Yves here. This IEA report is more significant that it might seem at first blush, since the IEA has a bullish bias.

By Nick Cunningham, a freelance writer on oil and gas, renewable energy, climate change, energy policy and geopolitics, based in Pittsburgh, PA. Follow him on Twitter @nickcunningham1. Originally published at OilPrice

For the second month in a row, the IEA has poured cold water onto the oil market, publishing an analysis that suggests 2018 could hold some bearish surprises for crude.

The IEA’s December Oil Market Report dramatically revises up the expected growth of U.S. shale, which goes a long way to torpedoing the excitement around the OPEC extension.

Late last month, when OPEC agreed to extend its production cuts through the end of 2018, the U.S. EIA came out with data – on the same day as the OPEC announcement – that showed an explosive increase in shale output for the month of September, up 290,000 bpd from the month before.

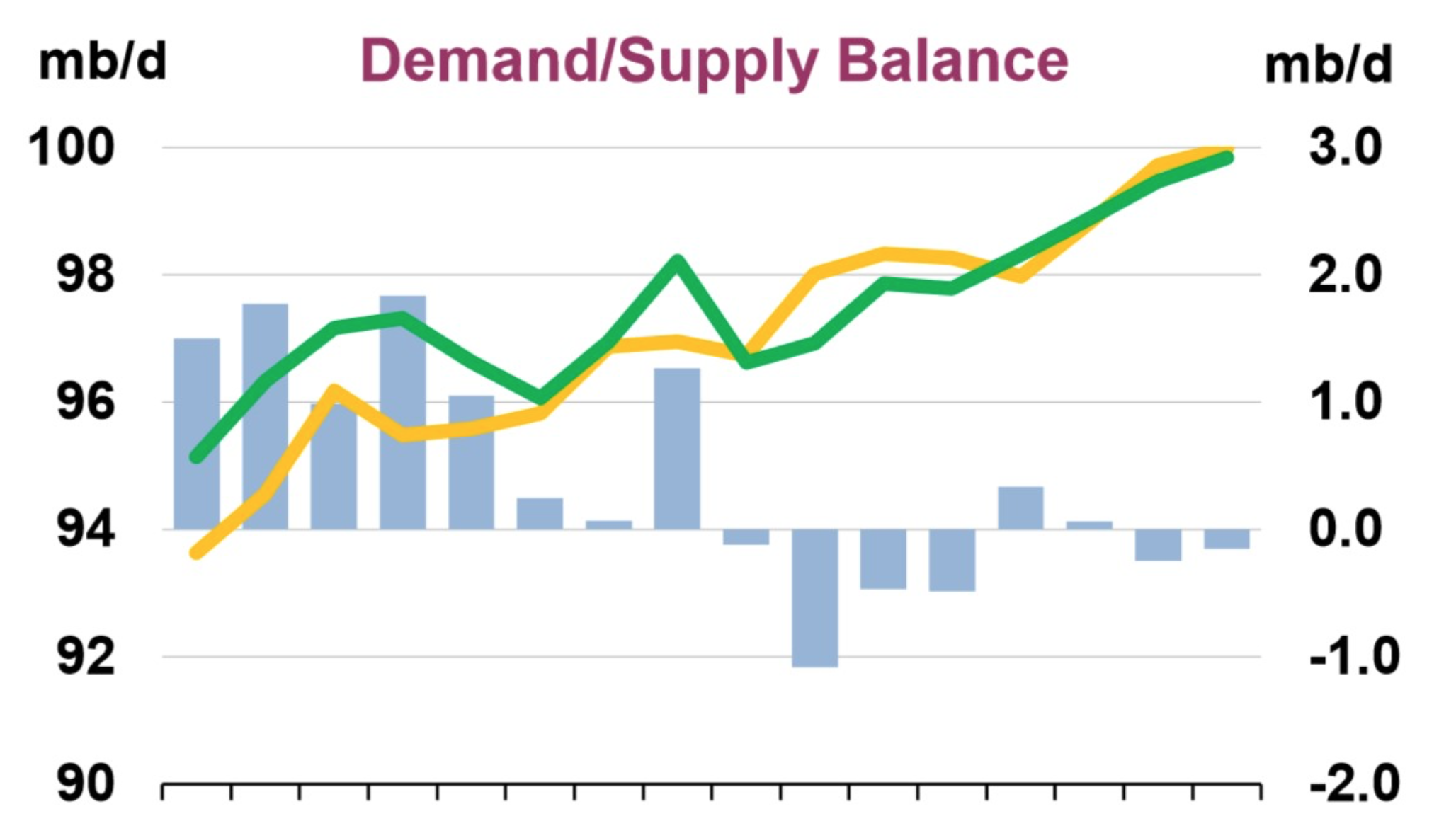

Although there is a time lag on publishing production data, the huge jump in output in September, plus the spike in rig count activity over the past few weeks, points to strength in the U.S. shale sector. Against that backdrop, the IEA predicted that non-OPEC supply would grow by 1.6 million barrels per day (mb/d) in 2018, a rather significant upward revision of 0.2 mb/d compared to last month’s report.

