I’m still hugely behind on the AIG bailout trial, and hope to show a ton more progress in the next week. I’m posting the transcript for days three the trial; you can find the first two days here and other key documents here.

The first week was consumed with the testimony of the painfully uncooperative Scott Alvarez, the general counsel of the Board of Governors, who Matt Stoller argued needs to be fired, and the cagier-seeming general counsel of the New York Fed, Tom Baxter. Unlike Alvarez, Baxter at least in text seemed to be far more forthcoming than Alvarez and more strategic in where he dug in his heels. But the revelations about the Morgan Stanley rescue alone are juicy. The main actors have sold a carefully concocted story for years.

One of the hopes was that this trial would unearth new information about how the crisis was handled by the officialdom. Just as in wars, the history has been written by the victors. Here conventional wisdom was set in place by what amounted to an authorized narrative, Andrew Ross Sorkin’s Too Big to Fail.

And in that version, the firm that failed or were effectively nationalized were headed by incompetents or figures who got so little coverage as to be cyphers. Dick Fuld was a bully and a lousy negotiator who kept blowing deals that might have salvaged Lehman. Freddie Mac CEO Dick Syron and Fannie CEO Daniel Mudd have walk-on parts. AIG’s Bob Willumstad gets more coverage, but seems little more than a typical colorless corporate leader who isn’t up to managing the escalating crisis at AIG. When the giant insurer was working with JP Morgan and Goldman on a last-ditch fundraising, the bankers were openly derisive that Willumstad didn’t have a good handle on how big AIG’s liquidity black hole was.

Shorter: the prevailing accounts of the crisis are clear on who the good and bad guys are, and paints them accordingly (although the CEOs of walking wounded Citigroup and Bank of America generally received less flattering treatment than Jamie Dimon and Lloyd Blankfein did). But reality is seldom so clean and tidy.

As we wrote earlier, the trial has already revealed that Treasury Secretary Hank Paulson refused even to entertain investment offers from Chinese and Singapore sovereign wealth funds, along with rich Middle Eastern investors. His pretext was that they would have required “guarantees”. But it was a given that the Fed was going to provide liquidity, so the “guarantee” they’d refused to give to Lehman was already in place. There was nothing to lose in entertaining these offers…unless the real objective was not simply to salvage AIG at minimal cost to the public but to use it to launder rescue money to banks. More on that in future posts.

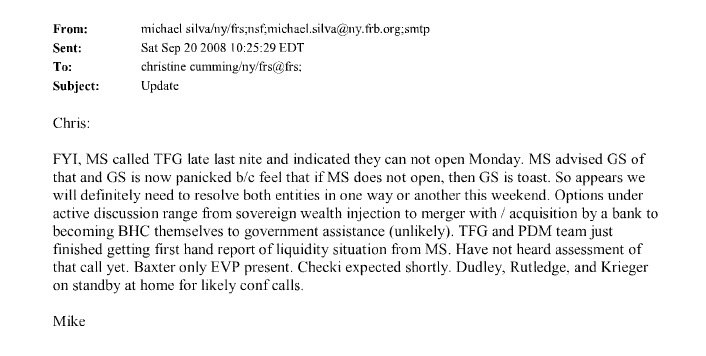

The Baxter testimony provides a key addition to the official history: This is Plaintiff’s Exhibit 175:

In case you have any doubts, TFG is Geithner.

I’ve checked my trusty copy of Too Big to Fail, have done some web searches (much less reliable than they were years ago) as well as called other crisis junkies for their recollection on this matter. If readers can show me any clearly contradictory evidence, I’d love to see it, but I am not aware of any published source previously saying that Morgan Stanley said it would not be able to open absent a bailout. And the e-mail also confirms something we’ve long said, and Lloyd Blankfein admitted to in a rare unguarded moment, that if Morgan Stanley failed, Goldman was next.

And don’t kid yourself. If Goldman and Morgan Stanley collapsed, you could forget about JP Morgan’s “fortress balance sheet”. JP Morgan and Bank of New York, the two linchpins of the tri-party repo system, would be engulfed by the cascading payment failures and bankruptcies that would ripple out of a Morgan Stanley/Goldman implosion.

