Yves here. Dueling opinions across posts! One of the observations made here is by Jim Hamiliton, who says that the upsurge in US unconventional energy production is what led to the price downdraft, and that once that production is taken off line, prices will revert. While that is narrowly true, John Dizard at the Financial Times argued that could take longer than most observers anticipate because too many players have access to cheap funding (what goes unsaid is they must also have perverse incentives to keep producing).

By Jérémie Cohen-Setton, a PhD candidate in Economics at U.C. Berkeley. Originally published at Bruegel

What’s at stake: Opec’s decision to leave its output ceiling of 30m barrels a day unchanged on Thursday has sent crude prices into a tailspin. Under normal conditions, falling oil prices would be a favorable macroeconomic development, but under current circumstances this is making the job harder for central bankers who struggle to deliver on their inflation targets.

Demand and Supply since September

Wonkblog writes that there’s one short-term reason and three longer-term reasons for this slump. The meeting was the most important in years, because it came amid a pre-existing slump in prices. Everybody wanted to know if OPEC would take any action to halt the decline. It didn’t — presumably because its members decided it was wiser to weather the current storm — and crude oil prices immediately tanked. The long-term reasons include booming U.S. and world oil production, little demand in Europe and Japan, and improving automobile fuel efficiency standards.

Brad Plumer writes that up until very recently that US oil boom — along with increases in Canada and Russia — had a fairly minimal effect on global prices. That’s because, at the exact same time, geopolitical conflicts were flaring up in key oil regions. There was a civil war in Libya. Iraq was a mess. The US and Europe slapped oil sanctions on Iran and pinched that country’s exports. Those conflicts took more than 3 million barrels per day off the market. Things changed again around September 2014. Many of those disruptions started easing. Libya’s oil industry began pumping out lots of crude again. And even more significantly, oil demand in Asia and Europe has been weakening — particularly in places like China, Japan, and Germany.

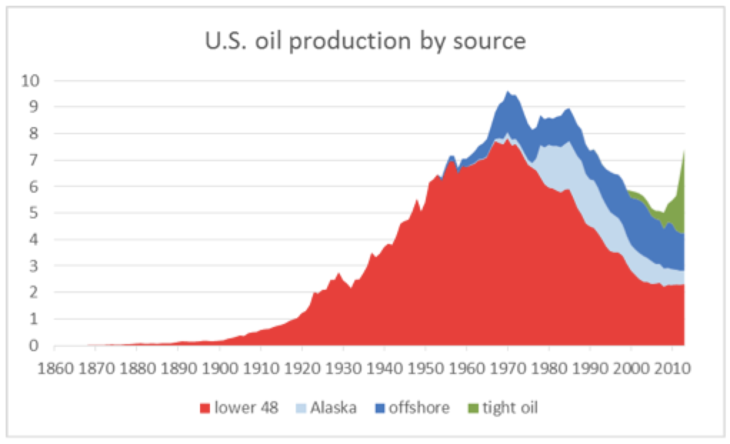

James Hamilton writes that the current surplus of oil was brought about primarily by the success of unconventional oil production in North America, most new investments in which are not sustainable at current prices. Without that production, the price of oil could not remain at current levels. It’s just a matter of how long it takes for the high-cost North American producers to cut back in response to current incentives. And when they do, the price has to go back up.

Brad Plumer writes that this marks a big shift in global oil politics. Essentially, OPEC is now engaged in a price war with oil producers in the United States. The cartel will let prices keep falling in the hopes that many of the newest drilling projects in the US will prove unprofitable and shut down. It’s very cheap to pump oil out of places like Saudi Arabia and Kuwait. But it’s more expensive to extract oil from shale formations in places like Texas and North Dakota. So as the price of oil keeps falling, some US producers may become unprofitable and go out of business. The result? Oil prices will stabilize and OPEC maintains its market share. The catch is that no one quite knows how low prices need to go to curb the US shale boom. According to the International Energy Agency, about 4 percent of US shale projects need a price higher than $80 per barrel to stay afloat. But many projects in North Dakota’s Bakken formation are profitable so long as prices are above $42 per barrel. We’re about to find out how this all shakes out — and which numbers are correct. Tyler Cowen writes that because of fixed costs and option value, a currently unprofitable project can remain up and running for a long time to come.

