By David Llewellyn-Smith, founding publisher and former editor-in-chief of The Diplomat magazine, now the Asia Pacific’s leading geo-politics website. Originally posted at MacroBusiness

“The Brexit vote implies a substantial increase in economic, political and institutional uncertainty, which is projected to have negative macro-economic consequences, especially in advanced European economies,” it said in its economic update released in Washington on Tuesday.

The fund’s chief economist Maury Obstfeld said Brexit had “thrown a spanner in the works”.

The new forecasts downgrade this year’s global growth from 3.2 per cent to 3.1 per cent and next year’s from 3.5 per cent to 3.4 per cent and slices 0.9 points off next year’s forecast for Britain, cutting it from 2.2 per cent to 1.3 per cent.

Yeh, it’s Brexit’s fault. Not.

This global business cycle stinks and the downgrades were coming anyway as China slowed again and the US tightened. Fact is, the only thing keeping the cycle going at all is stimulus of all varieties so why do these folk keep upgrading growth outlooks as if some wonderful private sector virtuous cycle will magically appear? The answer of course is that if they don’t then the headwinds will get even worse via the crashing confidence fairy.

The world is undergoing a secular deleveraging coupled with a demographic accident that has years, probably decades, to run.

Might have something to do with that spreading Democracy [neoliberal markets – globalism] had nothing to do with uplift in the first bloody place…. its one and only priority was increasing the customer… cough… consumer base so corporatists could increase revenue… cough… remuneration multipliers e.g. bonuses et al…

Disheveled Marsupial…. like the old sales joke…. but boss New Zealanders don’t ware shoes…. yeah kid… think how many we will sell…. first in best dressed my young Padawan…

PS… later in the story the poor NZ’ers have to turn their country into a tax haven – sell it off so they can import the cheap shoes… whilst the sales Sith lord muses about where to retire with his winnings…

Synoia

I’d dreadfully sorry about your …… condition. Does it hurt much? Or was it an accident at childbirth?

I prescribe a course, or two, of complete sentences.

Skippy

How about two words…. Powell Memo…

Disheveled Marsupial…whilst were at it, it should be noted that productivity has very little to do with most people… ask Rubin…

FluffytheObeseCat

Skippy might benefit from a course of soluble fiber and roughage. 10 days of Benefiber(TM) every morning, and pysillium husk capsules each night would add bulk to his stream of consciousness…………. and improve its consistency.

Skippy

Skippy might have benefited from never having to deal with Austrians or neoclassical’s nor the people that confuse numerology with history….

Now you have Eight People Sipping Wine in Kettering and calling it an election

CEO compensation grew faster than the wages of the top 0.1 percent and the stock market

Economic Snapshot • By Lawrence Mishel and Jessica Schieder • July 13, 2016

CEO compensation in the largest firms dipped temporarily in 2015 and remains 940.9 percent above its 1978 level. This growth in CEO compensation far exceeded the growth of the stock market, which grew forty-two percent less (up 542.9 percent). This shows that executives have done far better than the firms they have led and executive pay cannot be simply attributed to better firm performance. Neither can the spectacular rise in CEO compensation be attributed to the ‘market for talent’ providing more rewards for those at the top. The wages of the top 0.1 percent of wage earners (top one out of a thousand) is a decent proxy for the pay of the most financially successful and grew a remarkable 320.5 percent from 1978 to 2014 (the last year for which data are available). Yet, CEO compensation grew roughly three times faster than the wages of the top 0.1 percent. The fact that CEO compensation grew so much faster than the pay of other very highly-paid earners, and far faster than stock prices, indicates that unique dynamics are at play and that corporate governance is not adequately restraining executive pay. – go to epi.org

Don’t even get me started on the studies that show CEO et al pay is not correlated to performance… outside some industry fashion… ripping yarns of Al Dunlap and Perelman thingy…

But yeah deleveraging….

Disheveled Marsupial…. 27C here in wintry Brisbane

TheCatSaid

CalPERS should invest in CEO futures instead of PE. Heh.

EndOfTheWorld

RE Brexit, I’d like to quote Bob Moriarty of 321gold: “First of all Brexit is not the disease, it’s a symptom. The EU is utterly dysfunctional. There are 12,643 laws regarding milk. There are 50 pages of documents telling you how much water to use in the toilet to flush it.” Etc. His book with the catchy title “Nobody Knows Anything” went to #1 in its category on Amazon. I think I’m going to have to break down and buy it.

makedoanmend

Yeah it was regulation wot done it for us working poor, unemployed, zero hour contractual labour, the part-timer jobbers, underemployed, the food kitchen eaters etc. etc. etc. They was making us eat straight bananas. (Daily Mail fodder). This was wot made our minds up gov’ner. We voted against regulations. Regulation makes our lives hell.

It wasn’t that a tiny elite by-passed all democractic channels in the EU to dictate how our societies should operate, and the tiny elites of the bloc nations made sure to install every neo-liberal docrine to ensure the commodification of every facit of life.

Who needs them stinking regulations, safety rules and oversite of the elite and their corporate clients? We’re ready to sacrifice our health, limbs, lives and the environment so that few may prosper.

Free the corporations and we free ourselves.

We’ll all march behind the corporate Logo. Hold those flags high comrades!

EndOfTheWorld

The next line in the interview of Moriarty is: “The EU is a bunch of unelected bureaucrats, nobody knows who they are. They weren’t elected and they are not responsible.” Check it out—321gold. But you gotta admit that’s a lot of laws about milk.

beene

The reason for the length of laws is too give everyone the opportunity to avoid compliance.

