Yves here. Nicholas Shaxson’s landmark book on tax havens, Treasure Island, described how the US was the biggest sponsor of what Shaxson called “offshore,” or tax havens and tax secrecy. He tells us how the US is working to keep it that way.

By Nicholas Shaxson. Adapted from a post by the Tax Justice Network.

The U.S., seen from space

If people stash their wealth or earn income overseas, that is just fine — as long as their tax authorities get the information they need to tax that wealth or income according to the law, and as long as money laundering and financial crimes can be effectively tracked, and so on. Where there are cross-border barriers to legitimate tax collection, law enforcement and other instruments of democratic societies, then there is an offshore problem.

The only credible way to provide the necessary information is through so-called automatic information exchange (AIE), where governments make sure the necessary information is available across borders, as a matter of routine.

For years, those who advocated AIE were ignored or even ridiculed. Pie in the sky, many said. The OECD, the club of rich countries that dominates international rule-making on tax and tax-related information sharing, was for years pushing its so-called Internationally Accepted Standard which was, well, the internationally accepted standard for cross-border information exchange, despite being only slightly better than useless.

In the past couple of years, however, the world has turned.

The OECD is now in the middle of putting in place a system – known as the Common Reporting Standards (CRS) – to implement automatic information exchange (AIE). The CRS is the first ever potentially global system of AIE, and although it has serious shortcomings and loopholes, it is potentially a major step forwards from a largely transparency-free past.

Meanwhile the European Union had been moving ahead with plans to beef up its own, older schemes for AIE, notably through amendments to tighten up its loophole-ridden Savings Tax Directive and other related initiatives (for an overview of that, see here.) The United States, for its part, has been rumbling forwards with its Foreign Account Tax Compliance Act (FATCA), which is, at least technically speaking from a self-interested U.S. perspective, fairly strong. (In fact, the OECD’s CRS is modeled on FATCA.)

But – and here comes a big ‘but’ – how do these different initiatives mesh together? Might anything fall between the cracks?

The European Union, for its part, seems to be working hard and in fairly straightforward fashion to get its ducks in line with the CRS, the OECD’s emerging global standard. It will be incorporating a lot of the OECD technical standards into EU law, in cut-and-paste fashion, and will add categories to include in the mix: such as covering the all-important insurance sector more comprehensively than the CRS does, and covering other categories of income and capital including income from employment, directors’ fees, pensions, and ownership of and income from immovable property.

But the United States’ position on meshing FATCA with the global standards? Well, now there’s a story.

That building in the Cayman Islands is still there

President Obama recently gave his State of the Union address, with an eye to his legacy. He’s taken an interest in tax haven issues in the past, declaring in 2009 that Ugland House, a building in the Cayman Islands that then housed some 19,000 companies, was either

“the largest building in the world or the largest tax scam in the world. . . it’s the kind of tax scam that we need to end.”

With statements such as this, he managed to get himself some serious anti-tax haven credentials, at least from a public relations perspective.

But how has the Obama administration shaped up on tax havens since then?

Well, in the details of the emerging global architecture on tax and financial transparency lies an issue – we’d go so far as to describe it as an international outrage – that is likely to tarnish his legacy seriously. A failure to tackle this will make many wealthy people wealthier and poorer people poorer, and will undermine crime-fighting, in the U.S. and around the world.

USA: ‘we’ll pretend to join in’

The U.S. position on the emerging global transparency architecture has basically been to say ‘we are doing our home-grown FATCA project, and it’s technically similar to the OECD’s CRS, so we don’t need to join the CRS.’ Which, at first glance, looks like a position that could be defensible, depending on the detail.

A crucial part of the detail, however – and this is where the vortex starts to come in – hangs on the all-important question of reciprocity. The United States is extremely keen for other countries to pony up information about U.S. taxpayers hiding their cash offshore and overseas – as it should. But when it comes to reciprocity, or providing information in the other direction, things change.

The U.S. (again, on the surface) has said that is committed to sharing FATCA-related information under so-called Intergovernmental Agreements (IGAs,) which are bilateral deals that stipulate how and in what circumstances the relevant information may be handed over to foreign governments. (There are three basic models: 1A, 1B and 2: only the Model 1A agreements are reciprocal; the Treasury’s U.S. public list of IGAs is here, with the different models explained here.)

