Yves here. It’s now becoming cutting edge conventional wisdom that oversized financial service industries are bad for your economic health. Yet the media is only occasionally and timidly is willing to say that what is good for Jamie Dimon is bad for the rest of us.

I cited the IMF study referenced here in an older post. It’s good to see the OECD reaching similar conclusions.

By Leith van Onselen who has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs. You can follow him on Twitter at twitter.com/leithvo. Originally published at MacroBusiness

More and more studies are coming to the conclusion that having a large financial sector is actually productivity destroying for an economy and slows its growth.

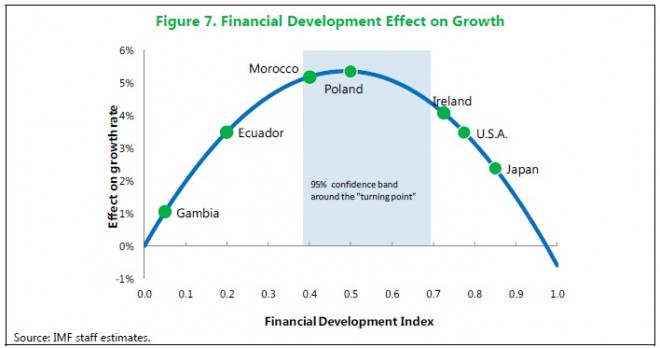

Last month, the International Monetary Fund (IMF) released a report concluding that the larger a country’s financial sector, the bigger its drain on total factor productivity and the greater the risk of economic and financial stability:

…the effect of financial development on economic growth is bell-shaped: it weakens at higher levels of financial development. This weakening effect stems from financial deepening, rather than from greater access or higher efficiency. The empirical evidence also suggests that this weakening effect reflects primarily the impact of financial deepening on total factor productivity growth, rather than on capital accumulation.

When it proceeds too fast, deepening financial institutions can lead to economic and financial instability. It encourages greater risk-taking and high leverage, if poorly regulated and supervised. In other words, when it comes to financial deepening, there are speed limits…

In other words, there is very little or no conflict between promoting financial stability and financial development. Better regulation is what promotes financial stability and development.

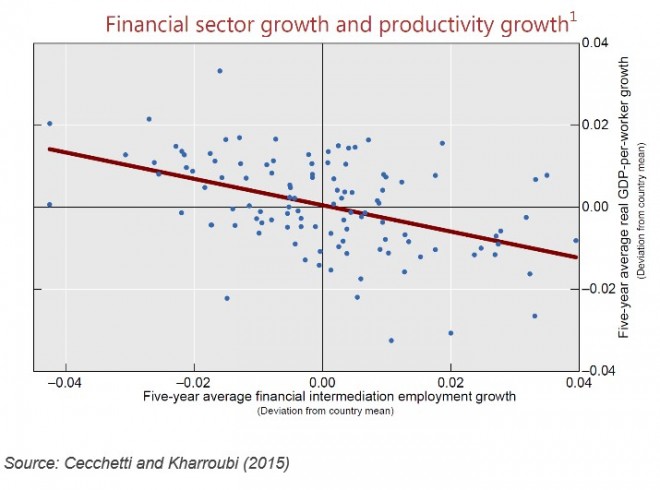

This study was followed by research released earlier this month from economists Stephen Cecchetti and Enisse Kharroubi, who concluded that faster growth in finance is bad for real economic growth. From Business Spectator’sCallam Pickering:

This is readily apparent between 1980 and 2009 — a period in which employment within the financial sector across a range of advanced economies rose at an unprecedented pace. A quick comparison between employment growth in the financial sector and real GDP per worker growth shows a clear downward trend.

The result might surprise some readers. A more developed financial system is supposed to reduce transaction costs, while complicated derivative products were supposed to reduce risk and largely eliminate the business cycle.

But the financial sector competes with other sectors of the economy for resources. It competes for physical capital — such as land and buildings — but also for skilled workers. There is a generation of Americans, Europeans and Australians who have decided to become investment bankers rather than teachers, scientists, or even entrepreneurs.

Yesterday, the OECD entered the fray, releasing a new report arguing that the bloated banking systems in most developed countries are sucking growth out of their economies as well as increasing inequality. The ABC’s Michael Janda has summarised the results:

“The empirical analysis documents a link from financial deregulation, measured by an aggregate indicator, to credit expansion and slower growth,” the report found.

“The data indicate that credit intermediaries may have developed in most OECD countries to a point where further expansion is at the margin associated with slower long-term economic growth and greater economic inequality”.

…when loans exceed around 60 per cent of gross domestic product (a key measure of an economy’s output) then further lending actually dents long-term growth.

