By Stephanie Kelton, Associate Professor of Economics at the University of Missouri-Kansas City. Cross posted from New Economic Perspectives

Neil Irwin at Wonkblog has a new post up: The Deficit is Falling Fast. Can Washington Accept Victory?

He quotes John Makin of the American Enterprise Institute, who says, approvingly, that the U.S. has probably imposed enough austerity “for now.” Then he shows us the evidence.

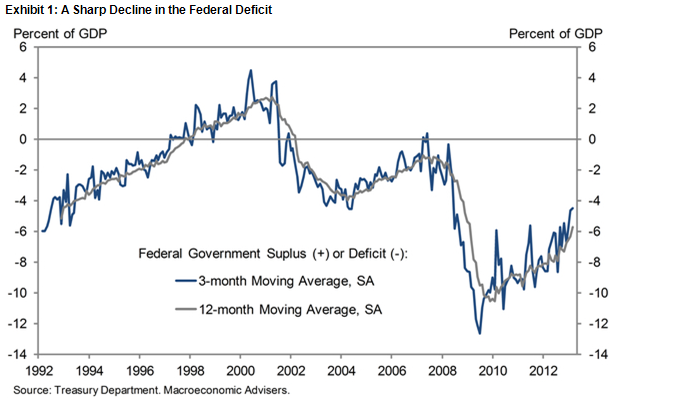

Irwin makes the obvious point that deficits tend to come down during the recovery phase of the cycle:

The economy is gradually healing, leading to higher tax revenue and reducing social welfare spending.

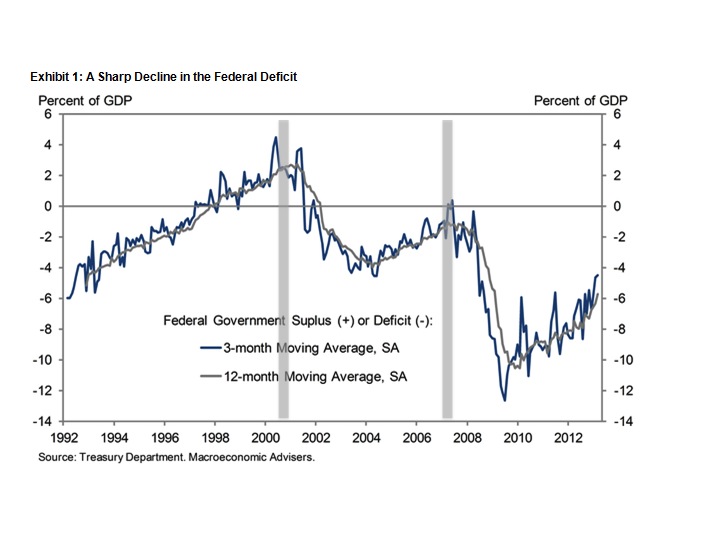

What he doesn’t show you is this:

It’s the same graph, but with recessions (grey bars) added. So what does it show? Basically, that the economy tends to go into recession whenever fiscal policy becomes too tight — a point made routinely by contributors to this blog. Unfortunately, it’s not something Irwin points out. Instead, he quotes Jan Hatzius (Chief Economist at Goldman Sachs), who says he expects the federal deficit to continue its downward trend, falling from its current level (about 4.5 percent of GDP) to 3 percent or less in FY2015.

Instead of raising a red flag about the consequences of letting the deficit get too small, Irwin offers this as prima facie good news. The basic argument being that we will have reduced the size of the deficit enough to keep us out of trouble — for the time being — so we can pause for a moment while we put together a plan to address our really pressing problem: unemployment the long-term deficit.

The lesson out of all this for Congress should be this: Focus on the long-term, not the short-term. The falling deficits of the next few years don’t solve the bigger longer-term problems the United States faces, on reining in rapidly rising health care costs and an unwieldy and frequently unfair tax code.

Alright, I can’t argue with the point about the tax code; it is unwieldy and frequently unfair, but let’s stop and examine Irwin’s other claim — the notion that we need to rein in rapidly rising health care costs because they are the drivers of the long-term fiscal woes.

