By Rumplestatskin, a professional economist with a broad range of interests and a diverse background in property development, environmental economics research and economic regulation. Cross posted from MacroBusiness.

What few seem to appreciate, either inside or outside of Japan, is just how strong the resulting Japanese recovery from 2002-2008 was. It was the longest unbroken recovery of Japan’s postwar history, and, while not as strong as pre-bubble Japanese performance, was in fact stronger than the growth in comparable economies even when fuelled by their own bubbles.

How on Earth did Japan manage that with their ageing population and zero population growth? Indeed, Japan outperformed Australia in productivity growth since 2000 and very nearly kept pace with real GDP per capita growth.

Australia’s average annual real growth in GDP per capita since 2000 is 1.28%. While I can’t find a direct measure from the Japanese Statistical agency, using the World Bank data collection I can make a comparison of real GDP growth per capita of Australia and Japan using a common methodology. Using these statistics I find that Australia had a mean annual growth in real GDP per person since 2000 of 1.8% while Japan’s was 1.4%.

Notice in the graph, however, that Australia’s growth in real GDP per capita fell considerable from 2004, when population growth rates began to push up from 1.2% to a peak of 2.16% in 2008. Since 2002, when Japan’s real growth per person increased, the population growth rate declined from 0.2% the preceding 2 years to near zero (average 2003-2008 is -0.002%) till the financial crisis hit at the end of 2007.

Australia’s economic performance is terms of productivity growth looks pitiful in comparison to Japan. Average annual Total Factor Productivity growth since 2000 was a shy 0.47% (including a productivity recession in 2004-05) while Japan recorded a strong 1.77% over the same period (data from OECD here).

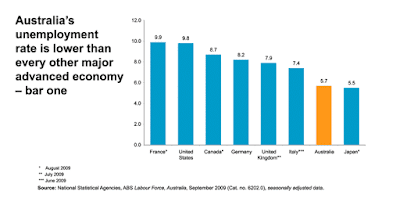

Of course there is always unemployment to consider. The graph below shows that on this measure, Australia is also behind Japan (having been in front for just the period 2007-2008). Some longitudinal data is here.

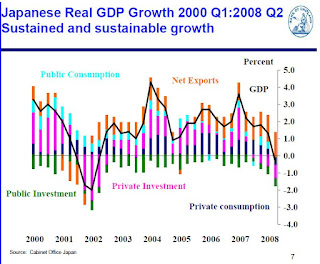

Recent research also suggests that Japan’s economic track record was unfairly blemished by asset price deflation followed by short recessions in the 1990s (1993, 1997 and 1998). The graph below (from here – including 20yr data set), shows Japan’s solid performance over the past decade, with their longest boom since WWII occurring from 2002-2008.

It appears that turning Japanese is not the tragedy it is made out to be by popular economic commentators. Here’s just one example of the popular perception-

As it turned out, Japanese investors lost nominal wealth equal to three entire years’ GDP. And the economy today hasn’t grown in 17 years or created a single new job.

Nor has the debt been reduced. Instead of permitting the private sector to destroy and pay off its debt, the public sector fought against it…borrowing heavily to try to bring about a recovery. Result: no recovery…and almost exactly the same amount of debt. But while the private sector paid off its debt, the public sector picked up the borrowing. Now it’s the government that owes money all over town.

Detractors cite the massive and growing public debt in Japan as a problem. But if the debt is denominated in Yen, and interest rates are set near zero, the burden from the debt is minimal. In fact, Modern Monetary theorists might claim public debt in ones own currency is never a burden because government can enact future policys to pay down debt with freshly printed money. I’ll leave that particulars of this option to a future MMT debate.

The above graph confirms that Japanese government debt has replaced a substantial portion of private debt since the early 1990s. In my view this is a justified effort to keep the value of the yen stable by maintaining money in circulation – an approach that could be adopted in Australia in the coming decade, with government debt replacing household debt for the same reason.

One must keep in mind that it is probably not the intention of the Japanese government to ever pay off this debt. I am sure they are happy to continue to progress with a high savings rate, high productivity, high GDP, net exports and almost every other fundamental ingredient for economic success. Turning Japanese appears to be about fundamental economic prosperity cradled in an unfamiliar monetary framework.

Tips, suggestions, comments and requests to rumplestatskin@gmail.com + follow me on Twitter @rumplestatskin

Eventually, those savings that soak up all of the government debt will be liquidated for one reason or another. ANY inflation would basically bring it all down. Your ‘boon’ is built on an edifice of bullshit.