James Kroeger

The world is undergoing a secular deleveraging…

Yes, all else equal, a steady period of deleveraging will not only retard growth, but will eventually turn growth negative. As you’ve correctly point out, given the clutch of assumptions that orthodox forecasters typically embrace, the only possible justification for their optimism is some kind of private sector miracle sustained by the Confidence Fairy.

There is, of course, a way to achieve/maintain strong economic growth even while levels of total indebtedness are unwinding, but it is one that the financial services industry does not ever want to talk about, for it threatens that industry’s future profitability. (And no, I’m not talking MMT.)

It is quite simple, really. Contrary to conventional wisdom, increasing tax rates always produces a net economic stimulus, all else equal. This is because at least some of the money that the government collects and spendswould have been removed from the economy by savers and that necessarily creates a net increase in aggregate spending, all else equal (the increase in G > decrease in C)

Of course, the more a tax increase falls upon the economy’s biggest savers, the bigger the economic stimulus gained.

Wall Street bankers will tell you, of course, that the money savers remove from the economy all gets spent on worthy economic investments, but that simply isn’t true. There is always a net leakage of money from the economy when savings occur (rather obvious when there is a reserve requirement). Almost none of the money that is lent to financial corporations ends up being used on economic investments in the real economy.

In spite of these rather obvious macroeconomic truths, almost all of the economic textbooks used in American schools today teach students that tax hikes are contractionary and that tax cuts—in and of themselves—are expansionary.

Precisely the opposite it true.

But because this misrepresentation of the effects of changes in income tax rates is so widely regarded as the truth, millions of the Main Street economy’s participants will suffer needlessly for years to come (EU austerity, Fed orchestrated recessions). So sad…

Jim Haygood

Savings = Investment

Reduce savings, reduce investment.

Short run, spending can offer a boost. Long run, spending instead of saving is a path to destruction.

Ignacio

In stupid times, savings of the few = stupid looser investments

Without spending there are not good investments opportunities

Skippy

IS-LM really Haygood… never knew you were with Krugman…

Disheveled Marsupial… don’t confuse scripture with reality… M’Kay

jsn

I think it’s pretty clear at the moment that savings=mal-investment.

If its not increasing future real productivity, its not a real investment: most of what’s going on now under the rubric of investment is looting and asset stripping.

Taxing the funds that finance that activity and spending the proceeds on infrastructure and de-crapification of public goods in general would constitute a real investment in real future productivity growth.

James Kroeger

Actually the accounting identity Savings = Investment has little to do with the real economy. In reality real economic investments are only a small fraction of total savings.

Part of the misunderstanding is due to the intentional efforts Wall Street makes to conflate financial investments with real economic investments.

Economic investments—the kind that actually end up improving the economic welfare of a population—involve purchases of capital goods or other economic resources that are used to either produce more capital goods or more final goods that consumers find desirable. In other words, they either increase output or expand the supply-side’s productive capacity. This happens whenever firms purchase machinery/equipment to improve productive efficiency or when they spend money on the construction of new stores or factories or on the salaries of new employees. However, not all firm expenditures are economic investments, e.g., money spent by firms on advertising that either (a) misleads consumers or (b) does nothing to help them with their purchasing decisions.

Financial investments—are purchases or commitments of money that provide the “investor” with an income stream. Saving money is a financial investment because it provides interest income; purchases of assets can be financial investments if they eventually provide a capital gain. Economic investments made by firms are usually also financial investments because they generate income that exceeds their cost. The economic investments made by governments that improve infrastructure or human capital are not financial investments because they do not provide the government with an income stream.

Some financial investments are also economic investments, but many of them are not. The purchase of a piece of land, for example, is a financial investment if it appreciates in value over time, but it is not an economic investment if it just sits there, undeveloped. Purchases of stocks in secondary markets (e.g., NYSE, NASDAQ) are clearly financial investments if the stocks appreciate in value, but they are not economic investments because they involve nothing more than exchanges of titles of ownership of already existing assets. They do not typically put any money into the hands of firm managers that could be used for economic investments. That normally happens only when stocks are first sold to underwriters, prior to an initial public offering.

*Sigh* When I first started blogging, you could find the empirical studies (from the 1970s and earlier) on Google pretty readily. But it’s now so widely accepted plus Google has become so crapified that I can’t locate them.

You will instead have to rely on the Bank of England telling you that’s how it works:

Conventional apples: raise taxes with all else being equal. Deficit reduced. Net consumption spending reduced.

Posited oranges: raise taxes and spend the increment. Deficit unchanged. Net consumption spending increased as argued.

Different situations. There is no conflict here. One being true does not prove the other false.

Detroit Dan

Thank you. I was hoping the Kroeger correction would be done by someone else. And your response is concise and to the point!

Synoia

some kind of private sector miracle sustained by the Confidence Fairy.

I’m sorry, the Confidence Fairy has joined a cult. This is now the appropriate use of the name:

some kind of private sector miracle sustained by the Confidence Fury.

MikeNY

But we all still need to believe in the GROAF fairy, who magically solves all economic problems. It’s the only way to keep every Croesus comfortably perched on his pile of pelf.

SteveB

Increase tax rates much more and I will shut down my small business and just go fishing.

Not a political statement…. just a fact of diminishing returns.. simply not worth the effort…

Already have the plan in place… will sell the technology and equipment to each customer in exchange for payment based on their payback period… Everyone wins except my employees……

James Kroeger

Increase tax rates much more and I will shut down my small business and just go fishing.

