the company say some sort of a deal will likely be worked out tonight. one other option being considered now is for the government to put money into citigroup.

The problem with buying the assets from citi is political: people close to the deal know that other firms will line up and ask the government to purchase their troubled assets as well knowing that all brokerage stocks got crushed when treasury secretary hank paulson reversed his plan on the tarp to direct capital infusions to the banks and away from buying troubled assets.

And why are we having such trouble with coming up with a deal? One way to characterize it is that the Administration is not willing to nationalize banks, out of both ideological sqeamisheness and the reluctance to consolidate debt.

But the real problem is more basic. Why does the Administration need to be fair? This is a one-off, emergency measure. The fact that it is worrying about other banks demanding the same deal suggests the terms are not sufficiently punitive to Citi management (note the stress on the impact on the key actors). But even if it is not as nasty as it ought to be to Citi, people in power have the right to be capricious. Citi is unique on so many dimensions that it is easy to argue that a deal for Citi need not apply to anyone else.

This does not add up. There may be another “real” reason, but the stated reason for reluctance makes no sense. Are the powers that be trying to see if they can push this back beyond the decision point on the auto industry rescue? If Citi is bailed out, it becomes politically untenable not to help Big Auto. Paulson’s initial strategy on Fannie and Freddie was to try to see if his bazooka bluff would work. It didn’t but it kept matters in play for a couple of additional months.

Also note the latest Bloomberg report suggests the amount of dud assets under consideration is $100 billion.

us tax payers should pay to insulate foreign depositors because???

Dear Fed,

Acquire Citibank. Pay last closing price for all common stock outstanding. Seize the assets, strap on some testicles, and assume the liabilities.

Or don’t acquire Citibank. Do it, or don’t. If you do it, just do it. What, exactly, is so difficult about this? Why is it necessary to befoul USG’s balance sheet with these ridiculous feats of creative accounting?

Normally, when you construct off-balance-sheet vehicles and other exotic financial structures, you’re trying to fool the IRS, the SEC, or both. When you do this in Washington, however, you are trying to fool voters. Not cool, guys.

Headly Lamar is getting peeved, someone chewing gum in line and there is not enough for everone.

Come on Headly pull the trigger and everyone will get the idea.

Skippy

us tax payers should pay to insulate foreign depositors because???

Isn’t that what Iceland tried to say to the UK?

The simple answer is, we shouldn’t. If the foreign countries wanted FDIC insurance, they should have enacted their own laws to force protection

When you do this in Washington, however, you are trying to fool voters.

You know as well as I do, moldbug, that if we had proper marks and accounting for the consolidated Treasury/Entitlement/Fed accounts, we’d be obviously bankrupt. I have two additional reasons beyond fooling voters, though:

* Fool foreign investors;

* Create the right distinctions to increase the likelihood we can selectively default rather than simply devalue, which might not work anyway

Isn’t that what Iceland tried to say to the UK?

Bingo.

The simple answer is, we shouldn’t. If the foreign countries wanted FDIC insurance, they should have enacted their own laws to force protection

Is that really the right answer? Remember how much capital we need from our friends right now. I’ve already had “I am not a Terrorist, Mr. Wen” tattooed on my chest, just in case.

“Is that really the right answer? “

Yes it is. The world b*tches about how we go around the world playing policeman with our military. Europe especially acts all uptight that they have no voice. Well if you can’t take care of yourselves, what makes you think you can take care of anywhere else? It’s time for the rest of the world to grow up.

The point about the lack of foreign deposits being insured goes to a run on the bank scenario by foreign depositors. You are saving the bank first and the foreign depositors only indirectly.

It’s time for the Europeans and the rest of the world to grow up?

Wow, I’m amazed at how blind Americans are as to their position in the world. Every country around the world is financing the U.S. to run these absurd budget deficits, out of which the U.S. government funds a banana republic Paulson Plan, illegal military campaigns and the fucking boys with toys military industrial complex that goes with it. Reality check: nobody needs the U.S. to take care of them.

I think people over there need to consider some serious ego-shrinking. When the dollar will stop functioning as global reserve currency, I don’t know where you guys are going to be at. And neither the rest of the world, for that matter..

but at least elsewhere people are not blinded by their national mythology..

All that needs to happen is for the Fed to issue a public statement saying “we have examined their books and found them to fundamentally be a healthy solvent institution; nevertheless, in the event there is a run on their deposits, we stand ready to provide them an unlimited line of credit to meet liquidity demands”. End of story. No need for complicated backstops, asset purchases, and capital injections. Unless of course, it’s not true that they are “fundamentally a healthy solvent institution”.