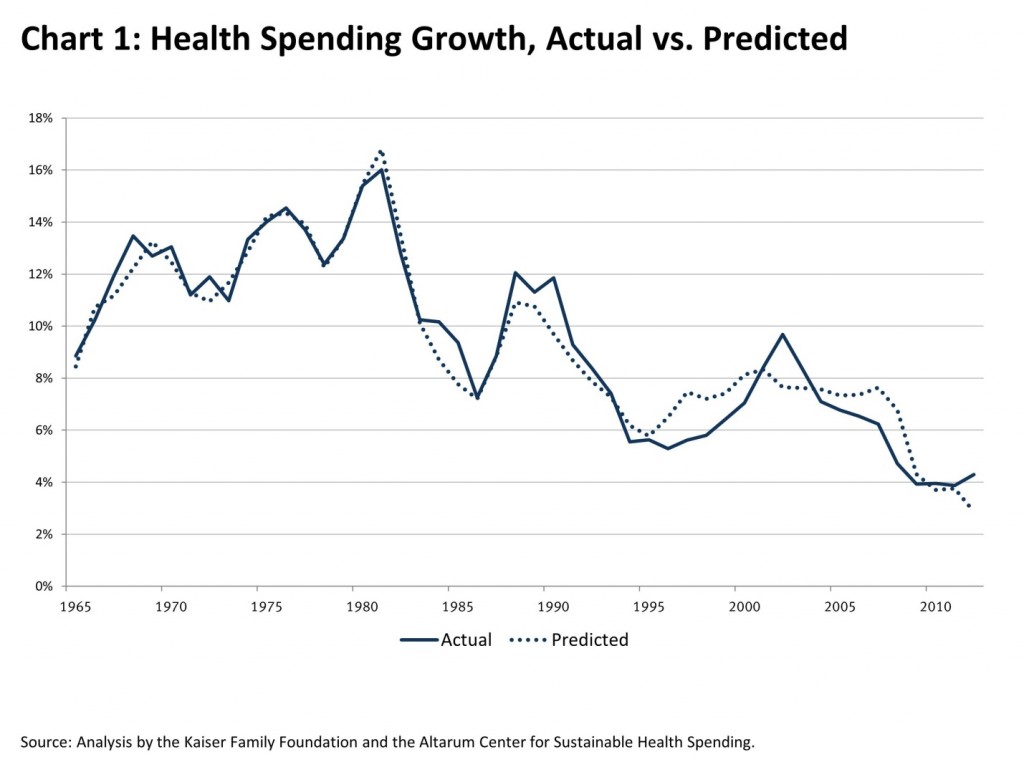

What? Wait a minute. Health care costs are already being “reined in,” as Irwin’s Wonkblog co-contributor Sarah Kliff has shown. Health care costs have been growing at their slowest rate in decades. (It’s ironic that Irwin’s post is about how the deficit is actually falling, yet he fails to point out that something similar is happening with health care costs.)

And this is an important dragon to slay, because runaway health care costs are widely considered (by majorities in both parties) to be the primary driver of our long-term debt and deficit woes. Rather than slay it, Irwin feeds the beast.

Next time, he could reference this important analysis from two staffers at the Federal Reserve. It does to the CBO’s forecast of rising health care costs (and subsequently long-term debt and deficits) what Herndon, Ash and Pollin recently did to Reinhart & Rogoff’s “tipping point” predictions.

Even better, Irwin could go back to what Hatzius said here and ask him whether he thinks Goldman’s 3 percent deficit forecast is: (a) desirable or (b) sustainable. Specifically, he should ask Hatzius to explain what it would mean for the domestic private sector in a world in which the U.S. is running a current account deficit that exceeds 3 percent of GDP. (I’ve already traced out the implications here.)

The fundamental problems with so much of what’s written about debt and deficits are twofold: (1) Almost no one distinguishes those who are merely users of the currency from those who are currency issuers. It’s a huge oversight, and it leads to grave errors when predicting things like sustainability (or “tipping points”); (2) Almost no thinks about the government’s deficit in the proper (balance sheet) context. We are connected, domestically and globally, by our balance sheets. Outflows from one sector of the economy show up as inflows elsewhere, and government deficits are an important source of corporate profits.

It’s time more people stopped to think about what this necessarily implies when the government tightens its belt.