He already said that he is a ‘professional economist’, i.e. someone good with e-conning people with bullshit.

“ANY inflation would basically bring it all down.”

Vulgar statement of the century?

Care to explain that one? No? Thought not.

He won’t because it’s non-sense.

Things turn over, in this world, and time never stops: but thee folks have an ever-present fixation on some imagined “day of reckoning” (gee, kinda like some religions).

They ought to remember: render unto ceasar that which is ceasar’s…that is to say, that the “inescapable day of reckoning” belongs to the religious, not the practical, sphere.

For, as religious folks know, to forgive a debt or trespass or “sin”, is divine – don’t they? And thus, in this world, a “day of reckoning” for the repayment of debt is never “inevitable”, and is almost always “rolled over”, or written off: for whether or not there will be such a “day of reckoning” ALWAYS depends on the hearts of the creditors, and is NEVER a result of “divine decree” or any other “inevitability” – will they really take a pound of flesh, or not? – is ever a live question, not a forgone conclusion….

Well….will they?

Have they ever?

The “inevitable day of reckoning” is a religious concept: and people ought indeed to render unto God, what is God’s. That concept of “inevitable and inescapable reckoning of debt and its re-payment” simply doesn’t apply to Ceasar’s world: that is to say, the world of money.

Unless, of course, Ceasar wishes it to. But does it apply as a necessity? As a divine law, or inevitable consequence of the relation of indebtedness? No, no, no…this remains Ceasar’s choice, not God’s.

“Detractors cite the massive and growing public debt in Japan as a problem. But if the debt is denominated in Yen, and interest rates are set near zero, the burden from the debt is minimal.”

Good point. Monetarily sovereign states should provide a risk-free fiat storage service that pays no interest. I see Japan has approximated that with government “debt”.

i also call bs – your turning japanese means maintaining the status quo or said another way it means keeping the ponzi scam from imploding – which of course is nothing short of magnanimous – after all, think of the poor children who would suffer if the emperor really has no clothes!

Japan’s GDP/capita was helped by the zero population growth during those years cited in the above post.

For the US to acheive that, I am afraid some might advocate we return all the illegal immigrants.

Yes, what about the fact that most of Japanese debt is owned locally? The fact that the pool of savings that allowed this to happen is evaporating and there will be consequences when that happens. Lets ignore all that, when it happens we will have Krugman say that the government didn’t borrow enough. Brilliant!

A sovereign currency issuer does not have to issue bonds to finance deficit spending. It can simply credit bank accounts. The risk of too much deficit spending is inflation, yet even with all this deficit spending, Japan is flirting with deflation.

The problem with the Japanese strategy (which is very similar to the US one) is geopolitics.

Let’s admit Japan faced any of these dangers in the next decade: 1. A socialist revolution; 2. A trade war with China and/or the West; 3. A break-up.

If any of these dangers, today looked at as impossible, were to be perceived as a bit more likely in the future, there would be a rationale for leaving either the yen or Japanese bonds. If debt is too high, that could lead to higher yields and inflation spiralling out of control, if debt is monetized.

Arguably, that is what’s happening in Europe: a re-assessment of a very unlikely risk (break-up). I think this, too, may happen to the US in the very near future (a re-assessment of trade war risk, revolution risk, and a break-up of the dollar-peg monetary system).

This is a time bomb to go off sometimes in the future.

Much better would be for governments to officially acknowledge that they do overspend and simply print the additional money. This would have the advantage that there is no interest to be paid and interest rates could reflect actual market rates.

Of course, in such a situation, banks would be hurt as they would not be able to earn money from rate differentials.

Much better would be for governments to officially acknowledge that they do overspend and simply print the additional money. Linus Huber

There is no “overspending” unless price inflation results in the government’s money.

This would have the advantage that there is no interest to be paid Linus Huber

Yes, it is an abomination that government rents its own money supply.

and interest rates could reflect actual market rates. Linus Huber

Yes, provided there was no lender of last resort which there should not be.

Of course, in such a situation, banks would be hurt as they would not be able to earn money from rate differentials. Linus Huber

Screw the banks. We need them like we need a hole in the head.

Did the following ever occur to people who make this argument:

Public sector spending = private sector savings

Therefore, as the government spend, cet. par. savings increases.

Accounting identity. Duh.

I think you meant “deficits” and not “spending” on the left side. Also, “savings” on the right side should read “net savings”.

