Yesterday, we wrote about a major loss by the electronic mortgage registry, MERS, in a major Federal court case in Pennsylvania. MERS suffered an additional blow via an important adverse decision in the Maine Supreme Court, against Tom Cox, the attorney who first made robosigning a national issue.

Because mortgage abuses have faded from national headlines, some readers may not be familiar with MERS. MERS was created to replace the system of local recording of mortgages. While such an idea could have had merit (for instance, Australia has a national mortgage registry that by all accounts works well), MERS was designed for the convenience of banks and mortgage securitizers, with no review of how it would work with well-established real estate law in 50 states. MERS is a classic example of what Lambert calls “code as law” where computer systems are put in place and contracts and legal precedents are expected to conform to the dictates of often-not-well-enough-designed “innovations”. And even worse, in the case of MERS, the database protocols fall shockingly short of well-established norms for information integrity and security.

It is important to remember that with over 60 million mortgages in MERS, the records that show ownership and liens against many Americans’ biggest asset are in serious doubt. Yet astonishingly, MERS has been able to maintain a facade of legitimacy, mainly by settling cases that looked to pose a threat to its operations. However, a few important challenges have crept through. One was a case filed on behalf of all Pennsylvania county recorders. If it survives appeal, it will deal a fatal blow to the use of MERS in that state, will almost certainly result in large damages, and will have serious ramifications in other so-called “title theory” states.

The Maine victory by Thomas Cox is more decisive, in that MERS has no where to go in Maine after losing in the Supreme Court. Its full ramifications are not fully clear, however. We’ve embedded the ruling below.