What taxes are you concerned about? Corporate income taxes? Or the personal income tax?

Higher marginal rates at the top end would still guarantee you a healthy disposable income up to a certain point; it’s only the ‘extra profit’ that would be taxed.

So in spite of the fact that higher marginal tax rates on your taxable income would still leave your business profitable, you would shut it down because you would be so disappointed that you wouldn’t be able to keep those last marginal dollars/euros/pounds that you believe you are entitled to?

Then by all means shut it down if things unfold as you fear. I’m sure that your current competitors would be happy to pick up your market share…

Arizona Slim

Not just the current competition. There are future competitors as well.

reslez

And yet megacorps somehow get away with paying nothing (or near nothing) in taxes.

Arizona Slim

OTOH, small business can’t get away with that. Which is why the business owner who’s threatening to close and go fishing has a point.

James Kroeger

Which is why the business owner who’s threatening to close and go fishing has a point.

Well, it’s a point, but it’s not a point that any policy maker should take seriously.

Any business owner who sells out because she doesn’t feel she is making enough after tax profits is certainly free to do so.

But policy makers need to be aware that when a firm goes out of business for any reason, its market share will simply be picked up by those firms in that industry that stay in the game.

That is why the industry as a whole will not suffer any loss of demand for what the closed business used to sell. And that means that total employment within the industry will remain roughly the same.

Displaced workers will either be rehired within the industry, or replaced by others who will do essentially the same jobs.

It should be noted that a sufficient number of businesses owners stayed in the game in the 1940’s and 1950’s and 1960’s to make it one of the most prosperous eras in our economic history in spite of the fact that they were all paying much higher taxes on the income they derived from their businesses.

The historical evidence suggests that whenever business owners threaten to close shop if their top marginal tax rates are set too high, it can be dismissed as empty rhetoric that shouldn’t be taken seriously.

They will still have profitable enterprises and they will still maintain their positions at the top of the economic ladder.

They won’t like having to pay higher amounts in taxes, but they will, and they’ll get used to it. Industry as a whole will not suffer at all, and will probably benefit from the improvements in infrastructure and aggregate demand.

SteveB

I once had this same discussion with someone who argued vigorously, (similarly to you)

including the old “taxes are the price for civilization” line…

It got quite heated and finally I asked one question he was hard pressed to answer..

If paying taxes is so noble and good, why do you cheat on your 1040?

I’m not asking for an answer here… Just think about it..

=================================================

Didn’t mean to post an run this AM.. I was in a truck picking up parts from a vendor in the next state and then delivering them to another for processing. then headed back to shop to make shipment to customers… So I can pay my taxes..

James Kroeger

If paying taxes is so noble and good, why do you cheat on your 1040?

I don’t….I suppose because I believe it is so noble and good? :)

Stein

You say that if he sells his business, others might pick it up.

Perhaps. But the others won’t be the same as the seller.

If higher taxes squeeze out small business and keep only the bigger companies competitive, then increasing tax will squeeze out small business and your economy will be reduced to Bluechips. That’s only “if” of course.

Also, I would disagree as to the “either way, everyone has a job.” Small business is not the same type of employer as big business. Especially in a scenario where there are fewer small businesses. (Again: “if”: I don’t know if the reverse is possible, but it’s imaginable: big companies leave due to high taxes, so only small business remains, but they jack up prices to maintain healthy profits. “If.”)

I’m not against taxing personally, but I’d be for taxing the big companies. Never understood why companies have a fixed rate and individuals have a progressive tax. How are they different? That’s mostly irrelevant though, as the much more pressing concern is collecting taxes of international companies that have all their profits in Ireland, even though all their factories are in Germany and France. Efforts are being done on that level already and I hope to see it within 5 years. That will be a global fiscal network for a global world. And we will finally have some fiscal justice.

Then again, I’m not really qualified and read stuff here out of curiosity more than anything else.

Being in business for yourself is one of the last tax shelters. You can run a lot of personal expenses through the business.

jsn

Taxes should be collected on activities that would benefit society by being discouraged. Finance, pharma and big ag as currently practiced fit the bill. Instead, we tax things we claim to appreciate like working people and small business: there is so little money left here the IRS is struggling to collect.

Tax idle wealth.

James Kroeger

Tax idle wealth.

Indeed. Which is why I’m not opposed to reducing corporate income taxes at the same time that I am championing an increase in other taxes:

A ‘sales tax’ on all Wall Street financial transactions would be a good start.

Eliminating the special treatment of capital gains income should be another top priority.

A significant boost in the top marginal rates that the top 1%-5% must pay would also be a good idea.

With the bundle of revenue that these fiscal policy changes would generate, the economy would be able to weather a period of significant de-leveraging with something close to full employment.

Adam1

“…so why do these folk keep upgrading growth outlooks as if some wonderful private sector virtuous cycle will magically appear?”

Because, sadly, that’s exactly what they believe in and what their models generate. Absent an external shock this is how DSGE economic models work.

grizziz

Secular usage in economics; every time that word appears or is spoken is an admission that whatever it is modifying, i.e., stagnation or deleveraging, is part of an attempted explanation which is outside the realm of the high priests of economics. It is an admission that writer does not have a theoretical framework in which to ground the phenomenon. It is rhetorical window dressing to allow writers in the economic canon or orators speaking to the lay to retain their vestments without admitting to their confusion and well, looking silly.

Steve H.

This is going to be a fun thread.

