Having made a few back-of-the-envelope calculations in this blog, and then having had readers jump on me, I know what fraught exercises they are. But at the same time, a lot of information is bandied about, and you can learn a lot by connecting the dots (although sometimes what you learn is that you didn’t connect them correctly but even that is educational). So I sympathize with those who advance the discussion by sticking their neck out a bit.

Ken Houghton at Marginal Utility works through the data to see to what degree the projected foreclosures may have already been counted in Wall Street and banking industry writedowns. Unfortunately, he makes several erroneous assumptions, namely, that the writedowns relate solely to actual or expected subprime foreclosures; that these supbrime losses will show up only at banks or securities firms; and that the writedowns correspond to the loss in fundamental value of the underlying assets.

Houghton was good enough to admit that he wasn’t certain as to his analysis and asked for input, so forgive me if I am making it sound as if he regarded his calculation as definitive.

Let’s start with his analysis:

There is a projection of 2 million (2E6) bankruptcies in the mortgage market over the next few years. Since most of those seem to be described as “subprime,” it is reasonable to assume that they will mostly be non-Jumbo, Fannie/Freddie-eligible mortgages. That currently means their value (of the mortgage that is, not the house) is capped at $417,000. (4.17E5).

Now 4.17 x 2 = 8.34, so we are talking—absolute worst case—$8.34E11, or $834 billion. And that’s if the home and the land are all worth zero, everyone took a maximum mortgage, and all two million bankruptcies happen. Over the next several years.

I think we can agree that the above should be the worst-case scenario. (Even if the properties are all on Lon Gisland, that should still leave at least 50% of the value intact.)

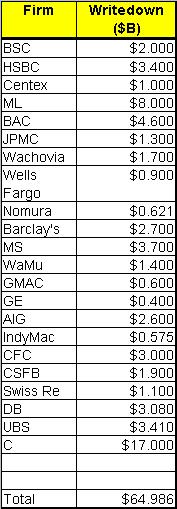

Now, it’s entirely possible that the WSJ and I have missed a few firms. But I believe most of the large ones, including Swiss Re today (h/t Calculated Risk) are represented below:

By my (and Excel’s) math, assuming the Absolute Worst Case Scenario being Discussed, just under 7.8% of the Total Possible Value of the pending bankruptcies has already been written off.

The Absolute Worst Case Scenario is clever, and going to the trouble to find and sum reported mortgage-related losses and writedowns is a nice touch. But Houghton has an apples and oranges problem. It isn’t entirely his fault, because the reporting is sloppy and even if you read press reports closely, it often isn’t obvious what is included in the losses.

To illustrate, let’s start with two big miscreants: Merrill and Citi. Of Merrill’s $8.4 billion in recent writedowns, $6.8 billion was CDOs (AAA tranches, mind you) and $1.1 billion was subprimes. So for Merrill, the great majority was CDOs (and remember, while a lot of BBB and BBB- tranches of subprime paper went into CDOs, the assets in those vehicles are heterogeneous. Overall, they can include tranches of regular ABS, collateralized loan obligations, whole loans, and securitized commercial real estate loans. So CDOs most assuredly do not equal subprime, although the often contain subprime).

Citi’s disclosure of its $8 to 11 billion expected writedown has been pretty hard to penetrate. From the Wall Street Journal:

Citigroup’s subprime exposure — and source of its problems — are two big buckets that together total $55 billion, the bank said. The first bucket totals $11.7 billion, including securities tied to subprime loans that were being held, or warehoused, until they could be added to debt pools for investors. The second, totaling $43 billion, covers so-called super-senior securities

Now you would think that calling something subprime would be bad enough. But it isn’t clear how “subprime” those “super senior securities” were. It turns out that Citi had created CDOs, and in a clever ruse to extract more profit, had the most senior tranche be commercial paper. Um, but CP goes out a max of 270 days while CDOs are generally expected to live 2 to 3 years. So Citi expected to roll the CP, and when it couldn’t, it was faced with either buying the CP itself or liquidating the CDOs.

Sp these CDOs clearly contained subprime paper, but how much is unclear. And the Financial Times had this to add:

The latest Citi blow contained three scary nuggets. The first is nobody really knows where the CDO debacle will lead. The complexity of valuing these things – not just how the cash from the underlying collateral gets divvied up but how the the default rates of the different securities correlate – was underscored by the $3bn range Citi attached to its potential hit. The second is that the scale of the mess could be even greater since there are many synthetic CDOs out there referencing the cash CDOs. Lastly, Citi added yesterday for good measure that all it had detailed was its direct exposure. Along with others, it may have offloaded credit risk to bond insurers. If those guarantees were to lose value, there could be a grisly end to this saga.

So you get the point: the losses in Houghton’s spreadsheet include more than subprime.

Houghton’s second miscue is that his taking the losses reported at banks and securities firms as the sum total of writedowns. Even if these were truly consisted only of subprime losses, he is missing the fact that much (most?) of this paper was securitized and sold to chump investors. In fact, what has been remarkable about this saga is how much is held by the intermediaries. It isn’t good practice to carry a lot of inventory in your warehouse, or on your trading books (an old Wall Street saying is, “A position is a trade that went bad.”).