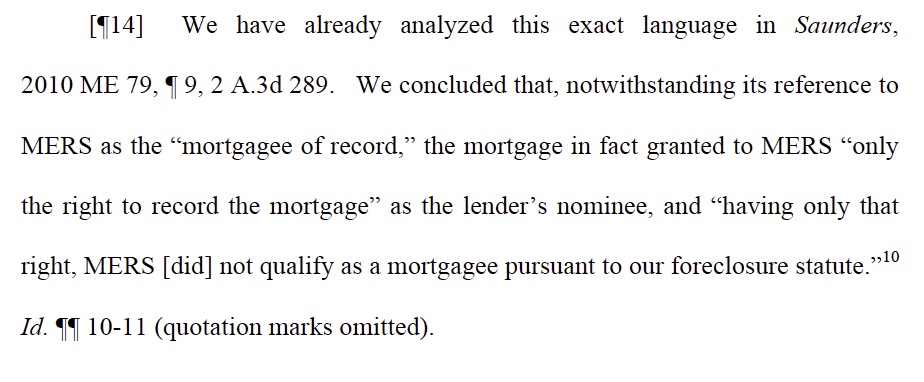

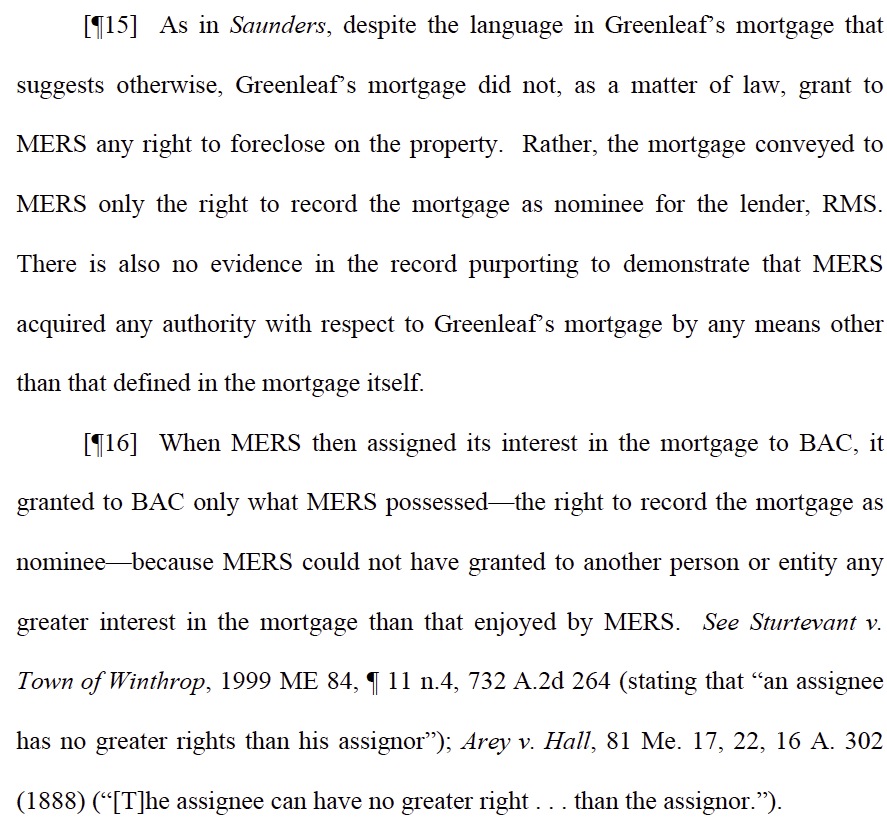

As the justices explain, the initial filing in Bank of America v. Greenleaf was a mess, leading the court to sanction the attorney. Nevertheless, BofA was able to muster enough of an argument to win a judgment against the borrower. Greenleaf appealed. The case made its way to the Supreme Court, with the argument focused on standing, as in whether Bank of America had the right to foreclose in the first place. The Supreme Court agreed that the bank had established that it was the holder of the note (the borrower IOU) in that it had possession of a note endorsed in blank. But the court stated that that was insufficient, and it also had to establish that it had “requisite interest” in the mortgage. Bank of America tried to show that through documents that showed that the Greenleafs had signed a mortgage with RMS, a lender, and MERS as the lender’s nominee. Another record showed that, as the court put it, “MERS purports to assign the mortgage to BAC” in 2011. The Supreme Court found that this did not pass muster. The key section:

Tom Cox explained what this means for MERS via e-mail:

The Maine Supreme Court has held that a MERS mortgage assignment, by itself, is not sufficient to prove an assignment of a mortgage. There are two solutions: one is for the forclosing party to obtain an assignment from the originating lender, but many of them are long out of business so this may not be a viable solution. The alternative is for the servicer for the forclosing party to prove up the MERS membership agreement of the foreclosing party, the MERS Membership Rules, the MERS Procedures Manual and related documents to prove that the MERS really does have the capacity to assign a mortgage. I don’t think that the evidence rules will allow the servicers to do this. Thus, this decision starts to raise a serious question as to whether MERS continues to be a viable operation in Maine. Maine is the first state supreme court with such a decision. If other states go this way, MERS is in trouble.

Hats off to Tom Cox for his continued good work. And let’s hope that these ruling against MERS force fundamental changes to a heretofore unaccountable and recklessly run operation.

‘The court determined that the Bank’s statements of material fact were “jumbles [of] multiple sentences” rather than a single concise fact per statement.’

Very satisfying to see a brain-dead bank lose a case for inability to assemble a coherent set of English sentences.

One could make the facile claim that the banksters shoulda studied English lit and rhetoric instead of biz. But honestly, it wouldn’t have helped.

robo-writing

Funny that code is law (delusions of grandeur), and oops! law isn’t code.

Here’s my favorite part,

“In short, the record demonstrates a series of assignments of

the right to record the mortgage as nominee, but no more.”

Successive parties purchased the right to record the mortgage? I think they got a bum deal LOL!

I liked that sentence too. Brooklyn Bridge.

MERS has fucked up the recording system nationwide. The courts have generally been unwilling to open that can of worms because it will be impossible to clean up the mess without further deranging the whole Real Estate industry. As a Broker I can assure you that buying or selling Real Estate is already deranged…

When I first heard about MERS and it’s associated multiple frauds, from reading NC a few years ago, I predicted this was going to turn into a gigantic legal clusterf*ck one day.

I can imagine a new breed of vulture lawyer/capitalists, getting people who’s houses were illegally foreclosed to sign over their rights to them, and then suing the bankers or whoever for the houses. A country as lawyer infested as the States should never have embarked on anything like MERS.

And who hired the lawyers? Control fraudsters in the executive suites. Nice to finally see some of them being prosecuted after those Senate hearings. Oh, wait….