Great post. Note that when Austerians say that we should focus on the long-term, what they really mean is that we should forget about unemployment and social services. Nothing new, as Keynes claimed, “the long run is a misleading guide to current affairs. In the long run we are all dead. Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us that when the storm is past the ocean is flat again.”

Austerians focus of creating a neo-feudal society–that is their agenda and it has nothing to do with economics and everything to do with political arrangements. The whole point of the effort is to move power towards the top. These people aren’t all stupid because their arguments just make no sense empirically.

I think this should be highlighted, emphasized, illuminated and made visible from space:

Almost no thinks about the government’s deficit in the proper (balance sheet) context. We are connected, domestically and globally, by our balance sheets. Outflows from one sector of the economy show up as inflows elsewhere, and government deficits are an important source of corporate profits.

It’s time more people stopped to think about what this necessarily implies when the government tightens its belt.

There are maybe a few thousand people world-wide who take this into consideration and bother to try and understand its macro-economic effects, which explains why we lurch from crisis to crisis: the guys at the helm haven’t a fucking clue.

I don’t think they are clueless. In 2008 I thought, who are these morons – this is no way to run a country. But watching them in action is very instructive. I’ve almost convinced myself that this is entrenched warfare and the US will be the last country standing, even tho’ it will look like a different country. Time and again Congress and the President have avoided any and all action that could stimulate the economy. They have instead kept it down relentlessly – not because they are clueless but because if the American economy is slowed down the rest of the world will stop. The only thing that is not clear is, why? I think there are several reasons but since it is termed a “financial” crisis, I think the main reason for it is a new financial system. That explains why Bernanke has kept the banks alive. Soon, when other countries begin to fail, our banks can move in and buy them up… more or less.

But this thought makes me very uneasy because now is the time to get rid of our “private” central bank and use the Treasury to spend directly into the economy to accomplish the things a country needs to do. No doubt that is why there is so much deception and secrecy right now.

Susan, listen to this Michael Hudson podcast very carefully (Rimini Italy 2012). It’s not the central bank that’s the problem, although you have the issue correctly.

http://mediaroots.org/mr-transcript-italian-mmt-summit-2012.php

Hudson starts at about the 19 minute mark. What I’m talking about starts at the 23 minute mark where he clearly delineates the difference between government/central bank real money and bank credit money.

I certainly agree with Prof Hudson. But he is blaming the banksters, the private bankster system, of which the Fed is the private central banker. I wish the Fed would surprise us and implement the living wills of the TBTFs. May they rest in peace sooner rather than later.

As I’ve stated in numerous places the reason is staring you straight in the face once you de-hypnotize yourself from the weird notion that “economics” is something discrete–it is another face of politics. Once you understand that the agenda for the powerful institutions and personalities that make up the world system, the Empire, if you will, you will see that the most important thing is to take power away from the middle-class and keep shoving it up by making sure the economy stagnates even if it means less wealth for those at the top. It will translate into more power and insure a neo-feudal future which has been the goal of institutions like the IMF (which early issued its plea for austerity immeadiately after the crisis).

Maybe we’d be all better off with rule of the few–I certainly do not automatically reject it but what I do reject is the illusion that Austericats mean anything else by their agenda other than the most retarded of their number–it is sheer Machiavellian politics.

Susan,

Thank you for raising what I consider to be one of the profoundly troubling questions of our time. I too have wondered about their true policy objectives… the River “Why?” that you posed. The policies themselves — fiscal austerity, continuing high price of oil, long term reduction in the velocity of money, ramping financial asset prices with QE-ZIRP/fractional reserve banking, no regulation, unilateral abandonment of the rule of law, etc. belie the propaganda messaging of their corporate media.

Does it have to do with hegemony control of money, markets, media, energy, food?… or is it limited to restoration of TBTF balance sheets through mark-to-market asset valuations and speculative derivative gains?… or is it just all about raw wealth concentration and political control objectives at the individual level under the Citizens United structural framework?… or some combination?

Heck, I dunno. It may be that banger is right. But I do know is that their values and thought processes are significantly different from my own, and that they do make mistakes… Big Mistakes!

