Your humble blogger generally refrains from writing about stocks for a host of reasons. First, there are tons of sites that cover equities actively, sometimes frenetically, with the authors typically money managers (raising the question of whether the stock or idea that they are pushing is talking their book, and worst, not because it’s a position they’ve taken and are keen about but one they are in the process of exiting). Second is that one can make the same comment about stock forecasting that one makes about forecasting generally: if you must do it, do it often (as in hope your new wisdom blots out the memory of the inevitable bad calls).

But for me, maybe the biggest reason for my lack of a strong interest in the stock market is the direct result of first real job in stock and bond underwriting. You may recall the famous saying by Bismark, if you like law and sausages, you should never watch either one being made. Well, for me, having watched how securities are made has reduced my appetite for them. I’m of the Amar Bhide school, that equities have so little in the way of rights (you get a dividend when management has the dough and is in teh mood to pay one, and you have a vote than can be diluted pretty much any time) that they aren’t suitable to be traded on an arm’s length, anonymous basis (his argument, and I concur, is that an equity investor should have a VC-like relationship with management, he should know management personally and have access to competitively-sensitive information, such as the company’s strategies and plans).*

However, the US equity markets have come to play an outsized role in the US from a policy and practical level. It’s never a good idea to try to assess complex phenomena with a single metric, yet for much of the public and the officialdom, the level and trend of the stock market is a proxy for the health of the economy (this view seems to have become even more entrenched over time, with the dot-com era allowing for intra-day dissemination of prices and Greenspan’s personal obsession with stock prices as contributors). So as the Greenspan and Bernanke puts attest, policymakers now have a vested interest in keeping the stock market up, both to boost confidence and out of personal vanity (if the stock market were to fall, that would mean they’ve done a bad job. Can’t have that!).

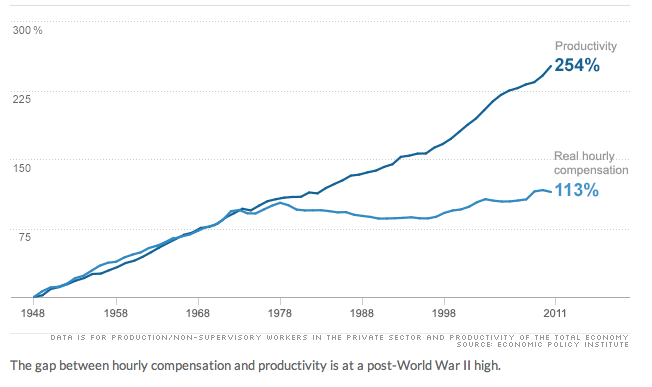

Another factor is that the stock market has played a significant, and all and all, not healthy, role in the restructuring of the economy. Without going into a longer form history (which would go back into the 1970s), a key development was the rise of share-price linked pay (a vogue that came out of a Michael Jensen paper in the early 1990s which he has since repudiated). That intensified and institutioanlized a trend towards short-termism and underinvestment (any investment also has associated up front-expenses, which will affect earnings before the investment pays off. See this paper for a longer discussion). When I was briefly in the business of playing a bit part in creating securities to be sold to the public in the early 1980s, it would have been seen as an extreme view to contend that companies should be run to suit shareholders over everybody else. Equity is a residual claim: payments to shareholders come after paying suppliers and employees, bondholders, leases and licenses, legal claims, and taxes. But our new ideology is that the last should come first. And to achieve that, companies in the US have abandoned the model of sharing the benefits of productivity gains with workers:

As this trend has accelerated, we’ve also seen falling levels of corporate investment. As I noted in a 2005 article, companies were net savers, which was unheard of at any time other than in a recession (the corporate sector is normally a net borrower in order to help fund expansion), as well as the rise in profit share of GDP relative to the amount of GDP growth paid to workers. It turns out those two developments were not unrelated. Not sharing wage gains with workers makes it less attractive to invest, leading to lower GDP levels. I’d argued in 2005 that companies were like neurotic bodybuilders, creating perfect-looking outsides while ruining their health. In an important Angry Bear post, Edward Lambert modeled that these two behaviors are intrinsically linked: lower labor share lowers investment returns. And at lower investment return levels, companies will indeed invest less (even before you get to the fact that short-termism also leads them to seek inappropriately high return levels).

And it’s even worse than this bloodless analysis suggests. Readers know all too well of the have and have-not world of work in America. People who are employed at reasonable to good income levels for the most part think the economy is fine. But people who are out of work or have unstable employment know how bad conditions are. Cohorts that traditionally held up well in bad times, such as new college grads, are having a particularly rough time.

And that recognition that we have a two-tier economy is finally reaching the consciousness of our generally oblivious elites. Admittedly, Larry Summers is on his best behavior these days as a result of campaigning to become the next Fed chair (I saw Summers speak when he was similarly pumping to become head the World Bank, and the contrast with his off-the-charts arrogance at an INET conference was remarkable). Summers, yes the same Summers who as Stephanie Kelton reminds us at DE Shaw had no compunctions about coming up with trading strategies that would rip off pension funds warned participants at a recent conference that he thought corporations had pushed profits at the expense of labor as far as they could go. More would be socially destabilizing. And I gather he didn’t mean “socially destabilizing” as in more homelessness, but in class-based violence.

This backdrop helps explain puzzled sightings by astute commentators, such at John Authers at the Financial Times, who provides an important piece on what he calls “profitless stocks“:

According to Bloomberg data, trailing 12-month earnings per share for the S&P 500 are 16 per cent above their level of October 2007 (when both earnings and share prices peaked before the financial crisis). On the same basis, earnings for the MSCI EAFE index, covering the rest of the developed world, are down 37 per cent. Those for the FTSE-Eurofirst 300 are down 42 per cent.

Earnings for the MSCI emerging markets index are up since October 2007 – but by only 13 per cent, having peaked and started to decline two years ago.

Look closely at the raw numbers for the US (with thanks to the regular Equity Market Arithmetic research produced by Société Générale’s Andrew Lapthorne), and they turn out to be less inspiring. S&P 500 companies are on course to increase earnings by 3.6 per cent year on year for the second quarter. But they have declined by 1.3 per cent once financials are excluded. During those 12 months, bear in mind, the S&P gained 18 per cent, and its financials index gained 33 per cent.

Other factors to consider:

That 16% trailing EPS gain is nominal. Inflation, as measure by the CPI since 2007 is a smidge under 13%. Even in a world of ZIRP, that’s hardly much return for equity risk.

We’ve had a couple of good quarters of S&P earnings. Is this really a recovery or just a bit of an outlier?

Authers points out that companies are guiding earnings expectations lower, while managing to produce the “aha” of upside surprises relative to that. And here is his zinger:

US companies are not generating that much in revenues but, over the past 12 months, they returned a record amount of it to investors, according to JPMorgan. This is an admission that they see few opportunities to invest for growth. But, in an environment where investors take little on trust and are desperate for a yield from anywhere, it has helped the rally keep going. This is not a strategy that can last forever. At some point, companies must start generating more revenues and profits with which to make these payouts.

Now of course, this behavior can continue until it doesn’t. Large companies are siting on boatloads of cash, so many can continue to buy back stock for quite some time.

