In case you missed it, it’s ugly out there. US markets swooned as an unexpectedly weak manufacturing report, the ISM, was so bad it couldn’t be attributed solely to bad weather and deepened investor funk. The January Institute of Supply Management’s manufacturing index dropped from 56.5 in December to 51.3 in last month. Worse, it’s new orders sub index plunged from 61.4 to 51.2, the biggest decline since 1980. The S&P 500 fell 2.3%, the ten year Treasury rallied as yield fell to 2.58%, and the dollar dropped as investors anticipated the Fed putting the taper on hold.

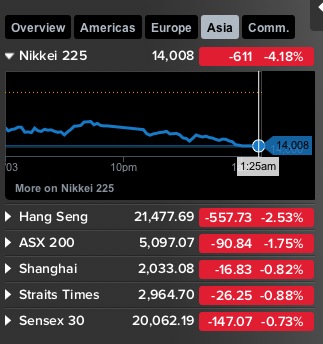

The rout continued in Asia, with the Nikkei an impressive 4.2%:

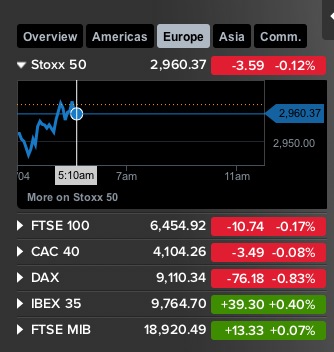

Now admittedly Europe is a little less roiled as of this hour, and S&P futures are up half a percent, so Mr. Market’s latest tizzy may be burning itself out:

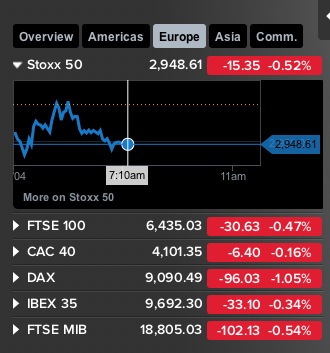

Update: Well, so much for allowing for the optimists braking the decline. This is Bloomberg as of 7:30 AM (admittedly with the usual retail user delay). S&P futures up only 6 points v. 8.5 on the earlier AM sighting:

Nevertheless, the distress in emerging markets continues apace. As we warned yesterday, even with the defensive increases in interest rates in Argentina, Mexico, Turkey, South Africa, and other emerging economies, investors who are now anticipating a return to the “old normal” are now looking at real returns relative to historical norms and deem them to be too low. So we can expect continuing pressure on emerging economies to raise rates further. That might halt the currency runs, but then you have the knock-on effect of the rate shock, which will kill growth. Most of these economies were already feeling a slowdown thanks to falling prices for commodities as demand from China cooled. A sudden downturn in these economies means more credit risk and lower prospective returns, leading to more capital outflows. It may take IMF intervention to break some of these vicious cycles.

If you have the luxury of being able to be detached, the market fireworks are perversely entertaining. At the beginning of January, the tone among US equity investors was close to being unanimously bullish as you ever get. The World Bank increased its global growth forecast on January 15. The IMF increased its global growth forecast on January 21. Last week’s FOMC statement ignored the emerging market perturbations, which was no surprise (the Fed has consistently refused to acknowledge the impact of its policies on emerging markets or commodities). And as Doug Noland points out, the central bank’s most vocal hawk, Dallas Fed president Dick Fisher, pronounced himself pleased that his colleagues were falling in line with his views. But even more disconcerting was the Fed’s increasingly optimistic reading on the economy.

Consider the contrast with today: Goldman forecasts a “more serious” global slowdown. Ford and GM revenues dropped sharply, with investors worried that the decline isn’t due solely to bad weather. And investor confidence about US corporate earnings growth is also waning.

The normal behavior at this point in the drama is for one or two regional Fed presidents to say reassuring things to the Market Gods. That might calm things down for a few days. But we have a new set of job reports due out on Friday. Before today, they were expected to show improvement from December’s weak 74,000 increase in nonfarm payrolls. The Bloomberg consensus was for a 181,000, increase, with forecasts ranging from 125,000 to 270,000. Presumably investors will shade their expectations lower based on the crappy ISM, but the open question is by how much.