“An increase from 100 to 110 per cent of GDP is linked to a 0.25 percentage point reduction in economic growth,” the OECD observed.

Janda notes that the results are bad news for Australia:

According to the latest Reserve Bank data, released earlier this month, Australia’s credit to nominal GDP ratio is above 140 per cent, putting it off the scale of the OECD’s chart…

That implies that the nation loses about a third of a percentage point of economic growth due to its bloated banking sector and excessive debt levels.

There is even worse news for Australia, where it is a surge in lending to households that has driven credit higher…

“The data show that households’ borrowing has a negative marginal link with growth that is twice as large as firms’,” the report noted.

That means Australia could be losing even more economic growth due to the banking system’s overwhelming reliance on home loans…

Financial sector workers have been found to earn a premium over workers in other industries with similar levels of education and experience.

That disparity is also believed to be one of the reasons why a larger financial sector actually inhibits economic growth.

“High wages can draw the most talented workers into the financial sector where they may not contribute as much to economic growth as compared to jobs in sectors with greater potential for productive innovation,” the OECD report hypothesised.

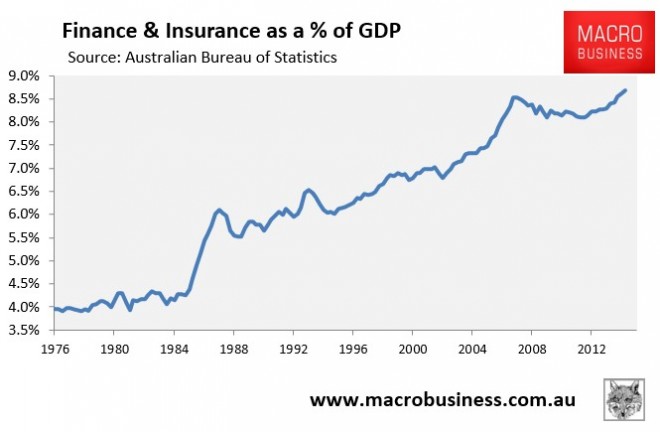

I won’t go over the many reasons why I agree that Australia’s bloated financial system is killing the productive economy, since these were explained in detail in Monday’s post.

All I will say is that Australia’s financial sector has more than doubled its share of the Australian economy since the mid-1980s:

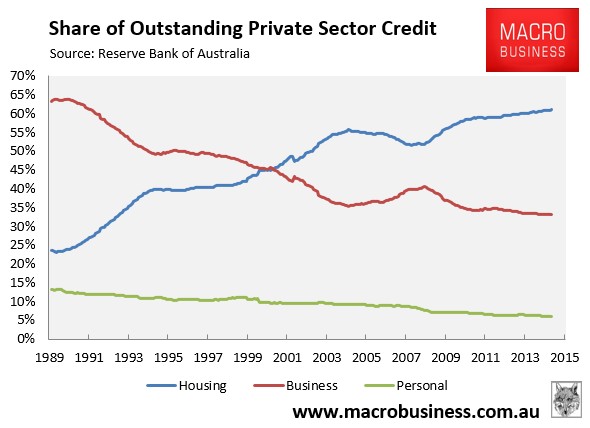

Meanwhile, it has channeled lending away from productive business into unproductive houses (mostly pre-existing):

This is simply called Tainter’s Law of diminishing return of complexity.

Ben

Is it not a sign of rising productivity? The more productive people are the more there is to skim off before people go nuts.

Balduks

Besides Tainter’s Law, You should also read what has to say “Limits to Growth” on this subject

Have a nice day

cnchal

The people working in the financial sector are actually doing us a favor by grabbing most of the money, and “killing” groaf.

With less and less income, the rest of the people working in the non financial sector will not be able to buy all that environment destroying crap, while the planet saving financial sector workers endlessly churn money, and produce nothing.

Larry

I don’t think that reading is correct. Even though American’s wages have stagnated for a generation, our consumption has continued unabated precisely because of the financial sector. Credit cards, auto loans, and mortgages have allowed us to continue consuming no matter what. China itself is a deeply poor nation that has undergone a growth spurt fueled by building and buying with little to no check on the environmental consequences. It seems unlikely to me that the financial sector will do us any favors any time soon, intentional or unintentional.

susan the other

Unwittingly maybe. Financialization didn’t set out to stop groaf. They thought they could use it to jump start the economy. Not. So we have Karma to thank. Because we gotta rethink this whole mess. Fun.