While economists in the US are becoming more positive about the outlook here, Warren Mosler by e-mail says that he thinks they’ve misread the impact of deficit cutting in combination with no growth in private sector borrowing. Bridgwater Associates argues in a new report that the developed world will be the driver of growth (meaning the US can’t look to it as much as in the past to help lift global growth) and Europe, which is hardly robust, faces further headwinds as a result of the Basel III requirement that Eurobanks shrink their balance sheets by €3.2 trillion by 2018. Of course, if you are fundamentally oriented, as I am, it’s hard to wrap your mind around a market where the authorities have aggressively and deliberately been manipulating the dials and now are saying they’ll do that less going forward.

Keynes warned of the American’s susceptibility to overly speculative capital markets:

Even outside the field of finance, Americans are apt to be unduly interested in discovering what average opinion believes average opinion to be; and this national weakness finds its nemesis in the stock market. It is rare, one is told, for an American to invest, as many Englishmen still do, “for income”; and he will not readily purchase an investment except in the hope of capital appreciation. This is only another way of saying that, when he purchases an investment, the American is attaching his hopes, not so much to its prospective yield, as to a favourable change in the conventional basis of valuation, i.e. that he is, in the above sense, a speculator. Speculators may do no harm as bubbles on a steady stream of enterprise. But the position is serious when enterprise becomes the bubble on a whirlpool of speculation. When the capital development of a country becomes a by-product of the activities of a casino, the job is likely to be ill-done.

And I’ve never liked the idea of going to a casino. Why play when I know the house always wins?

____

* Please don’t try arguing that the stock market is indispensable to the financing of business. Bhide is a professor of entrepreneurship and has been investigating the funding of new ventures for the nearly 20 years. Suffice it to say much of the work ex Bhide suffers badly from “drunk under the streetlight” in that research focused on VC backed companies which are only about 1% of all startups, and only about 25% of the biggest, fasting growing companies (Bhide uses the Inc 500 as his proxy). Moreover, there are other regimes, most notably the German Mittelstand, of high growth, internationally competitive, innovative companies, which came out of a completely different funding model than is present in the US. Yes, the stock market is now important in the US, but to argue for some sort of stock market manifest destiny is a big overreach.

I read an article a few years ago–can’t cite it, but I think it was published in Barron’s–that held that most of the money made over the lifetimes of companies that go public was made by the organizers and VCs. The public gets the dregs of the deal. One might argue that the stock market permits easy diversification, but…how many really use it for that purpose?

Stark. Refreshing. As always, a gripping read that provokes the thought, “Why doesn’t everyone see this?”

But what does the average investor, with no influence, much less leverage, on either policymakers or company boards, do?

This kind of crazy thinking ruins perfectly good businesses. I’m personally involved in the restructuring of two companies which started off in 2000’s as solid, well regarded and generally well managed enterprises. They operate in mature sectors so while there is some limited organic growth (which is also susceptible to cyclical variances) there’s never going to be any magic formula to achieving significantly above trend growth when compared to the underlying economies which support these corporations.

So, any fool could see that promising “to increase shareholder value by 10% per year” and “double digit returns to shareholders annually” could not be delivered for more than a few years at best.

Even the most inefficient business practices have upper limits to the efficiencies which can be introduced e.g. new technology gives you an improvement, but it’s a one-time-only. Sweating assets can only be sweated so much (and often shorten asset life or asset quality). Grabbing market share through “suicide” pricing can be done if you’re head and shoulders above the other market players, but if they’ve got similarly deep pockets (and there’s more than one or two of them) they can outlast you in a game of chicken.

Unless sanity dawns, these business can (and did) end up taking more and more risks. Dubious suppliers were used which caused major embarrassment product recalls — and compensation. Capital expenditure was so curtailed that it wasn’t only in the back office where premises upkeep was obviously not being performed — the customer space showed it too. And then there was labor — shafted, basically.

I must confess though, although I could extrapolate the inevitable results of this obsession with producing quarterly results which “delighted” investors but hid all manner of nasties, the fall from grace took 10 years for one of the businesses, 7 years for the other. I’d reckoned 5 tops. So the problems can be hidden by management for a long time.

But only for so long. Now you have two retail type operations which operate from shabby often falling-apart stores with a backlog of infrastructure spending as long as your arm, poorly skilled (the skilled ones chucked out or walked long ago) staff who largely don’t give a toss and, worse, actively pick up on the pretty much corrupt management values which have been inculturalated (if that’s a word) for so long that they’ve become part of the furniture and, given half a chance will perpetrate petty thefts and frauds and divert a lot of their energies to playing the system — the management hired a lot of consultants who brought in a lot of systems, many eminently “playable” with a little thought by the employees to their own advantage.

Enticing customers into these depressing and bleak outlets takes rock bottom pricing policies. Meanwhile, competitors who weren’t quite so brazen and slavish in following this crazy trend pick away at the edges and error the market share a percent or two a year. I can’t tell yet whether the corporations so devoted to shareholder returns are in an irrevocable death spiral — they are very big players and unlikely to encounter an extinction level event because it would have to be absolutely huge. But a lingering, slow decline into oblivion isn’t out the question.

I won’t even go into the financial engineering which is corrupting the balance sheets, let’s just say an accountant could spend a happy career trying to unpick the convoluted and opaque leaseback deals, CapEx depreciation shenanigans, strained capitalisation rules, weird accruals, hedges, repos and derivatives skeletons which are buried there. Oh, and auditors which are in the pockets of the management make any oversight meaningless too.

The main problem is though that it take so-ooo long to see the damage. A generation or two of top management can get away with it (and the looting) and be off before its apparent.

Concur in Toto.

Everything is inverse, mean reversion arrghhh… electrons of price dictating everything at onset regardless of utility, sustainability or externalities… FFS.

skippy… humanity reduced to price scanners… sigh.

Robert Cringely ran an awesome set of columns a while ago showing how IBM is following the exact same trajectory, essentially eating itself into nothingness for the sake of goosing the share price and letting the executives cash out. Here are some links. Fascinating (and sad, for people who admire the American industrial titans of olde…), especially the comments from current and former IBM’ers.

http://www.cringely.com/2013/07/25/the-new-ibm-vampires-in-our-midst/

http://www.cringely.com/2012/04/18/not-your-fathers-ibm/

There’s many more if you peruse his archives.

I think ‘inculcated’ is the word you were after.

Good post.

Amar Bhide is basically recommending what Mohammed recommended. If you’re going to own part of a company, it must be a meaningful ‘part interest’, not just a fungible certificate.

Old wisdom is best!

I think there is a possibility for a contrarian view on this and its based on the fact that sometimes the past is not a good indicator for the future and certain trends are developing which I think may upset the apple cart. Namely that some of the American austerity business models are falling out of favour globally.

Like Clive I have seen many firms hollowed out over the past giving short term returns to investors and I don’t disagree with Yves that equity markets really make no sense. Real investors are begining to wise up to the cut corners, cut costs, cut wages, automate everything, out source it, austerity business model. Some successful firms these days are innovating into different areas of business (investing in research instead of cutting costs), improving service (using automation as a tool not as an answer), concentrating on quality at the right price point (building reputation), and investing in the knowledge base of the work force.

Just because its a casino now does not mean it will be in the future and I think that there are one of two promising signs that change is coming.