In May last year Alex Cobham at the Center for Global Development wrote a useful blog entitled Joining the Club: The United States Signs Up for Reciprocal Tax Cooperation, welcoming the U.S. commitment to reciprocal information exchange, as far as the announcement went. By November, though, as the details came through, he began to raise the alarm. In a post entitled Has the United States U-Turned on Tax Information Exchange? he wrote:

“A full commitment to reciprocal and automatic, multilateral information exchange, backed by legislation to ensure beneficial ownership information is available, has been replaced by an indication that the United States will seek to provide information in the few bilateral Foreign Account Tax Compliance Act (FATCA) agreements that require it, for which the United States accordingly commits to ‘advocate’ for domestic legal changes that would create the necessary beneficial ownership transparency.

After the midterm elections, the success of such advocacy seems unlikely. But it would be a sad irony if the legacy of an administration that began with such strong rhetoric on shutting down tax havens was to leave the United States as the biggest remaining centre of anonymous company ownership.”

Now that more information, source material, and details, is available, matters look worse still. The precise details of what the US is offering are alarming.

The gory details

The United States is already a tax haven for foreigners, as outlined in detail in the “Fall of America” chapter in my book Treasure Islands, and, more recently, here. To achieve effective reciprocity with other countries the U.S. would need to tighten up its rules considerably, and in numerous ways.

The U.S. Treasury’s Financial Crimes Enforcement Network (FINCEN) seems to be taking a lead on some of the internal stuff to prepare the ground for international co-operation, with new rules entitled “Customer Due Diligence Requirements for Financial Institutions.” Here we get into the weeds a bit.

How good are the Fincen rules? Well, for starters, on page 45152 Fincen says it

“is proposing rules under the Bank Secrecy Act to clarify and strengthen customer due diligence requirements for: Banks; brokers or dealers in securities; mutual funds; and futures commission merchants and introducing brokers in commodities.”

Our emphasis added. The first thing to notice is that these are just proposals. To get approved, they’re going to have to get this lot past Senator Rand Paul, the combined lobbying power of the Big Four accounting firms and Wall Street and Florida banks, and a host of other vested interests.

Then there are the loopholes larded through this document.

For instance, the players identified in the Fincen paragraph above are just a subset of actors in the financial menagerie that is out there. The document continues:

“In addition to input from covered financial institutions, FinCEN sought and received comments on the ANPRM [Advance Notice of Proposed Rule Making] from financial institutions not subject to CIP [Customer Identification Program] requirements, such as money services businesses, casinos, insurance companies, and other entities subject to FinCEN regulations.”

There are no plans to cover these chaps as yet. And this is a problem: in many countries insurance policies, for example, are classic tax evasion and secrecy vehicles — and they’re already carved out.

Then there is the question of trusts, where no useful beneficial ownership information seems to be required. There is this, mostly on p45160:

“There are many types of trusts. While a small proportion may fall within the scope of the proposed definition of legal entity customer (e.g., statutory trusts), most will not. . . . identifying a ‘‘beneficial owner’’ among the parties to such an arrangement for AML purposes, based on the proposed definition of beneficial owner, would not be practical. At this point, FinCEN is choosing not to impose this requirement. “

Our emphasis, again, added. Trusts are a matter of astonishing complexity, slipperiness and importance in the world of offshore secrecy. The world of offshore trusts is a multi-headed hydra, and through these vehicles it is possible to achieve levels of secrecy that are at least as strong as the traditional Swiss banking kind.

And there are potentially even more egregious exemptions. Take a look at this corker:

“Financial institutions noted that a requirement to ‘‘look back’’ to obtain beneficial ownership information from existing customers would be a substantial burden. FinCEN proposes that the beneficial ownership requirement will apply only with respect to legal entity customers that open new accounts going forward from the date of implementation. Thus, the definition of ‘‘legal entity customer’’ is limited to legal entities that open a new account after the implementation date.”

Translation: we’ll accept a complete whitewash of everything in the past, because it will be a “burden” on those poor, belaboured financial institutions. And stuff that’s still going on won’t be covered if the account in which it’s happening was opened before then. Oh, and for now there is no “implementation date”, anyway.

