Yves here. This paper has an important finding: that the usual measures of board independence are inadequate. Regulators and investors need to look at a broader range of connections and perceived obligations between CEOs and directors.

By Jens Hagendorff,Professor of Finance and Investment, Cardiff Business School and Arman Eshraghi, Senior Lecturer in Finance and Director of MSc Finance and Investment, University of Edinburgh. Originally published at VoxEU

Banks are regularly under scrutiny for their professional and ethical behaviour. This column assesses the role of boards in monitoring and advising conduct, and offers new insights for how to structure bank boards to prevent misconduct. Conventional board measures such as board independence and financial expertise have no measurable impact on misconduct being committed or detected. Instead, governance metrics revolving around CEO connections warrant more attention from regulators, investors, and governance activists.

The reputation of banks in terms of professional and ethical conduct continues to be in sharp decline. In recent years, regulators have targeted banks with record numbers of enforcement actions, requiring them to take corrective measures against financial misconduct. Among the banks engulfed in misconduct cases are various high-profile institutions. Wells Fargo is currently in the news regarding a large case of misconduct, with many commentators viewing poor board governance as the main reason behind the Wells Fargo debacle (Financial Times 2016). Likewise, JP Morgan has faced several enforcement actions related to credit card fraud, money laundering and internal accounting controls over the past few years.

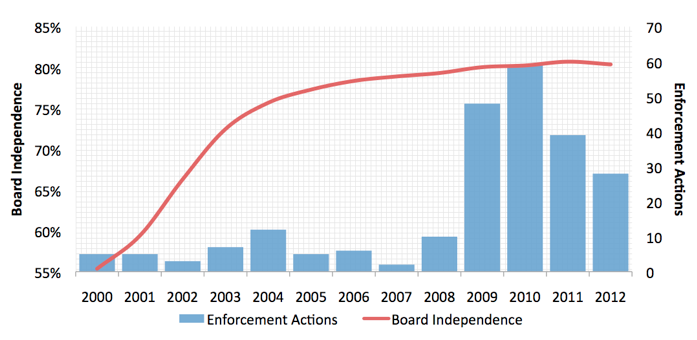

On one level, it is surprising to see the recent surge in cases of bank misconduct. One explanation holds that when a CEO has too much authority within the firm, misconduct is but one potential outcome (Khanna et al. 2015). However, by most accounts, oversight of CEO decision-making has improved markedly in recent years. Data from Riskmetrics show that eight out of ten US bank board members are classified as independent in 2012, up from around half in 2000 (see Figure 1). With increasing levels of independence, one would expect bank boards to be more effective in preventing misconduct. However, far from a declining trend, the number of enforcement actions has increased from 5 to 28 over the same time period.

Figure 1. The percentage of directors classified as independent on US banks, and the number of enforcement actions received by US banks

Source: Riskmetrics and Nguyen et al. (2015)

The rise in cases of bank misconduct under increasingly more independent boards is consistent with the view that true board independence is difficult to achieve. Board independence can be undermined if CEOs exert intangible influence over those charged with monitoring them. One way in which a CEO could wield soft power is by ‘capturing’ the board through director appointments (Khanna et al. 2015). Since the CEO is typically involved in the process of recommending directors to the board, directors appointed during the tenure of the current CEO have an incentive to return the favour (Coles et al. 2014, Khanna et al. 2015). Even independent directors may reciprocate the CEO’s requests and side with the CEO to support, engage in, or conceal wrongdoing.

Thus, only directors appointed before the current CEO’s tenure are free from this type of intangible influence, and are therefore capable of objectively monitoring the CEO. In the case of Wells Fargo, around half of all current members of the board have been appointed under the bank’s current CEO. This ratio is not unusual for US banks, but it raises questions over how independent, assertive, and effective Wells Fargo’s and the boards of other US banks really are.