Nice work, but it is pure bs to suggest that public companies are run in shareholder interests. They are run in executive interests. The idea is to fictionalize accounting, evoke enthusiasm among herd driven money managers, boost the stock price, and enable top management to cash out cheap stock and free options. The hollowing out of investment is a logical loot driven strategy, probably developed at McKinsey and Harvard Business School. Employees are just disposable ciphers. Companies can always find them if they ever need them. Corporate big idea is to keep getting bigger and bigger, find a way to monopolize an important market, and then collect rent.

Meanwhile, an army of overeducated nitwits is well paid to “manage” other people’s money by ferreting out trading opportunities and bullshitting one another about future earnings. The forecasts are pure guesses, since even the current earnings are fabricated out of thin air, so who could possibly know what the future earnings might be? All this would be merely silly, were it not for the fact that honest people have their savings tied up in this cesspool of fantasy leavened with fraud, and get to watch their pathetic portfolios bob around like serf boards during a tidal wave.

A person can make a small fortune playing this game and I have done it myself in the easiest way. I started with a large fortune. Good luck suckers.

The fact that stock markets are now used almost exclusively as an exit vehicle for VC/PE/founders etc. vs. raising capital to do something new/productive is all that you really need to know about it. When new capital is raised, it’s with debt issuance.

I find it perverse that (say) Apple is selling bonds to pay its shareholders (perverting the usual credit waterfall in the process)

The results tell you about incentives, which’d tell you pretty much all you need.

As I view the stock market, it is one big auction house. Every one can bid. What us bidders bid on is crucial. We are bidding on the means of production of a particular member company in a global economy. If you buy all of its stock, the company is yours. No fooling. So, for example, when the value of 500 cherry picked companies is tracked by a stock index like the S & P 500, one is tracking the true instantaeous measure of what all of us bidding in the aggregate have valued these means of production entites. These companies are the real assets that back the value of our money. According to Keynsian economic theory, the only other thing in an economy to consider is the labor. “It is my belief that much unnecessary perplexity can be avoided if we limit ourselves strictly to the two units,

money and labour, when we are dealing with the behaviour of the economic system as a whole; reserving the

use of units of particular outputs and equipments to the occasions when we are analysing the output of

individual firms or industries in isolation; and the use of vague concepts, such as the quantity of output as a

whole, the quantity of capital equipment as a whole and the general level of prices, to the occasions when we

are attempting some historical comparison which is within certain (perhaps fairly wide) limits avowedly

unprecise and approximate.

It follows that we shall measure changes in current output by reference to the number of hours of labour paid

for (whether to satisfy consumers or to produce fresh capital equipment) on the existing capital equipment,

hours of skilled labour being weighted in proportion to their remuneration. We have no need of a quantitative

comparison between this output and the output which would result from associating a different set of workers

with a different capital equipment. To predict how entrepreneurs possessing a given equipment will respond to

a shift in the aggregate demand function it is not necessary to know how the quantity of the resulting output,

the standard of life and the general level of prices would compare with what they were at a different date or in

another country.” Chapter 4, part 5 of The General Theory of Employment, Interest, and Money by Keynes.

My comment seems to have dispeared. Our views of the market differ radically.

As I view the stock market, it is one big auction house. Every one can bid. What us bidders bid on is crucial. We are bidding on the means of production of a particular member company in a global economy. If you buy all of its stock, the company is yours. No fooling. So, for example, when the value of 500 cherry picked companies is tracked by a stock index like the S & P 500, one is tracking the true instantaeous measure of what all of us bidding in the aggregate have valued these means of production entites. These companies are the real assets that back the value of our money. According to Keynsian economic theory, the only other thing in an economy to consider is the labor. “It is my belief that much unnecessary perplexity can be avoided if we limit ourselves strictly to the two units, money and labour, when we are dealing with the behaviour of the economic system as a whole” Chapter 4, part 5 of The General Theory of Employment, Interest, and Money by Keynes.

The problem I have denim is that what I’m bidding on isn’t a tangible good, like, say, an apple. If it was, I could look over the apple and make sure it was an apple, not rotten, of the right variety, not made of plastic, was actually a real physical apple not a promissory note to supply an apple. Things like that are tricky to manipulate.

For the stock market, what you’re bidding on is an earnings stream. It gets repeated so often hat we tend to ignore it that “past performance is no guarantee of future performance”. We ignore it because we’ve nothing better to go on.

Thus, if you can manipulate that earnings stream, you can manipulate the bid price. As the article documents, it’s not that difficult to manipulate the earnings stream and therefore the bid price.

No, actually you are bidding on the ownership of the company. Just because you are not as wealthy as a hedge fund or other buyout group does not change the fact that buying all of the shares makes the company personally yours. If you want to speculate on the noise that the stock price chart demostrates, you can. Doing that puts you into a casino or lottery mindset of the “retail” “investor” looking for an edge to luck out.

Except if you don’t own all the stock you don’t own anything except a casino chip. Thinking things like “you are bidding on ownership of a company” is what makes suckers.

Your man Keynes understood stock picking as being a beauty contest judge whose task was to select not the prettiest girl, but the girl the other judges would find the prettiest. He was damn good at it, too.

No, denim you are NOT bidding on control. Owning one share or 100 shares or 10,000 shares is not control.

I’ve done M&A and the market for control is completely different that retail or even institutional investors buying stocks. The fact that you are equating them is misguided.

Even activist hedge funds and powerful investors (Calpers, Hermes in the UK) have perilous little influence on corporations, much less control. Companies have erected substantial barriers against hostile takeovers, including poison pills and staggered boards.

Unless you are a heavyweight billionaire and actually can buy the overwhelming majority of the shares of a company, you are deluded. Do you even have enough money to get the attention of an M&A partner at, say, Cravath to get you started? Do you even know the names of the respected and feared M&A partners at the serious shops? I’d wager a large amount of money not.

I don’t get it. Why do you invest in a company when it is non-dividend paying and when you will never have control (or even a substantial influence)? Your sole hope of profit is for someone else to come along and pay more for the stock than you did. How is this different from, say, buying gold?

Well, your shares could combine with other shares to reach a 51% majority and you could then boot the management.

And except for the government-enforced monopoly the banks have on private money, you’d see more of the direct use of common stock itself as private money.

But as I often say, why share when you can legally steal instead?

You seem to have suppressed my reply and attempt to respectfully show that you were misunderstanding my points. It is your blog. So enjoy your (not really) last word. But tell me, what nerve did I hit that prompted the overwhelming ad hominem attack on me as though I am some know nothing rube because I am not rich, well connected, and famous?

I agree with Denim. What prompted the attack? “Respected and Feared”…seriously give me a break….with this twaddle. Perhaps you respect and fear them, the rest of us think they are overpaid egomaniacs.

Take your 100 shares and your regular attorney and see how much “control” you have. Demin argued that ordinary investors are bidding on “control” and that’s simply untrue. There’s even an academic literature on the “market for corporate control” precisely because it is recognized as different than routine buying and selling of shares.

Like it or not, obtaining control or even trying to pressure a public company entails hiring the right advisors who know the drill, which is based not just on statute but also on case law. You can try snarking at me, but you are basically shooting the messenger. I don’t like that companies have erected barriers to make it difficult to dislodge management, but they have, and pretending those don’t exist and deriding those who point that out simply confirms that you don’t know this terrain.