Wouldn’t it have been nice if Fincen could at least come up with something strong, then expect it to be watered down at a later stage of law making? But no: they seem to be hobbling themselves from the outset. Is Fincen even trying?

And even then – if Fincen were to close all these loopholes and obtain all this customer information, it doesn’t seem clear that it would be authorised to pass it on to the U.S. Internal Revenue Service (IRS), which would be the body that would be mandated to hand over the necessary information to foreign governments that need it to tax or police their wealthy citizens and criminals.

A Europe-based expert we spoke to went as far as to describe the U.S.’ adherence to the emerging global transparency standards, just based on what this Fincen document says, ‘farting in the wind.’ This document shows that the US is currently unable under its domestic law to reciprocate with information exchange, because its banks are not required to collect the necessary beneficial ownership information.

So much for the requirements for financial institutions in the U.S. to fish the information out of its customers, ready for exchange with their home governments. Now look at how the (non-)information they do obtain is to be shared out with the U.S.’ foreign partners. Article 6 from one of the U.S. Model IGAs (Intergovernmental Agreements) says:

“Reciprocity. The Government of the United States acknowledges the need to achieve equivalent levels of reciprocal automatic information exchange with [FATCA Partner].”

The U.S. government acknowledges the need to be reciprocal. That’s nice. But will it be reciprocal?

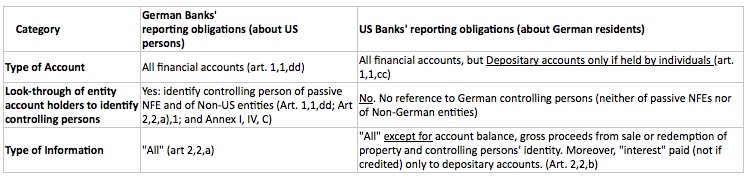

Turn to Article 2, and you get a picture of what the U.S. may obtain from other countries, versus what other countries may obtain from the U.S. Here’s a summary of some of the differences, from Andres Knobel of the Tax Justice Network. Take Germany, for instance: look at how thin the US banks’ reporting obligations are about Germans, compared to German banks’ reporting obligations about US persons.

You get the picture. A comparison with more details is available here.

Reciprocity, anyone?

Oh, and then there is the problem that only some countries, but not others, have signed or committed to sign these IGAs.

After that, there’s the problem that the U.S. legislation required to tackle this stuff is all over the place, in different legislative nooks and crannies. Jack Blum gave a good overview of an earlier version of this mess to the U.S. Senate Finance Committee in 2008, and he added this detail, in an email to me last week:

“after the current round of IRS budget cuts there is no way the United States could implement Information Exchange. Without the people nothing the law says really matters.

Things here are in a real mess.”

Loophole USA: the big one. Will the OECD and its member states – not to mention developing countries – wake up to these issues? And will the United States itself realise that if it doesn’t play ball, others won’t want to play either?

If not, the world’s wealth will flood more upwards and out of sight rather more rapidly than it would have done. That’ll be quite a legacy for President Obama.

Nice teaser! I read the book a month or so ago. It was one of the best explainations of the financial crapification of the global economy I have found.

Thanks MartyH. I agree wholeheartedly: but then I would, wouldn’t I . . .

Nicholas,

If you are London-based (checking now), would be great if you could join with Prof. Yanis Varoufakis, Prof. Steve Keen, Prof. David Graeber and others at the Gibson Hall on 12th February – we are pushing Sir and making headwinds, and your book and views are testament to these efforts.

Thanks for the invite – unfortunately I currently live in Berlin so won’t be able to make it. But it sounds like a very good event.

Shocking isn’t it? Another Obama policy directly contradicts his rhetoric: FATCA is inverted and perverted into a giant FATCAT loophole. For the only people that matter to him, this is not going to tarnish his legacy at all; it’s going to burnish it, seriously.