Deep Thought

“complicated derivative products were supposed to reduce risk” – I snorted at this bit. I am yet to see a financial product that truly reduces risk, instead of shifting it somewhere else. What ensures your counter-party is actually going to pay up? Better insure against that too…

Chauncey Gardiner

Unsurprising, and also related to the lack of federal domestic fiscal spending, the ascendancy of the monetarists, and the intentional hollowing out of U.S. manufacturing.

Given the incredible rate of growth of China’s financial sector, wonder where China would now fall in the IMF staff’s estimates for their Financial Development Index chart in the article and potential implications?

washunate

I find the naivete of the groaf crowd so charmingly quaint.

The result might surprise some readers. A more developed financial system is supposed to reduce transaction costs, while complicated derivative products were supposed to reduce risk and largely eliminate the business cycle.

Say what? A more developed financial system and complicated derivatives (ie, consolidation and government bailouts instead of competitive markets) are designed for one, and only one, purpose. They are looting tools to skim the productivity of the economy, furthering the concentration of wealth and power. Trickle down economics. Fascism. Whatever we want to call it.

To assign more noble purposes to theft is to be willfully blind to our entire system of political economy.

MikeNY

But you surely don’t expect our elites to begin calling things by their proper names, do you?! The people are not so far gone as to believe, without some mental discomfort, that fire is cold and night is day. Our elites have been about constructing anodyne and obfuscatory narratives for bad behavior for a long time. Keynes:

Capitalism is the astounding belief that the most wickedest of men will do the most wickedest of things for the greatest good of everyone.

Christer Kamb

In general I agree with the conclusions here but in my view I look at the growth of a financial “industry” as “natural” ending or transmission phases between longer secular trends in the real economy. For example the Industrial Revolution-periods from say 1760-1860(first machines), 1860-1920(mass-production/ communication), 1920-1980(consumer-economy/welfare, 1980-2000(electronics/computer), 2000- . Every phase dramatically increased productivity in the markets. We also note that every era ended with a financial crasch and depressions. 1837-1843: Speculative boom, inflated landprices, wildcat banking led to debt-crises and depression. The goldrush led to speculative inflation-boom and a crash 1857, 1864, 1869 and depression from 1873-79. Several depressions(4) followed until The Great Depression after the Roaring 20´s. Overlending by governments, business/banks seem to by a natural phenomen during big industrial progress. You can´t restrict optimism and business-cycles, can you! BUT:

To prevent depressions the Federal Reserve System was created 1911(elastic money). But most important, The Glass-Steagall Act, separating investmentbanks(and trading) from business-lending banks, 1932/33 effectfully prevented speculative crashes/recessions/depressions until the late 80´s. S&L-recession was the dawn of mass consumer-credit made possible by goverment supporting a housing boom with subsidies and a well hidden start to repeal Glass-Steagall Act from 1979 resulting in the formal repeal 1999. We all know what is going on since!

The easiest way of containing the banking-industry from creating severe recessions/depressions are:

1. Stop the big money-contributions to congress etc

2. No more revolving doors to congress and the executive powers

3. Regulatory improvements for lobby-activities

4. Concentrate financial regulatory oversight to one main instituition

5. Reduce private housing-subsidies and reform(the Mac/May´s etc)

Most direct important steps though:

1. A real New Glass-Steagall Act(Dodd-Frank is not even a half-cock)

2. End TBTF for both banking-categories(Sherman Banking Anti-Trust?)

3. Better transparency/disclosure on derivatives(i.e limitation on non-standard-contracts, clearing-functions)

4. End the perception of “Share Holder Value” and the management take-over of corporations.

The latter is about ownership by “ombud”(funds) leading to short-term management incl stock dilution and management enrichment.

Is cheap consumer-credit really a goal per se? I don´t think so. Savings-ratio in the US are very low demanding more and more dollars abroad for financing real domestic investments. No wage´s without investments. Reallocate frontrunned transactional bankmoney into the real economy. By this you also reallocate competence away from banking.

A New Glass-Steagall will do the most important job to reduce the financial service´s sectors share of GDP(back to 4-5%).

Mel

“But the financial sector competes with other sectors of the economy for resources. It competes for physical capital — such as land and buildings — but also for skilled workers. ”

I don’t believe that. The huge ex-factories in the rust belt aren’t full of financial operators — they’re just abandoned waste. The financial industry competes for mind-share. When you can make big profits by working directly on corporate accounts, who needs manufacturing, employment, processes, resources? All those just represent unknown unknowns to the financially adept. They create needless risk. They are superfluous. Some fool who wants to deal with them can go in there and lose money, but we can do better.

