By Tatiana Didier, Research Economist, Office of the Chief Economist for Latin America and the Caribbean, World Bank, and Sergio Schmukler, Lead Economist at the World Bank. Originally published at VoxEU.

The growth of China and India’s financial sectors is hard to ignore. This column presents a new dataset on domestic and international capital raising activity and performance of the publicly listed firms in China and India. The data suggest that expanding capital markets might tend to directly benefit the largest firms – those able to reach some minimum threshold size for issuance. More widespread direct and indirect effects are more difficult to elucidate.

Lambert here: Dunno. Warren Mosler’s sig: “The financial sector is a lot more trouble than it’s worth.”

China and India are hard to ignore. Over the past 20 years they have risen as global economic powers, at a very fast pace. By 2012, China has become the second-largest world economy (based on nominal GDP) and India the tenth. Together, they account for about 36% of world population.

Their financial systems have also developed rapidly and have become much deeper according to several broad-based standard measures, although they still lag behind in many respects. For example, stock-market capitalisation increased from 4% and 22% of GDP in 1992 to 80% and 95% of GDP in 2010 in China and India respectively. By 2010, 2,063 and 4,987 firms were listed in China’s and India’s stock markets. Their financial systems have not only expanded, but also transitioned from a mostly bank-based model to one where capital markets have gained importance. Equity and bond markets in China (India) have expanded from an average of 11% and 57% of the financial system in 1990-1994 to an average of 53% and 65% in 2005-2010 in China and India (see Eichengreen and Luengnaruemitchai 2006, Neftci and Menager-Xu 2007, Chan et al. 2007, Shah et al. 2008, and Patnaik and Shah 2011).

But how much has this overall expansion in capital markets implied a more widespread use of those markets? Has it allowed different types of firms to obtain financing, invest, and grow? Do the cases of China and India show that the policies to promote capital-market development might be conducive to growth? If so, how inclusive is this growth? Is it associated with some convergence in firm size, with smaller firms benefitting the most? Or are China and India cases of growth without finance?

New stylised facts

To study these questions, we assemble a unique and comprehensive data set on domestic and international capital raising activity and performance of the publicly listed firms in China and India (Didier and Schmukler 2013). In particular, we match transaction-level information on equity and bond issues with annual firm-level balance sheet information. Our matched data cover 2,458 firms in China and 4,305 in from India between 2003 and 2011.

This new dataset allows us to document important stylised facts:

- The expansion of financing to the private sector in China and India has been much more subdued than the aggregate numbers of financial depth suggest.

Although capital raising activity in equity and bond markets expanded substantially in 2005-2010, it remained small as a percentage of GDP.

- Importantly, this expansion was not associated with widespread use of capital markets by firms.

For example, the number of Chinese firms using equity markets to raise capital per year increased from 87 to 105 between 2000-2004 and 2005-2010, out of an average of 1,621 listed firms.

- Not only have few firms made recurrent use of equity and bond markets, even fewer firms have captured the bulk of the capital market financing.

For example, the top ten firms in China and India captured between 43 and 62% of the amount raised in 2005–10.

- Thus, capital markets have not been a significant source of financing across firms.

This contrasts with the perception in the literature that equity markets in these countries, and particularly in India, are relatively well-developed.

- Firms that use equity or bond markets are very different – and behave differently than – those that do not do so.

While non-issuing firms in both China and India grew at about the same rate as the overall economy, issuing firms grew twice as fast in 2004-2011.

- Firms that raise capital through equity or bonds are typically larger than non-issuing firms initially and become even larger after raising capital.

Firms grow faster the year before and the year in which they raise capital.

- The evidence on firm size and growth has important implications for the firm size distribution of listed firms.

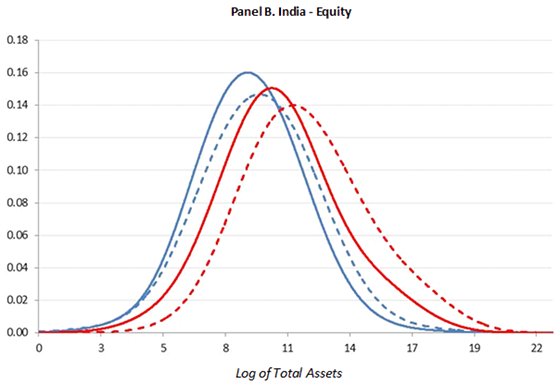

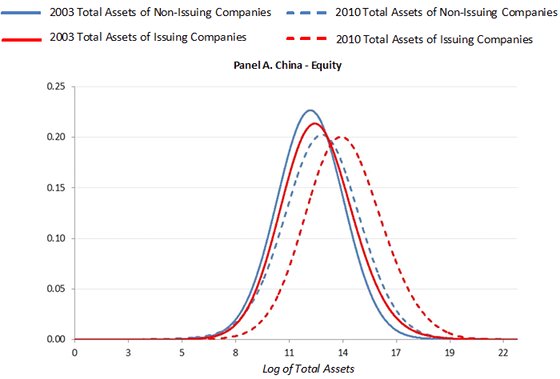

The distribution of issuing firms is tilted to the right and shifts more over time than the distribution of non-issuing firms, suggesting no convergence in firm size. If anything, the distributions seem to diverge (Figure 1).

