By Lambert Strether of Corrente.

A few days ago, the Upshot ran a putatively data-heavy “interactive” explainer on ObamaCare, “Obama’s Health Law: Who Was Helped Most.”[1] It relies on data from Enroll America, the private entity that was tasked by the Obama administration with signing up the uninsured, and which is a reincarnation of Obama for America. The piece is one example of the slick new grammar of data visualization that all the cool kids are playing with these days: Not just the Upshot, but Vox, and FiveThirtyEight, and Quartz, and plenty of the majors, too. Of course, the essence of grammar is that people can construct an infinite variety of statements using it, and this particular piece is rife with false and unexamined assumptions, conventional wisdom taken as fact, category errors, and naive assumptions about official Washington. In fact, if today were not my day to be kind, I’d characterize the piece as puffery.

Anyhow, since the piece is “interactive,” I thought I’d swipe through it by annotating screen shots, as you see below. Maybe when you see one of these things on your cell or your tablet, you’ll be encouraged to whip out your own mental yellow highlighter, and start making your own notes on the howlers you see. There are seven screens in all; I’ll present each screen, and then comment.

Screen 1 exhibits a fundamental confusion that ObamaCare defenders, wittingly or not, make over and over again: They confuse health insurance with health care[2]. The two are not the same, given the high deductibles, high co-pays, narrow networks, narrow formularies, and an insurance system that profits by denying care, instead of providing it. So, “who was helped” is a fundamentally misleading, even disinformative headline: Insurance helps nobody. Only care does that.

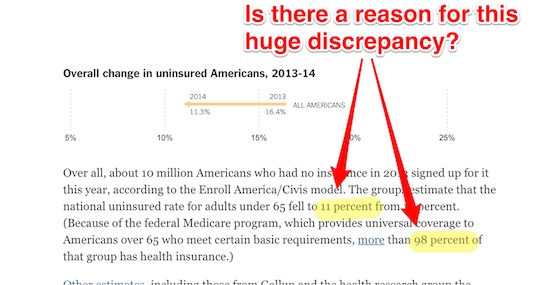

Screen 2, interestingly, uses an arrow pointing left to show a good or at least less bad outcome; left means down, as in a reduction of the uninsured. Of course, the visual grammar of incremental reduction conceals the fact that universal coverage for those under 65 is “off the table,” as the prose makes clear. Apparently, if you’re 64 years and 364 days old, or younger, your life is just worth less than if you’re one day older. Come to think of it, that makes the headline even more disinformative: “Who was not helped” would be just as valid, would it not?

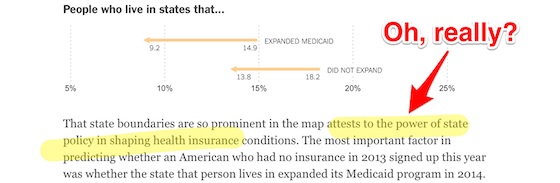

Screen 3 again reifies conventional wisdom. States have “power” over insurance except when they don’t: In national, single payer programs like Medicare or the Veterans Administration.

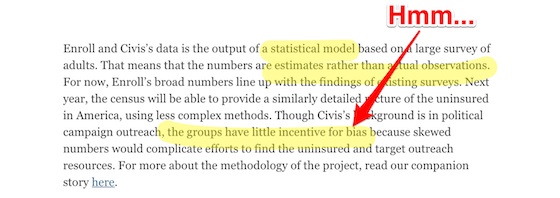

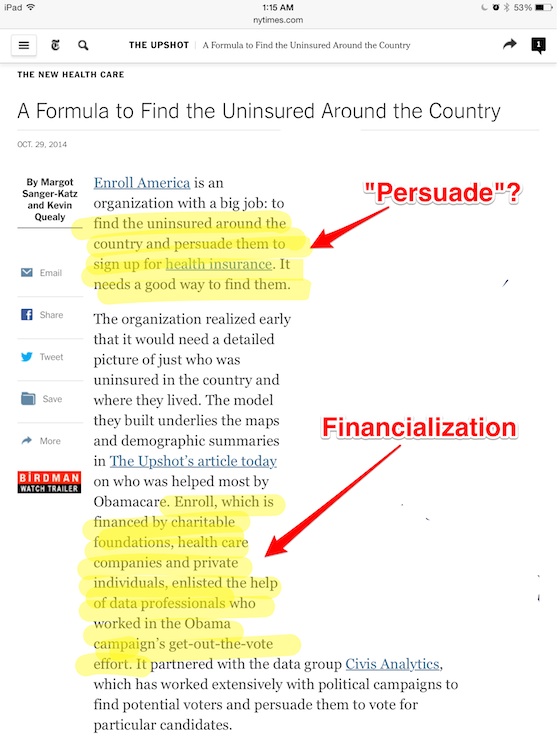

Screen 4 explains, in prose — it’s interesting to think about how these issues might be visualized — the provenance and credibility of the Enroll America data used in the vizualizations, which we’ll discuss further below. What’s not discussed is why we even need this data in the first place. Personally, I find it mind-boggling that we don’t know how many people are enrolled in ObamaCare, and so have to pay a private entity for guesstimates.[3] Imagine if we had to do the same thing for Social Security, or Medicare, or to find out how many people we had working for the Post Office or the Army!