Adding insult to injury for OPEC, the IEA sees oil demand growing by just 1.3 mb/d. In other words, supply will grow at a faster pace than demand next year, opening up a global surplus once again. “So, on our current outlook 2018 may not necessarily be a happy New Year for those who would like to see a tighter market,” the IEA said. The surplus will be front-loaded – the first half of the year will see a glut of about 200,000 bpd.

“A lot could change in the next few months but it looks as if the producers’ hopes for a happy New Year with de-stocking continuing into 2018 at the same 500 kb/d pace we have seen in 2017 may not be fulfilled,” the agency wrote. In the past few months, a sense of bullishness and optimism returned to the oil market for the first time in years, but the IEA warned that it won’t last.

The news wasn’t all bad for oil bulls. OPEC production fell by 130,000 bpd in November, due to lower output in Saudi Arabia, a rather large decline in Angola, and the continued erosion of output from Venezuela. It is the fourth consecutive month of falling output from OPEC, and the compliance rate for the cartel jumped to 115 percent in November, the highest rate so far this year. That bodes well for the extension of the deal – OPEC and its partners seem resolved to keep compliance high heading into 2018.

Inventories also continue to decline. The IEA said that OECD commercial stocks fell by 40.3 million barrels in October to 2,940 mb, the lowest level since July 2015. That decline was almost twice as large as usual for this time of year. And for crude inventories specifically, they fell counter-seasonally by 19.7 mb, including the first decline in China this year.

But even there, the IEA was quick to point out reasons to be bearish, noting that the inventory drawdowns will soon end. “Going into 1Q18, our balances imply that global oil stocks will increase by 300 kb/d, assuming stable OPEC crude production of 32.5 mb/d,” the IEA said in its report.

Those increases in inventories in 2018 largely come down to U.S. shale, which continues to grow at an impressive rate. Rystad Energy says that almost 1,000 horizontal wells were completed in October, the highest total since March 2015. That should ensure a rush of fresh supply will be added onto the market by the end of this year and into 2018.

Overall, the downbeat conclusions from the IEA report were largely backed up by OPEC itself a day earlier. The cartel published data that also anticipated large increases in U.S. shale output, including an upward revision for 2017 output by 150,000 bpd – an acknowledgement that shale drillers are adding supply at a faster rate than expected. More ominously, OPEC predicts that the U.S. will add more than 1 mb/d of new supply in 2018 – a truly staggering figure.

Putting it all together, OPEC is essentially keeping 1.2 mb/d off of the market in 2018 so that the U.S. can add 1 mb/d. It’s a quite a gamble; a bet that by doing so, the group can prevent oil prices from falling. But the payoff is debatable. OPEC is selling less oil and allowing the U.S. to sell more.

The bet is that next year inventories will fall and oil prices will gradually rise, but the IEA’s report predicts that such a scenario may not play out.

‘The surplus will be front-loaded – the first half of the year will see a glut of about 200,000 bpd.‘

That don’t square at all with WTI futures being backwardated from Feb 2018 ($57.08) to Dec 2022 ($49.79).

Me so bullish …

By continuing its’ easy money policies well past any recession or growth scare, the Fed has created a monster. Most shale companies aren’t profitable and are in fact losing money using any kind of GAAP. However, cheap financing allows them to survive and “drill baby drill.”

The unintended consequences may include destabilizing Saudi Arabia to the point of an economic and political collapse. One can always hope …

Economic collapse in Venezuela due to low oil prices – good!

Economic collapse in Saudi Arabia due to low oil prices – bad!

Solution – extend cheap financing to Saudi Arabia via Aramco IPO!

Meanwhile, China says it will be moving to all-electric cars and trucks to help solve its horrible urban air pollution problem. . . Meaning global demand has nowhere to go but down.

Why do I feel that this will not end well for the American hegemon? Particularly with Trump in office working overtime with boy genius Rick Perry to promote coal and sabotage renewable energy. . .

The 36″ North Sea Forties pipeline is currently shut down for repairs. Short and medium term prices will carry the effect of that supply loss. In the long term, unexpected developments are common. Considering how completely wrong so many oil analysts have been over the past ten years, including the IEA, there is not a lot of credibility in oil market predictions.