Professor Kelton is probably too dainty, elite and timid for the peanut gallery — where reticence and superciliousness would be artfully masked by an air of officious and distracted time-challenged business — but if I was in her class where she had to deal, I’d raise my hand and ask:

“About this sectoral balances stuff, I get the general idea but what about all the corporate cash and back and forth spending of it? For example, let’s say three companies have loads of cash and decide to invest it in capex and other stuff buying and selling products and services among themselves. That produces revenue and profit and employment, which may in turn produce bank loan-funded consumption by people who have jobs and income, even though no money is moving between sectors. So you’d have GDP growing in this case but no inter-sectoral fund shifts, if I’m thinking this right.”

I’m only an amateur economist so I freely admit I may be missing something. But it seems to me you could, in theory, have a situation where intrasectoral fund flows outweigh intersectoral funds flows in their ability to instigate economic growth.

The mysterious “confidence fairy” could manifest here, in theory, even though it has been absent in recent years. There seems little chance of mathematically forecasting when and what would cause the drivers of growth to shift from inter to intrasectoral factors. It seems to be a product of some construction of group behavior, probably inherently unforecastable, like the formation of herds of animals and their dissolution into scattered singularities. At least it seems that way to me, right now.

So are you saying Stephanie has overlooked all the differences that make an economy uneven by definition? Sometimes you are very cryptic Craazy. And that deficit spending would unjustly benefit the already productive sectors more, so over time this would impoverish the less efficient ones?

Not trying in any way to be cryptic or presume anything about Professor Kelton’s knowledge of what academics call “economics”.

Nor am I implying any normative judgment about the phenomenon of deficit spending. I’m attempting to be as positive as possible, no pun intended.

And I tried to state my confusion as plainly as possible.

At any rate, I don’t expect Professor Kelton to jump down into the peanut gallery mosh pit and get dirty with the savages. She probably has better things to do, like indoctrinate her students. bowhahahahahahahah. Hey teacher, leave them kids alone . . . all in all it’s just a notha brick in the wall. We don’t need no education/bamp/we don’t need no thought control . . . OK, that’s not Professor Kelton’s class – I’m just having fun — that’s Professor Mankiw’s class. I know that.

It’s hard to get rich quick without working. The four horseman of the financial apocolpyse have worn my portfolio down. I’m talking Hussman, Martenson, Shedlock and Harrison. Ed tries to pretend he’s above the fray, but he blew my confidence with his recession call last year. These guys may be right eventually but by that time I’ll still be working and the idea is to get rich in a month or two. They’re not much help, I have to say. Fortunately Shedlock and Hussman don’t charge for their advice. I pay Martenson and Harrison, so that allows me to rationalize that I must be getting my money’s worth somehow. An intelligent person wouldn’t pay for nonsense and since I’m paying I must be intelligent. At least I feel smart even when I’m losing money hand over fist.

They all have me under their spell and I’m immobilized in a state of poverty and confusion, unable to trade or even think clearly about how to get rich quick other than going short, which doesnt work. Professor Kelton doesn’t have me under her spelll so I can still ask questions. But she is hot, so she’d probably have me under her spell in person. I’d still ask the tough questions though.

Calling Stephanie. Please pick up.

…global equities…(for the moment)…

Bank loans aren’t financed by deposits. Loans are created when banks credit accounts, and the money is destroyed when the loans are paid back, i.e. no net increase in private sector financial assets.

Net assets can only increase by inflows from other sectors greater than outflows.

DEMOCRATS=SUCCESS

1945-1980 democrats worked hard in creating a successful middle class

that had jobs that paid enough to afford a nice home,

Health Care and Education for children.

Since 1980, it has been decades of loading them with debt in order to afford a middle class life style. Since 1980, the top 1% had a 281% after Tax income and middle 20% got 25% which was less than. Inflation. The wealthy had the money to loan and took advantage of it.

The Outsourcing of our Manufacturing Industries was biggest sham and hit on the middle class and decent paying jobs.

The Tax Code was loaded with goodies for the rich and corporations

There is a series of Solutions to reverse course before we go over that cliff.

Progressive Flat Tax by Group. Tax Total Income not AGI with the loads of exemptions

Assure a progressive Flat Tax that will balance our budget and start paying down that horrid Republican created Debt of $15,800 Billion

Fed fund campaigns and election—6 months—3 primary 3 general—free equal tv time—No personal or outside money. Debate a week=12-=adequate to evaluate candidates

Since no need to raise campaign funds keep em on job not on road.