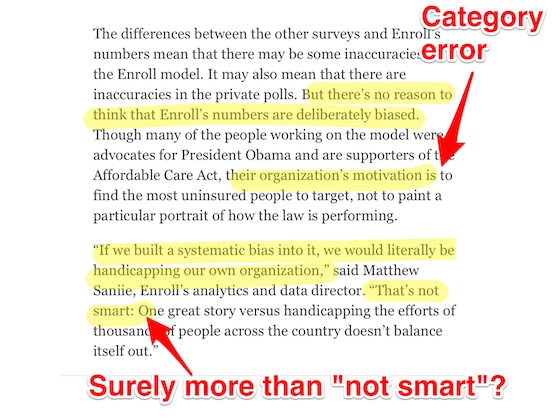

Screen 5 exhibits both a category error and a naive assumption. The category error is “organization’s motivation”; organizations don’t have motivations; only people do. So let’s categorize the kind of people we’re dealing with: People who move easily from roles in political campaigns to roles as staffers to roles in government contracting. Janine R. Wedel, in Shadow Elite, calls them Flexians. (Liz Fowler is, I think, the candidate for Flexianhood health care-minded readers might be most familiar with: Wellstone VP -> Baucus CoS -> White House -> Big Pharma Lobbyist.) Flexians have several distinguishing charateristics, but here is the key one for the purposes of this discussion:

[Flexians are] members of a flex net… Flex nets draw their membership from a limited circle of player who interact with each other in multiple roles over time, both inside and outside government, to achieve mutual goals. While their roles and environments change, the group provides continuity. …. Members of what I call the Neocon core, an informal group of a dozen or so members and a successful flex net, have worked with each other in various incarnations for some thirty years to realize their golas for American foreign policy via the assertion of military power… [M]embers of flex nets are united by shared activities and interpersonal histories. “Interest groups” and “lobbies” so not convey the ambiguous state-private nature of flex nets, which coordinate power and influence from multiple vantage points — often far removed from public input, knowledge, or potential sanction.

That is, the writers of the piece are naive to think that the institution’s “motivations” are the same as the Flexian’s motivations; for them, it’s their flex net that counts, not whichever institution they are embedded in, playing a tempory role. So, when the writers say “there’s no reason to think that Enroll [America’s] numbers are deliberately biased,” they’re naive; there’s every reason to, at the very least, exercise a hermaneutic of suspicion (and one would think that was a reporter’s role). What if David Axelrod (or Karl Rove) were quoting those numbers? Finally, I don’t think I’m the only one not to be re-assured that Saniee would never cook the books because that wouldn’t be “smart”; there could be reasons that would make that smart that we don’t know anything about. I would be much more re-assured if Saniee had said that cooking the books would be wrong. Eh?

In Screen 6, the Times has directed us to a separate, and slightly more technical, article, supposely on Enroll America’s methodology. Instead, the article raises two institutional issues, both part of conventional wisdom, and neither openly discussed.

First, “persuade them to sign up” carefully airbrushes the fact that (some) people are legally mandated to sign up. Given that social dynamic, the article’s focus on how many people signed up is almost laughably simplistic. A more useful approach would compare uptake under conditions of compulsion, as with automobile insurance in some states. I have the feeling that ObamaCare’s numbers would look less impressive that way.

More importantly, the entire Enroll America process exhibits a characteristic called financialization, where middlemen collecting fees crowd their way into every conceivable relationship and turn it into a transaction. For example, instead of a single payer program where everybody is enrolled, and so enrollmen data is very easy to get, we have a program with insurers (middlemen), and marketers like Enroll America (middlemen) to do the enrolling, and data analysts like Enroll America (middlemen) to count the enrolled, with all the middlemen taking a cut along the way.