Oil Prices and Inflation Expectations

VCpost writes that one of the most obvious effects of falling oil prices is that it brings down inflation and exerts a downward pressure on inflation expectations. Under normal economic conditions, falling inflation could be seen as positive under, but in the present circumstances with major economies struggling to meet the inflation target of around 2 percent, plunging oil prices is not good news.

Tony Yates writes that the argument for loosening is that on account of oil being a major input, it will raise potential output relative to actual output. Which in models like those central banks uses is deflationary. Also, if inflation expectations are extrapolative, a temporary oil price fall would lower inflation expectations, transmitting into core inflation. (Inflation itself being lower on account of the fall in expected inflation). Neil Irwin writes that to the degree those one-time shifts change peoples’ expectations about future inflation, and lead people to doubt the credibility of the central banks’ promises to keep inflation at 2 percent, it is a problem. That’s particularly true when inflation expectations are already below where the likes of Mario Draghi, Janet Yellen and Haruhiko Kuroda would prefer.

Michael Mackenzie writes that while the Fed has played down the recent drop in break-even measures, the slide in oil prices has not escaped the attention of consumers. The University of Michigan’s consumer sentiment survey last week showed a drop in long-term US inflation expectations from 2.8 per cent to 2.6 per cent, the lowest level since 2009. Olivier Coibon and Yuriy Gorodnichenko point that household expectations might be more important than professional forecasts for the dynamic of inflation. More than half of the historical difference in inflation forecasts between households and professionals can be accounted by the level of oil prices. Because gasoline prices are among the most visible prices to consumers, households pay particular attention to them when formulating their expectations for other prices. Coibon and Gorodnichenko present evidence that firms’ inflation expectations are, in fact, better proxied by household than by professional forecasts.

Other Channels

Gavyn Davies writes that the disinflationary effects are uncontroversial. But the boost to growth is more debatable, since lower oil prices involve a redistribution of income from oil producers to oil consumers. Why should this reallocation of resources lead to a rise in real gross domestic product? It is because of time lags. Oil consumers, which are mainly households, have seen their real incomes rise, perhaps permanently, and they are assumed to allocate part of this gain quite quickly to increased real expenditure on other goods and services. Oil producers, on the other hand, are mainly rich governments and corporates, and they may take much longer to reduce their expenditure in line with their lower real incomes. That, anyway, is what economic models tend to assume when oil prices decline for supply-related reasons.

James Hamilton writes that lower gasoline prices likely also contributed to the recent rise in consumer sentiment. Historically a 20% drop in energy prices would predict a 15-point rise in consumer sentiment. That relation weakened considerably as consumers got accustomed to the up-and-down yo-yo of prices in recent years. Nonetheless, consumer sentiment is now at the highest level it’s been since the Great Recession

If you’re a gibbering fool who likes it when commodities are expensive, or a central banker (but I repeat myself), then this is indeed a ruinous development.

“but under current circumstances this is making the job harder for central bankers who struggle to deliver on their inflation targets.”

Where “current circumstances” would be the globally comprehensive neoliberal fiscal turpitude?

It seems to me that the drop in oil prices will only provide a meaningful increase in consumer spending if the reason for any lack of spending is because of higher oil and gas prices. If oil and gas prices fall, but people are either saddled with other rising costs or have other issues to deal with, like weak employment opportunities, then there may not be much of a bounce. Given the lack of any increase in spending power, i.e., the fact that the <1% have gotten all of the income from productivity gains over the past two decades at least, I doubt there'll be much effect. None of the commentators seems to have considered that.