In a recently published study, we employ a unique dataset of regulatory enforcement actions issued by the three US supervisory bodies – the Federal Reserve Board (FRB), the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC) – against banks that engage in unsafe, unsound and illegal banking practices (Nguyen et al. 2016). Generally, one can only observe detected misconduct (once an enforcement action has been issued), but not the set of all committed cases of misconduct. That is, even in the absence of enforcement actions, a bank may still be engaged in undetected misconduct. To address this problem of partial observability, we follow Wang (2013) and Wang et al. (2010) in employing a bivariate probit model that disentangles committing misconduct from the detection of misconduct, conditional upon misconduct having occurred.

We find that a bank in which monitoring quality is high (i.e. all directors have been appointed before the CEO takes office) has a 27% lower probability of committing misconduct and a 35% higher probability of detection (conditional upon misconduct having occurred) compared to a bank where all directors have been appointed under the current CEO. Further, in all specifications, we control for the proportion of independent directors and the number of directors with financial expertise. We find that these traditional measures of board monitoring and advising have little or no power to prevent misconduct in the banking sector.

Interestingly, we also show that CEO bonus and CEO option payments are positively related to the probability that misconduct is committed. This is consistent with the argument that some CEOs commit wrongdoing in order to boost stock prices and enjoy higher pay-outs.

How do board monitoring and advising prevent bank misconduct? We examine two channels that help explain the results. First, many enforcement actions are issued when bank fundamentals indicate increased bank risk. Our results show that better monitoring prevents enforcement actions because these boards are associated with higher bank capital cushions, lower portfolio risk, and fewer non-performing loans. Second, CEOs will be deterred from committing wrongdoing if they know ex ante that a board will penalise them for instances of misconduct. We find that boards not captured by the CEO are more willing to impose heavier penalties on them following detected misconduct. That is, after misconduct is detected, better monitoring quality is associated with a larger reduction in (i) the level of CEO pay, (ii) the level of CEO pay relative to the other top executives at the same bank, and (iii) the value of CEO risk-taking incentives.

Our study offers novel insights for how to structure bank boards to prevent misconduct. These include important lessons for the ongoing case at Wells Fargo and other banks. We show that conventional board measures such as board independence and financial expertise have no measurable impact on misconduct being committed or detected. By contrast, the board metrics we study related to monitoring and advising are important predictors of misconduct. Overall, our study illustrates the importance of board governance in banking. Our findings demonstrate that governance metrics revolving around CEO connections warrant more attention from regulators, investors, and governance activists.

See original post for references

Good corporate governance practices in the financial sector today is certainly an oxymoron as attested to in the recent Stumpf/Wells Fargo hearings.

It was Stumpf and the Board who crafted the departure scenario Carrie Tolsted that included millions upon exiting with no mention of wrongdoing. In one week’s time between the senate and house hearings it became apparent to the Board that Tolsted’s exit scenario was woefully inadequate. All this points to a Board who is out of touch with reality on top of their failure to this point to monitor mischievous conduct of management that encouraged and permitted the fraud for years on end.The Board should resign.

Shareholders have a major role in all this especially as to their willful blindness to both managements and the boards activities. Could it be that shareholders turn a blind eye to fraudulent conduct as a result of the dividends therein? Perhaps this is slouching into Gomorrah.

First, I doubt the board had anything to do with the negotiation of Toldstedt’s departure. Wells did have a reason for regarding the fine as a nothingburger. $185 million and a mere maximum of $5 million in consumer relief is chicken feed for a bank as big as Wells. In fact, it’s more likely that she had a better sense of the downside and decided to resign to collect her cash and prizes in case things got ugly.

Second, boards never resign.

Until we rid ourselves of the idea of “limited liability”, I think the best preemptive policy for corporate “misconduct” is to put the CEO and all board members in jail after “misconduct” is proved: nothing like the threat of a night in jail to motivate “right” conduct of current and future CEOs and board members.

Forget boards, the headline should read “When bank executives are immune from prosecution, expect misconduct”.

This stuff is not that difficult to figure out.

Completely agree John. The two tricks that screw the game are the two political concessions that mindless representatives sold to the men of commerce – limited liability and the thing about a company being a person.

Both these indulgences need to be repealed.

Unlike other large companies, until the 1970s large bank stocks traded almost exclusively over the counter instead of on the Big Board (NYSE). Citibank was one of the pioneers to switch from OTC to NYSE listing in 1968.