How is the sanctioned history different, and why does this matter?

While everyone with an operating brain cell knows that all of the major capital markets firms, particularly what were then US investment banks, were in a world of hurt after the Lehman bankruptcy, there is a big difference between having the (correct) view that they were inevitably going to need to be put on the official drip-feed and knowing for a fact that they clearly were going to fail if they didn’t get a Fed rescue over the weekend of September 20-21. And remember, this weekend, when Goldman and Morgan Stanley were made bank holding companies, was the same weekend that the AIG demand note that bridged it into the weekend was replaced with an $85 billion credit facility on terms that were vastly more punitive, much to the surprise and consternation of its board.*

However, if you read Too Big to Fail, it depicts Geithner as having his hair on fire, desperately trying to browbeat Morgan Stanley’s John Mack into merging his bank for $1 into JP Morgan. And this is stated as if it is Geithner’s personal mania, rather than based on Morgan Stanley making an official report that it was a goner. From page 480 of the first edition:

Geithner, still holding court from his office downtown, had become convinced that Morgan Stanley would fail if it didn’t complete a deal by the time the markets opened on Monday. H e had threatened Mack earlier in the day that he would deny his request to become a bank holding company unless he found a sizeable investment or merged….

Not everyone at the Fed was in agreement with Geithner’s insta-merger strategy, however. So unpopular was Geithners’ single-mindedness about merging banks that afternoon that some CEOs began referring to him as “eHarmony, the online dating service. “If we sell more of these guys for a dollar,” [Fed governor] Kevin Warsh complained, “this whole freakin’ thing is going to come undone.”

In fact, Sorkin depicts Mack as a cool-headed, high-stakes poker player, evidently based on the assumption that the collapse of Morgan Stanley was not baked in. Remember, Mack was negotiating with Mitsubishi to make a capital injection, which they did in very general terms before the weekend was over.

What is kept hidden is that Mack knew he had the Fed and Treasury by the balls. After Lehman, they would not be able to let another major firm fail. It would clearly take the entire system down. So from his perspective, he had no reason to knuckle under. The Fed would blink and make Morgan Stanley a bank, as indeed it did. In other words, telling the Fed on Friday that the Morgan Stanley would not open Monday guaranteed that the opposite would happen, somehow. He could always do a deal with JP Morgan later if he really had no other option.

Mack himself apparently supported this misrepresentation, that it was the Fed/Treasury tag team that decided on its own that Morgan Stanley was about to go under, with since this account incorporates Mack’s point of view. The immediately following section from Too Big to Fail:

At about 3:30 PM, John Mack’s assistant, Stacey Cruck, announced that Secretary Paulson was on the line. Mack took the call on the phone next to his couch. The New York Giants versus the Cincinnati Bengals game was playing on the TV behind him.

“Hi, John, I’m on with Ben Bernanke and Tim Geithner, we want to talk to you,” Paulson said.

“Well,” Mack said, “since you are all on the line, can I put my general counsel on?”

Paulson agreed, and Mack hit the speakerphone after the television was muted.

“Markets can’t open Monday without a resolution of Morgan Stanley,” he said in the sternest way he knew. “You need to find a solution, we want you to do a deal.”

Mack just listened, dumbstruck….

“We’ve spent a lot of time working on this and we think you need to call Jamie,” Geithner insisted.

“Tim, I called Jamie,” Mack replied, clearly exasperated. “He doesn’t want the bank.:

“No, he’ll buy it, Geithner insisted.

“Yes, for a dollar!” Mack exclaimed. “That makes no sense.”

“We want you to do this,” Geithner persisted.

“Let me ask you a question: Do you think this is sound public policy?” Mack asked, clearly furious. “There are thirty-five thousand jobs that have been lost in this city between AIG, Lehman, Bear Stearns, and just layoffs. And you are telling me that the right thing to do is to take forty five to fifty thousand people, put them in play, and have twenty thousand jobs disappear? I don’t see how that’s good public policy.”

For the moment, there was silence on the phone.

“It’s about soundness,” Geithner said impassively.