Two examples: a buddy tells me someone at Morgan Stanley woke up in February and realized the mortgage markets were headed south. He unloaded $20 billion of paper at a small loss. He is now a hero at the firm. Similarly, the recent reports on how Goldman avoided the losses of other firms stresses that they too lightened up on their positions and went net short.

Now no one know what proportion of subprime paper is held by originators and dealers versus end investor. End investors will not (except perhaps in a very extreme case) report losses on subprime paper separately. So we have no way of knowing how much has been marked down, and to what degree.

Third is because of the vagaries of mark to market, it is quite possible that subprime paper is or will be marked below its economic value. Unless you are a distressed investor, buying subprime-related paper right now is pretty sure to be a career-limiting event. So any sales of subprime paper or complicated ABS is likely to meet with a supply/demand imbalance (the “fire sale” scenario. That, for example, is the logic behind the attempt to create the SIV rescue entity.

So there is no way of knowing whether the writeoffs to date are too conservative, or conversely, whether some have used real market prices and therefore, although accurate, show a worse picture than indicated by the fundamentals of these deals.

http://www.atimes.com/atimes/Global_Economy/IG14Dj01.html

“What happened this week was a result of the prices of mortgage securities falling sharply in the past few weeks. Finally on Wednesday, the rating agencies moved to cut ratings of more than $12 billion worth of bonds. This forced the “hogs” mentioned above to sell their bonds into a market that was already nervous about further weakness in the US economy.

The result was, of course, carnage. Being unable to sell all the securities they had, many of the investors had to sell other securities, including corporate bonds hitherto unaffected by the rating moves.”

Because most banks use leverage, thus the sudden move of AAA to Default leads to fire sale in other debt. The danger of this problem is time, not money. Any banker will tell you that time is money, and money arrives late on time can’t save the bank.

“The Absolute Worst Case Scenario is clever”

Really?

I checked a few subprime deals for original loan balances.Highest I could find :average [for the pool]$216000.Every 2006 and pre-2006 are below $200k.

someone at Morgan Stanley woke up in February and realized the mortgage markets were headed south. He unloaded $20 billion of paper at a small loss. He is now a hero at the firm.

Yeah, now he’s a hero. I wonder how long it took for this heroism to be determined.

A comment by someone who strongly believes in getting out early with the small loss, and whose “heroism” has often been challenged by her “you coulda ridden it out!” brethren. Heh.

Tanta

It would be interesting to see someone scope a comparison between US generation of losses and US absorption of losses. $ 500 + billion is a zone being bandied about for mortgage and other credit losses in this cycle. A good portion of that will be absorbed outside the US. Within the US, a good portion will be absorbed outside of the integrated money center banks – by dealers, hedge funds, pension funds, etc. Across those numbers, a good portion will be extended out over time.

It is absurd for the market to be perplexed about the uncertainty of current numbers, given that the actual loss experience that will compare with current expectations will play out over the next several years and can’t be known before then (e.g. emerging ARM defaults). The good thing about this is that the worst case losses are now being considered by markets well before they are known, so it is reasonable to assume that the risk will be reflected efficiently in the market fairly soon.

The point that the bag-holders include entities other than securities firms is a good one, but Ken allows that via the perhaps slightly cryptic remark about Jim Hamilton’s pension plan.

As far as an amount that I might agree to over drinks as the maximum scope of the mortgage problem, something approaching $1T seems reasonable enough. I’d expect that sometime before we were too hypothetically drunk, I would object that he omitted subprime modifications and prime everything (a reasonable critique of the “model”), to which he’d probably say that the $417K-per-adverse-event figure covers those in principle. (This Partly defuses jck’s critique.) None of this is to say that it wouldn’t be desirable to have separate and more finely tuned prime and subprime inputs for the fundamentals.

As for the vagaries of the market and marking to it, that’s a good point too; it’s reasonable enough to describe that as having an unknown effect.

In the end, having something that looks like a ceiling but isn’t a supremum leaves me feeling underinformed. It seems that the amounts written off are large, but it hasn’t been established whether the worst is over or is yet to come.

(Substantially identical comment also left at my place.)

Tom:

The writedowns so far come from mark-to-market losses not from actual defaults in the underlying securities.For ex, none of the tranches on the ABX (including the BBB-) has experienced a principal writedown/shortfall so far.

So trying to estimate the cost of the crisis, starting with the basic subprime mortgage is going to be difficult.The mark to market is driven by expectations, expectations may be right or wrong, but for some banks or investors the damage is done regardless of whether expectations turn out to be right or wrong.

I would add one more thing — if you are considering this a subprime problem, you are underestimating it. The Mortgage Bankers Association has published statistics showing that of mortgages originating in the years 2003-2006, more than half were refinancings. The numbers are 66% (2003), 54% (2004), 50% (2005) and 48% (2006). Since every one of these people had already qualified for a mortgage before the go-go subprime years, they were likely prime, Alt-A or prime jumbo borrowers.

Most of these people were doing cash out refinancing. They may be in the same position now as many of the subprime borrowers, upside down on their mortgage, owing more than the house is now worth. I personally know a number of people in that situation. Many took just bull rate mortgages at a low teaser rate, just like the subprime borrowers. Many of them are now having problems refinancing to a fixed-rate, and can’t afford the rate adjusted, fully amortizing payments.

So if you are trying to calculate the extent of the problem based on only subprime, you will underestimate it.