And if the effect of declining oil and gas prices is so stimulatory for homes, why not for governments too? This should be another indicator that austerity is just bad policy. Again no comment there, other than to mention the lag effect for large purchasers like goverrnments. It's a shame that the economsits just keep pounding the same polygonal shaped pegs into ellipsoidal holes.

We’re all getting a lesson in price-elasticity of demand. This is where a one million barrel per day surplus in oil production, a small fraction of the total, leads to a 25 percent decline in the producer price. So what to do with it? One possibility is Congress taking the opportunity to increase the gas tax. Right now, a 30 cent increase in the gas tax would only cause a 15 cent increase in pump price, because the Saudis and other producers would eat the other 15 cents. The money would go to employment repairing the roads and bridges, which we need to do. I don’t expect the current leadership in Congress to even talk about such a plan, but creating jobs fixing the infrastructure is something to talk about, and inflation has eroded the value of the present gas tax.

Damn good idea, but like most damn good ideas, it will never happen. Certainly not once January rolls around.

Not so good of an idea. Who would a gas tax hit the hardest? The upper 10% or the lower 50%?

The lower 50%. A gas tax, like most sales taxes, is a regressive tax. The upper 10% drives Priuses and Teslas – they don’t even hardly use gas. The bottom 50%, if they drive a car at all, drives a car from the 1980s. A car from the 1980s, of course, uses a lot more gasoline than Elon Musk’s latest invention.

Black Friday and cyber Monday proved to be flops, so cosumers are not spending.At Best, thay are paying down debts.

I think I mentioned it in a comment some time back that the main benefit to the US consumers from the QE is going to be cheap oil for US via the dirt-cheap funding of shale. How big a benefit it’s going to be is still a question though..

The crash of oil prices are a look in the rear view mirror of the world economy … Demand is down because of austerity across the board and the ominous signs of WWIII with the sanctions and military maneuvers against Russia. The demand destruction that has precipitated this crash is ongoing.

While consumers will welcome lower gas prices they also know that falling wholesale and retail sales mean scant raises. With healthcare in flux and those less fortunate already part of demand destruction there is little hope for a recovery. What we’ve had and will have are lying government figures and plenty of market whipsaw …

The last oil price crash, in 2008, was demand-driven. Is this really reflecting an expectation of increasing supply or an expectation that we’re going to have further economic crises? The various big players aren’t looking too good – China is looking wobbly, Japan has caused a recession with a sales tax increase – and plans another!, and Europe remains in effective recession. Even the best-off major economy, the US, is only doing mediocre, and the Republican takeover of Congress risks a shutdown confrontation that would almost certainly precipitate a global depression.

If the banks are having a problem meeting their inflation targets then they should go back to including food and energy costs into their equations. What kind of a crazy world have we got here when lower prices for the masses is not a good thing for all?

In my eyes this is a narrative in the making being as there is no official reason the Saudis cut their asking price per barrel. The discussion is great, owing to the contributors and commenters, but it’s easy to get lost in the flood of input of opinion.

To my mind when these events become some abstract of possibilities that seem to confound my limited understanding

of what inferences to make, I’ll generally scrap what I’ve read to date and start over with the material facts.

It occurs to me that if the Saudis possess the wherewithal to sustain the affects of a lengthy cut in their asking price per barrel, they could also reverse market price by removing a like quantity in production, thus reviving the market.

I don’t think the Saudis are flying solo on this. Who is supporting them and Why?

The Saudis are and remain the swing producer. Oil fell below $90 when the Saudis made clear they weren’t supporting it at $90. And the reports out of the last OPEC meeting was that the other producers wanted production cuts and the Saudis didn’t but the Saudis prevailed.

As to Yata’s point, in our earlier posts, we said this was a brilliant move by the Saudis. They get to hurt their prime geopolitical enemies (Iran being top of the list, but the Saudis are also mad at the US these days) as well as commercial competitors (particularly fracking and renewables).

I was thinking both beyond and also possibly certain powerful constituencies within the category of sovereign oil producers. As you alluded, there are geopolitical implications to this move that were outside the focus of this article.