I thought I was making myself clear about how I viewed the stock market buyers. Perhaps you took my “bidding on the ownership of the company” more literally than I meant. Buffett says buy stock as if you were buying the company (even though you are only a micro-investor). Legendary speculator Jesse Livermore said buy and sell on the trends of the ticker charts among other tips. That is noise investing, in my view.

Let me repeat myself.

“denim says:

August 12, 2013 at 9:47 am

No, actually you are bidding on the ownership of the company. Just because you are not as wealthy as a hedge fund or other buyout group does not change the fact that buying all of the shares makes the company personally yours. If you want to speculate on the noise that the stock price chart demostrates, you can. Doing that puts you into a casino or lottery mindset of the “retail” “investor” looking for an edge to luck out.”

Honestly, I don’t know what is wrong with you, Gary, and denim.

Denim’s comment is naive and finance orthodoxy. Yves’ response was not an ad hominem. Both of your offended comments read like you are emotionally invested in the religion of stocks and don’t like Yves’ apostasy.

There appears to be some bugs in the software that causes posts to disappear, don’t take it personal.

Unless you are a heavyweight billionaire and actually can buy the overwhelming majority the shares of a company, you are deluded. Yves Smith

Wait, you mean 51% don’t you?

No, most companies have “poison pill” provisions that allow them to issue additional shared precisely to escape hostile takeovers. I’m not current on the state of the art. The big era of hostile takeovers was the 1980s, and that’s also when companies put in place their defenses. I’m sure a reader can fill in the blanks, but I can’t think of a big hostile fight for a long long time.

Pretty much every large company has staggered board elections, so even if you were to surmount the dilution procedures, it would still in theory take you three board election cycles to vote in your own board.

The battles are usually by activists, who get 10-15% blocks and push for changes (like throwing out cronyistic management and cutting spending or divesting underperforming businesses).

In practice, when you did have hostile deals, “hostile takeovers become friendly takeovers”. Once the target is convinced the predator really will win, they then start to negotiate terms with incumbent management (of course, incumbent management long ago installed golden parachutes that will be triggered in the even of a hostile takeover, another reason they eventually capitulate once they’ve determined the hostile suitor will prevail).

Finally, in some industries, hostile takeovers are impossible for regulatory reasons (as in approvals are required). For instance the last effort to launch a hostile takeover of a bank was Saul Steinberg v. Chase Manhattan in the late 1960s. Banks will also not finance takeovers of other banks unless it’s consensual.

Thanks for the thoughtful reply. Once the counterfeiting cartel is overthrown (peacefully, of course) and common stock is more widely used as private money then I’d expect the common stock of companies that abuse stock holders to be rightly spurned.

As it is now, I’d bet, the stockholders don’t complain too much because their so-called creditworthy corporations steal on their behalf too. “Ya can’t cheat an honest man?”

One day I am sure the truth will come out i.e. it’s not that QE is causing investors to buy stocks to reach for yield, etc. Rather, the Fed is buying stocks posing as “investors”. After all the BOJ have been buying ETFs. What stops the Fed from doing the same? I also recall the Hong Kong Central Bank buying large cap stocks (belonging to local tycoons obviously) to “defeat speculators” back in the 90s.

Zero evidence for now obviously, but perhaps there’s a Fed version of “Snowden” coming out someday.

The Fed doesn’t have to buy stocks. It facilitates bank lending to speculators at near zero interest rates. Same result with clean hands. Except if you look closely.

Wow…. That’s pretty amazing. The gap appears to start widening around the same time the US closed the gold window.

Could it be that the metal was indeed beneficial to the common man?

>The gap appears to start widening around the same time the US closed the gold window.

There were many more changes: Oil crises, deregulation, politics, power loss of the unions, computer revolution, automation, out sourcing. Not all at the same time, but each one may have contributed to the loss.

Unless you can make a convincing argument for the actual method of causation, the events mentioned by Uwe are much more likely causes of the decline in labor-share of revenue.

Otherwise, I will remain skeptical that artificially limiting the amount of currency in an economy on the basis of how many shiny rocks people can dig out of the ground can, in any way, be beneficial to humankind.

Gold backed money insured positive interest rates, which at least limited speculation and made the financial system less dishonest. The DM provided the same function, which is why the elite needed the Euro. Now all money is dishonest and easily manipulated by central bankers. Guess who benefits? Not you or me.

I’m pretty sure we had speculative bubbles before Nixon closed the gold-window (i.e. roaring twenties). Also, we had relatively high interest rates during the run-up to the S&L crisis, so I don’t see how you can claim that positive interest rates limit speculation or other destructive activities.

I can see no a priori reason that money should have a positive interest rate. Since most people are borrowers, low interest rates would seem to be in the interests of a greater number of people (especially now when households are still trying to de-leverage).

Easy money isn’t the problem, it’s easy money going to bankers instead of workers/consumers. We need fiscal stimulus now not more monetary stimulus, but we don’t need higher interest rates either.

You had speculative bubbles, but you didn’t have bailouts. It is bailouts which are the problem. They eliminate the downside consequences of speculation for those whom the Fed chooses to favor.

>You had speculative bubbles, but you didn’t have bailouts.

I’d attribute that to the fact that these bubbles rarely endangered the whole economy, or that at least people didn’t understand or see that risk.

But bailouts were known even in the days of bretton woods: Nixon approved the Emergency Loan Guarantee Act of 1971 on 1971-08-09, 6 days before he ended the era of the gold standard. The ELGA was just a bailout made for Lockheed. The company was able to pay back the 1.4 billion dollars in 1977, thanks to the fact that Lockheed got no fines for the bribery scandal.

I fail to remember one case where the government in question didn’t somehow bail out a company of high importance to the country or its politicians. These things are just almost never named as bailouts, and the usual way there are done around here is to give the company some new contract and “ask” some bank to give the company a new credit because of that (that’s one reason every german state had its own landesbank).

>It is bailouts which are the problem. They eliminate the downside consequences of speculation for those whom the Fed chooses to favor.

A company might be sound, even though its current situation is desperate (think of delayed payments by the state or cities – something which happens quite often around here).

Of course in most other cases a bailout should be handled by the good old bankruptcy laws.

IIRC, JP Morgan had to organize a bailout for the US government in the days of the gold standard.

There isn’t enough gold in the solar system to back the kind of money supply the world now needs. Quadrillions. If there were it wouldn’t be very precious. So Catch-22. Gold backed money is just the shortest path to total devastation. Bernanke has stated as much (my interpretation at least). His first goal was to save the banks and to do that saving the people (mortgages) were abandoned. His second goal seems to be the reflation of the stock market and all assets. Again saving the elite. And his third goal was to create enough money to fund the world without threat of bond vigilantes stealing it all. Just my brain spinning away here. So I’d just say this about Larry Summers coming to Jesus about labor: Larry wants interest rates to spike so his vulture friends can pick some bones. If he can’t bring himself to endorse QE he endorses higher interest rates by default.

The trick would be to create jobs without spiking interest rates. And besides, everybody knows the stock market is diluted and a big dog and pony show. Why not let it go to 30k? If getting money into the system is the goal how about debt jubilee? Which new Fed Head would promote that solution?