Tick…Tick…Tick

Kaboom!

It’s gotten to the point of a recurring nightmare where the dream is always the same and you can feel it coming:

-Shares begin to drop

-Rumors get denied and mongerers are accused -Weekend confirms the worst

-A partly public bailout occurs but yet another crippled financial firm becomes a ward of the state

And joins the others in the assylum

Tick…Tick…Tick

Kaboom!

It’s gotten to the point of a recurring nightmare where the dream is always the same and you can feel it coming:

-Shares begin to drop

-Rumors get denied and mongerers are accused -Weekend confirms the worst

-A partly public bailout occurs but yet another crippled financial firm becomes a ward of the state

And joins the others in the assylum

Yeah, because the USA in recent years has been a case-study in maturity.

There is no faith in Henry Paulson. TARP is a failure. The government must take over the bank. Don’t pay the stock-holders a dime. That will keep other banks from begging. It’s all or nothing, you’re either with us or against us. The government will split the bank, put the bad assets in a separate entity. Sell off the working bank unit within 2-3 years. It worked with great success in Sweden which had a severe financial crisis (once in a lifetime!) in the early 90’s. There’s nothing wrong about learning from history. Don’t follow the Japanese.

Blah.

They’re hesitant about the outright acquisition for the same reason the entire banking bailout process has been so contradictory so far:

they’re afraid of a system mark-to-market event.

Say it again:

They’re afraid of mark-to-market.

There’s still that huge swirling cloud of dodgy assets out there. If the housing market wonks are correct, there’s still 10-30% more price contraction coming. Multiply that by the leveraged position that (the few remaining) big banks have, and the answer is clear.

If the govt. just seizes one of these monsters and sells off the assets, it’s game over for the whole system. Same reason we have this bizzaro-world “we-own-it-but-not-really” bailout of AIG.

It is funny to listen to the obama hacks who have firmly established that we have a confidence problem and all we need is time. Bush and co told us we had a liquidity issue until they were brought to their kneews with BS and then LEH. These political hacks are all the same. “the Handlers” are clearly trying to play a psychological game here. The porblem is the feel good era is over.

This entire charade is a disgrace.

Very sad. We now need to have high stock prices to have “confidence.” We need to have high house prices to have “confidence.” We really are soft.

my read of the bloomberg report was 400bn in bad stuff and the ‘negotiation’ was around how much of that was gonna stay and how much the gov’t asumed.

they also said in the secnd half of the article that things could get worse IF the emerging market went down because citi is highly exposed.

wow…IF the EM goes south. it is and will go way south…is that a doubt??

so, these guys made bad investments and have bad management and no risk management, have been happily making tons of $ selling shit basically, fly of private jets, have staff and white collar workers being paid more per hr then auto labor with better bennie and it is blantantly obvious it will get worse…yet they are too big to fail so we have another AIG whether the line after them is long or shot.

plus a lot of folks from other countries using citi for their own personal (maybe tax or ror reasons). and we are suppose to give them money over the weekend?

no big congressional hearing and public/pundit outcry???

can someone tell this layman what i am missing in this?

\ oh, i know, this first big bail out…no the second, they already got 25Bm..will likely buy some time and give them a moment to sort out some of the important counter players….guessing maybe goldman..maybe jpm???

then once they sorted them out ‘fairly’ and flushly…then the EM will turn south (oh, it already has you say…they must not have noticed)…once south the real issues come out and …wow..still too big to fail and deeper black hole.

didn’t japan try to hid all the ugly stuff for too long too? how is this different really and who is being fooled…foolish??

they’re afraid of a system mark-to-market event.

You’re absolutely right, CTMM, but I think it’s irrelevant at this point. We already have extraordinary regulatory and accounting forbearance in place, and a bit more could always be added.

We’re way beyond where bank accounting is trusted or even matters. Investors, depositors, and creditors will believe whatever they want to believe. This, combined with internal strife, will be the pressures that blow things up now.

yes indeedy. afraid of a mark to market EVENT. probalby that is why hank used bait and switched from buying toxic stuff to injection. imagine if they had to buy that stuff and them tell someone (congress,public, press) how much they paid…how much its worth.

If they paid market, everyone could then claim that value on their books and everyone would be fooled…a fool..for about one nano second..and want to same price to sell the same stuff on their books.

it seems like the old game kids played with the water balloon…push on side and it moved the otehr way..push, etc etc…unitl of course, the balloon broke and mom got made. in this case there seems to be no mom and with the media owned by same..john q public is treated like mushrooms…kept in the dark and fed shit daily.

will it change? how can it change?

Reality check: nobody needs the U.S. to take care of them.