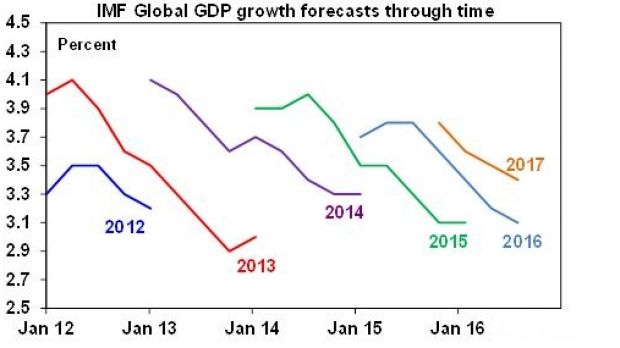

: I don’t understand that chart, and following the links leads to nothing. That can’t be real data, since the overlapping years are non-functional. ?.

: James & Jim, well yes you are talking monetary theory, since dollar savings come from spending, but savings as in held cash is not investment.

: End & mend, solve for x^2 = n; some questions have more than one answer. How is it possible you are both right?

: To the post itself: cannot the Magical Money Wand of Fiat overcome the flightiness of the Confidence Fairy? Theoretically at least, as long as money is created to goose stock prices then nest eggs can keep ‘growing’.

: It’s not a wealth problem, it’s a distribution problem. Both for wealth (sequestering of decision process leading to greater inequality, so GDP becomes virtually meaningless), and for energy. By which I mean, we don’t have an energy problem in the long run, we have a heat-dumping problem. Steve Keen touched on this but I can’t find the post.

: There is a deep kernel concerning time delays. The use of the tally stick was to allow commerce to occur before the ship/harvest came in. Time delays are a source of complex behavior in ecological systems. HFT seems destablizing, too-high r causes chaos in the Verhulst equation, and Taleb on signal-noise indicates that seeking stimuli too quickly leads to disorientation. Herrnstein found that without a time-delay, there was no weighing of potential rewards, just simple switching between behaviors.

: Play nice, kids. Remember to have fun here.

Detroit Dan

I believe the charts show the evolution of forecasted GDP for a given year over time. For example, the January 2012 forecast for global GDP growth in 2013 was 4%. When the final results were in at the beginning of 2014, the 2013 growth turned out to be about 3%.

Steve H.

Thank you, Detroit Dan. That was enough for me to then dig this up:

The projections in Table 1 match in the way you explain.

The trend looks to me like they’ll start getting it right around 2032…

NeqNeq

The world is undergoing a secular deleveraging coupled with a demographic accident that has years, probably decades, to run.

Is this a true statement? Last I heard there was little to no global deleveraging during the 2012 – 2015 period.

The 2015 McKinsey Debt report shows only the US, UK, Ireland, and Spain having any personal deleveraging (and it wasn’t that large). Links here at NC point to an increase in personal debt in the most recent times. Additionally, it appears corporate debt has been going up fueled by cheap rates. So even when we ignore that there is an entire world outside of the above 4 countries, it seems like the deleveraging evidence is….spotty at best.

Are there better sources which show the globe deleveraging post 2007?

A big part of the rise in corporate debt in the US has not been to invest but to buy back shares. So all they’ve done is rearrange the balance sheet. That means by not adding to new spending, it does not add to or subtract from the “deleveraging” picture.

And you still have classic balance sheet recession dynamics at play. As Steve Keen points out:

Why have interest rates remained low since? Because the reason economic growth is so anaemic (for what is supposed to be a recovery) is that high debt levels means reduced willingness to take on new debt, and hence a suppressed level of credit-driven demand. Even though credit growth is positive again—after being negative between 2009 and 2012—it is still a smaller percentage of GDP than at any time since 1994 (see Figure 1 again).

Hmm. It seems to me that the argument needs to be fleshed out more.

If, as you say, corp debt used for buy backs does not matter (either adding or subtracting), then we can ignore a big part of the debt. The small part that was not used for buy backs still matters. There is still a net positive gain, even if that gain is fairly small.* So, if corp debt and personal debt is growing (lets ignore government debt) then in what sense is ‘deleveraging’ a factually correct term?

Maybe Llewellyn is using the term for rhetorical flourish and not in a technical sense. In that case, we can interpret him through Keen’s quote. Net, there is an increase, but the small size of the net increase indicates that many people are still not increasing their existing debt loads regardless of the price of credit. Then his view is that people are not making as many purchases on credit anymore and, therefore, low rates wont help.

But if that is his view it undermines his other statement that the only thing keeping the wagon in the track is the low rates being used to stimulate growth. If debt-growth is not effected by price, then low rates can’t be seen as the factor keeping the cycle going.

It seems like Llewellyn needs the ‘deleveraging’ term to be true in a technical sense for his other statements to be internally coherent. On the whole, then, interpreting him along Keen’s line isnt going to work. If that is correct, then his post really turns on evidence for an ongoing decrease in debt on the global scale (imo… others mileage could vary).

*Also consider that debt for share buy backs, given that it requires a firm to be public, is a subset of total global business debt. I do not recall the values for the larger picture of firm debt, but (iirc) its in the McKinsey reports.

Sound of the Suburbs

It is the knowledge that is hidden that confuses everyone, the very nature of money itself.

Money is created when banks make loans and is destroyed when the repayments are made.

They said debt doesn’t matter, but it does, especially when banks extend credit into asset bubbles.