But the bigger issue is how wretchedly wrong the Fed has been, and how consistently it has believed its own PR and been hostage to confirmation bias. In the runup to the crisis, it was Bernanke who coined the phrase “Great Moderation,” mistakenly seeing dampening of business cycles as a virtue, while ignoring the financialization of the economy, the dependence of growth on rising and unproductive consumer borrowing, and business net saving (as in disinvestment), previously unheard of in a period of growth. He professed to be worried about deflation in 2002 in his “Helicopter Ben” speech which gave cover to Greenspan to hold interest rates low for an unprecedented nine quarters after the dot com bust.

But what were Bernanke’s bulwarks against deflation? The first was a “buffer zone” of not letting inflation rates fall too far. But in driving short term rates below 1% (which alarmed me during the Fed’s crisis responses), the Fed anchored lower inflation expectations. His second bulwark was:

A healthy, well capitalized banking system and smoothly functioning capital markets are an important line of defense against deflationary shocks. The Fed should and does use its regulatory and supervisory powers to ensure that the financial system will remain resilient if financial conditions change rapidly.

The Fed failed and has continued to fail on that front. It sat pat as banks increased their leverage levels as the 2000s progressed and ignored the fact that they’d have to stand behind supposedly off-balance sheet vehicles like SIVs and credit card securitizations. While it has prodded banks to improve capital levels post crisis, most commentators deem the increases to be insufficient to eliminate the “too big to fail” problem. As for “well functioning capital markets,” the central bank has also ignored post crisis the rise of high-frequency trading, which has come to dominate the US equity markets and is making inroads into foreign exchange and commodities markets. HFT weakens market stability by providing the finance equivalent of junk calories: more liquidity when it’s not necessary or helpful (when markets are trading normally) and worse, a disruptive draining of liquidity when it’s most needed, when markets are roiled.

So despite professing concerns about deflation, Bernanke and his colleagues failed to take preventive measures and ignored the obvious signs of danger before the blowup, of extreme underpricing for risk across all credit markets. During the crisis, the central bank again failed to understand the severity of the problem, going into “mission accomplished” mode after each for the first three acute phases prior to the September-Octber 2008 meltdown.

We’ve chronicled at length how the authorities merely used duct tape and baling wire to patch up the financial system rather than engaging in badly needed fundamental reforms or focusing their rescue efforts on the real economy.

Unduly impressed with their “success” in largely restoring the status quo ante that got us into this mess, the Fed appeared to have persuaded itself that QE would help the real economy, as opposed to simply goose financial asset prices. Admittedly, there was some indirect stimulus as credit-worthy homeowners refinanced en masse and the top wealthy saw strong income growth. But the Fed has simply chosen to ignore inconvenient information: that per Willem Buiter, the wealth effect of housing works only when housing prices are in bubble territory (meaning the real economy stimulus of QE would be weak), that per Richard Koo, consumers and businesses in a balance sheet recession prioritize paying down debt over spending (so the Fed should have pushed for debt restructuring, particularly of mortgages, rather than giving banks and investors a free pass on reckless lending), that QE was not going to lead banks to loosen lending much to consumers or small businesses (and separately, even if banks were predisposed to be more generous, businesses don’t decide to run out and invest because money is on sale. Unless the cost of money is one of your major input costs, meaning you are a financial services industry participant, the cost of money is a secondary or tertiary consideration. It might constrain investment, but the big driver is whether the principals see a market opportunity. And in a generally crappy economy, opportunities are thin indeed).

From what we can tell at this remove, the Fed realized sometime last year that QE was not working and decided to get out. But even then, it seems to have failed to understand how it has painted itself in a corner. Nathan Tankus wrote how the Fed ignored what Keynes had written on this point:

Since Bernanke started talking about “tapering off” Quantitative Easing, the bond markets have freaked out. This is a very logical reaction….

Bernanke and other Federal Reserve economists appear bewildered by this phenomenon. The impression one gets from their follow-up comments is that they wished they could ask bond speculators “did you read the damn speech?” The answer, of course, is no and for good reason.