“Well, look, I have the utmost respect for the three of you and what you’re doing….But I just won’t do it. I won’t do it to the forty-five thousand people who work here.”

And with that, he hung up the phone.

Now understand how this reads if you don’t know that it was Morgan Stanley that told the New York Fed that it would not be able to open on Monday. Mack is presumably relaxing, watching football and is ambushed by Geithner, Bernanke, and Paulson to do a deal and manfully wards them off. Remember, we’ve just seen Paulson successfully browbeat both Freddie Mac and Fannie Mae’s boards into accepting a resolution, when Fannie’s board and bank regulatory lawyers were convinced it wasn’t justified but found they had no way out.

We see a broadly similar story from Mack in a Wharton write-up of a talk he gave:

During the depths of the global financial meltdown in September 2008, John Mack faced the most critical moment of his tenure as CEO of Morgan Stanley. The investment bank was nearly out of cash, its stock price plunging into the single digits as investors lost all confidence in the financial sector. Mack was under enormous pressure from U.S. Treasury Secretary Timothy Geithner — who was then head of the New York Federal Reserve Bank — and from Geithner’s higher-ups, then-Treasury Secretary Henry Paulson and Fed chairman Ben Bernanke. Their suggestion: Save the bank by merging with another player, most likely JPMorgan Chase & Co., for a price as low as a dollar…..

Mack stayed on the phone as Mitsubishi agreed to invest up to $8.4 billion in Morgan Stanley — the largest overseas investment by a Japanese financial firm ever — and then he worked out a deal with regulators to convert the investment bank into a bank holding company, a move that offered much greater flexibility for dealing with the fast-moving crisis.

What is the wee problem with this story? My archives show that the Fed approved that Morgan Stanley and Goldman become a bank holding company before the Mitsubishi deal was announced. From the Bloomberg story announcing the deal:

Mitsubishi UFJ Financial Group Inc. will invest up to 900 billion yen ($8.4 billion) for as much as a fifth of Morgan Stanley, the U.S. securities firm seeking capital following the collapse of Lehman Brothers Holdings Inc….

Morgan Stanley and Goldman Sachs Group Inc. won approval yesterday from the Federal Reserve to become banks, effectively ending the era of the Wall Street investment bank and capping a week that saw Lehman file for bankruptcy and Merrill Lynch & Co. rush to sell itself to Bank of America Corp.

Notice how all of the principals were apparently on the same page as far as the messaging was concerned: that it was the Fed and Treasury that were panicked about Morgan Stanley, that the Mitsubishi deal did not depend on Morgan Stanley having gotten the Fed lifeline of being made a bank holding company. The sequence of events strongly suggests that it did.

Here’s the political significance: the hiding of key details about the Morgan Stanley bailout obscures the degree to which officials bent the rules to salvage big, well connected financial firms, and remember, this is even with the public knowing the rules were already bent a plenty. The rushed approval of Morgan Stanley and Goldman as bank holding companies was utterly in violation of official procedures. It isn’t simply that normal waiting periods were waived. The Baxter testimony reminds us that the New York Fed and Board of Governors had to pretend black was white to approve Morgan Stanley as a bank holding company. Q here is David Boies, A is Tom Baxter:

Q. And in order to find that a company can be granted financial holding company status, you must find that they are in sound financial condition and well managed, correct?

A. Well capitalized and well managed, yes.

Q. And who has to make those findings?

A. The Board of Governors of the Federal Reserve System.

Q. And do you know whether the Board of Governors for the Federal Reserve System made a finding that Morgan Stanley was well capitalized and well managed the weekend of September 20th?

A. My belief is they did.

Q. Were you present when that happened?

A. I was not.

Q. Do you know what information was presented to the Board of Governors that would provide a basis for such a finding?

A. I do not know.

Boies’ questions to Baxter also expose that Morgan Stanley managed the difficult feat of borrowing more from the Fed via the Primary Dealer Credit Facility, which had been loosened on September 14 to allow broker-dealers to pledge non-investment grade securities, as in any dreck they could round up, than the larger AIG had taken in its bridge loans during the same time period.

So while Mack comes out of this sort of looking like a good guy, let us remember that this moral comparison is more like what the Japanese would call a height competition among peanuts.