Ban ALL federal employees from accepting anything with a financial value.

This closes K Street Bribery.

It give middle class a chance to win an election since they cannot be bought.

Burn the tax book—It gets enough revenue $1100B that immediately balances our budget.

Start anew—Exemptions must serve a common good not fat wallets

clarence swinney burlington nc

Oh yeah, I will agree the Dems pretty much made the middle class.

But those were dems of over half a century ago.

The modern dems are bringing the sledgehammer out of the closet to help the Republicans in the demolition of the ‘middle class’ their grandfathers created.

Dont put too much faith in the modern Democratic party, mate. The party of Obama is NOT the party of FDR. Times change, and its been over half a century. It should be self-evident that its not the same party.

Regarding the Democratic party as if its still the party of FDR is as stupid as thinking the Republican party is the same as the party of Lincoln’s time…

The discussion on “Debt and Deficits” is unbelievably shallow because we have near zero focus on deficits throughout the private and current account sectors which are more relevant drivers of economic activity. The entire focus is on public deficits in isolation, and of course no distinguishing between currency issuers and users

The group Fix the REAL Debt aims to change this. Please “Like”

http://www.facebook.com/pages/Fix-the-REAL-Debt/509295442446051?fref=ts

You’re speaking gobbldey-gook, but thanks for playing!

Is there a more succinct description of the Austerians/ R AND R debate?

SOURCE: WIKI ENTRY FOR LEON FESTINGER

“Festinger and his collaborators, Henry Riecken and Stanley Schachter, examined conditions under which disconfirmation of beliefs leads to increased conviction in such beliefs in the 1956 book When Prophecy Fails.Rather than abandoning their discredited beliefs, group members adhered to them even more strongly and began proselytizing with fervor……..

Festinger and his co-authors concluded that the following conditions lead to increased conviction in beliefs following disconfirmation:

1. The belief must be held with deep conviction and be relevant to the believer’s actions or behavior.

2. The belief must have produced actions that are difficult to undo.

3. The belief must be sufficiently specific and concerned with the real world such that it can be clearly disconfirmed.

4. The disconfirmatory evidence must be recognized by the believer.

5. The believer must have social support from other believers.[52]

Festinger also later described the increased conviction and proselytizing by cult members after disconfirmation as a specific instantiation of cognitive dissonance (i.e., increased proselyting reduced dissonance by producing the knowledge that others also accepted their beliefs) and its application to understanding complex mass phenomena.[53]”

I agree – my concern over many years has been that economics doesn’t use ‘data of ordinary lives’or examine the ideology of ‘tough love’ that justifies this. The ‘guys at the helm haven’t a fucking clue’ is an understatement – they seem to abhor solutions that would take the power of poverty away from them.

We know before we dump EU onion surplus into Senegal that we will shatter the local onion economy – but we do it. We have faith that market forces will replace jobs and social structure in systems like this or, say, the collapse of UK shipyards and manufacturing generally. On actual data the faith is very questionable.

We seem to be able to raise money for dud projects like Facebook and Netflix (selling access to crud quicker) and assume rational social-economic planning is the route to Soviet Paradise. We have even turned higher education into a debt peonage trap of unemployment and under-employment even in ‘booming’ economies like China (The Ant People).

I suspect that economics is the technology that denies the creation of self-sustaining community. At heart is the denial of sharing this competitive advantage for the quality of human living. We send our kids into more or less useless higher education to better them, yet our solution for the poor is to make them poorer to ‘inspire’ them into innovation. If we modernised third world agriculture we’d effectively murder those rendered unemployed. Economic solutions to unemployment are like the Black Death. Mineral and oil exploitation don’t look that different from ‘Red Rubber’ days.

We all think we understand belt tightening, but these days one could cut household outgoings and consumption just as the powers that be stiff you with the Cyprus template and you discover it would have been better to have spent, spent, spent!

Stephanie’s thrust in analysis is the right one. One aspect of the global spreadsheet concerns the “profitability” of the reserve army of poor unemployed, under-employed and often miserable. All we can state as “profit” is the threat maintained against those having it better in work and the role in global wage arbitrage of this “excess carbon footprint”. I want a global spreadsheet written in terms of what actually goes on. Balance sheets increasingly exclude more than they contain ($3.5 billion is currently off that of Netflix).