I am a former broker. I will not sell real estate in this climate until the real estate agent’s liability isn’t on the line. All I can say to other real estate brokers—–DISCLOSE, DISCLOSE and DISCLOSE some more.

The title insurance industry and escrow are closing deals with nothing more than a Lost Note Affidavit and an agreement that exempts them from any liability.

When the buyer has any problems, who do they sue first? Their real estate agent. NOT ME!

Looks like the title insurance business is about to get a lot more interesting (and probably less profitable).

Most people who buy homes only buy the title insurance required. That policy is written with the lender as beneficiary, not the homeowner. If the homeowner desires insurance against defects in title they must pay an additional premium for a policy that lists the homeowner as the beneficiary. Once again, banks will win and homeowners will lose.

Thanks that is educational. I did not realize the title insurance I buy does not benefit me (which makes me wonder how they can require I buy it for them but that’s another topic).

But I have to wonder if the problem isn’t the same for them. The lenders are not likely to recover enough via title insurance claims to clean up the mess MERS has created. The title insurers don’t have the money anyway. Maybe the title insurers are planning to assert fraud on the lenders to save their businesses?

thanks! That is good to know.

As Amateur Socialist alluded to, Is there a rationale why the home buyer buys this “insurance” that apparently does not benefit themselves?

If the homeownere is obtaining a loan to purchase the property or is refinancing, then the lender is at risk when a property has title problems which requires research on the title to make sure there are no title problems, no liens, no other mortgages other than those exposed, so “Title Insurance” is required on every single loan closing. If the title insurance company gives a clean bill of health, and something happens down the line that was not disclosed by the title company through their search, then that company has to make good by paying it off and making the title without encumbrances or claims of any kind. It does benefit the client. Example: Lender A does loan to Client, title search done and nothing shows up that would hinder the ownership of the property or the lien position of the lender.

Then IRS filed a lien earlier and someone in the clerks office did not record it properly and it was missed. The Title insurance co must pay off that lien to make the Title whole and clean. That benefits the client as well as the lender.

The title industry has been EXEMPTING any transfer that is not recorded for YEARS. They know to exempt themselves from liability. They are in bed with the bankers.

A title industry lobbyist in my state testified before our Senate Financial Services Committee that “if you start require a promissory note to reconvey, I tell you that none of you will be able to sell your property!” What he didn’t say? The promissory note is REQUIRED on the CONTRACT that the homeowner signs called the DEED OF TRUST prior to reconveyance. So, the title industry is lying their ass off to cover for the lying ass bankers. It’s an entire racket. One. Big. Circle. Jerk.

An article Linked to a few days ago mentioned that the U.K. was trying to set up a centralized lands registry office, and thus render the local registrars powerless to set the standards for what constitutes a legitimate deed or lien. Keep an eye open for some such effort here soon. It will probably be described as a “necessary and prudent measure.” Who wants to wager that MERS will be employed as the “most experienced and capable” private contractor in the field? After all, look at the fine mess the County Clerks have ended us up in! (Chortle. Snort. Counts money.)

Indeed, Ambrit. They are in the process of writing that legislation now but they are keeping it very quiet. They have acknowledged that getting all the states to conform is difficult – which means they will probably write a bunch of equivocating nonsense (and call it code). We’re so lucky to have all these wonderful representatives in Washingston.

Paranoid scenario: Sell it as a “consumer protection” measure.

Susan (et. al.),

http://www.uniformlaws.org/Committee.aspx?title=Home+Foreclosure+Procedures+Act

Under “Drafts,” on the right hand side, look at the 3rd link down, “2014 Annual Meeting Draft.”

All should give this a read.

The Seattle conference begins in 3 days.

Is anybody going there to protest? I’m reading Section 401 and it doesn’t look good for the citizens

Wow! Thanks, Supendous Man!