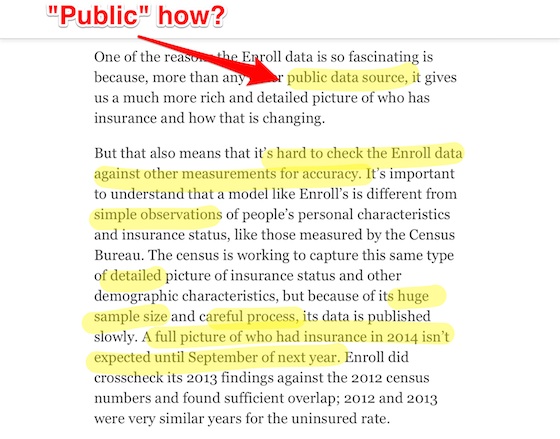

Finally, with Screen 7, we see the Flexian “ambiguous state-private nature” (quoting Wedel, above). In what sense is this data “public”? It’s public, but it’s not really public data, created by and for the public. Literally, it’s created by a private organization, Enroll America. However, if the data were truly created by a public institution that supports “simple observations” for the simple reason that it’s truly universal — like the Census, or Medicare, or the Veteran’s Administration, or Social Security, for example — then the data would be “detailed,” have a “huge sample size,” and be collected with a “careful process.” It’s ludicrous that we don’t even have hard numbers (if that’s what a “full picture” even means) of ObamaCare enrollment until two years after launch.[4] In fact, the data is as crapified as the process that created it, and the program from which it is derived.

So, fun with parsing, eh? I hope when you see examples of this new visualization gramar, especially online, you’ll look at them critically. What they leave out will often be much more important than what they include.

NOTES

[1] The headline itself includes an uneasy compromise between “ObamaCare,” a name once politicized but then denatured by Obama himself, when he said the name was OK to use, and “the health care law,” which ObamaCare’s defenders used when they wanted to avoid using “ObamaCare,” and found “PPACA,” “ACA,” or “Affordable Care Act” too unwieldy.

[2] Perhaps for some, who have good policies, the skills with language and bureaucracy that certain privileges bring, and the time to track the bills, “health care” and “health insurance” are operationally equivalent. That is most certainly not true for everyone.

[3] I would have expected the ObamaCare back-end to be able to provide such data, given its status as the hub through which all enrollment flows.

[4] And enrollment numbers are just a bare mimimum, the lowest possible baseline. How about quality of policies? How about quality of care?

First off, I think there is an obvious reason why the people running Enroll America (that’s an order!) might want to fudge the numbers on the high-side a little bit: it’s called the mid-term elections…maybe some of you have heard of it. And I find it telling that they’re already engaging in CYA regarding the accuracy of their numbers.

Secondly, a personal anecdote: the deductible for the bronze plan that I would have purchased–had I purchased any of the plans available to me–was $6,000+! Now, the reason that I would be purchasing a bronze plan in the first place is because I’m what’s colloquially known as “poor” (I’ve spent enough time in Nepal to know I’m not actually poor, but I digress). That being the case, it should be obvious that even if I did sign up to hand over $50/month in premiums to Blue Crucifix, I would still be paying for my care out-of-pocket…unless something really bad happened to me.

Turns out, something pretty bad did happen to me, not too long ago. In August of ’13 I had a ladder come out from underneath me and I ended up bruising my heel pretty good. I thought I might have fractured it, so I broke down after a week of wondering and went to the walk-in clinic. $750 for a couple x-rays to find out that it wasn’t broken and to be told to take some aspirin and stay off of it for awhile (duh!). I was pretty happy to not have insurance after that little incident, as I would have still been out the $750 plus my imminently affordable premiums.

Let’s be clear: the purpose of the ACA was to find an excuse to give a bunch of gov’t money to health insurance companies, NOT to provide affordable health care. I’ve said it before and I’ll say it again: the only word you need to pay attention to in any bill coming out of congress is the last one in the title–“Act.” The Affordable Care Act is just Congresscritters and the Prez acting like they care about health care. As for the affordability part, I’m 90% sure that’s referring to insurance companies–the ACA has been very affordable for them…

Putting that $6000 in context, the government was telling you that essentially you should in addition to premiums be putting $500 away towards health care coverage because you’d be on the hook for it.

The median income in this country is around $50,000. The government is essentially saying that health care should be more than 10% of your budget. All they did by capping premiums for “affordability” at below 10% is shift costs. You’re still paying out a significant portion of your budget if you get sick. Even more disheartening is each year that deductible resets. So if your costs one year are $5500, the next year you still have to come up with $6000 before they’ll even touch a bill.