Creating jobs is not going to solve anything unless the jobs pay decently. All this slobering over jobs has greased the skids of the past thirty years. You have States giving away the store to corporations that create jobs which are not worth having. Why not build another 200,000 Walmarts? Walmart creates jobs, even as it destroys businesses and fills the world with worthless dreck.

agree.

Paper reserves in Central Banks around the world have grown from 0.5 trillion to over 11 trillion. That’s 22 times more reserves than 40 years ago. Even looking back to 2000, paper reserves were only 1.5 trillion.

Why did we “need” less back in 1971? If you look at the rate of increase in the paper reserves, you know that this can’t go on much longer and when it blows, it will blow sky high.

1970 – 0.5

1990 – 0.65

2000 – 1.5

2005 – 3.5

2009 – 7.5

2011 – 10

2013 – 11

The moral of the story is that the free market can set the supply of money and it’s value (rate). Central planning has proven not to work in Russia and many other socialist crap holes. It will not work here either.

I’m inclined to believe that, in fact, and in action, the free market did actually establish how much money was necessary to run the world; that the “third” world needed lots more money, and the “first” world needed no less than a certain amount. And that is probably where we stand today, aghast at the proliferation of money. But it is money that is necessary to run the world. So it’s a totally acceptable idea to me that this amount of money is what is necessary to run the world and not just a fool’s errand to keep the US afloat. Still it’s frustrating. Confusing. And I’m just generally pissed off.

Don’t be confused.. Money is simply a store of purchasing power. You work and produce, and for that you ask for purchasing power so that you can survive. That, you store in dollars which we entrust the government to safeguard. Printing new currency is the same as counterfeiting, but it can be done in a fiat system in which the third world and countries like China want to sell to the superpower. It seems to work for a while, but it creates imbalances, China won’t buy much from the US ever, but the US will definitely continue to buy from China. How on earth is the US work going to compete with Chinese workers?

This is possible in a fiat world where most countries are happy to hold dollars as reserves. If these countries had to trade on gold, China would never get away with just selling to the US. It would have to TRADE to do so. This is why the gap between productivity and earnings was less under the gold standard. I would vote for a gold standard tomorrow if I had the chance and so should everyone else.

I don’t think the “free market” established how much money was/is needed.

The 2008 rip off has the plutocrats getting most of the bailout monies so when the US dollar falls, they are still positioned to have complete control…..ZIRP is still bleeding us.

Is there an article out there that shows the different kinds of US Treasuries/debt and relative “pecking order” when the fall of the US dollar lines everyone up at a settlement window?

Sure it does, there were times were mining gold was profitable while other times it was not. Guess what happened to the supply of money during profitable times.

There is really no trick to fixing the economy, gold is not perfect, but it forces settlement. There hasn’t been settlement since….drums ease.. 1971. Fractional reserve, NOT gold, caused the great depression.

I have to agree with Ohse and Diptherio. Theres really no way you can prove that correlation = causation.

It may be a contributing factor, but its next to impossible to prove it was THE factor. Personally I think rising prices of oil + sociopolitical rot are larger factors.

No.

You again?

You know what Moses did to gold idolators? He ground the Golden Calf into powder, scattered it onto water and made em drink the water.

Maybe you could hunt for the latrine they used afterward and get rich?

No, correlation is not causation. Please see the economic history of the later 19th century in the US. Farmers were fighting the gold standard then precisely because it was crushing them. Go read William Jennings Bryan on how ordinary workers were being crucified on a cross of gold.

Going off the gold standard was caused by the US running persistent trade deficits. That in turn was caused by the US running persistent and unsustainably large fiscal deficits when the economy was at full employment. This blog has stated repeatedly the time you don’t want to run fiscal deficits is when employment is high. Johnson and Nixon weren’t willing to raise taxes to fund the cost of the Cold War, Vietnam, the space program and the war on poverty. We had too many fiscal commitments and Johnson basically said he wasn’t willing to raise taxes to pay for an unpopular war.

So the US went off the gold standard, which was equivalent to a dollar depreciation. That made the Saudis really mad because oil was denominated in dollars. So when they had a good excuse, the jacked up the price of oil. That gave a second whammy to the inflation that was already underway. So we had stagflation on top of declining US competitiveness (the Japanese and Germans were eating our lunch in autos and other manufactured goods and the US response was not impressive. The lower dollar didn’t do enough to solve problems of design and product quality).

So the response was to start squeezing labor. And if you go back and look at the Fed flow of funds, companies weren’t having a profit problem. This was all about 1. The flagging stock market (stocks do badly in times of high inflation) and 2. Conservative businessmen using the fact that the Keynesians (and remember, American Keynsians seriously bastardized Keynes) were discredited by by the stagflation and used it to wage a campaign against worker rights and social safety nets (the Powell memo of 1971).

Succinct summary!

I agree that budget deficits can be overdone but there should be a Constitutional Amendment against budget surpluses, sectoral balances or not, since they are a subsidy of the real purchasing power of foreigners at the expense of domestic consumers.

“made the Saudis really mad?” That’s a crock. The Saudis were created by the banks and the oil companies. It was a David Rockefeller operation with Kissinger running the point. The Saudis couldn’t have stayed in power five minutes without support of the US military, the US banks and the US oil companies, all of whom conspired to escalate the price of oil in order to drive American youth back to work and end the rebellion of the Sixties. And of course to make endless money recycling Arab deposits through the banking system and impose a regime of usury on the developing world.

You need more than business school to understand this stuff.

It all started with a King, President FDR and a translator in a closed meeting. The King thought the Jewish state should be located in Germany, crime and punishment thingy.

This did not occur, what bargain was struck, yet it has become a whale which the world is irrecoverably entangled.

skippy… how does 6,042,000 people cause so much ruckus out of 7 billionish???

Ya just had to ask, didn’t ya? Well, here ya go:

The burden of the word of the Lord concerning Israel.

Thus declares the Lord who stretches out the heavens, lays the foundation of the earth, and forms the spirit of man within him, “Behold, I am going to make Jerusalem a cup that causes reeling to all the peoples around; and when the siege is against Jerusalem, it will also be against Judah. It will come about in that day that I will make Jerusalem a heavy stone for all the peoples; all who lift it will be severely injured. And all the nations of the earth will be gathered against it. Zechariah 12:1-3 New American Standard Bible (NASB)

Oops! That stretchy universe thing again.

Funny how the answer always proceeds the question, like an advertising campaign. Nothing about suggestive projection linked to the creators will now… eh.

Personally I have no wet ink on any such contract[s. Void.

Per your earlier comment, reading the bible, yes I have in total and more, cross referenced with prodigious amounts of history in antiquity and constantly updated forensic anthropology. This is to include all classical religions and primitive… globally, with environmental, technological aspects included.

As far as I can tell… the ones that were not human centric had the best social cohesion, but, were quite unprepared to defend against the onslaught of those that were. Those that were human centric had lots of practice in this art *of conquest* due to murderess internecine warfare.

Something to do with population to land ratios and availability of resources as viewed from a social prerogative to wealth accumulation in a priori imperative.

skippy… old sales parable… boys were going to expand our market to the primitives over there and expand our base… but boss they don’t ware shoes… exactly[!!!]… they won’t know what hit them… were going to all get rich (chump change for labor and co w/beanies for a few wonder kids and the lions share for the C suite see Nike et al).