All investors need to know is the conditions under which QE (and for that matter, the Zero Interest Rate Policy) will be pursued has changed. Now the substantive change may actually be relatively minor, but that’s irrelevant to speculators. The reason is very simple: those holding assets with longer maturities will take huge capital losses with relatively small changes in interest rates (As a reminder: it is basic “bond math” that a change in interest rates send bond prices in the reverse direction. A rise in interest rates makes bond prices fall and a fall in interest rates make bond prices rise). It is better to exit now when those future changes are uncertain then take even more massive losses.

This is the logic behind the actual “liquidity trap” presented by Keynes in the general theory. Specifically, Chapter 15 entitled “The Psychological and Business Incentives To Liquidity.” Here he argues that every fall in the interest rate relative to what is commonly believed to be a “safe” rate increases the “risk of illiquidity”. The the “risk of illiquidity” is the risk of holding an asset not easily convertible into money at “book” value (this also means an asset is more or less “liquid” based on the relative easiness to convert into money “book” value). Further, rather then seeing interest as a return to “waiting”, Keynes argues that it is “a sort of insurance premium to offset the risk of loss on capital account”.

How can one evaluate the uncertainties relative to the “insurance”? By what has been subsequently known as “Keynes’s square rule”.

The square rule was defined by Keynes in this chapter as “an amount equal to the difference between the squares of the old rate of interest and the new” (mathematically represented as Δi = i2 ). If interest rates (at that maturity) are expected to rise faster then a squaring of itself, it means your capital losses (market price of the bond or investment) will fall faster then the increase in the rate of return (and vice versa).

Based on this understanding, a liquidity trap is not a short term rate of interest at zero but a uniform expectation that interest rates will rise to such an extent that the rate of return on a bond or equity won’t preserve your principal and thus a refusal by anyone but the central bank to buy bonds at such a high price (i.e., low interest rate).

So what happened was perverse: the Fed lost nerve temporarily and hedged its taper talk. Investors, who have strong incentives not to leave the party until it is almost too late, resumed investing in most risky trades (although Treasuries and MBS did not revert to their prior levels). Traders at big financial firms and many fund managers had every reason to keep asset prices aloft until December 31, since their bonuses keyed off full year profits. And many investors also seemed to take confidence in the notion that big financial crises happen only in the fall, so even if there might be some taper-related upheaval, anything in the first half would be a blip.

Now this investor confidence was also based on persistent sunny readings of decidedly mixed data. For instance, for the past three quarters, companies have increasingly beaten earnings expectations by lowering guidance. There have been far too many monthly improvements in official data that have resulted in part from downward revisions of the prior month’s results. The Fed and many investors have chosen to underweigh the severity of stress in the job market. But one of the biggest factors may well be the way income inequality plays into readings of the economy. The top wealthy simply don’t see it. The top 10% are for the most part not badly impacted. The Board of Governors is located in Washington, which is one of the strongest performing economies in the entire US. And who do they interact with, mainly? Bankers and CEOs, who are in the top income cohort.

The Fed has acted as if it can master the markets, and until late last year, that appeared to be correct. But consider what is happening in China, where observers have even more confidence in the authorities’ ability to control outcomes in a supposed command economy. The officialdom was afraid to let an entirely disposable mid-sized trust company default (instead there was an 11th hour rescue which smells of having been orchestrated). Most observers expected a default and assumed it would serve as a salutary warning to speculators. The fact that even the Chinese look to be fearful of crossing the Market Gods bodes ill for a soft landing there, and betides ill for the Fed navigating its way out of its cul de sac successfully.

As I often say, it would be better if I were proven wrong. But I find it hard to script a happy ending to this movie.

Another wonderfully depressing posting.

And on the labor front, Dell just announced the coming layoffs of 15K

I can’t get the poem I wrote for Yves posting from yesterday out of my head. I don’t know if it will get by the troll monitor but I am going to try to share it again here:

Ring around the debts

A pocket full of bets

Derivatives, derivatives

We all fall down

This is not an “original” poem any more than the one about the Great Plague was but I suspect folks will get the gist of my message.