The Saudis are basically flying solo. They figured out that if OPEC does production cuts, everyone except the Saudis cheats and produces extra. If, instead, there are no production cuts, the Saudis can drive everyone else bankrupt, pretty much. Because Saudi oil is *far* cheaper to produce than any other remaining source in the world, and they’re sitting on a huge amount of it.

As Yves says, this move hurts Iran, Russia, the US/European “multinationals”, the wildcatters, and ISIS/ISIL all at once. There’s no downside from the Saudi point of view (unless Russia invades or something).

So when the world is in a depression like this what gives first? Governments have to stimulate demand and do big projects. Let us all hope that the big projects are not manufacturing millions more combustion engine cars; toxic batteries; and refined gasoline. If the big projects which will require energy just create more of the same we will have wasted a good financial crisis. And will create inflation much higher than 2%. And be right back where we started with global warming and inequality skyrocketing. When it comes to oil there probably is no way to establish a market price because it is like establishing a market price for money itself. The price of oil will have to be fiated. And controlled.

Humanity exists in a CRT/ART in a CRT/ART, and builds CRTs inside CRTs, which are largely arbitrary, which is why they always implode, which is neither here nor there to the universe, because humanity largely lives in its spoil pile.

If you want to get anywhere, other than swapping dresses, you have to turn 180 degrees from the ground, which in the case of modern society is money, which means that you have to reorganize your mind, which the vast majority cannot do in real time, but that is the way you turn an aircraft carrier on a dime at full speed, which is an illusion of time to begin with, by changing the channel, the frame of reference, beginning with the return.

The universe is a circle with a switch, and there are an infinite number of numbers between 1 and 0. Pick one and make a gate. The loads create perceptions in time, environmental capacity. More hours spent in failing schools, increasing income disparity with tax on real estate inflation, money laundering, isn’t the answer, but it is a problemsolution, which is why the critters herd up and elect a bully; they just want the D fish, regardless of need, to temporarily relieve their bipolar anxiety.

Remember when we were talking about the $45 hinge contract price for oil? What is the relationship between oil, gold, CAN$ and UST? How much toilet paper did silver leverage help the Fed to print? Sorry, from the perspective of labor, PMs are way, way over capacity, Switzerland or no Switzerland.

Like all traps, the liquidity trap is nothing more than a shared perception. Funny, the critters skip Genesis, and read what confirms their assumptions, electing leaders to leverage their assumptions with money to scale, at increasing profit, time consumed by empire, with make-work, of which fracking is just the latest iteration.

A feminist, a chauvinist and a homosexual, the counterweight, an economy does not make, for what should be obvious reasons, unless you want to be trapped in the elevator. You can apply your brain as a tuner, a motor-generator, whatever you want, so long as you maintain its flexibility, but empire efficiency demands inflexible, programmable, certified automatons.

Appreciate your spouse, encourage your children to think for themselves, and leave the revolving bullies behind, on the train from and to democracy, with the upper middle class gatekeepers travelling in a smaller circle, faster and faster. Be the needle at the station.

Bay Area IPOs are about increasing extortion efficiency with money laundering, providing the empire with an exit, increasing pressure on decreasing volume. Participation isn’t falling by accident. Feudalism is just a counterweight, whether it’s in Russia, China, Germany or California.

The banks are always in quicksand, Congress fairly represents the majority, jumping in to prop them up, joining the divide and conquer war, and sooner or later the flippers all get caught, because they cannot make the quantum leap. You might want to check earth EMF/CEMF, before you take the critters with panties in a bunch, creating the acts of stupidity, seriously. In 25 years, at least 1/3 of the population on this planet will be gone. Empire or no empire, what you replace it with is up to you.

My kernel begins with 3 phase, which is why the critters cannot see it. Power is transformed on a relative timeline, only from the perspective of the closed system. Net voltage is zero. And that, my friends, is quantum physics, looking ahead, turning the empire on its head, by discounting the redundancy and fascism created by feudal media misdirection.