Mack did manage to muscle his and his staff’s way into a lifeboat after the banking system hit the iceberg. But let us not forget that the lower classes in steerage of the Titanic, just like hapless Americans and foreigners who were exposed to the financial system collapse, such as business owners who had their credit lines cut and non Morgan Stanley bankers who lost their jobs, perished. And at least on the Titanic, the captain did go down with his ship. Here, instead, the captains got book deals and speaking gigs and used them to rewrite history.

____

* Note we are not saying AIG should have gotten a sweetheart deal. All of the rescued firms should have been treated harshly. At a minimum, their boards and top executives should have been replaced.

2014.10.01-DAY-3-Full

2014.10.01 – DAY 3 – Full

Great stuff, Yves! You’re providing an invaluable public service by following this case and explaining the important bits to the rest of us. And man-oh-man, if that conversation between Paulson, Bernanke, Mack and TFG (“that f—ing guy”) doesn’t have ‘fabrication’ written all over it, I don’t know what does. Somehow, the counter-narrative you’re pointing to rings much more true.

On a side note, it wasn’t clear whether this quote was also from “Too Big To Fail” or from another source:

Just wondering. The way the preceding sentence is phrased leaves it somewhat unclear.

Thanks again for your work on behalf of Truth–somebody’s gotta stick up for her.

Oh, let me clarify. That was an even puffier source, “Knowledge at Wharton”, which was a write-up of a talk Mack gave.

Thanks for the clarification.

Yes. Great parsing for the real sequence of events. I remember watching Mack and the other indignitaries leaving a White House meeting with Paulson, they were walking down the driveway in a very somber little parade with grim faces, and John Mack looked so very revealing it wasn’t funny. He looked like he was in physical pain. The cover story was that these erudite banksters didn’t really need the bailout money but Hankster’ made them take it” anyway. And the amazing thing is that we Americans bought this crap. BS-PR. And it is such a fragile story still because it will raise all the correct questions about how the “financiers” got all the MMT (because foreign money was totally rejected – amazing and another piece of evidence that MMT is alive and well if utilized for the sole purpose of American Financialism, and etc.) they could ever have hoped for and the rest of America went down with the ship. Killer Titanic metaphor.

And why, exactly, was all this information concealed from SIGTARP, the FCIC, the GAO, and the Senate Permanent Subcommittee on Investigations? What are the parameters of the coverup?

That is a pretty important question. Especially since the piece of evidence is an email from a FRB of NY in the piece above. There should be a massive email trail to parse as this was a crisis handled on the fly by remote parties.

Yves, the first big thing I took from TBTF was that I got this sense that Lehman was treated as the sacrificial lamb in all of this. On one hand, Timmy, Hank, and Ben were all working their butts off to save GS, MS, etc. Yet when Fuld would call up Hank asking for help, Hank would say it was Fulds problem and that Fuld had to find the answers. But before hanging up the phone, Hank would give reassurance that everything would be ok and work itself out. So Fuld would get the sense that the company would survive no matter what happened. Since none of the Big 3 had connections to Lehman, they let Lehman sink so they could bail out their connected firms. I also felt they treated BofA the same way. Yet apparently BofA had enough luck to save it from certain death (maybe because they were already a bank. or maybe because they were being forced to buy Merrill, which gave them a hand at the proverbial poker table).

Of course, you get it right as usual Yves. This is all about making the private sector look like heroes and the govt (actually the private fed, but the public is too stupid to realize this) look like the overreaching evil monster.

This quote really struck me:

“Let me ask you a question: Do you think this is sound public policy?” Mack asked, clearly furious. “There are thirty-five thousand jobs that have been lost in this city between AIG, Lehman, Bear Stearns, and just layoffs. And you are telling me that the right thing to do is to take forty five to fifty thousand people, put them in play, and have twenty thousand jobs disappear? I don’t see how that’s good public policy.”

Did you ever notice how with people like this, they only start talking about “saving jobs” when it’s to save their own skin? It’s just one more bullshit defense in a long series of them. Any other time, they couldn’t care less about who they send out the door, but when self preservation kicks in it’s suddenly “won’t somebody please think of the jobs!!!”