Figure 1. Firm size distribution

Note: The panels of this figure show the estimated Kemel distributions of the log of total assets (in2011 US dollars) for issuing and non-issuing firms in 2003 and 2010. User firms are those that raise capital through equity between 2004 and 2010, and non-users are the other firms in our sample. All firms with capital-raising activity in 2003 are excluded from the sample in this figure. Only firms with data on total assets in both 2003 and 2010 are included in this figure.

Contribution of the results

These results are relevant to many discussions in economics:

- First, a large number of studies argue that financial development is positively associated with overall economic growth (Levine 2005, Beck et al. 2013).

Most of this finance and growth literature focuses on the size of the financial systems by analysing aggregate measures. Our results suggest that, to the extent that capital-market financing spurs growth, it does it through few firms and through an expansion of their investments. These results also show the mechanics that connect finance and the corporate sector.

- Second, China and India have generated significant interest because they do not appear to fit the predictions of the law, finance, and growth literature, according to which more developed legal and financial systems spur growth (Allen et al. 2005, 2012; Yao and Yueh 2009).

China is the most cited counter-example to this literature because it is one of the fastest growing economies in the world and it is not clear which sources of financing propel the fast growth of its private sector. Our findings provide evidence on the positive association between the use of capital markets and firm performance.

- Third, other work studies Gibrat’s law, which states that firm size and growth are independent and that the firm size distribution is stable over time and approximately log-normal.

This view has been challenged over time. Although the growth of large firms seems independent of their size, including smaller firms in the analysis typically introduces a negative relation between growth and firm size. Moreover, the distribution of young firms is skewed to the right (most of the mass is on small firms) and the skewness tends to diminish monotonically as firms age and become larger (Cabral and Mata 2003, Angelini and Generale 2008).

Our findings suggest that even among the publicly listed firms, which consist of the largest firms, there is some heterogeneity: firms that use capital market financing are larger to begin with and grow faster than non-users. In fact, our results indicate that there is no convergence in firm size. Moreover, a misallocation of capital in China and India (Hsieh and Klenow 2009) might have kept large, highly productive firms artificially small, which might explain why they are the ones that grow the most when financing becomes available.

Policy implications

The findings suggest that finance matters, but in more nuanced ways than previously thought. Even though the financial markets in China and India are not yet fully developed, the firms that are able to raise capital do seem to benefit from it, particularly in their overall expansion. In other words, at least part of the high growth in these countries seems to come from the firms that are able to raise new funds from the markets.

Moreover, the findings suggest that even the large, publicly listed firms (that arguably have access to formal markets) appear to be partly financially constrained. The results of differentiated performance between users and nonusers of capital market financing suggest that firms that issue securities are sensitive to the external capital raised. That firms perform differently and expand when they raise capital also suggests that they had investment opportunities ex ante that they could not realize. While we show that capital raising activity is related to changes in firm dynamics, we do not analyse to what extent the effects are driven by the supply side (the capital market side) or the demand side (the firm side). Doing so requires further research.

In recent decades, many emerging economies have undertaken large efforts to increase the scope and depth of their capital markets and to liberalise their financial sectors as a way to complete and increase the provision of financial services. But expanding capital markets might tend to directly benefit the largest firms – those able to reach some minimum threshold size for issuance. More widespread direct and indirect effects are more difficult to elucidate.

For the broader set of emerging economies, these findings suggest that even in fast-growing China and India with plenty of growth opportunities, receiving large inflows of foreign capital, and with thousands of firms listed in the stock market, only a few firms have directly absorbed the capital market activity. This could suggest that it might be difficult for a broad set of corporations from smaller and slower-growing countries to benefit from capital-market development.

References

Allen F, R Chakrabarti, S De, J Qian, and M Qian (2012), “Financing firms in India”, Journal of Financial Intermediation 21(3), 409-445.

Allen F, J Qian and M Qian (2005), “Law, finance, and economic growth in China”, Journal of Financial Economics 77(1), 57-116.

Angelini, P, Generale, A (2008). “On the evolution of firm size distributions”, The American Economic Review 98(1), 426-438.

Beck T, H Degryse and C Kneer (2013), “Is more finance better? Disentangling intermediation and size effects of financial systems”, VoxEU.org, 8 April.