“As I often say, it would be better if I were proven wrong. But I find it hard to script a happy ending to this movie.”

In that case, there’s very good news! The track record gives much reason for optimism. Four straight years of doom & gloom and the market has doubled and tripled from the 2009 bottom. Doom & Gloom last year and the market went up 40%! At some point the market will go down. Maybe it’s now, maybe a lot! Sometimes the Fed has nothing to do with it. Even God rested on the 7th day. Doesn’t the market get a day off too?

Trying to figure out if I should add to my short position or just go big for out of the money puts on some high flyer. This could be a good time to get rich quick. Of course if Yellen tapers the taper we could see a 300 point up day and then another. Ouch.

You rogue.

For every 100 slavishly adoring comments I make as an Yves Smith fanboy, I have to make at least one or two that are neutral. That way I don’t go overboard and lose all credibility!

Yellen will soon remind the Market that Taper is a two way street, data dependent bla bla bla. Two days, 500-600 points is all the power the Fed has now. Stay craazy.

The “Market” does not equal the economy.

There has been almost no improvement in the economy since the Great Recession when accounting for population growth. If you hold the labor participation rate close to its pre-crash level, unemployment is still around 10%. Sounds to me that the doom and gloom has been dead on.

How do you think the economy is supposed to get back to “normal” growth when the money supply aka private debt is well below its historical (post-1980) trend of above 5% yoy growth?

The economy is supposedly great if you have in-demand skills, experience, and youth on your side. So, basically, if you’re an engineer of some sort or a doctor or something like that.

I doubt that the valedictorians and the high aptitude sets worldwide are losing any sleep over the market fluctuations.

At times like this it pays to remember that other speculators are not playing with their own money. Also, that market calls generally look best in retrospect, when those who have made the wrong ones are no longer talking except to tell you the fare as you exit their cabs.

The real economy and the stock market have been at a significant disconnect. Perhaps at an all time disconnect. If I were to wager a guess I’d say that Mr Market needs approx. a 50% correction from recent highs to fall in line with present economic reality. Of course, unlike when I was a boy growing up in the 60’s, Wall Street has become quite adept at projecting illusions to reality, so I won’t hold my breath waiting for an accurate or enduring barometer on our economic health coming out of illusion central. I’m sure the rolls of newly minted duct tape will be employed in some form to hold together the untruth spewing from Mt. Bullshit over at corner of Broad and Wall. Another 2008 market type waterfall would likely be a fatal blow to all the shit spewers, so like desperate cornered cats you can expect every stop imaginable will be erected to mitigate such an outcome.

Good observation, but while you and I would be happy with a disconnection, TPTB are doing everything they can to get our money into risk assets. But let’s not just focus on the stock market – most Americans don’t get their risk there. Its housing. I believe, real estate values will fall.

Markets stay up only if they are sufficiently juiced that they can ignore reality. Every so often, nevertheless, reality intrudes, and they get spooked.

It’s sort of the reverse of what happens here. Most of us look at the fundamentals. We know how bad things are, but most of the time we have to navigate through the happy talk and upbeat reporting. We know things are going to hit bumps and eventually the wall, but it is still disconcerting living through markets that as Keynes remarked can stay irrational far longer than we can remain solvent.

Re the 181,000 jobs, it is important to remember that is a trend (seasonally adjusted) number. It is a projection about job conditions later in the spring. In actual (non-adjusted) terms, the Christmas job losses show up in the January report. Last January, for example, the number of jobs declined by more than 2.8 million even as the trend line number projected an eventual increase of 148,000. So the economy is not actually going to have added any jobs in January. If conditions are weakening in the economy, then those 181,000 jobs or whatever are not going to materialize later in the spring.