Gio Bruno

The financial sector has to do something with their profits; they buy land and buildings and develop LBO’s that do nothing for the general public, but destroy jobs. And given how much easier it is now to “skim the system” and make a profit than develop a valuable good and be successful by making reasonable profit over time, folks who can follow the money into finance.

And then our culture of malevolence recycles itself. The last part of your comment is a paraphrase of the articles position.

MaroonBulldog

They are worse than superfluous. A benign tumor is superfluous. They are malignant tumors. They are toxic.

Eileen Appelbaum

Rent seeking by bloated financial sector makes banksters richer and everyone else poorer.

Profit seeking: Make economic pie bigger and watch everyone’s slice of the pie grow.

Rent seeking: Use financial engineering to make finance’s slice of the economic pie get bigger at the expense of other economic actors.

reason

I think there is a simpler explanation – ownership.

Bank lends to A to buy property B (B owns property completely). A can provide 50% down. Prices rise because of increase in total money invested, and ownership of property now moves 50% to the bank. A goes bankrupt – property goes completely to Bank.

Interest rates on rents are rent, so rent moves to bank.

More and more of rents flow to bank, but total return on investment in the economy falls, so there is less incentive to invest.

john c. halasz

Where does the 60% of GDP debt load figure come from? It seems to be a fallacy insofar as it is applied to all economies, large or small, rich or poor, across the board. In the U.S. the total debt load exceeded 360%. It seems what is missing is the international dimension of financialized imperialism.

Ben

I totally agree with the thrust of this article but take issue with the casual use of the term “growth”. It’s used here to mean GDP growth in real terms. I’d dispute the value of this metric – it hides that the situation is even worse. What looks like growth is simply debt. We have no way of knowing if we simply had inflation due to printing via lending against land or true wealth creation.

We really need to get away from the banker terminology.

MaroonBulldog

If a so-called “financial service” (a) produces no social benefit, and (b) comes at a social cost, then it should be no surprise that (c) the more we get of it, the worse do.

This is simply called Tainter’s Law of diminishing return of complexity.

Is it not a sign of rising productivity? The more productive people are the more there is to skim off before people go nuts.

Besides Tainter’s Law, You should also read what has to say “Limits to Growth” on this subject

Have a nice day

The people working in the financial sector are actually doing us a favor by grabbing most of the money, and “killing” groaf.

With less and less income, the rest of the people working in the non financial sector will not be able to buy all that environment destroying crap, while the planet saving financial sector workers endlessly churn money, and produce nothing.

I don’t think that reading is correct. Even though American’s wages have stagnated for a generation, our consumption has continued unabated precisely because of the financial sector. Credit cards, auto loans, and mortgages have allowed us to continue consuming no matter what. China itself is a deeply poor nation that has undergone a growth spurt fueled by building and buying with little to no check on the environmental consequences. It seems unlikely to me that the financial sector will do us any favors any time soon, intentional or unintentional.

Unwittingly maybe. Financialization didn’t set out to stop groaf. They thought they could use it to jump start the economy. Not. So we have Karma to thank. Because we gotta rethink this whole mess. Fun.

“complicated derivative products were supposed to reduce risk” – I snorted at this bit. I am yet to see a financial product that truly reduces risk, instead of shifting it somewhere else. What ensures your counter-party is actually going to pay up? Better insure against that too…

Unsurprising, and also related to the lack of federal domestic fiscal spending, the ascendancy of the monetarists, and the intentional hollowing out of U.S. manufacturing.

Given the incredible rate of growth of China’s financial sector, wonder where China would now fall in the IMF staff’s estimates for their Financial Development Index chart in the article and potential implications?

I find the naivete of the groaf crowd so charmingly quaint.

Say what? A more developed financial system and complicated derivatives (ie, consolidation and government bailouts instead of competitive markets) are designed for one, and only one, purpose. They are looting tools to skim the productivity of the economy, furthering the concentration of wealth and power. Trickle down economics. Fascism. Whatever we want to call it.

To assign more noble purposes to theft is to be willfully blind to our entire system of political economy.

But you surely don’t expect our elites to begin calling things by their proper names, do you?! The people are not so far gone as to believe, without some mental discomfort, that fire is cold and night is day. Our elites have been about constructing anodyne and obfuscatory narratives for bad behavior for a long time. Keynes:

Capitalism is the astounding belief that the most wickedest of men will do the most wickedest of things for the greatest good of everyone.