Same difference, I’m in the middle of writing something on a different topic, hence the lack of specificity.

I’m also sick and tired of these idiot “savings in Japan will run out” memes. They’re so f$%king stupid they make me want to cry. And everyone falls for it because it sounds intuitively correct. But it’s not, because when the government spends, by accounting identity, they add to savings. Hence, much of the Japanese savings are probably DUE TO THE GOVERNMENT DEBT! They’re not allowing the debt to expand. THEY’RE THERE IN LARGE PART DUE TO THE GOVERNMENT DEBT.

Easy enough to see from the sectoral balances:

http://static.seekingalpha.com/uploads/2010/1/13/saupload_sectoralbalances.png

Yet the dunderheads remain out in their legion.

Aet says above that they want a ‘day of reckoning similar to a religion’. Spot on. Clowns. One day we’ll exit the Middle Ages, but not today.

The two are profoundly different. “Public sector spending = private sector savings” implies that the private sector has no means of saving (without the public sector spending). Savings and net savings are different; it is entirely possible for them to move in different directions.

I wasn’t 100% clear the first time. But what you just wrote is wrong. ‘Private sector savings’ implies an aggregate. And I said ‘cet. par.’ — so we’re ignoring the external sector. In those circumstances the private sector in the aggregate cannot save unless the government spends.

I should have been clearer. But you’re just muddying the water further.

Keeping the Yen weak helped with exports quite a bit. China seems to get criticised relentlessly for keeping the Yuan weak, Japan not so much.

2002: Japan pins hopes on weak yen (BBC)

2003: “Japan’s success in keeping the yen from gaining significant strength against the dollar — and other currencies — is helping the country’s economy rebound by keeping its exports more competitive abroad.” (NYT)

I have long been of the suspicion that even though things were not hot in Japan in the 1990s (they had a raft of financial firm failures in 1997 when they cut stimulus spending), they exaggerated so the US would not bust its chops over the cheap yen.

This completely ignores 2 critical facts:

1) US was in a bubble.

2) China was, and is, in a bubble.

Japan’s key export markets supported this “growth”. One is hobbled, the other is the biggest bubble of all time.

As with many things economic, it might work for a while if ONE party does it. But it’s suicide if everyone does.

However, what Japan CAN do, and in future MUST do, along with the rest of the world, but sooner, given it has no resources whatever, is move more quickly to a steady-state, sustainable economy.

If the world goes into depression, every country goes into depression. I am not sure we should criticize an economic model for not being robust enough to a global depression.

Arguably, the US would have a bigger problem than either Europe or Japan if financial and trade flows stopped growing around the globe. The US needs oil, but doesn’t produce enough to finance its oil imports.

Arguably, the US would have a bigger problem than either Europe or Japan if financial and trade flows stopped growing around the globe. The US needs oil, but doesn’t produce enough to finance its oil imports

I think there are too many moving variables to say with certainty.

The US has perhaps more natural resources than any other country on Earth. If trade flows stopped, we can feed ourselves, and although a tough decision we would shift away from Oil and towards Coal. Yes, very dirty, but doable. We would also for sure impact “drill baby drill” policies including raping Alaska and our Gulf coast.

we would enact protectionist trade policies as well, thus dropping our importation of other goods (leaving some wiggle room to still import oil), as some of our exports will happen even under trade wars (such as food exports).

obviously: this would also crush Japan, China, and Germany as well as their economy is dependent on a large part to exports to the US.

Thus, we’d see a rebalancing, with China/Japan/Germany needing to increase domestic consumption, and the US reduce consumption of imports and increase domestic production. Future trade war or not, some of this rebalancing needs to occur anyway.

anyway, these are just some ramblings showing how difficult it is to predict “the biggest loser” (since we’d all lose immeasurably).

all that said… if the US lost too much energy due to lack of oil it would be war anyway, which is why I think it’s too hard to say who the “biggest loser” would be.

That rebalancing means less disposable income for US families and more disposable income for Chinese, Japanese and German families.

No matter how you construe it, US families are on the losing end. Good luck trying to reduce their income even more in order to send carriers against China…

Diego, I think you misunderstood me.

I highlight this part of my post:

anyway, these are just some ramblings showing how difficult it is to predict “the biggest loser” (since we’d all lose immeasurably).

I do not argue that America/Americans would be fine, or even all right. I also don’t argue they’d be better or worse off than German/Chinese/Japanese citizens.

I only argue that it is difficult to foretell exactly how it would fall out.