If we could only make the willy wonka economy viable. Or take your pick of bogus industries. The chocolate factory as the engine that runs the economy instead of the stupid auto industry is a deceptive thought when you get down to the bottom line of reality because chocolate is no more viable than cars. That is – not viable at all. We need an economy that functions from top to bottom in a declination of support that does not deprive the bottom from the energy (thus profit or return) it needs to thrive. So more energy, much more – like 99% more – needs to get to the lower strata of the economy because there are MORE people there. More people should mean more scientists and more ecologists, etc. And the good news for the 1% is that conversely, that energy reaching the bottom then circles back upward and nourishes the “upper” strata.” Aka the oligarchs. It’s hard for them to lose even tho they have been unconscionably derelict. But unless we have enlightened policy, it is equally true that it is hard for the 99% to win. Once again, everything is politics.

QE1 could be defensible by doing the confidence fairy bit (which _is_ important to markets). QE2 was dubious at best, QE3(inf) was just dumb (if for no other reason, it made QE unexitable w/o major problems).

Fed’s reaping what they sown, but I doubt they are going to change their policy on a dime – even though right now they could do it (with Yallen in for BB). The problem is that too much of the old fed (voting) still remains, and that Yallen herself believes that monetary policy can (even in current situation) affect employment (which is bollocks to anyone who watched the real world for the last few years – not just in US, but just about anywhere in the world).

I expect that the current EM crisis will blow over (it’s in just about everyone’s interest it does, and Turkey, SAR etc. can be salvaged for a few more months – the problem there is more political than economical anyways, but where it isn’t?), but that we’ll get China problem within a few more years, and the question then will be, is China too large to be saved?

What really worries me is that military hawks are getting a bit more bold in China, and when there’s a country in turmoil, especially a country that believes it’s entitled to something and can blame not getting it (or in general its problems) on someone else, history tells us that military is what it tends to turn to.

Amazon, he biggest online retailer reports lowered revenue and profits. Walmart, the biggest bricks and mortar retailer reports lowered revenue and profits. Pending home sales drop. Car sales dry up. Employment numbers crater.

The WSJ reports today that most all of the big durable goods manufacturers lack pricing power and are, in fact, having to discount to drive sales.

Wages fell over 2% last year when adjusted for inflation, which is only a little over 1%. The seat belt/safety net signs have been turned off. I could go on and on.

Central banks are having their Minsky Moment and are removing the foam on the runway at the greatest moment of impact with deflation.

If it makes you feel any better, the flyers in first class will be fine. Everybody else, not so good.

It seems that it was just last month that the mainstream corporate news reports were telling us how rosy everything seems to be in the markets. Clearly these people have their heads up their arse or they were hoping they could create a self-fulfilling prophesy. If the latter they sure had that backfire on them but I suspect such poorly conveyed reports by the MSM are that they simply have their heads too far up the derrieres of Wall Street

No one can possibly claim this was unforseeable. Following the burst bubbles of 2000 and 2008, “Fed” policy has met and exceeded Einstein’s classic definition of insanity, of doubling-down on the same action that caused the crisis in the first place and of using the same level of thinking that created a problem—neoliberal, supply-side voodoonomics—to solve it. Give the cartel gamblers free money to wager throughout the world, suspend all accounting standards, tear down the firewalls to contain “investment” banking, sell foreclosures to PE slumlords to goose housing bubble 2.0, eliminate accountability for fraud, give obscene raises to unindicted felons (dimon), shred the safety nets, legalize political bribery and then expect the dynamic economy of the New Deal to return. It’s beyond insanity; it’s lunacy, stark raving madness.

Or is it? Forgive my fashion-don’t foil sombrero, but this looks like classic JPM, GSquid pump’n’dump (submerging markets are a bargain!), Shock Doctrine disaster capitalism. Combine such “creative destruction” with police-state surveillance, NDAA, TPP “negotiations”, wars and rumors thereof, and executive assassination powers and this reeks of a global coup.

Somehow, the hoocoudanode? script just doesn’t cut it anymore. Before long, if my paranoia proves prescient, I think we will witness more puzzling contra-indicated machinations from our Machiavellian POTUS, very likely war, in response to this crisis, revealing a deeper and more sinister agenda.