That sure does look like what has already been done to my whole region way down here in the Kaipara District of New Zealand. Enforce the law and redress wrongs that were clearly illegal, like debts being secretly loaded on property owners by those with government-bestowed power to do so? Well, enforcement might hurt the banks, or the credit ratings of local government bodies. So in a special Act of Parliament (Kaipara Rates and Other Matters Validation), the citizen safeguards and promises made in the original act of Parliament (Local Government Act) were withdrawn (for this one case!), and the secretly and illegally incurred debt for services never rendered was officially made binding. Parliament was prompt, and rushed the Bill through under urgency before the High Court could act on an already-in-progress lawsuit brought by the public.

Beware, America, imo it is the same bunch looting the public here and there, and this is what they do.

Yes! We will be protesting in Seattle at Westlake at NOON. Then marching to The Westin Hotel at about 12:30/12:45. Come join us! Spread the word.

http://www.rollingrebellion.org/actions/

The Uniform Law Committee’s last update to the UCC was passed in zero states.

Anything the Uniform Law Committee does has to be passed on a state level to become effective.

Not quite correct, Yves. The last ULC amendment to UCC Article 3 was adopted in only ten states. The ULC Uniform Nonjudicial Foreclosures Act was not adopted in any state.

Mr. Cox nice work. I’m originally from Maine so I’m astounded by the laws in Colorado where it only takes a corrupt attorney’s signature to take your home. I sure wish we had an attorney in this state like you.

On another note I recently ran across a Corporate Disclosure in Federal Court. I am only posting the part about Fannie and Freddie but the case number is 1:13-cv-02715-REB-MJW.

1. Chase is a wholly owned subsidiary of JPMorgan Chase & Co., which is

publicly traded. No publicly held corporation owns ten percent or more of JPMorgan Chase & Co.’s stock.

2. The parent corporation of MERS is MERSCORP Holdings, Inc. No

publicly held corporation owns 10% or more of MERS’ stock. MERSCORP Holdings, Inc. does not have a parent corporation. The Federal Home Loan Mortgage Corporation and the Federal National Mortgage Association each owns 10% or more of MERSCORP Holdings, Inc.’s stock.

Are Fannie and Freddie the largest shareholders in MERSCORP Holdings, Inc. and if so how is this going to impact them? Freddie and Fannie both have MERS member IDs and can move things around at will without any supervision.

This Home Foreclosure Procedures Act is being funded and pushed by the big banks, Freddie Mac and Fannie Mae.

I’m not sure if you’ve been paying attention to your state politics, but anything the bankers want these days gets passed. And because Freddie Mac and Fannie Mae will tell your legislature that if they don’t pass this, they will yank buying paper from your state, pretty sure that will scare the be-jeezus out of the state legislators and they (along with greased palms) will vote anything through.

Google “Home Foreclosure Procedures Act.” The Uniform Law Commission is attempting to do JUST this very thing in the USA right now. The Committee drafting this bit of garbage is funded by Freddie and Fannie.

http://www.marinkapeschmann.com/2014/06/30/legalizing-mortgage-theft-ulcs-paper-to-electronic-home-foreclosure-procedures-act/

On top of assignments, there are a huge amount of mortgage releases executed by Mers. This ruling throws a huge wrench in the title for a lot of properties.

That is the big picture. Millions of mortgages which may not be able to be lawfully satisfied upon payment in full or upon foreclosure of the security interest on the real estate. Everyone must demand the return of their original Notes marked paid in full, discharged or satisfied to assure that they are not subject to Zombie debts created by the securitization practice enabled by MERS which separated the Notes from the Mortgages.

Wendy, the big picture is quite different really. No MERS mortgage needs or requires satisfaction, because upon being savaged by the MERS procedure, and the multiple resales, splintering of note and deed, lack of recording/fictional recording, all to support a claim against the property that didn’t exist if it went into the MERS system to begin with. It was a fraud from day one. Few to none of the “securitization” documents or trusts exist in reality. The mortgages were wiped when they tried to add them to these “trusts” years after the 90 day deadline.

If this weren’t a complete sham to hide ownership, obstruct justice and steal property from the party that was not privy to the deal, there is nothing left except a series of false claims.

MERS requires that documents are created upon foreclosure, as I am sure you know. Because they don’t exist before the need to foreclose. If you have sent an FDCPA letter or made a qualified written request, you know they don’t answer truthfully, or can’t answer due to a lack of documents to support the claim. They make them up. They get attorneys to falsify them. My county records are full of it, as are those in all the states in this country. I have had 5 different attorneys claim different things about the existence of a lien, 2 of which admitted they had to falsify the documents to make the claim.