PS. this public service announcement was brought to you by Queens brand Skin Bleaching products… guaranteed to get you that job with your betters and increase your social upward mobility.

http://www.amazon.com/African-Queen-Beauty-Cream-White/dp/B00145HGHU

Seriously… look into this kind of stuff in history… its every where…

Seriously… look into this kind of stuff in history… its every where… skippy

Of course it is but you’ll have a very hard time finding any Biblical justification for it. And the Conquest of Canaan does not count since strict boundaries were put on the Lord’s land grant to the Hebrews.

Anyway, as per predicted, Israel and Iran are likely to be the cause of WW III. It’ll take a Miracle to forestall that so the logical thing to do is to assume God exists and ask for one. He might at least admire your logic and survival sense:

For whoever is joined with all the living, there is hope; surely a live dog is better than a dead lion. Ecclesiastes 9:4

The Saudis were around al long time before Aramco. Please don’t spread historical disinformation:

It was in 1150 AH that Ibn Abdul Wahab from the area of Nejd began in earnst the task of spreading his ideology. His interpretations were refuted by many scholars of the time including his own brother Shaykh Suleyman.

It was at this point that the story of the House of Saud begins, from the eastern areas of the Arabian peninsula Muhammed ibn Saud entered into an alliance with Ibn Abdul Wahab.

It is of interest that Ibn Saud belonged to the banu Hanifah tribe who where historically the people of Musaylima al Khazzab the false prophet who was fought and killed by Khalid ibn Waleed.

After the death of Muhammed ibn saud, his son Abdul Aziz took over the alliance with the movement of Ibn Abdul Wahab.

http://forum.mpacuk.org/showthread.php?11572-The-formation-of-the-House-of-Saud

By 1973, the Russians (who had been Israel’s sponsors) dropped their backing, and the US, which had tried playing honest broker in the Middle East (not sure we were all that effective, mind you) became Israel’s patron.

And it was the support of the Arabs (brokered by TE Lawrence) that was critical to the British winning WWI. The Arabs had been promised self-determination (which would include control of the area that later became Israel) but the Balfour Declaration (with the French and British governments signed with Baron Rothschild) promised the same land for the formation of a Jewish state.

There’s a lot of history here before Kissinger got on the scene. And if the House of Saud was such a bunch of passive stooges to the US, pray tell how did they implement the oil embargo?

Pricing something in dollars is actually meaningless. Oil has traded and continues to trade on other currencies, without an iota of impact on the dollar. Currencies are fungible.

I agree that Nixon did not want to fund the war by raising taxes, no administration wants to fund spending with taxes as there is an immediate pain on the population tied to the spending. The reason for the inflation of the 1970s was not entirely oil prices (although the embargo did have impact), but was also due to the cost of war.

I think we are missing the best qualities that a gold currency has to offer, and it’s not just because it’s shiny. The fact that gold is not easily created forces honest discipline. Under the gold standard all players in international trade knew that it was only possible to sell to a country that sold something else in turn. It was not possible to buy from a country that did not buy in turn. Trade was naturally balanced by this restriction. The “structural imbalances” so commonplace today were unheard of.

Under the current money regime, there will never be anything close to “full employment”, what there will be is more and more unemployment until the economy and financial system blow sky high.

Please reread the history of this period. Oil was most decidedly demominated in dollars, and the end of the Bretton Woods system and the resulting fall of the dollar resulted in a large loss of wealth by the Saudis, as the Saudis themselves complained to the US.

The US has been resistant to having oil priced in other currencies. The formation of bi-lateral pacts to conduct oil transactions in non $ currencies is seen as an attack on the dollar’s standing as reserve currency. I see this issue as a bit overblown, but some see it as a big deal.

Im a but confused. If the Saudis lost wealth, doesn’t that mean that it was their wealth (already sold oil) that lost value? Just like all else, oil prices will rise as the currency depreciates but like all investments it’s not a profit until you sell.

If they had too much wealth stores in dollars, they took the risk and deserve the outcome.

Do you understand what the end of Bretton Woods meant? Currencies were all pegged at various rates to gold, which meant they were also pegged de facto at fixed rates to each other.

In a fixed rate regime, your “what currency you hold something in” is a non-concept. You don’t really care asa a store of wealth unless some country is being really reckless and you can tell they will revalue downward. You’ll look primarily for administrative convenience (if you do a lot of business in Germany, you might prefer DMarks just to save on transaction costs, or you think you have a insider advantage and can pick German companies better than you can pick US or English companies to invest in). You are projecting floating rate regime concepts back on the fixed rate era.

What Nixon did (the “Nixon shock”) was destroy the entire currency REGIME. How would you feel if you held gold, and had been told over and over again gold (or in this case, the dollar) was the foundation of the currency regime (the reserve currency and therefor the best to hold) and then the next day someone says “You know, that gold you own which has been $1000 an ounce by statute and international agreement for the last X years? Last night while you were sleeping we tore up all those rules and now it’s $600. Have a nice day.”

“You know, that gold you own which has been $1000 an ounce by statute and international agreement for the last X years? Last night while you were sleeping we tore up all those rules and now it’s $600. Have a nice day.” Yves

The Sovereign governments can impose that on it’s people, who would impose that on other sovereigns? Nobody, that’s who. I’m quite surprise on this answer given your involvement in the markets, isn’t the market bigger than anyone else?

Would the US be able to stop China paying 1,000 an ounce to Russia? Gold is the answer…

Yves:

No need for them to read, lets quote it here:

“If they say bimetallism is good, but that we cannot have it until other nations help us, we reply that, instead of having a gold standard because England has, we will restore bimetallism because the United States has it. If they dare to come out in the open field and defend the gold standard as a good thing, we will fight them to the uttermost. Having behind us the producing masses of this nation, and the world, supported by the commercial interests, the laboring interests and the toilers everywhere, we will answer their demand for the gold standard by saying to them: you shall not press down upon the brow of labor this crown of thorns, you shall not crucify mankind upon a cross of gold.” – William Jennings Bryan

Again Labor paid . . .

Never been to a casino? A few airline sick bags are in order. They really aren’t about gambling. Money-laundering, drugs, prostitution, money-lending and suckering only begins the ethnography. You can gamble down the pub in a sweepstake with no skim by the landlord. Casinos are fee takers like lawyers, accountants, brokers and the rest of the professional class. Many of their rackets are now state and government run as lotteries at a lower rate of return to punters than Frank Nitty managed.

A big problem with shares (as we call stocks)is the fees we have to pay to be invested in them. Given investment alpha is a form of rocking horse dropping we should have a Beard-like Post Office to invest through. For that matter, we should have something similar for gamblers, machine-matching bets at low administration fees. One only has to look at “personal pension plans” against decent company ones with fees at 25% against 2% to know the whole shebang is hornswaggle. The stockmarket is really not much more than the result in the 3.30 p.m. at Haydock or perhaps more like whether a Pakistani bowler bowls a no ball on the second ball of his third over.

We are in a casino and assets are being sweated as surely as the mug punter when the boys are sent round. The fees and obscene bonus payments don’t get enough attention in terms of the opportunity costs of not having boring investment banking and organic growth. We are now as shattered as economic communities world-wide as any group at gamblers’ anonymous, though most of us never placed a bet.

It looks like the death throes of a Ponzi scheme to me. We can’t value any of the assets and pay outs have not been from productive generation but financial fabrication and new money with nowhere else to go. We’ve no doubt all seen the Keiser Report, but where is the killing analysis?