I waver back and forth between your formulation and the old fashioned notion that people really are stupid and self-deluding when it comes to wealth and power. Greenspan and Bernanke might have been insidious cunning geniuses working to a master plan of global financial hegemony, or they could have been Hitler in the bunker moving about phantom armies in a desperate, delusional play for time so that the Allies can begin the Cold War a few months early (you could argue that Hiroshima and Nagasaki were the first salvos in that conflict) and Germany’s fat is hoisted out of the fire. Both scenarios fit the facts as far as I can tell. Both are plausible. Perhaps these guys (and now our gal Yellen) are simply out of their league and, like Mr. Micawber, waiting for something to turn up.

Keynes’s square rule is flawed, because he did not stipulate the duration (that is, the weighted average maturity) of his ‘long-term’ bonds. Also, and more fatally, it requires perfect foresight.

During 2013, the 10-year Treasury note delivered a total return of -7.27%, according to Barclays 10-year nominal comparator index, as its yield rose from 1.76% to 3.00%. Shorter-maturity Treasuries lost less, while longer-dated issues lost more. In Bondland, 2013 was a bloody nightmare, reminiscent of the annus horribilis of 1994.

In 2014, by contrast, Bloomberg is agog at how 10-year T-notes bounced down from their 3 percent yield ceiling: ‘The performance of Treasuries is confounding forecasters who predicted a second consecutive year of losses with their best annual start since 2008, returning 1.6 percent in January as measured by Bank of America Merrill Lynch index data.’

http://www.bloomberg.com/news/2014-02-03/gundlach-shows-why-betting-against-treasuries-a-fool-s-game-3-.html

Timing is everything, comrades. If you think Keynes’s square rule will help you forecast interest rates, by all means get yourself a vintage slide rule and let your fingers do the talking, as your friends with ‘smart phones’ look on in amazement and envy!

Bernanke did what was expedient and expected. He cashed in the Greenspan put and then some.

Lets not forget that the ‘fix’ is in. Dodd-Frank set up the Financial Stability Oversight Council which can approve ‘bail-ins’ for systemically important firms (including insurance companies and major industrials – or finance arms of major industrials – like GE).

“Duct tape and bailing wire” are sufficient when a compliant government has set up a crony safety net. Hoocoodanode?

Over several cycles of boom and bust, I’ve learned that the signal that tanks the markets is when the business press starts doing articles about “wage inflation”.

It seems that for the last 40 years general prosperity has been deemed bad for profits.

Yves — on style alone, this was just a delicious read. I enjoyed it hugely!

POVERTY

Local paper (times news.com)had an excellent article on 50 year war on poverty.

It was 19% under LBJ and now 19%.

It ranged 11-15% with decline in boom and rise in recessions.

Recent job depression longest since Great Depression.

The missing ingredients are Job Growth and Minimum Wage.

We have been stalled in 7-8% Range unemployment since 2007

The Minimum wage has not kept up with inflation as has Food-Housing-Health Care costs.

Had it done so the minimum wage would be 15%+.

Obama has proposed 10.5% which would be a great step to lowering Poverty.

Obama is a bum.He and the democrats are every bit as responsible for the carnage in this country as the republicans.Be it George hw bush,or Clinton,or George bush,or Obama…. they are all fascist /corporatists of the same order.

Democratic party regulars need to wake up to the fact that the democratic party is as complicit in the crimes before us as the republicans.They just talk a different talk, but they have the same walk.

Don’t be such a party pooper Yves. Surely this time is different. OK, well…maybe not. LOL!

http://jessescrossroadscafe.blogspot.com/2014/02/nyse-margin-debt.html

https://scontent-b-lhr.xx.fbcdn.net/hphotos-prn2/t1/1890993_797989803548606_426361731_n.jpg

Lol

This reminds me of a spin done on a Simpsons meme(dental plan/lisa needs braces) from one of the episodes that aired in the 1990s.

BAIL OUT PLAN

The global economy needs braces.

BAIL OUT PLAN

The global economy needs braces.

BAIL OUT PLAN

The global economy needs braces.

Agree with comment above re Yves’ writing – always lucid and well-argued.

A rough start to a pivotal year. Sadly, worse to come on several fronts.

You were so right a while back, when you pointed out how the Fed *has* to say their policies are working, and *has* to taper.