We know austerity usually follows wads of bad lending by banks we would except, in all simplicity, to go bust – they rarely do. These bad lending decisions are repeated time and time again – so much so one can only believe these are not bad decisions at all for the banks and that they have access to a balance sheet we never get to see. Just as misery and death caused by austerity are off balance sheet, we don’t get to see how pre-austerity lending is written-off and profited from. One of Miami Vice’s darker episodes suggests the drug-trade as the mechanism, but I suspect a combination of looting, asset-grabbing in fire-sale conditions and tax losses. I don’t see this as conspiracy in a world in which microfinance can be the prelude to a land-grab.

Is there a good layperson definition of austerity out there? For those of us who don’t have time to follow the intricacies of the academic disputes, I’m not sure the term austerity possesses any useful meaning whatsoever.

What matters is how we spend money – do we invest it in productive outlays (like social insurance and infrastructure), or do we squander it in waste and corruption (like AIG and pornoscanners)? What we have done over the past several years is not austerity in the sense of spending less money or balancing the federal budget within arbitrary 12 month time periods.

Quite the opposite, we have spent truly massive sums of money in almost unprecedented ways, from permanent non-war war to permanent bailouts-but-everything-is-fine.

Good question. I can only talk about what I directly perceive. The austerity regime currently holding power in the West is not an economic plan that we should cut costs, save money and live simpler lives. It is a political agenda that moves power and wealth away from the middle-class towards the emergent oligarchy and the international bureaucracy that sustains that class. It has nothing whatever to do with economics. Austerity should cut wasteful spending and emphasize investing–the fact it does not means it the agenda has nothing whatever to do with economics.

There are clear rational plans out there that are ignored by everyone. The way out of this crisis is not hard but the crisis is being used for political gain with a long term agenda leading to some kind of feudal future.

Thanks for the replies, I appreciate hearing the different perspectives.

You are asking the $64,000 question. I don’t think the academic papers are driving the policy so much as they are being used to justify pre-existing beliefs – ie, confirmation bias is at work in a big way. People who come into this believing thrift==good simply latch onto the economic analysis that supports their position. This is especially true when you have a field like economics where predictions are frequently wrong and there isn’t complete agreement among practitioners.

Politicians simply go where the votes are – they reflect their constituents. They latch onto analyses that confirm their constituents beliefs and help them get re-elected. Bottom line: the anti-austerity crowd is going to have to do a _much_ better job of explaining their case in laymans terms. It might help to have some big, visible projects so people have a sense of where the money is going instead of zillions of smaller ones that leave people wondering.

Austerity is the premise of putting government finances on a “fiscally sustainable path” where debt/GDP ratio declines sufficiently that markets (the investor/speculator/CEO class) gains confidence taxes won’t have to go up to pay off debt, and start spending.

“So what does it show? Basically, that the economy tends to go into recession whenever fiscal policy becomes too tight — a point made routinely by contributors to this blog.”

That may be a case of correlation not causation. Be careful.

I mean debt for a given year is revenue – expenditures, and our progressive tax system lends revenue to be leveraged relative to economic output.

And Government expenditures are a minority component of overall GDP and it’s doubtful that it is a huge lever on private sector growth.

So is the tail wagging the dog or is it the other way around?

More food for thought, typically when a recession hits there is typically large indications of malinvestment (read inneficiencies), so why would government throwing ever greater money at the economy help as recession points are approached, it would only exacerbate that problem which many believe is the root of recessions, not government spending.

Inneficiencies get too great and so the system as a whole slows down, thus reducing revenues,meanwhile government spending doesn’t adjust much and debt to GDP heads the other way.

That’s what I see in the second chart.

And Government expenditures are a minority component of overall GDP and it’s doubtful that it is a huge lever on private sector growth. Tim

Deficit spending by the monetary sovereign provides interest so that private debt can be repaid in aggregate.

Or are you opposed to the population being able to pay their debts; debts they were driven into by the government-backed banking cartel?

Malinvestment? According to what version of Austrian Business Cycle Theory?