One market historian claims that for decades, the NYSE resisted listing banks because they were viewed as too sleazy. That is, banks would lower the moral tone of an otherwise exemplary stock exchange. Banks were put in the same reject category as miners (“liars with holes in the ground”), who also were obliged to trade OTC.

In Texas in them days, deep-set popular contempt for banks was expressed by members of Congress such as Wright Patman, who spent an incredible 47 years in the House (1929-1976) cracking bankster skulls. Prohibitions on branch banking and interstate banking were rigidly enforced in Texas until an oil bust obliged acceptance of out-of-state bailouts.

Cleaning out the Augean stables of bank boards ain’t enough. Banksters need to be registered like prostitutes, and kept off the streets during daylight hours when respectable folks are about.

Give banks a license to steal and they steal – no surprise there.

And the license? ans: Largely virtual liabilities wrt to the general population via extensive government privileges such as deposit insurance and exclusive access to accounts in fiat – when fiat is supposed to be for all citizens to use, not just depository institutions, aka banks.

The problem? The current system is deeply corrupting since those privileges for banks allow each of us to steal from our neighbor – according to our own so-called creditworthiness with the poor being at the bottom of the heap, looted by their supposed betters.

The solution? Reform and restitution.

Maybe it’s not too late.

The entire underlying value system needs to be ditched and replaced. Even a “well-run” capitalist (i.e. extractive) financial institution would still be a bad deal. Euthanize them all and replace them with publicly accountable utilities. You don’t try to figure out how to make a tumor less damaging, you remove the f***ker! Just sayin’…

Euthanize them all and replace them with publicly accountable utilities. diptherio

Except what shall be the basis for so-called creditworthiness? Wealth as is now the case? Political connections? Political correctness, whatever that is at the moment?

Government should stay out of the lending business. Otoh, grants are perfectly acceptable and perpetual deficit spending an actual moral requirement* of the monetary sovereign, be the deficits ever so small at times to control price inflation.

*So the old don’t loot the young via deflation.

The “Board of DIrectors” model of corporate governance is basically a joke in this country and will continue to be so long as CEOs get to name the board members. What we’ve seen time and again is boards stacked with CEOs of other bompanies, who then engage in a mutual back-scratching that makes a mockery of boards as representatives of the shareholders. THis has been particularly evident wrt the explosion of CEO compensation since the ill-considered Clinton tax reform of 1993 made salary undeductible over a $1 million but left stock options and other “performance” related bonuses tax deductible.

The other category of directors is even more laughable: celebrity or other directors who have little to no experience in business. Two immediate examples: Hillary Clinton, as a 30-something lawyer with a (commendable) focus on children and family law issues (or so she says now), was appointed to the board of Tyson Chicken, the largest employer in Arkansas, and Walmart (IIRC); and Laura Deandrea Tyson (no relation to the chicken family AFAIK) who was on the board of Lehman Brothers while also serving as a professor of economics at UC Berkeley. Both smart people but with zero qualifications to serve as outside directors with a putative duty to check the CEOs when they want to do loony things.

I don’t have a solution but I know the first step is to acknowledge that there’s a problem.

Just fyi, Tyson was on the Morgan Stanley board, not Lehman’s.

“Interestingly, we also show that CEO bonus and CEO option payments are positively related to the probability that misconduct is committed. This is consistent with the argument that some CEOs commit wrongdoing in order to boost stock prices and enjoy higher pay-outs.”

It sounds almost like this was a revelation to the authors. What other reason is there for the CEO’s to commit fraud? Bill Black made this point and had the evidence back during the S&L debacle of the ’80’s. It never ceases to amaze me that these academics never seem to get out of their ivory towers and see what is happening on the ground.

And, naturally, since this is an academic study, they won’t use the word fraud, it’s “misconduct”.

Hear, hear!

Sometimes you must fight fire with fire. For those people, who are not most casual observers and are oblivious, you need numbers and ‘studies’ to convince them. This is the kind of stuff for them. For the rest of us folks, it’s ‘Er duh!’. Besides which, even academicians need work.