The frequency of the average human is no more than a knat relative to the universe. Vision is not a function scaling knats.

Can I have some of that which you are drinking?

are you terry gilliam?

but seriously, if i understood you correctly (big if), fascism is not the word here. “The system” is not a closed system that limits our ability to think or whatever, it actually works by NOT WORKING, (its a feature not a bug).

whats perverse is that it just goes on, even though everyone knows its fucked. its not a secret that people need to reprogram their minds for or whatever, its OBVIOUS, and yet it GOES ON even though EVERYONE KNOWS. Were all already atuned to it.

this is whats weird.

kthxbai

Yes, God forbid we have lower prices. How these bankers have convinced everybody that the need to pay interest on the mountains of debt is the main priority of life on Earth is beyond me.

Be careful what you wish for. Deflation is extremely destructive.

Deflation is the natural order of things, i.e., higher productivity leads to low costs [all things being equal]. The only time it doesn’t work is in a system such as we enjoy today where the very purpose of life is to create/service debt.

But doesn’t that depend on what causes the deflation? Deflation due to lower prices from price competition, etc. is good and isn’t, strictly speaking, deflation in a macroeconomic sense since the money from price cuts still exists and will be spent somewhere else by the buyer who now has extra cash.

Destructive deflation is constricting the money supply so tightly that the economy shrinks due to an inadequate monetary base (a-la the Great Depression, or current efforts by the European periphery to pay down foreign-owned sovereign debts by raising taxes and cutting spending).

If deflation of the former type was truly destructive, then we should have had armageddon given the massive “deflation” of information technology prices (which constitute a larger expense for most companies than energy costs) not to mention the “deflation” of workers’ wages which somehow is always seen as a good thing by elites.

These prices and the volatility that goes into the price history through it (as it will not soon be forgotten even if prices might rise in the near future) may well precipitate bankruptcies in esp. the fracking oil industry which is deeply in debt or highly leveraged. This in turn might, given the way markets are already rattled due to e.g. the Ukraine crisis etc., be the tipping point to set off another 2007/2008-style crisis.

Deflation is destructive to empire, the counterweight, but exists in an equilibrium…the Fed is trying to titrate…chaos is reality/order is the illusion/noise is what you make of it. Basically, the corporations are all operating at a real loss, subsidized by G to get accounting profit, putting all the small businesses out of business, for now…loading the spring…threshold is when that counterweight drops. Increasing rates reverses leverage, and no one wants to be responsible for the MAD derivative explosion. Whether it’s fracking or anything else is of no concern to labor.

Deflation is destructive to the 99%. I suggest you read up on the after effects of deflation in the late 1920s (1929 to name the precise year).

yes, it is destructive, and labor is quite creative with the result.

I’m no fan of the 99% in case you have not been following along.

my pop educated me on the reality on the ground at the time. I don’t need to read the propoganda.

Ain’t indoctrination via blood lines great!

Kevinearick–

“Basically, the corporations are all operating at a real loss, subsidized by G to get accounting profit”

Some of us are having trouble with your poetic style—or word salad–but this is as clear and apt as clear can be. Our economy operates in a state of ongoing physical loss or decline. Resources are destroyed; they are never created–nor renewed–this is what unsustainable means. This process of terminal descent is masked by a fake accounting system.

Humans have not always lived like this. The needful thing is to walk away.

–Gaianne

With regards to Yves’ comments on “perverse incentives”:

Drill to keep the lease.

Produce to keep the lease.

Many large scale development projects in the Bakken, Eagle Ford and Marcellus (gas) have large operators who partner with several other companies in what is known as a JV. This is how it is done in the oil patch. Not all projects are traditional bank financed. Oil companies often act as banks to one another.

Seems like the energy glut is about not orchestrating the introduction of alternative fuel/energy. A lot of the petroglut seems to be tar sands and mid-continent fracking, which is stranded without pipelines.