Tom knows, I have read his work for years. Max Gardner knows and put down a $10,000 check for any attorney that could bring him a legal claim against a property, it remains uncashed. Neil Garfield knows, and provides the information every day now for 5 years.

What began as a crime has become an organized syndicate that includes the entire industry. It has to, they know the title insurance is based on fiction. That is why they don’t offer old fashioned title policies any longer. They are dead men walking because they assisted MERS destroy the records.

So what happens when every bank, every title company, every trust and everyone involved is found out to be involved in a criminal conspiracy larger than any before it on earth?

“what happens when every bank, every title company, every trust and everyone involved is found out to be involved in a criminal conspiracy larger than any before it on earth?”

Interesting question. Maybe the answer is “They get together and elect a President?”

Lambert,

I think the answer is: we get together and force the banks to prove up where all this goddamn money went and take it back!

Brian – So are you saying that even tho we buy title insurance, it is worthless? Does it help for the homeowner to purchase title insurance for themselves on top of the title insurance bought to protect the lender? I am not clear on the implications of what you said. How can we protect ourselves?

Title insurance is totally worthless. Title companies have been exempting the major issues with title since this shit began. Call your title company up and ask for your title policy. Ask if they cover “non-recorded transfers” because that is what MERS has been doing…..shuffling that mortgage around like it’s whiskey at a frat party….and everyone’s lips have been all over that bottle.

And there should be new, specific legislation that all homeowners can claim triple damages against MERS for screwing up their title.

I don’t think MERS has deep enough pockets. Isn’t that really one of the beautiful thing about MERS?

MERS just needs deep enough pockets to bribe sufficient congress critters plus one pres. to get a new law saying everything is ok. Coming soon to a congress near you.

Google “Home Foreclosure Procedures Act.” Freddie and Fannie are doing so as we speak. They are drafting new legislation to shove onto state legislatures to make all the bank crimes just disappear! How ’bout them apples?

The US Congress is considering a national mortgage registry, I believe, in the Johnson-Crapo bill. Such an effort creates a serious constitutional issue because land records have always been state issues, reserved to the states under principles of federalism embodied in the Tenth Amendment. There is also a current effort by the Uniform Law Commission to draft a proposed Uniform Home Foreclosure Procedures Act, which contains proposed provisions which would deprive homeowners of their due process and equal protection rights by creating a class of persons who are not entitled to the application of the Best Evidence Rule and altering the burdens of proof in litigation. This is all generated by the MERS mess and the Too Big To Fail response of Congress and many state and federal courts. It is not MERS that matters. It is the liability of MERSCORP Holdings, Inc. members for fraudulent documents being created under MERSCORP policies by which homes have been confiscated by parties who cannot establish the lawful right to foreclose. “Oh, what a tangled web we weave, when first we practice to deceive.”

‘[A national mortgage registry] creates a serious constitutional issue because land records have always been state issues, reserved to the states under principles of federalism embodied in the Tenth Amendment.’

So true. Yet Congress already intruded into real property conveyance with RESPA in 1974. Similarly, Obamacare retains the facade of state insurance regulation, while dictating key contract terms.

With the Tenth amendment a dead letter, federally-sponsored Too Big To Fail legislation is all too likely. Let’s be evil ought to be engraved over the doors of the Capitol.

“Crapo”? C’mon. The bill can’t be called “Crapo.” That’s too much!

“Crapo” is a Senator. I would never have believed a politician could win with a name like Crapo. Will wonders never cease. Vote for Crapo! Don’t we always have to??? Two choices usually: Crap and Crapo.

After connecting all the dots, it is quite obvious that MERS was established (in 1995) on a purposeful basis to allow the banksters to immensely profit from the establishment of Mortgage Backed Securities. The end result was a housing implosion in the US and a decimation of assets in pension and sovereign wealth funds on a global basis. That the Democrat regime in the US promoted, encouraged, and legislated home ownership, during the Clinton years, especially among those who could least afford it, is no coincidence. Both Dodd and Frank, ironically, should be emprisoned for their contributions to this rape and theft.