Good luck trying to reduce their income even more in order to send carriers against China…

This is exactly what happened with Germany due to crushing war reparations imposed by the French. Germany was impoverished. and still managed to mount a pretty devastating war effort on Europe. Obviously, the US would not go to war with China. what would be the point? we would do what we always do-go to war in the Middle East for the Oil. China/Russia/Europe would then have to decide if they wanted to join this war.

That rebalancing means less disposable income for US families and more disposable income for Chinese, Japanese and German families.

Not quite, but close. An orderly rebalancing means more disposable income for those three groups (and as I said, a rebalancing is needed regardless). But a disorderly rebalancing most likely means a loss of disposable income for all groups. again, we all lose.

but even that isn’t quite right either, because Americans have already had progressive loss of disposable income for over 10 years now… masked by DEBT which allowed our consumption to stay artificially high, which allowed German/Chinese/Japanese production to stay artificially aloft. (in fact, the Chinese/Japanese governments are part of the problem here by recycling American debt in part of their mercantilist machinations).

We already have seen what happens to Europe/China/Japan when American consumption drops. Now imagine if it is torpedoed. A decrease in American income combined with a locking out of Americans from debt would put the stop on their consumption, which would feed back negatively to German/Chinese/Japanese exports causing loss of income to the German/Chinese/Japanese families.

who would lose more? Perhaps Americans, but I stress again we’d all lose pretty darn bad.

Yearning to Learn,

I agree with you on everything. I expect rebalancing to occur disorderly. There are just too many things that can go wrong and set it off.

obviously: this would also crush Japan, China, and Germany as well as their economy is dependent on a large part to exports to the US.

I don’t think this as true at it once was. The Chinese are busy increasing domestic demand like crazy – more than enough to absorb the loss if the US were to run protectionist. A China-EU-Japan trading block in response to US protectionism would be very bad news to the US (Which is why the US will never again adopt severe protectionist measures).

If the point of this article is “Turning into Japan is not that bad”, then I agree with it.

But I’m not sure I’d twist it into “We should try to emulate them”.

One point explicitly made in the article: Japan’s population has stalled. Thus, they don’t need GDP growth to get increased per capita income. In fact, even without productivity gains it is possible for them to have increased per capita income with negative GDP, so long as the fall in population is greater than the fall in GDP.

This is not possible in an American economy that is adding approx +100-200k workers per month or so.

a point implicit but not perhaps explicit: Japan is an exporting juggernaut, with mercantilist policies. Thus, they are able to get a boost in GDP (or at least make a less negative GDP print) despite falling population due to a larger world population to export to.

Much of the world economy’s problems are due to the fact that we simply don’t have enough jobs for the ever increasing population, especially given automation.

It is unlikely that the US will achieve decreasing population AND a world economy to export to using mercantilist policies any time soon.

that said, this article is from Australia I believe, so perhaps the point is only to show what Australia can do, and not the US?

“Modern Monetary theorists might claim public debt in ones own currency is never a burden because government can enact future policys to pay down debt with freshly printed money.”

Ummm… I think most MMT proponents would say that gov’t debt is equivalent to private sector savings NFA (echoing PP above). To Yves point, the risk of higher deficits is inflation. MMT is not concerned with “paying down debt” per se.

Marley: MMT is not concerned with “paying down debt” per se. Yes, it is. It just correctly identifies what the reflux, the redemption, the “paying down debt”, of money – is. In the private sector it is the repayment of loans. In the public sector it is taxation & government sales & fees.

One of the biggest problems is the mainstream confusion of bond sales as a reflux of money, a loan which needs to be repaid, when it really is not. It is nothing but an asset swap, an exchange of one form of money/nfa/credit/debt for another. Sometimes, not usually or in the long run, it can act sort of like one, be disinflationary, which the mainstream irrationally generalizes.

Thanks for the clarification. I should have said “govt deficit” instead of “ebt”, and further qualified by adding “as an exercise in balanced/surplus budget attainment”.

One other point:

I keep hearing from MMT and others like Krugman, Ridholtz, the Fed etc., that “inflation is the only threat from printing”.

Wrong. Because in the REAL world, not the models, the money always passes through banks hands FIRST, which simply enables another round of intense concentration of wealth and power, and further destruction of accountability to citizens. If the money did NOT go through banks hands first, printing post-Weimar would never have been tolerated, i.e., banks would immediately crash the system or otherwise do whatever it takes to end the experiment.