Nordics use foundations instead of trusts…same game, different lawyers…germans love to act as though information is out there…nonsense…verbal gymnastics make a huge difference…natural person verses legal person is one game…meaning, the world bank (and the interests they protect) argues in its own fine print that if a trust is controlled by a legal person (a corporation or other entity) then it is not really something that has to be “disclosed” (people are corporation too ???)…secondly, discussions of trusts are always lost in the pedestrian notion that are passed around with 20 dollar books where individuals are misled to think they can just “set up a trust” and the “trustee” controls the asset…nonsense…the director controls the trust…any properly drafted trust agreement will have someone who is given the “power of direction”…that can be set up as a veto over actions and requests of the beneficiaries or can be a full out control of the assets or “corpus” of the trust…disclosure is for the little people…but only pedantic fools take their money “out of America” when the rest of the world is trying to get its money into America…

Kowtowing to the elite is a feature of the Obama Administration – NOT a bug. Further, the dude is a fantastic marketer – and like all marketers, we would be wise not to listen to him and instead watch what he does. There is a common theme.

I am reading Nomi Prinz’s All the Presidents’ Bankers … kowtowing to the rich (especially the bankers) has been a national tradition for many, many years. It is a truly bi-partisan arrangement.

Irony of ironies…I happen to know some very wealthy people in Chicago who were leery of Obama (because they lived in Chicago), and their wealth has multiplied fantabulously since his election! They just didn’t realize how corrupt he would be ON THEIR SIDE. Now they assure me that Hillary will be the next president.

If the 99% only had someone to vote for…well they do, but they aren’t allowed to know it, so they won’t.

Jill Stein was the best candidate in 2012 and she will be in 2016, too. But only a very small, elite, intellectually rich but financially impoverished community will be allowed to know. And only a tiny percentage of that group will actually stand up for their convictions and vote for her.

F***ed, aren’t we?

I had totally forgotten about this author and how much I wanted to read their book. Thanks for discussing it.

Remember when, about 5 years ago, the USG went full throttle, with great fanfare, against Swiss banks and an insider whistle blower received something like $150 million for ratting out US citizens? Problem solved? No, not by any measure. For those US citizens of influence, such as the 535, SCOTUS, and others, the preferred tax haven has always been the Caribbean. The insider’s insider law firm, DC based Sullivan and Cromwell, has set up 1000’s of supposed tax compliant trusts for the political class to hide the bribes, payoffs, and outright theft. Yet no concerted effort to go after anything in the Caribbean. Hmmm

The only way to “go after” anything is with the military. Instead of piddling around with loophole-ridden rso-called eforms, the real solution is to seize, freeze and squeeze these offshore Caribbean tax havens. (after we reclaim our country, that is).

Failure to reciprocate by the US isn’t a bug, its a feature. The ability of the the US to shelter all manner of foreign cash is both a means to accumulate liquid wealth as happened with Gold with World Wars I and II, and with 1% foreigners today.

Equally the sold-out state of federal and state government means that there are numerous powerful reasons why both US nationals and foreigners (and dual/triple passport holders) don’t want the US to reciprocate with Europe. After all, what point to beating up Switzerland, Luxembourg, and other traditional tax havens if American banksters don’t benefit?

For that matter – the thousands of corporations in one building in the Cayman Islands is only a different scale than what happens in Nevada or Delaware.

Do as I say, not as I do…

So where are all the radical solutions? Think like a demonic farmer. Cut those weeds off at the root. Poison them with a dose of kleptocide that guarantees eradication. It might be that all of us will be slightly poisoned, but those guys will die an agonizing death. There is always genetic modification – a forced medical procedure for anyone who looks too affluent – which kills the survival instinct. Or there is an easier way. End capitalism as we know it. If profits are eliminated, then hidden wealth is also not a problem. Who needs all that gain in a world that can supply every need? It is a dinosaur.

Not to quibble too much but, how long did the dinosauria hang on for? Wasn’t it a generally accepted ecological catastrophe that ended their reign? In most science, two plus two equals four. In Klepto Finance, two plus two seems to equal infinity.

No where in this article is it mentioned that there are only two countries in the world that tax its citizens on all their income no matter where it’s earned: The United States and Eritrea. You might be someone who has lived and worked in another country all your life. If you are considered a “U.S. Person” by the U.S. government through birth or linage (U.S. parents), you are in effect the property of the U.S government. You must file tax returned an pay U.S. taxes. FATCA is in reality the imposition of U.S. law extra-territorially. Only the U.S. has been able to impose this, but not Eritrea for some reason.