Yes, it’s utterly ridiculous. The insurers all seem to have set their deductibles for the low-class plans set at the maximum yearly out-of-pocket. Because affordability.

i must be in a similar cohort, because that is about what i found when i looked at the bronze-crap, as well… about $6250 deductible, BUT i was having to pay approx $500 per month, not $50…

needless to say, i said fuck the insurance-parasites-full-profitability bill and will pay the fine/tax/whatever…

and -for the millionth time- point out the blindness of so-called progressives who completely ignore the mandate aspect, and how the law was tortured to get it to submit to that; AND how the idiots have now made such a huge precedent that ANY kongresskritter who gets a notion can now make it mandatory for this, that, and the other…

the upside is, apparently we are destroying the planet faster than i’m aging or my health is deteriorating, so we will all be dead before i need health insurance, anyway…

so i got *that* going for me…

What a joke! $6000/yr just to play. One little ER hiccup and you’re out another 6K before anything kicks in. I would classify that as the definition of unaffordable if you’re in the middle class living hand to mouth.

The purpose of high deductible plans under O-Care is to make sure hospitals receive the bulk of their billings should you end up in one. That is meant entirely as a benefit to the hospitals. Any benefit to you as a result occurs merely because it cannot be avoided.

Although I truly appreciate the skewering of the insurance industry, you forget to stick it to the doctors, walk in clinics, and hospitals. A skilled and honorable physician should have been able to palpitate your heal and determine it wasn’t broken, and charge you 30$ for that service. If your a hypochondriac, given you an x-ray for another 30$ if you insisted.

I disagree with the idea that a doctor can always determine whether something is broken based on palpating. The reality is that even with X rays fractures are not always readily visible. I actually spent a couple of weeks walking on what the doctor’s in an ER had called a bruised hip. It turned out I had a hairline fracture that was missed. I actually have to wonder what the purpose of health care advances are if the health care industry is not going to actually use the objective data.

In Japan MRIs are cheaper, not because physicians don’t use them but because the technology IS utilized. Here we essentially tell our doctor’s to guess a diagnosis to save insurance companies the costs associated with tests sometimes to the detriment of a patient. I personally think it is reasonable thing for a Dr. to X Ray something if a patient comes in with a pain that occurred from trauma if the pain didn’t improve after a week.

I think you are arguing a distinction without a difference, and that may show the degree to which you’ve been conditioned to accept overdiagnosis.

A hairline fracture doesn’t merit any special attention or treatment UNLESS it is a location that is vulnerable to begin stressed in a way that the hairline fracture could turn into a full-blown break. Did your doctor tell you to do ANYTHING different than you would have done otherwise knowing you had a hairline fracture in your hip?

Let me give you a more extreme example: I sprained my little toe badly and thought I broke it. I called my orthopedist to come in and have a look. He called back and said, “Don’t waste your time and money. Tape your little toe to your next toe.” The treatment was the same, break or no break, so why bother with the X-ray?

Tell me how many doctors would tell you that and tell you NOT to give them your money.

Great work, Lambert. And these fools wonder why folks aren’t head-over-heels in love with Obamacare and racing to the polls to vote for Democrats.

BTW:

Once they privatize the Post Office, we WILL know that number. As to the Army, don’t forget to include all the mercenaries.

Right. Because if there is one group that will try something to help the uninsured, it is the republican party. Their proposals are awesome; said proposals being summed up as: die.

As an individually paying Massachusetts member of “the insured”, I am nauseated by the ACA cheerleading of the Democratic candidates and look forward to seeing these posterior chapeaus get their lunch eaten tomorrow.

Obama quote: ‘no more bailouts’ (a la auto makers, banks)

Semantic change to “Affordable Care Act” (Obamacare) Not about care. Definitely not affordable.

All about getting $$$$ to insurance companies. A BAILOUT!

‘You vil do as I say, or, you vil be fined.’

“(Nancy DiParle is, I think, the candidate for Flexianhood health care-minded readers might be most familiar with: Wellstone VP -> Baucus CoS -> White House -> Big Pharma Lobbyist.)”

Although Nancy-Ann DeParle might well qualify as a “Flexian,” that particular employment string belongs to Liz Fowler.

Ack, I got my villains confused. Fixed! Nice to see you, however, and thanks for all the good work you do at PNHP.

Good work, as usual–this is your field man–you know it and seem to love delving into it!

Just a note here–it’s not just insurance that is gaining from all this it is the whole “industry” that is, in my view, based on fraud, anti-science and politics. I include here the medical profession, the drug companies and so on. One of my big suspicions when health-care and even universal coverage was that these political forces that came together in 2009 were, in part, trying to re-capture a market that had begun to migrate towards “alternative” health practitioners. I have believed, for some time, that the system in place before Obamacare would have caused more reform because doctors would be forced to move towards more holistic methods, i.e, the medical model that we are not a list of body parts but a mind-body system linked to communities and cultures. This idea is now in decline and both HC providers and patients are met with a new set of perverse incentives.