In general I agree with the conclusions here but in my view I look at the growth of a financial “industry” as “natural” ending or transmission phases between longer secular trends in the real economy. For example the Industrial Revolution-periods from say 1760-1860(first machines), 1860-1920(mass-production/ communication), 1920-1980(consumer-economy/welfare, 1980-2000(electronics/computer), 2000- . Every phase dramatically increased productivity in the markets. We also note that every era ended with a financial crasch and depressions. 1837-1843: Speculative boom, inflated landprices, wildcat banking led to debt-crises and depression. The goldrush led to speculative inflation-boom and a crash 1857, 1864, 1869 and depression from 1873-79. Several depressions(4) followed until The Great Depression after the Roaring 20´s. Overlending by governments, business/banks seem to by a natural phenomen during big industrial progress. You can´t restrict optimism and business-cycles, can you! BUT:

To prevent depressions the Federal Reserve System was created 1911(elastic money). But most important, The Glass-Steagall Act, separating investmentbanks(and trading) from business-lending banks, 1932/33 effectfully prevented speculative crashes/recessions/depressions until the late 80´s. S&L-recession was the dawn of mass consumer-credit made possible by goverment supporting a housing boom with subsidies and a well hidden start to repeal Glass-Steagall Act from 1979 resulting in the formal repeal 1999. We all know what is going on since!

The easiest way of containing the banking-industry from creating severe recessions/depressions are:

1. Stop the big money-contributions to congress etc

2. No more revolving doors to congress and the executive powers

3. Regulatory improvements for lobby-activities

4. Concentrate financial regulatory oversight to one main instituition

5. Reduce private housing-subsidies and reform(the Mac/May´s etc)

Most direct important steps though:

1. A real New Glass-Steagall Act(Dodd-Frank is not even a half-cock)

2. End TBTF for both banking-categories(Sherman Banking Anti-Trust?)

3. Better transparency/disclosure on derivatives(i.e limitation on non-standard-contracts, clearing-functions)

4. End the perception of “Share Holder Value” and the management take-over of corporations.

The latter is about ownership by “ombud”(funds) leading to short-term management incl stock dilution and management enrichment.

Is cheap consumer-credit really a goal per se? I don´t think so. Savings-ratio in the US are very low demanding more and more dollars abroad for financing real domestic investments. No wage´s without investments. Reallocate frontrunned transactional bankmoney into the real economy. By this you also reallocate competence away from banking.

A New Glass-Steagall will do the most important job to reduce the financial service´s sectors share of GDP(back to 4-5%).

“But the financial sector competes with other sectors of the economy for resources. It competes for physical capital — such as land and buildings — but also for skilled workers. ”

I don’t believe that. The huge ex-factories in the rust belt aren’t full of financial operators — they’re just abandoned waste. The financial industry competes for mind-share. When you can make big profits by working directly on corporate accounts, who needs manufacturing, employment, processes, resources? All those just represent unknown unknowns to the financially adept. They create needless risk. They are superfluous. Some fool who wants to deal with them can go in there and lose money, but we can do better.

The financial sector has to do something with their profits; they buy land and buildings and develop LBO’s that do nothing for the general public, but destroy jobs. And given how much easier it is now to “skim the system” and make a profit than develop a valuable good and be successful by making reasonable profit over time, folks who can follow the money into finance.

And then our culture of malevolence recycles itself. The last part of your comment is a paraphrase of the articles position.

They are worse than superfluous. A benign tumor is superfluous. They are malignant tumors. They are toxic.

Rent seeking by bloated financial sector makes banksters richer and everyone else poorer.

Profit seeking: Make economic pie bigger and watch everyone’s slice of the pie grow.

Rent seeking: Use financial engineering to make finance’s slice of the economic pie get bigger at the expense of other economic actors.

I think there is a simpler explanation – ownership.

Bank lends to A to buy property B (B owns property completely). A can provide 50% down. Prices rise because of increase in total money invested, and ownership of property now moves 50% to the bank. A goes bankrupt – property goes completely to Bank.

Interest rates on rents are rent, so rent moves to bank.

More and more of rents flow to bank, but total return on investment in the economy falls, so there is less incentive to invest.

Where does the 60% of GDP debt load figure come from? It seems to be a fallacy insofar as it is applied to all economies, large or small, rich or poor, across the board. In the U.S. the total debt load exceeded 360%. It seems what is missing is the international dimension of financialized imperialism.

I totally agree with the thrust of this article but take issue with the casual use of the term “growth”. It’s used here to mean GDP growth in real terms. I’d dispute the value of this metric – it hides that the situation is even worse. What looks like growth is simply debt. We have no way of knowing if we simply had inflation due to printing via lending against land or true wealth creation.

We really need to get away from the banker terminology.

If a so-called “financial service” (a) produces no social benefit, and (b) comes at a social cost, then it should be no surprise that (c) the more we get of it, the worse do.