I can quote ‘I told you so’ papers from the 1970s – especially on focus on property bubbles and consequent failures to bring in new productive capital equipment. Even Drucker from about 1950 on what work restructuring usually was under the bull. In the end I’m back, after a good 30 years, to feeling like a cop with scam victims barely able to admit to me, let alone themselves they’ve been had.

The solid figures we have are that this has all been a great theft from the bottom 50% – just look at the decline in liquid assets and flat earnings. I have the average down from 14% in 1980 to 1% now. It doesn’t matter in some ways, if stockmarkets are at 5 times real value if everything else is in some kind of standard inflation, but sadly something much more rotten is at work. On price to earnings one would expect many new start-ups to be in competing on a lower cost and finance base – where are they and wouldn’t they be likely to actually depress overall jobs with more ‘efficiency’?

I can’t pick a stock to save my life – but when we ask people who have been successful they trot out what I could tell you in financial investment 101. They either keep it all secret or were just lucky individuals in the frequency distribution. My guess is that shares (stocks) are priced against a coming (existing) bear market in bonds and known over-pricing in property and financial assets – with cash inflating away under the mattress at 12% since 2008 and about to do who knows what. We can’t tell much – look at the few bank takeovers that look to be blackhole sacks – and think why they couldn’t do due diligence or whatever hostile equivalent properly. Companies have cash but aren’t conglomerating, instead buying themselves. The Chinese miracle is leading to cash and personnel exodus.

Remember when we were supposed to become much more committed workers by owning shares? Now we own debt that most will be lucky to have covered by housing and pension assets wrapped up in a potential collapse. There’s a point in housing markets when no one will sell and prices seem stable. What price any asset now if currencies go south?

Beyond this we have banks ‘recovering’ by doing the same old things and business models based on tax theft, low wages (hence no money to buy) and rent-seeking – all needing tax payer subsidies. That we need a radical employment plan on an international basis is plain – not least in stopping so-called flexible employment that means bending workers’ bcks further, cheaper and without health plan.

My Dad bought six stocks in 1982. For twenty nine years he never even opened his brokerage statements. Those six stocks, all prosaic industrials, appreciated 20 times on average during those years. Was this genius or simply luck?

Had he only had more money Roger Lowenstein would have written his biography and Becky Quick would have been kissing his ass on CNBC at the turn of the Millenium. He would have liked that.

You do realize your father was the exception right?

Like in a casino, the person who makes it big in the stock market is ultimately an anomaly.

If nobody wins the lottery, the rubes don’t play.

Luck and timing.

Had he looked in March 2009, the stocks would have only doubled. Some better, some worse, but that was the S&P number. Now that the Fed’s pumped in oceans of air, that’s much of the return.

And there’s no predicting six stocks that won’t go bankrupt in the thirty years. It is predictable the Fed will stop inflating.

Your father was just lucky. He jumped into the market as one of the greatest debt binges in all of history began and accompanying market appreciation.

[IMG]http://market-ticker.org/akcs-www?get_gallerynr=2843[/IMG]

1982 was the start of the great bull cycle. This was luck, period. He bought when Volcker created the great disinflation that lifted all financial assets, stocks most of all.

+100 – what we need is a radical employment plan!

Always with the jobs?! There seems to be a case of “Stockholm Syndrome” with Progressives: “Please Massa, can I work on your pyramid, please?”

What we need is justice, not jobs. The production problem is solved and it has been solved with stolen purchasing power. It’s time for restitution, not miserable make-work.

Great post Yves. You should write about the markets more often. Very insightful. My few cents on the issues

1) The current bull market has been driven yes by QE, low bond yields and a dearth of other opportunities, but do not underestimate the power of forward earnings expectations. Check out Dr Ed’s blog. I believe earnings growth (which is still expected for 2014) has underpinned the rally. The problem is that historically it is not a very forward looking indicator and is autoregressive

2) Ok the stock market is very much like a ponzi scheme and the average investor is at a disadvantage. But over the long -term (20 year) its hard to argue with the Jeremy Siegels. What other options to most have to do with their savings?

3) The fact that the stock market is used as a confidence measure does make sense, as businesses make investment decisions around future growth expectations and business risk. The stock market is a collective assessment of these factors. It is comical how much of the market is based on the short-term however from a practical standpoint it makes sense. Predicting what will happen in 5 years is hard to have a high level of confidence unless on the most ridiculous scenarios are priced in. In more normal scenarios its easier trying to predict what will happen tomorrow or next quarter as there are less (albeit it still numerous) variables to deal with

“And I’ve never liked the idea of going to a casino. Why play when I know the house always wins?”

That is reality . . .

for additional reading if you’re interested…

“Where Are the Customer’s Yachts” by Fred Schwed and “The Money Game” by Adam Smith (not the Scottish philosopher).

and “The Logic of Collective Action” by Mancur Olsen.

An interesting part of the wealth concentration story – the stock market is largely irrelevant to all but the top 20% or so. The top 10% control the vast majority of shares.

Which I think reveals one real use scenario for average citizens without inside information. For those in position to save a significant chunk of their wages, putting a portion of that savings in equities has been a way to ‘hedge’ the wage stagnation trend.

And it reveals an interesting policy option, too. Allowing the stock market to crash would be one of the easiest actions to reduce inequality – it would happen naturally if we simply stopped bailing out the criminals.

allowing the stock market to inflate by deflation (worth less and less) would accomplish the same leveling without all the devastation

Would you be willing to expand on that thought a bit? What is the link you see between falling stock prices and devastation?

In other words, what is the public purpose for government to artificially support asset prices when those assets are held by private actors?

Clive’s description of what happens because of our obsession with quarterly numbers is spot on. The concept of ‘continuous improvement’ as articulated by Edwards Deming, has fallen from public consciousness twenty years after Deming’s death. It fell in an odd way, being usurped by Six Sigma, which people with only a passing knowledge of the subject assumed was an encapsulation of ‘continuous improvement’ and an improvement. Jack Welch at GE, that master manager of quarterly earnings (Barron’s cover story about his shenanigans is a good read), is partly responsible. He somehow managed to mix the incompatible concepts of ‘goal setting’ and ‘continuous improvement’, rendering the result meaningless.

When looking at current reported earnings of U.S. based companies, it is worth considering the following:

1. Corporate profit margins are at or near all time highs.

2. Corporate tax revenues as a percentage of total tax revenues are at an all time low.

3. The most recent number I saw was that corporate profits are 11-12% of GDP. Warren Buffett warned in a Fortune article in the late 90’s that based on history, corporate profits of more than 6% of GDP were unsustainable. (Of course, Uncle Warren is now an unofficial cheerleader for the stock market and the economic policies of the Obama administration, but that’s another story.)

4. Stocks compete with bonds, and the Fed has used QE to push bond rates as low as possible. It has been government policy to try to force money into stocks in hopes that a rising stock market produces a “wealth effect” that causes people to feel richer, spend more money and stimulate the economy.

Given the facts above plus the characteristics of stocks that Yves accurately states, I have no interest in putting money in the stock market.

Warren is terribly fascinating.

Its amazing how so many people thinks hes a great guy for…

Essentially preaching against the very things he does and has been doing for decades. Hes part of the problem, but gets respect for being publicly against the problem. Even Eisenhower speaking about the MIC he created was less brazen.