Excellent observation, Roquentin. “Neutron Jack” Welch, “Chainsaw Al” Dunlap, and private equity parasites such as Mitt Romney certainly never cared about protecting jobs. Typically, when there’s a layoff at a major corporation, that company’s stock price rises.

From a New Yorker’s perspective, the interesting thing about this comment is that the big financial firms have been shrinking their labor forces (due to automation, everyone else has been doing the same thing) and moving back office operations out of the city for years. But I think if the “industry” disappeared it would be better for New York in the long run, since its presence crowds out the development of other business sectors by inflating costs, particularly real estate, for everyone.

I’m not so sure about that. James Howard Kunstler voiced a feeling I had but could not articulate when he strode about Manhattan recently and noticed how bustling and polished it looked, inconceivably more burnished and bright than it was in the 1970s when he left it. The answer he came to–this is all the result of the greatest theft of wealth in human history by the Manhattan financial sector–is almost certainly true. Manhattan has grown fat on wealth extracted from around the globe. Nothing that New Yorkers could do would make up for that windfall. If the financial firms all left, the economic crash would swamp all boats. Perhaps something good would come of it, but it might take a generation of want and squalor to get there.

Have the other boroughs benefited?

Did you notice the article about the Manhattan of China? 120 miles from Beijing. A port. A trading center. Built to order with a Manhattan skyline. Is Manhattan being honored or ridiculed? Or does one go with the other?

We’re living in a sort of inverted “bad old days” right now. Crime is gone, but no one can afford the city anymore. It gets worse every year. I couldn’t afford my neighborhood if I had to get a new place in it. The story of NYC is as follows: In the years following WWII capital started flowing out of the 5 boroughs and into the suburbs (Westchester, Suffolk, Nassau, Connecticut, etc). This is the same story as every other major city in the US. It really hit full speed in the 70s and 80s, to where so much capital had flowed out of the city there wasn’t even enough sloshing around to keep basic infrastructure (the infamous “drop dead” moment and bankruptcy).

What we are seeing now is all that capital flowing back in. Anyhow, anyone who doesn’t work in financial services, making massive amounts of money, stands to gain very little from their presence here. That’s not to say the ride down when they left would be pleasant. It’d be almost as rough as it was back then. It’s a Catch-22 and change is never easy.

Present day “Manhattan” is more the result of other countries’ oligarchs, who use Manhattan real estate to launder their money. This drives up the cost of living for people who actually live in New York and businesses that want to operate from there. Its really hard to come up with a worse urban development policy than to turn a major city into a bank, which is effectively what happened with New York.

My understanding is that something similar has happened in London.

Seems to point to the Fed being like deer caught in the headlights with the central problem being a breakdown of tri-party repo and hence money market funds.

There seems to be good progress here by stabilizing money market funds by reverse repos and keeping that money from cheaply financing risky behavior via tri-party repo.

That plus some stress inoculation (Janet Yellen had a front row seat in all of this), should give her a stronger hand in dealing more appropriately with the banks the next time around.

“…the next time around.”

The Powers needed a sacrificial lamb for appearances sake the first time. (Really, for every time.) So, who will be thrown into the brazen belly of the Beast this time?

Citi bank

Yves — could you please elaborate on this? “Paulson even acknowledged that Fannie didn’t technically warrant being put into resolution, but the markets weren’t savvy enough to differentiate between the two GSEs, and if Freddie was put down, the same had to be done to Fannie.” The popular media narrative is that the government saved Fannie, but your statement makes it sound more like government was improperly using Fannie for their own ulterior purposes/end-game?

I’m not opining either way. I’m recapping what is in Too Big to Fail. But you did catch an error based on flawed memory.