Debt inflated asset bubbles:

1929 – US (margin lending into US stocks)

1989 – Japan (real estate)

2008 – US (real estate bubble leveraged up with derivatives for global contagion)

2010 – Ireland (real estate)

2012 – Spain (real estate)

When they burst there is hell to pay.

Japan has had twenty five years in the balance sheet recessions that follow:

Richard Koo tells you what they learnt, fiscal stimulus is necessary to get you through them to stop the money supply contracting.

Ideologically, it was a bit of a nuisance finding we need Government spending and so QE was the big cover up, it doesn’t work because no one is borrowing and so the money never hits the real economy. Hence the low inflation in the US, Japan and Europe.

Austerity is the worst thing you can do and Ben Bernanke had read Richard Koo’s book and ensured the US Government kept spending. He didn’t tell anyone else killing Greece and damaging the other Club-Med nations.

Reckless US bank lending killed the global economy twice, 1929 and 2008.

As soon as they were free from the 1930s legislation, they did it again.

The world is in a balance sheet recession after 2008 and QE isn’t going to help.

The country that did no austerity is in the best shape, the US.

Knute Rife

Our alternatives have now boiled down to Classical despotism with an international economy or Medieval feudalism with local economies. Woo hoo!

Might have something to do with that spreading Democracy [neoliberal markets – globalism] had nothing to do with uplift in the first bloody place…. its one and only priority was increasing the customer… cough… consumer base so corporatists could increase revenue… cough… remuneration multipliers e.g. bonuses et al…

Disheveled Marsupial…. like the old sales joke…. but boss New Zealanders don’t ware shoes…. yeah kid… think how many we will sell…. first in best dressed my young Padawan…

PS… later in the story the poor NZ’ers have to turn their country into a tax haven – sell it off so they can import the cheap shoes… whilst the sales Sith lord muses about where to retire with his winnings…

I’d dreadfully sorry about your …… condition. Does it hurt much? Or was it an accident at childbirth?

I prescribe a course, or two, of complete sentences.

How about two words…. Powell Memo…

Disheveled Marsupial…whilst were at it, it should be noted that productivity has very little to do with most people… ask Rubin…

Skippy might benefit from a course of soluble fiber and roughage. 10 days of Benefiber(TM) every morning, and pysillium husk capsules each night would add bulk to his stream of consciousness…………. and improve its consistency.

Skippy might have benefited from never having to deal with Austrians or neoclassical’s nor the people that confuse numerology with history….

Now you have Eight People Sipping Wine in Kettering and calling it an election

CEO compensation grew faster than the wages of the top 0.1 percent and the stock market

Economic Snapshot • By Lawrence Mishel and Jessica Schieder • July 13, 2016

CEO compensation in the largest firms dipped temporarily in 2015 and remains 940.9 percent above its 1978 level. This growth in CEO compensation far exceeded the growth of the stock market, which grew forty-two percent less (up 542.9 percent). This shows that executives have done far better than the firms they have led and executive pay cannot be simply attributed to better firm performance. Neither can the spectacular rise in CEO compensation be attributed to the ‘market for talent’ providing more rewards for those at the top. The wages of the top 0.1 percent of wage earners (top one out of a thousand) is a decent proxy for the pay of the most financially successful and grew a remarkable 320.5 percent from 1978 to 2014 (the last year for which data are available). Yet, CEO compensation grew roughly three times faster than the wages of the top 0.1 percent. The fact that CEO compensation grew so much faster than the pay of other very highly-paid earners, and far faster than stock prices, indicates that unique dynamics are at play and that corporate governance is not adequately restraining executive pay. – go to epi.org

Don’t even get me started on the studies that show CEO et al pay is not correlated to performance… outside some industry fashion… ripping yarns of Al Dunlap and Perelman thingy…

But yeah deleveraging….

Disheveled Marsupial…. 27C here in wintry Brisbane

CalPERS should invest in CEO futures instead of PE. Heh.

RE Brexit, I’d like to quote Bob Moriarty of 321gold: “First of all Brexit is not the disease, it’s a symptom. The EU is utterly dysfunctional. There are 12,643 laws regarding milk. There are 50 pages of documents telling you how much water to use in the toilet to flush it.” Etc. His book with the catchy title “Nobody Knows Anything” went to #1 in its category on Amazon. I think I’m going to have to break down and buy it.

Yeah it was regulation wot done it for us working poor, unemployed, zero hour contractual labour, the part-timer jobbers, underemployed, the food kitchen eaters etc. etc. etc. They was making us eat straight bananas. (Daily Mail fodder). This was wot made our minds up gov’ner. We voted against regulations. Regulation makes our lives hell.

It wasn’t that a tiny elite by-passed all democractic channels in the EU to dictate how our societies should operate, and the tiny elites of the bloc nations made sure to install every neo-liberal docrine to ensure the commodification of every facit of life.

Who needs them stinking regulations, safety rules and oversite of the elite and their corporate clients? We’re ready to sacrifice our health, limbs, lives and the environment so that few may prosper.

Free the corporations and we free ourselves.

We’ll all march behind the corporate Logo. Hold those flags high comrades!

The next line in the interview of Moriarty is: “The EU is a bunch of unelected bureaucrats, nobody knows who they are. They weren’t elected and they are not responsible.” Check it out—321gold. But you gotta admit that’s a lot of laws about milk.

The reason for the length of laws is too give everyone the opportunity to avoid compliance.