Yeah, that makes perfect sense… Because a Priest that preaches against raping children only to do so after mass is so eminently respectable.

I suppose it depends on whether uncle Warren is buying or selling. If he’s buying, corporate profits are unsustainable, if he’s selling, things are great!

I’ve never believed he had my best interests at heart.

Great quote, Yves.

WHERE did the Keynes quote come from? (page # too)?

This shows that asset-price inflation has been the strategy for nearly a century.

Michael

To help out:

Source: John Maynard Keynes, The General Theory of Employment, Interest and Money, New York: Harcourt, Brace & World, 1936), p. 159.

Real damage is being done to the real economy by the stock market when a company like Amazon is given leeway to roll up vast segments of the retail economy without generating any bottom line profits, only capital gains financed by stock issuance and dirt cheap financing. Rather than being just a casino side show to the real economy, the stock market is a weapons grade destroyer of private business, wages, and equality. No wonder it is hailed as the proxy for the health of the economy by the 1% who own 80% of its issuance.

“…capital gains financed by stock issuance and dirt cheap financing.”

Also, cash payments from the Federal Government under the cover of ‘tax rebates.’

I’d post the news story link, but Google seems to be fussy.

Equity is a residual claim: payments to shareholders come after paying suppliers and employees, bondholders, leases and licenses, legal claims, and taxes. But our new ideology is that the last should come first. And to achieve that, companies in the US have abandoned the model of sharing the benefits of productivity gains with workers: Yves Smith

But what if workers were paid with common stock? As they would be perhaps if companies had to pay honest interest rates for the workers’ savings?

And dividends are dumb since the purpose of a common stock company is to consolidate capital for economies of scale, not dissipate it. Instead, let the profits accumulate in the share price and use stock-splits to keep the price per share reasonable.

But what good is common stock if one never gets a dividend? Simple. Let the common stock company sell the goods and services it produces in exchange for its shares. That’s an ethical form of “stock buyback” since it does not involve the use of legally stolen purchasing power, i.e. loans from the government-backed credit cartel.

Ah, ethical money is fun! Too bad our version is filthy lucre.

There is something wrong here (or, more likely, important to understand)- productivity growth continues unabated in that graph, yet the claim is that companies aren’t investing as before?

You can literally see where the break happened just after 1970, and you can see that, after an initial gap, workers managed to just barely keep up (in wages paid terms) until 1978-79.

Yves, put the pieces together!

It makes you wonder whether the analytic tools we use for measuring our “product” are at all adequate or accurate. Somewhere between 8 and 9 percent of that so-called product is in financial services. Finance is important, but some no insignificant percentage of the measured product probably represents economically destructive looting of one entity by another, where the destruction side is unreported, unmeasured, hidden or hard to observe directly.

And yet some argue that finance needs to grow even bigger to allegedly grow GDP:

http://www.independent.co.uk/news/business/news/financial-sector-could-lift-gdp-3-if-allowed-to-flourish–report-8725457.html

The finacialization of our economy seems to have created a vast class of money managers and their clients who don’t actually know where real wealth comes from or how it is created, but who are frantically involved in finding ways to extract cash flows from the real productive activity of others. It’s amazing how people have been convinced that there are nearly bottomless “returns” to be extracted.

This is the real pathology of the so-called ownership society. Marx thought that it was part of the internal dynamic of capitalism that the capitalists would destroy the productive foundations of their own society. But I don’t think he realized that the way this would happen would be to entangle everyone in the financial component of the economy, so that we all become capitalists, participating in the collective self-destruction of our own society by the frenzied conversion of real value into money that then chases after a dwindling store of real value.

I doubt that any econometricians really know how to analyze this process and distinguish financial froth from fundamentals.

Please reread the piece.

1. Underinvesting is not the same as not investing. In the 1970s, companies in the US were not investing much if at all due to high borrowing costs, lousy stock prices, and a lousy economic outlook

2. Productivity is defined as output per dollar of labor input.

So how do you increase output if you don’t invest? You can improve work methods without investing (just in time manufacturing, or you can squeeze your suppliers). You can cut corporate waste (free anything and everything, from free lunches to cut travel to cut middle managers who don’t do much). But that was the 1980s trend, of discovering that big companies had gotten too fat and happy and cutting fat). The 1990s version, which also involved not investing, was offshoring and outsourcing, replacing US labor with cheaper foreign labor (mind you, I’ve argued that a lot of this was in fact not attractive, particularly if you adjust for the risks of extended supply chains, but Wall Street would bid up stocks of companies that announced offshoring and outsourcing programs, so this went way beyond where it made economic sense)

Since the mid 2000s, if not earlier, the trend has simply been not to spend. I’ve been hearing from McKinsey people since the dot-bomb era how it’s virtually impossible to get companies to launch any new initiatives. One classic example was a by-product business. Didn’t even require capital investment, just a big marketing push on their highest-margin service. Payback of less than a year. Company refused to do it because they weren’t willing to take the initial quarter costs. The mere fact that the expenses would come in one quarter and the payoff would be in the following three quarters was too much for them.

So how are companies eking out productivity gains? More squeezing of labor. Have you noticed how everyone in a white collar job in corporate-land is expected to be on call all the time? That’s an increase in work hours with no increase in pay. In fact, everyone I know in a corporate job is doing what would have been 1.5 to 2 jobs in 2000.

I have the Keynes quote in my handy stock as:

John Maynard Keynes, The General Theory of Employment, Interest and Money (photo. reprint 1997) (New York: Harcourt, Brace & World, 1936), p. 159.

We aren’t told the truth about what is going on. The left and once right used to argue against casino capitalism and the intransigence of banks regarding productive investment. Manufacturing and agriculture became highly competitive and there was a massive de-skilling and embodiment of work in machines across the board making it easier to ‘up plantation’ to cheap labour, with consequent pressures on investment in plant. We seem to be forgetting now just how much empire, trade restrictions and political deals (classics between UK and Argentina) kept up manufacturing margins. Much of what has gone on is repeat after repeat of the offshoring of ,say, Dundee’s jute industry to Bengal.

We need something better than lean production and given the pressures of this it seems peculiar that finance and retailing add so much to purchase prices – though retailing is clearly dying too. One can think of many ways to cut retailers out of the equation by direct sales, pre-ordering clubs and so on.

So how to value stocks? We hear banks need a presence on the high street, but I’ve been in to mine only once in 5 years – what is high street property worth, is it an asset or liability? You could look at bank shares and get a very false view of even their own buildings. Even their customer base might be a liability if all we need is money clearance and recording – with loans and the rest available to us by putting up an auction as big manufacturers do for parts.

Financial assets themselves look increasingly like a bag of magic beans with assets one monster Ponzi. The clearest indications are when a bank buys another bank. I see no way now to value any companies – beyond counting the number of customers using a chop shop over a spread of weeks.

Supply sided economics makes stocks the rage. IMO, this not the improvement in inventory management is the reason why the 90’s, 00’s and 10’s recoveries have been they way they are.

Stocks are very attractive in this type of economic system. It takes time however, for them to “trickle down” into investment before the blowup. Investment is what drives employment and thus income growth. Outside the Y2K refit of the late 90’s, we have not had a bit of income growth.