But the growing building of petroleum tank cars for the railways, if laid off, is another kneecap, impacting steel and fabrication shops.

While I’m willing to grant that perhaps Saudi Arabia initiated this price war for the reasons stated (punishing its enemies while killing off shale oil), I’m not sure that will be the result. Predatory pricing is only successful if you can outlast your competitors, and that’s not at all guaranteed for Saudi Arabia in this current price war.

1) Demand truly is shrinking. That means even if a bunch of fracked oil goes off the market, that still leaves a glut of conventional oil. While the KSA may have the stomach for a price war against high cost unconventional producers, can they also withstand a price war against conventional producers?

2) While everyone talks about unconventional production (e.g. deep water drilling, shale, tar sands, etc), *conventional* production will likely increase in the next few years. Check out http://www.zerohedge.com/news/2014-11-30/we-are-entering-new-oil-normal. The summary is that production in Libya and Iraq will continue to increase, while if/when a political settlement is reached with Iran, it will resume its previous exports. In total, this would add 4 million bpd of cheap, conventional crude, which would offset any declines from unconventional sources.

3) To compound this, while the KSA may be able to weather current prices, other producers (e.g. Venezuela, Russia, and even a few M.E. countries), faced with yawning deficits, will likely increase their production as much as possible. Countries with sovereign control over oil resources frequently set a budget target, then produce enough oil to meet that budget. Paradoxically, that means that when oil prices go down, they *increase* their production to meet their budget targets. While this is ultimately a self-defeating strategy, no politician cares about the long term when hungry people are rioting in the streets.

4) I’m not an expert on shale oil finances, so I won’t speculate about how much production gets shutdown at different price points. But I do remember the old maxim “don’t fight the Fed”. It still holds true. And shale oil is a product of the Fed’s current cheap money policies, which means Saudi Arabia is picking a fight with the Fed, even if it’s by proxy. When faced with abandoned fields in North Dakota and soaring unemployment in oil patch states, who’s to say that the Fed won’t do everything in its power to keep the industry going? Does Saudi Arabia really feel it has the financial resources to fight a proxy war with the Fed, which is what a price war against U.S. fracking truly is?

5) Finally, for the rationalist in all of us, I quote Keynes “The market can remain irrational longer than you can remain solvent.” That applies even if “you” are the mighty Saudi Arabia with hundreds of billions of dollars in reserves (especially if your opponent is the Fed, per my previous point). Maybe fracking doesn’t make sense at $80/bbl. Maybe Arctic drilling should be shut down at $70/bbl. Maybe the people should throw Putin out when oil hits $50/bbl and the Ruble’s only worth is as kindling for firewood. And yet none of these things may happen. Irrationality in a market as tied up with strategic, nationalist, and geopolitical concerns as the oil market, with players as big as entire sovereign nations, means a market can behave irrationally for a *long* time.

In short, I’m not sure Saudi Arabia truly understands the war they’ve just started, and may yet wish to reconsider…

“While that is narrowly true, John Dizard at the Financial Times argued that could take longer than most observers anticipate because too many players have access to cheap funding (what goes unsaid is they must also have perverse incentives to keep producing). ”

Sure — their business model is land-flipping, not oil & gas production. If you look at it as a land-flipping business model, it’s obvious what the perverse incentive to keep producing is.

Cheseapeake is explicit in its land-flipping business model, it’s actually published in its annual reports. Some others are a little cagier about it but do the same thing.

“According to the International Energy Agency, about 4 percent of US shale projects need a price higher than $80 per barrel to stay afloat. But many projects in North Dakota’s Bakken formation are profitable so long as prices are above $42 per barrel. We’re about to find out how this all shakes out — and which numbers are correct. Tyler Cowen writes that because of fixed costs and option value, a currently unprofitable project can remain up and running for a long time to come.”

It’s worth noting that the land-flippers will advertise very low breakeven oil prices. The real breakeven prices may be higher.