Yes, all else equal, a steady period of deleveraging will not only retard growth, but will eventually turn growth negative. As you’ve correctly point out, given the clutch of assumptions that orthodox forecasters typically embrace, the only possible justification for their optimism is some kind of private sector miracle sustained by the Confidence Fairy.

There is, of course, a way to achieve/maintain strong economic growth even while levels of total indebtedness are unwinding, but it is one that the financial services industry does not ever want to talk about, for it threatens that industry’s future profitability. (And no, I’m not talking MMT.)

It is quite simple, really. Contrary to conventional wisdom, increasing tax rates always produces a net economic stimulus, all else equal. This is because at least some of the money that the government collects and spends would have been removed from the economy by savers and that necessarily creates a net increase in aggregate spending, all else equal (the increase in G > decrease in C)

Of course, the more a tax increase falls upon the economy’s biggest savers, the bigger the economic stimulus gained.

Wall Street bankers will tell you, of course, that the money savers remove from the economy all gets spent on worthy economic investments, but that simply isn’t true. There is always a net leakage of money from the economy when savings occur (rather obvious when there is a reserve requirement). Almost none of the money that is lent to financial corporations ends up being used on economic investments in the real economy.

In spite of these rather obvious macroeconomic truths, almost all of the economic textbooks used in American schools today teach students that tax hikes are contractionary and that tax cuts—in and of themselves—are expansionary.

Precisely the opposite it true.

But because this misrepresentation of the effects of changes in income tax rates is so widely regarded as the truth, millions of the Main Street economy’s participants will suffer needlessly for years to come (EU austerity, Fed orchestrated recessions). So sad…

Savings = Investment

Reduce savings, reduce investment.

Short run, spending can offer a boost. Long run, spending instead of saving is a path to destruction.

In stupid times, savings of the few = stupid looser investments

Without spending there are not good investments opportunities

IS-LM really Haygood… never knew you were with Krugman…

Disheveled Marsupial… don’t confuse scripture with reality… M’Kay

I think it’s pretty clear at the moment that savings=mal-investment.

If its not increasing future real productivity, its not a real investment: most of what’s going on now under the rubric of investment is looting and asset stripping.

Taxing the funds that finance that activity and spending the proceeds on infrastructure and de-crapification of public goods in general would constitute a real investment in real future productivity growth.

Actually the accounting identity Savings = Investment has little to do with the real economy. In reality real economic investments are only a small fraction of total savings.

Part of the misunderstanding is due to the intentional efforts Wall Street makes to conflate financial investments with real economic investments.

The difference between financial investments and real economic investments:

Economic investments—the kind that actually end up improving the economic welfare of a population—involve purchases of capital goods or other economic resources that are used to either produce more capital goods or more final goods that consumers find desirable. In other words, they either increase output or expand the supply-side’s productive capacity. This happens whenever firms purchase machinery/equipment to improve productive efficiency or when they spend money on the construction of new stores or factories or on the salaries of new employees. However, not all firm expenditures are economic investments, e.g., money spent by firms on advertising that either (a) misleads consumers or (b) does nothing to help them with their purchasing decisions.

Financial investments—are purchases or commitments of money that provide the “investor” with an income stream. Saving money is a financial investment because it provides interest income; purchases of assets can be financial investments if they eventually provide a capital gain. Economic investments made by firms are usually also financial investments because they generate income that exceeds their cost. The economic investments made by governments that improve infrastructure or human capital are not financial investments because they do not provide the government with an income stream.

Some financial investments are also economic investments, but many of them are not. The purchase of a piece of land, for example, is a financial investment if it appreciates in value over time, but it is not an economic investment if it just sits there, undeveloped. Purchases of stocks in secondary markets (e.g., NYSE, NASDAQ) are clearly financial investments if the stocks appreciate in value, but they are not economic investments because they involve nothing more than exchanges of titles of ownership of already existing assets. They do not typically put any money into the hands of firm managers that could be used for economic investments. That normally happens only when stocks are first sold to underwriters, prior to an initial public offering.

That’s the loanable funds theory, and it was debunked decades ago by Keynes and Kaldor.

Banks can lend without having deposits to “fund” them. Their loans create new deposits. This has been verified empirically by the Post-Keynesiasns.

Empirically?! Where? Link please :)

*Sigh* When I first started blogging, you could find the empirical studies (from the 1970s and earlier) on Google pretty readily. But it’s now so widely accepted plus Google has become so crapified that I can’t locate them.

You will instead have to rely on the Bank of England telling you that’s how it works:

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

As well as this post, that explain operationally why it has to work that way:

http://neweconomicperspectives.org/2012/04/krugmans-flashing-neon-sign.html

This is a bibliography with the key papers:

http://socialdemocracy21stcentury.blogspot.ie/2012/04/endogenous-money-bibliography.html

Apples vs oranges.

Conventional apples: raise taxes with all else being equal. Deficit reduced. Net consumption spending reduced.

Posited oranges: raise taxes and spend the increment. Deficit unchanged. Net consumption spending increased as argued.

Different situations. There is no conflict here. One being true does not prove the other false.

Thank you. I was hoping the Kroeger correction would be done by someone else. And your response is concise and to the point!

I’m sorry, the Confidence Fairy has joined a cult. This is now the appropriate use of the name:

But we all still need to believe in the GROAF fairy, who magically solves all economic problems. It’s the only way to keep every Croesus comfortably perched on his pile of pelf.

Increase tax rates much more and I will shut down my small business and just go fishing.