Cabral L and J Mata (2003), “On the evolution of the firm size distribution: facts and theory”, The American Economic Review 93(4), 1075-1090.

Chan, K, H G Fung and QW Liu (2007), “China’s Capital Markets: Challenges from WTO Membership”, Edward Elgar Publishing, Cheltenham.

Didier, T and S Schmukler (2013), “The financing and growth of firms in China and India: evidence from capital markets”, World Bank Policy Research Working Paper 6401, also forthcoming in Journal of International Money and Finance.

Eichengreen, B and P Luengnaruemitchai (2006), “Why doesn’t Asia have bigger bond markets?” in Bank for International Settlements (ed.) Asian Bond Markets: Issues and Prospects.

Hsieh, CT and P Klenow (2009), “Misallocation and manufacturing TFP in China and India”, Quarterly Journal of Economics 124(4), 1403-1448.

Levine, R (2005), “Finance and growth: theory and evidence” in Aghion, P, Durlauf, S (eds.) Handbook of Economic Growth, Elsevier, Amsterdam.

Neftci, S N and M Y Menager-Xu (2007), China’s Financial Markets: An Insider’s Guide to How the Markets Work, Elsevier Academic Press, London.

Patnaik, I, Shah, A (2011), “Reforming the Indian financial system”, NIPFP Working Paper 2011-80.

Shah, A, Thomas, S, Gorham, M (2008), India’s Financial Markets: An Insider’s Guide to How the Markets Work, Elsevier, Oxford.

Yao, Y, Yueh, L (2009), “Law, finance, and economic growth in China: an introduction”, World Development 37(4), 753-762.

Capital markets make sense when capital is disbursed and accounting is transparent and fraud is discouraged by law and determined regulation. None of these conditions seems to exist today anywhere in the world. Capital markets are simply casinos and participants on both sides are merely running cons. It isn’t surprising that academics fail to understand this.

I am a bit jaded when I read an article like this. All this research coming up empty handed, still in the fog, unsure and inconclusive.

I think it also should be explicit regarding the sectors of business studied as opposed to one lump. it also should differentiate between financial capital and industrial capital, hard assets and paper assets etc.

Maybe I am just too slow to pick up the distinctions in the text – or that definitions are being blurred – Like Free-Market as defined as anything goes today instead of it’s classical meaning as a market free of economic rents.

More than 50% of India’s economy is underground/black market. Studies that do not account for that fact are very likely to reach erroneous conclusions. I suspect this paper is one such example.

I wonder how much of their findings are due to the difference between domestic and international funds flowing into equity markets. I suspect that international funds tend to concentrate their investments in large, visible corporations in emerging markets for several reasons:

1) they’re the only ones big enough to absorb a decent amount of investment and thereby justify the expense of paying for ongoing analysis, etc.

2) Most foreign funds probably come through straight index investing

3) Perhaps most importantly, being a foreigner means you don’t understand the local companies as well as the locals do, so you avoid (or aren’t able to do) the type of deep analysis that would allow you to take profitable positions in smaller or more specialized companies and industries.

Most domestic investment in India and China is probably in real estate (not to mention Gold, at least in India). This is partly because quite a bit of India’s wealth (at least) is black money that can’t be invested in public stocks or bonds but can easily be hidden in private transactions like real estate.

Thus, despite their size, I would speculate that India and China’s stock markets are disproprionately funded by foreign funds which means only the most successful and largest firms have access.

Hello!

I think you need to read three very good books about China’s financial capitalism:

Red Capitalism by Carl Walter and Fraser Howie published by Wiley. By readed this book, you can see there aren’t something like a “free” financial market in China…

http://www.amazon.fr/Red-Capitalism-Financial-Foundation-Extraordinary/dp/1118255100

Another good book is Capitalism with Chinese Characteristics: Entrepreneurship and the State by Yasheng Huang, published by Cambridge university press

http://www.amazon.fr/Capitalism-Chinese-Characteristics-Entrepreneurship-State/dp/0521898102

And the last, and i think the deepest of the three, is China’s Development: Capitalism and Empire writted by Michel Aglietta and Guo Bay ( Routledge).

Sadly, it’s the more expensive, but the more informative about ALL part of Chinese capitalism…

http://www.amazon.fr/Chinas-Development-Capitalism-Michel-Aglietta/dp/0415535026

As Michel Aglietta is a french heterodox economist, if you can, read it in French: La voie Chinoise: Capitalisme et Empire, published by Odile Jacob.

http://www.amazon.fr/Voie-chinoise-Michel-Aglietta/dp/2738128467

Corporate India has an inside problem. They are a bit unethical. Here are a few problems that Corporate India faces: http://abigbrother.com/index.php/2013/05/cleaning-up-corporate-india/