At any rate, Obamacare should be repealed and medical practice should be reformed based on the idea that we are whole and not a series of parts and that we use real science (as opposed to fraudulent drug-company science) to work towards relieving disease and not individual diseases that are usually manifestations of stress, a dysfunctional life and a dysfunctional society. That whole discussion is a big one but we ought to engage in it and Obamacare has put off that larger discussion by forcing us at the point of a gun to participate in “official” medical care.

Note that the health insurance industry does not profit by denying care. It profits via the MASSIVE cash flow generated by the premium stream.

The reason for the denial of care is a bit more complex. Essentially, when your profits come from cash flow, you are always looking to maximize that cash flow, and that means maximizing the number of customers you have. The way of course to maximize the number of customers is to have the most price-competitive product, i.e., sell for as low as possible. The problem we have in health insurance is that this results in the product selling below its actual cost. To recoup for this, the companies resort to denial of care. Which means that denial of care is done in order to break even on the product itself; not to make a profit. [I was told this quite explicitly by the finance gurus at my former (health insurance company) employer. The only thing we, the health insurance people, were to worry about was not losing money. They (the finance people) would then produce the profits.]

The premium stream IS essentially what they are protecting when they deny care.

The problem is not the product is being sold below cost at all. As a matter of fact costs are being manipulated to maximize profits and consumers are caught in the middle.

It goes something like this : Hospital bills patient insurance $150. Insurance company insists that it get a discounted price. It gives hospital $50. Hospital decides it can only break even if it gets $50. Hospital raises price to $450 so that it can collect the initial $150 it wanted to make a profit. Insurance company decides it needs more money to cover increased payout. Insurance company raises premium or increases the deductible to maximize it’s profits. Meanwhile the guy without insurance gets charged $450 for a service that a hospital could break even on with $150 all so the insurance company can feel it is getting a “value.” Meanwhile the consumers are caught in the middle. There’s nothing more fun then having to be in the middle of the idiocy. My insurance company routinely blames the hospital for things like the fact that I had a out of network doctor bill in an in network hospital. My hospital routinely blames the insurance company for why I’m stuck with a bill like when I got billed as a non emergent visit because “coding” said I had a headache(even though that headache was accompanied with an extremely high BP and I have a family history of heart attacks and strokes in early 40s and 50s which makes my migraine headaches a little more problematic. ) It almost seems like they’ve pulled from the Republican/ Democrat playbook where they take turns blaming each other.

Thanks for this. I found the whole NYT article suspect. It’s almost as if no one actually wanted to know what affects the law had.

Thanks for staying on top of this Lambert.

You’re welcome!

Thank you for an excellent dissection of a multifaceted topic.

I wish that the Grey Lady would become more Manichean and at least attempt to live up to their motto of “All the News That’s Fit to Print”.

Otherwise, they’ll recede further and faster from their cherished self-proclaimed status of paper of record.

I live in NYC, am poor, and pay approx. $120/mo. (after subsidies) for a silver plan with a $250 deductible, and a $2,000 annual cap. Finding docs who accept the insurance is a bit of a challenge, and I could probably just pay as much out of pocket for the annual preventive stuff I need — but I am covered in the event of illness/injury. It’s not great, but it’s not terrible either, for now. However, if my freelance gigs pick up and my income goes up, I’ll have to pay more, and I’ll have to pay back the difference. But Art Guerrilla, I’m thinking that either you’re not as poor as you think you are, or … I dunno, somehow you got rooked.

Talking about misleading information. This article is full of misleading information. Assuming people are so dumb that they do not know the difference between health insurance and health care is arrogant, and an insult to the American people.

The only system we have and have had for many decades is health insurance for people under 65 years of age. It is not politically realistic to anticipate anything different unless we are able to vote out the lawmakers who are obstructing health care reform and who only want to return to the pre-ACA status so that the corporate medical industrial complex can go back to filling those deep pockets. The regulations of the ACA are hurting them.

Health insurance provides access to health care! So being insured is synonymous with having access to health care. Without insurance many have been left to die. Per a Harvard study done in 2009, 45,000 uninsured Americans died per year due to the inability to access adequate health care. The ACA has significantly reduced that number, thus saving lives, and will continue to reduce it even more. ER stabilization is not adequate health care.

As an RN, I see the numerous benefits of the ACA. I see lives being saved and families being saved from the pain and stress of not having access to health care. People must ask themselves why anyone would want to take away or undermine the only health care system this country has had and has strived for the past 50-100 years, when there is no realistic way to switch simultaneously to a better alternative .