Not a political statement…. just a fact of diminishing returns.. simply not worth the effort…

Already have the plan in place… will sell the technology and equipment to each customer in exchange for payment based on their payback period… Everyone wins except my employees……

What taxes are you concerned about? Corporate income taxes? Or the personal income tax?

Higher marginal rates at the top end would still guarantee you a healthy disposable income up to a certain point; it’s only the ‘extra profit’ that would be taxed.

So in spite of the fact that higher marginal tax rates on your taxable income would still leave your business profitable, you would shut it down because you would be so disappointed that you wouldn’t be able to keep those last marginal dollars/euros/pounds that you believe you are entitled to?

Then by all means shut it down if things unfold as you fear. I’m sure that your current competitors would be happy to pick up your market share…

Not just the current competition. There are future competitors as well.

And yet megacorps somehow get away with paying nothing (or near nothing) in taxes.

OTOH, small business can’t get away with that. Which is why the business owner who’s threatening to close and go fishing has a point.

Well, it’s a point, but it’s not a point that any policy maker should take seriously.

Any business owner who sells out because she doesn’t feel she is making enough after tax profits is certainly free to do so.

But policy makers need to be aware that when a firm goes out of business for any reason, its market share will simply be picked up by those firms in that industry that stay in the game.

That is why the industry as a whole will not suffer any loss of demand for what the closed business used to sell. And that means that total employment within the industry will remain roughly the same.

Displaced workers will either be rehired within the industry, or replaced by others who will do essentially the same jobs.

It should be noted that a sufficient number of businesses owners stayed in the game in the 1940’s and 1950’s and 1960’s to make it one of the most prosperous eras in our economic history in spite of the fact that they were all paying much higher taxes on the income they derived from their businesses.

The historical evidence suggests that whenever business owners threaten to close shop if their top marginal tax rates are set too high, it can be dismissed as empty rhetoric that shouldn’t be taken seriously.

They will still have profitable enterprises and they will still maintain their positions at the top of the economic ladder.

They won’t like having to pay higher amounts in taxes, but they will, and they’ll get used to it. Industry as a whole will not suffer at all, and will probably benefit from the improvements in infrastructure and aggregate demand.

I once had this same discussion with someone who argued vigorously, (similarly to you)

including the old “taxes are the price for civilization” line…

It got quite heated and finally I asked one question he was hard pressed to answer..

If paying taxes is so noble and good, why do you cheat on your 1040?

I’m not asking for an answer here… Just think about it..

=================================================

Didn’t mean to post an run this AM.. I was in a truck picking up parts from a vendor in the next state and then delivering them to another for processing. then headed back to shop to make shipment to customers… So I can pay my taxes..

I don’t….I suppose because I believe it is so noble and good? :)

You say that if he sells his business, others might pick it up.

Perhaps. But the others won’t be the same as the seller.

If higher taxes squeeze out small business and keep only the bigger companies competitive, then increasing tax will squeeze out small business and your economy will be reduced to Bluechips. That’s only “if” of course.

Also, I would disagree as to the “either way, everyone has a job.” Small business is not the same type of employer as big business. Especially in a scenario where there are fewer small businesses. (Again: “if”: I don’t know if the reverse is possible, but it’s imaginable: big companies leave due to high taxes, so only small business remains, but they jack up prices to maintain healthy profits. “If.”)

I’m not against taxing personally, but I’d be for taxing the big companies. Never understood why companies have a fixed rate and individuals have a progressive tax. How are they different? That’s mostly irrelevant though, as the much more pressing concern is collecting taxes of international companies that have all their profits in Ireland, even though all their factories are in Germany and France. Efforts are being done on that level already and I hope to see it within 5 years. That will be a global fiscal network for a global world. And we will finally have some fiscal justice.

Then again, I’m not really qualified and read stuff here out of curiosity more than anything else.

Being in business for yourself is one of the last tax shelters. You can run a lot of personal expenses through the business.

Taxes should be collected on activities that would benefit society by being discouraged. Finance, pharma and big ag as currently practiced fit the bill. Instead, we tax things we claim to appreciate like working people and small business: there is so little money left here the IRS is struggling to collect.

Tax idle wealth.

Indeed. Which is why I’m not opposed to reducing corporate income taxes at the same time that I am championing an increase in other taxes:

A ‘sales tax’ on all Wall Street financial transactions would be a good start.

Eliminating the special treatment of capital gains income should be another top priority.

A significant boost in the top marginal rates that the top 1%-5% must pay would also be a good idea.

With the bundle of revenue that these fiscal policy changes would generate, the economy would be able to weather a period of significant de-leveraging with something close to full employment.

“…so why do these folk keep upgrading growth outlooks as if some wonderful private sector virtuous cycle will magically appear?”

Because, sadly, that’s exactly what they believe in and what their models generate. Absent an external shock this is how DSGE economic models work.

Secular usage in economics; every time that word appears or is spoken is an admission that whatever it is modifying, i.e., stagnation or deleveraging, is part of an attempted explanation which is outside the realm of the high priests of economics. It is an admission that writer does not have a theoretical framework in which to ground the phenomenon. It is rhetorical window dressing to allow writers in the economic canon or orators speaking to the lay to retain their vestments without admitting to their confusion and well, looking silly.

This is going to be a fun thread.

: I don’t understand that chart, and following the links leads to nothing. That can’t be real data, since the overlapping years are non-functional. ?.

: James & Jim, well yes you are talking monetary theory, since dollar savings come from spending, but savings as in held cash is not investment.

: End & mend, solve for x^2 = n; some questions have more than one answer. How is it possible you are both right?