Freddie’s CEO agreed immediately to Paulson’s bear hug that the GSE be nationalized. By contrast, when Fannie was told, its management, and particularly its normally composed uber lawyer Rodgin Cohen exploded, called Ken Wilson, who was representing Treasury, and screamed that the plan was “bullshit”. I recall reading a statement, and cannot find it, so it may not be in TBTF, that during the row that someone from Treasury, and it may not have been Paulson, basically said Fannie had to be put down too. TBTF says that the Treasury had Morgan Stanley do an in depth analysis, including analyzing loan tapes, and conclude both GSEs needed a rescue and what was then called OFHEO was prepared to put Fannie down, voluntarily or not. Thus the remark may not have been a concession but tantamount to, “Even if what you say were true, it doesn’t matter, the markets don’t see you as any different and we can’t resolve Freddie and not resolve you.”

I’ll tweak the post accordingly.

So, the official narrative, sordid and horrible as it is, is now proven to have omitted major, substantive events — and the guardians of that narrative — Hi, Michael Lewis! [waves] — proven to be at best useful idiots and catspaws for the banks. Who knew that “telling a good story” wasn’t enough?

One can only wonder what other bodies will be unearthed as this trial proceeds!

The official excuses for the bail-out never smelled right.

Thanks for the confirmation.

Thank you, Yves. This trial is presenting a much better post-mortem than either Sorkin on the MSM of what happened during September 2008. You educated me that the Fed did not do the bailout at bank direction (I had believed that because the big banks own all the stock in the Fed, the Fed did their bidding) because the Fed directors from the banks have no role in regulatory policy. Thanks for the info – but its a tad unsatisfying. I am still struggling to understand why the Troika did what they did. They pushed if not outright ignored the limits on their authorities to recapitalize the TBTF banks. Instead, they could have nationalized the banks, cleared their obligations in an orderly fashion and restored order pretty quickly – and they would today be enjoying hero status, rather than being paharias, being cross-examined, and deposed. Is there some frame for their logic I can’t see? I suppose that if one considers a mass conflagration among the financial firms as an unacceptable outcome, then one might take the direction they took, but if one believes in the “system”, then one should also believe that its sub-systems (regulation/bankruptcy) work, or could be made to work to reset the larger system. I suppose I have an easier time believing these guys are evil than I would have believing them to be stupid ideologues. Or, am I such an financial dunce that I have no idea what a cascade of bank failures would mean and all the king’s men and all the king’s horses couldn’t have put Humpty Dumpty back together again?

Philosophically, they were not willing to nationalize the banks. Period. Once you understand that that was a boundary condition for them, plus they basically thought well of the investment bank execs, what happened looks more internally consistent.

The last time a major bank was nationalized, and that was Continental Illinois in 1984, it took 7 years to resolve the bank. And that was when the economy was healthy.

The US would have wound up owning most of the banking sector had it gone down the nationalization path. Personally, I think that would have been ducky, we’d have officially recognized that banks really are public utilities.

But even if they were willing to consider that idea, they were still hostage to the idea that you had to have Masters of the Universe to run these businesses, and they needed that juicy private sector pay to stay in place. Oh, and then you have those highly paid employees, now on the government dime, running capital markets businesses with government credit! You can’t shut down or sell a capital markets (major trading business) tidily; we saw that with Lehman. If you “resolve” it, you have to close down positions to value them. Counterparties hate having their funds tied up and in many cases it can do them damage. So the alternative it to keep the business going but try to shrink it. No road map for how to do that.

Anyone placing odds on whether Andrew Ross Sorkin admits that his sources misled him and the narrative of Too Big To Fail is way off base?

He’ll ignore this but in the highly unlikely event that he’s asked, he’ll say this was a minor point in the book.

Yves is providing a unique public service here. In a previous article she noted none of the print Editors have sent reporters to the trial. They are still up to their old tricks but Naked Capitalism is putting it all on the net.

There’s a little chap in Hong Kong bowing in your direction, Yves.

Speaking of Titanic‘s Captain Edward J. Smith going down with the ship, there’d have been even much greater justice done if J. Bruce Ismay, the chairman and managing director of the White Star Line, which was the owner-operator company behind Titanic, and also aboard her that night, had also gone down with the ship. Instead, in due form, and like the high and mighty characters in the financial ship-wreck you describe above, he saved himself by taking a place in a lifeboat.

Thank you Yves, I’m sending a new donation. And thanks for that end note which reminds us that it’s not a witch hunt but a snake roundup; really, given the plaintiffs, a snake-on-snake tag team match.