China sure needs American consumers. Just watch.

“the Handlers” are clearly trying to play a psychological game here.

bingo. its been a confidence game from the start and failed every time. this I imagine will set off a bear rally rocket – but it will be short lived, perhaps a few months, or just a few days.

C has been trying to shed their liabilities to someone, anyone, for 14 months while retaining all their assets. That is nothing more than gross fraud. The fact the public authorities even entertain that concept for an instant is an indescribable disgrace; that Paulson has repeatedly tried to force such an outcome is a crime. But what that have in the District now is a political problem: Mere hours, not even days, after the auto industry with all its workers, suppliers, and pensioners was told that $25 was far too much to ask for, How dare they?, Pandit wants $400B for a _single_ mega-bank. Bad visuals, call it that.

I expect that within days we will have AIG Redux, where the Guvming ‘assumes the position of responsibility’while leaving management in place, equity untouched, and bond holders [nominally] in the money. Of course, that’s a total delusion, bigger than even the Japanese keeping their insolvent big banks propped, but this is what things have come to. And it ‘worked’ in Japan, and has ‘worked’ with AIG, so it works, right? . . . But. But the zombie will have to be fed.

Yves, have you really thought this out?

Why does the Administration need to be fair?

Remember this:

brokerage stocks got crushed when treasury secretary hank paulson reversed his plan on the tarp to direct capital infusions to the banks and away from buying troubled assets.

The best way to freeze up the market is to suddenly make investment unpredictable. If you say to people, all the banks will be bailed out, then people can have some degree of assurance when planning their investments. Likewise, when you publicly state that you refuse to bail out the banks, people can invest somewhere else. But when you say to people, we’ll bail out some banks and not the others, you totally freeze financial investment, since you make investments inherently more risky. Treasury should have some sort of consistent policy, instead of making it up as they go along. But that of course presumes that they know what they are doing; which of of course, they don’t.

Social Pathologist,

The Treasury can be unfair all day as long as it communicates clearly. “Unfair” in this context means “Just because Citi got a deal, you can dream and send lobbyists all day. Ain’t happening. We are lame ducks and immune to anything other than complete, undeniable imminent train wrecks”

The problem with TARP is that Paulson said, very clearly and repeatedly, what he intended to do and then changed course 180 degrees.

All they have to do is say convincingly is that the Citi deal is ONLY for Citi, cone up with some reasons why Citi is unique (there are tons, not hard) and rebuff all approaches.

Save us Obi Ben Bernoki, you’re our only hope!

I love the Sunday night bailouts! It makes me so…bullish! Think I’ll buy some Amercian stocks. Not. Robert Rubin is on my dartboard. I’m aiming for the balls. A criminal of the first order.

Citi the latest ploy is to leave the toxic stuff on C’s books and have the US gov guarentee above about 40Bn in bad debt. this will amount to over 1 trillion for sure.

but the ploy is to keep the number in hiding for many months, years from press, congress and u and me. cause if they move it to a ‘bad bank’ or ‘buy it’ we will wonder ‘how much is it worth or gonna cost us.

eventually, all this guarenteeing and buying by FED and gov will come to lite and wow…tax payers might not be counting,press might not be counting ,nor congress..but surely other governments are counting as the total runs into the 3 trillion range already

gee, wonder how that will affect the dollar and US credibilty?

Yves, there is no way for the government to “convincingly” say that the Citi deal is only for Citi. There is no reason for anyone to believe that because actions speak louder than words and it is clear that Paulson et al can change their minds at a moments notice. It is also clear that they are remarkably intimidated by a low stock price. This tells everyone that they have no confidence in their own analysis. It also tells equity investors to stay away, which in turn lowers stock prices which in turn causes the feds to panic. It also tells shorts to pile onto any financial stock that starts moving down because the lower their selling can make it go, the more likely they are to spur some sort of dilutive government bailout.

Watch other bank stocks tank tomorrow. That won’t be because fundamentals changed in the last few days. It will be fear of where Paulson will strike next.

No bank is safe now. Citi appeared to have been designated a survivor since it was given TARP money and had the ok to acquire WB. Other banks have rallied as they have gotten TARP money because that seemed to indicate the bank was safe from a fate like that of WM, WB, GSEs, and NCC. Nope.

The government continues to destroy equity and subsidize debt despite the obvious need to de-lever the system.

tompain,

With all due respect, you do not have enough imagination. If Cheney were to take it upon himself to tell bank supplicants “no” in private, it would be believed.

All they have to do is say convincingly is that the Citi deal is ONLY for Citi

If they only had the spine or political will to do that. When GM and Ford come rattling the can, London to a brick the will be coughing up.