: To the post itself: cannot the Magical Money Wand of Fiat overcome the flightiness of the Confidence Fairy? Theoretically at least, as long as money is created to goose stock prices then nest eggs can keep ‘growing’.

: It’s not a wealth problem, it’s a distribution problem. Both for wealth (sequestering of decision process leading to greater inequality, so GDP becomes virtually meaningless), and for energy. By which I mean, we don’t have an energy problem in the long run, we have a heat-dumping problem. Steve Keen touched on this but I can’t find the post.

: There is a deep kernel concerning time delays. The use of the tally stick was to allow commerce to occur before the ship/harvest came in. Time delays are a source of complex behavior in ecological systems. HFT seems destablizing, too-high r causes chaos in the Verhulst equation, and Taleb on signal-noise indicates that seeking stimuli too quickly leads to disorientation. Herrnstein found that without a time-delay, there was no weighing of potential rewards, just simple switching between behaviors.

: Play nice, kids. Remember to have fun here.

I believe the charts show the evolution of forecasted GDP for a given year over time. For example, the January 2012 forecast for global GDP growth in 2013 was 4%. When the final results were in at the beginning of 2014, the 2013 growth turned out to be about 3%.

Thank you, Detroit Dan. That was enough for me to then dig this up:

http://www.imf.org/external/pubs/ft/weo/2013/update/01/

The projections in Table 1 match in the way you explain.

The trend looks to me like they’ll start getting it right around 2032…

Is this a true statement? Last I heard there was little to no global deleveraging during the 2012 – 2015 period.

The 2015 McKinsey Debt report shows only the US, UK, Ireland, and Spain having any personal deleveraging (and it wasn’t that large). Links here at NC point to an increase in personal debt in the most recent times. Additionally, it appears corporate debt has been going up fueled by cheap rates. So even when we ignore that there is an entire world outside of the above 4 countries, it seems like the deleveraging evidence is….spotty at best.

Are there better sources which show the globe deleveraging post 2007?

A big part of the rise in corporate debt in the US has not been to invest but to buy back shares. So all they’ve done is rearrange the balance sheet. That means by not adding to new spending, it does not add to or subtract from the “deleveraging” picture.

And you still have classic balance sheet recession dynamics at play. As Steve Keen points out:

http://www.forbes.com/sites/stevekeen/2015/10/28/the-unnatural-rate-of-interest-ultra-wonkish/3/#7beeb9382647

Hmm. It seems to me that the argument needs to be fleshed out more.

If, as you say, corp debt used for buy backs does not matter (either adding or subtracting), then we can ignore a big part of the debt. The small part that was not used for buy backs still matters. There is still a net positive gain, even if that gain is fairly small.* So, if corp debt and personal debt is growing (lets ignore government debt) then in what sense is ‘deleveraging’ a factually correct term?

Maybe Llewellyn is using the term for rhetorical flourish and not in a technical sense. In that case, we can interpret him through Keen’s quote. Net, there is an increase, but the small size of the net increase indicates that many people are still not increasing their existing debt loads regardless of the price of credit. Then his view is that people are not making as many purchases on credit anymore and, therefore, low rates wont help.

But if that is his view it undermines his other statement that the only thing keeping the wagon in the track is the low rates being used to stimulate growth. If debt-growth is not effected by price, then low rates can’t be seen as the factor keeping the cycle going.

It seems like Llewellyn needs the ‘deleveraging’ term to be true in a technical sense for his other statements to be internally coherent. On the whole, then, interpreting him along Keen’s line isnt going to work. If that is correct, then his post really turns on evidence for an ongoing decrease in debt on the global scale (imo… others mileage could vary).

*Also consider that debt for share buy backs, given that it requires a firm to be public, is a subset of total global business debt. I do not recall the values for the larger picture of firm debt, but (iirc) its in the McKinsey reports.

It is the knowledge that is hidden that confuses everyone, the very nature of money itself.

Money is created when banks make loans and is destroyed when the repayments are made.

A very good video primer:

https://www.hiddensecretsofmoney.com/videos/episode-4

They said debt doesn’t matter, but it does, especially when banks extend credit into asset bubbles.

Debt inflated asset bubbles:

1929 – US (margin lending into US stocks)

1989 – Japan (real estate)

2008 – US (real estate bubble leveraged up with derivatives for global contagion)

2010 – Ireland (real estate)

2012 – Spain (real estate)

When they burst there is hell to pay.

Japan has had twenty five years in the balance sheet recessions that follow:

https://www.youtube.com/watch?v=8YTyJzmiHGk

Richard Koo tells you what they learnt, fiscal stimulus is necessary to get you through them to stop the money supply contracting.

Ideologically, it was a bit of a nuisance finding we need Government spending and so QE was the big cover up, it doesn’t work because no one is borrowing and so the money never hits the real economy. Hence the low inflation in the US, Japan and Europe.

Austerity is the worst thing you can do and Ben Bernanke had read Richard Koo’s book and ensured the US Government kept spending. He didn’t tell anyone else killing Greece and damaging the other Club-Med nations.

Reckless US bank lending killed the global economy twice, 1929 and 2008.

As soon as they were free from the 1930s legislation, they did it again.

The world is in a balance sheet recession after 2008 and QE isn’t going to help.

The country that did no austerity is in the best shape, the US.

Our alternatives have now boiled down to Classical despotism with an international economy or Medieval feudalism with local economies. Woo hoo!

I’ll take Medieval Feudalism for 10, please Alex.

I thought national savings was unused resources…