What I can’t understand is, how was MERS allowed to be a monopoly, even after the problems became apparent? Was there even an option for mortgages to be recorded any other way, once it became established?

MERS was/is owned and created by the big banks, the same ones that were bundling and selling mortgages to MBS trusts. They needed a less cumbersome means of transferring mortgage rights than the traditional method of obtaining hard copies of mortgages and notes, in order to make the necessary high volume of rapid successive transfers of rights. They created an entity that perfectly met their needs. There was no need for competition. Whether MERS met the needs of homeowners wasn’t a consideration. Loan contracts are always written to favor the interests of the lender. This is especially true in title theory states that can foreclose without judicial oversight.

Under analysis of the judges from the Maine Supreme Court, MERS presents itself has a simple registry when in fact it the consequences of its claims on the property rights reveals it to be a holding company. From my perspective, the original lender must have a note and a mortgage and all of the property rights that go with them. MERS as a nominee is given a specific, limited set of rights, perhaps one and only one right, to record a note and a mortgage. If the time comes to foreclose on a property, the recorded note and mortgage at MERS does not by its mere presence of being recorded in a file constitute a property right that would give it legal standing to initiate a legal action to protect its property interest. If that is what MERS claims, a legal standing that comes with the full set of rights of ownership, and not just an attenuated limited set, it would also be claiming to be a holding company and thereby the rightful owner of all 60 million notes and mortgages.

If by claiming full property rights by right to record, then all county records of the same would also convey ownership rights to counties. And where does the bank, the original note holder stand in all of this? Are they completely relinquishing all rights of ownership when they do business with MERS? How does MERS sue the homeowner and then liquidate the note as much as it is possible conveying the proceeds to the bank? Doesn’t conveying the proceeds after the sale of the foreclosed property demonstrate who really is in possession of the note? MERS does not award itself these proceeds on a percentage of ownership. If it does not, how can it claim standing as having an interest in the note. Wouldn’t it also materially benefit to some percentage if it held an interest? It can NOT pretend to be a simple service provider limited to recording and acting as a long term, perpetual depository of notes and mortgage for real estate in America and then claim an interest as implied or understood. There does not seem any basis for such a claim based upon the limited service it provides.

Good comment. MERS wants it more than both ways because mortgages have been in the asset column and have been rehypothecated like cattle in a slaughterhouse for decades. Whereas the note, considered to be the explicit obligation, has been ignored because it is a tad more problematic to rehypothecate no doubt. No assisgnments. Who assigns the rights of cattle. Etc. Commodities are just such a wonderful thing. This was such a heart-warming post. On top of Pennsylvania. Almost got my energy back. The stuff you said about holding companies should be incorporated into every legal argument. 60 million mortgages are stuffed into MERS. And in order to rehypothecate them they have to, as in “must,” separate them. Otherwise it’s just old fashioned, county by county business. It’s totally intentional and deeply fraudulent. So here’s a question: why aren’t 60 million mortgage contracts enough for our housing industry to thrive with profits out the wazooo? That’s alot of money, unless you are siphoning your brains out. But who cares about a few bloody brains in a vat of money that big? Clearly somebody does.

http://www.scribd.com/doc/40664635/MERS-Appellants-Brief-MERS-v-Nebraska-Dept-of-Banking-Filed-15-Oct-2004

10 years old, and I’m still amazed more folks aren’t familiar with this Appellant’s Brief by MERS.

And this:

“When MERS then assigned its interest in the mortgage to BAC, it granted to BAC only what MERS possessed—the right to record the mortgage as nominee—because MERS could not have granted to another person or entity any greater interest in the mortgage than that enjoyed by MERS.”

nemo dat quod non habet – no one can give what he doesn’t have

Levitin, and others (perhaps you too, Yves), have covered nemo dat in recent years.

Yes, but I didn’t use the Latin and so it would take some doing to find where I discussed it (only a few times).

I continue to be stunned by the absolute rapaciousness of the rich. Then I’ve been nervous since the S and L Fiasco proved that looting mortgages was very profitable.

Great post and great comments. Thanks for all your expertise. Since this all began I’ve been thinking that title insurance is a joke. Looks like it still is.