“OPEC production fell by 130,000 bpd in November, due to lower output in Saudi Arabia,”

There’s no industry capability to put this figure as a fact. They still have people looking at tankers with binoculars figuring out how much the Sauds are putting out. Even better the WSJ printed in a story last week that the Sauds were putting out oil at $2.25 a barrel!

Anyway, all oil numbers should be taken with a grain of salt, always. Shale is meeting with increasing geological limits, going to cost even more to produce, this in an industry that’s never made a profit, even at $100 and is some $280 billion in debt, which I guess its good debt doesn’t mean anything.

And the band played on

https://www.bloomberg.com/news/articles/2017-12-14/u-s-oil-cocktails-spoil-chemistry-in-budding-asian-love-affair

this is good piece on Asia refiners having trouble with US shale as US refiners have previously.

Condensate is not the oil, “black gold, Texas tea” of old and fact is that type of oil basically peaked a decade ago in low 70s mbd. Shale fields have always produced a lot of condensate and are now producing more and increasing amounts of just gas.

Anyway “oil glut” has always been at best a nebulous term for many reasons, but then we here in the US just think, as Mr. Obama proudly stated in his last State of the Union, “$2 a gallon gas ain’t bad either.”

[“OPEC is selling less oil and allowing the U.S. to sell more.”]

Or … allowing the U.S. to slow down the depletion of the most “valuable” legacy wells…

It’s a matter of perspective.

My impression is that this a gap (could be intentional) between IEA statistics and predictions and the reality. This is propaganda agency after all, with the explicit agenda of keeping the oil price for Us consumers low. So typically that produce too “rosy” forecasts that later are quietly corrected. Their short-term forecasts are based on oil futures and as such has nothing to do with the reality on the ground. Which is quite disturbing.

It is undeniable that shale boom which played such a beneficial role for the USA allowing to squeeze oil price (with generous help from KSA) for two and half years is dead.

Now is kept artificially alive by junk bonds and directs loans that will never be repaid. In other words, the USA now enjoys a period of “subprime oil. Unless there is a new technological breakthrough there will be an only minor improvement in efficiency of drilling and oil extraction in the next couple of years, but the lion share of those was already implemented, and on the current technological level we are close to the “peak efficiency” in drilling and services.

Those minor efficiencies will be negated by rising prices of service industries, which can’t take the current pricing any longer and need to raise prices for their services.

Old “classic” land-based oil fields deteriorate to the tune of 5% per year, while deep sea deteriorate more and subprime wells much more. You can probably double the figure for each, although much depends on particular geology. Infill drilling accelerates depletion, allowing to maintain high production for sometimes so changes can be abrupt.

In any case each year you need somehow to find 5 MB/d of oil, finance new wells in those areas and infrastructure required. All Us shale production is around 6 MD/day. So you get the idea.

Moreover, with each year, “subprime wells” (multi-stage shale well) costs more and now are at a range of n 6-10 million depending on the number and the length of horizontals and number of fracking stages and other factors. Only few area (sweet spots) can recover this capital investment during the life of the shale well at current prices). More at around $80 and almost all around $100 per barrel. The later is also the price that KSA needs to remain solvent (rumored to be in low 90th).

The shale oil produced in the USA is really “subprime” because large part of it has lower energy content (by 20% or more) and different mix of various hydrocarbons that “classic” oil. Especially condensate from gas wells. Which optimally can be used only as diluter for heavy oil. EIA does not differentiate between different types oil and use wrong metric (volume instead of weight). May be intentionally.

So the future remains unpredictable but general trend for oil prices might be up with some spikes, not not down. Although many people, including myself, thought so in early 2015 ;-)

Another factor is that world consumption continue to grow and will do so because population in large part of Asia and Africa is still growing and number of cars on the road increase each year requiring on average 1-1.4 MB/d additionally.

So it looks like the situation gradually deteriorate despite all efforts and related technological breakthrough which allow to extract more from the old wells and more efficiently extract shale oil.

The problem is that new large deposits are very hard to find now and several previously oil-exporting countries gradually became oil-importers. Mexico is one, which will be huge hit.

Obama administration screw the opportunity to move US comsumers to hybrid cars so the situation in the USA deteriorates too despite rise of percentage of more economical vicicle in the personal car freet each year. Rumore were that they pursue vendetta against Russi and that wwas primary consideration – to crash Russian economy and install a new “Yeltsin”.

the USA generally is in better position then many other countries as theswitch to natural gas and hybrid electric cars for personal transporation is still possible. It already happened in several European countires for selected types of cars, buses and trucks (taxi, in-city buses and “dayly round trip or short trips trucks).

But there is no money for infrastructure anymore and for example many miles of US rail remain non-electrified. Burning diesel instead.

As maintenance was neglected for two and half year disruption of existing supply might became more frequent. also mid Eastern war is also a possiblity with Tump siberrattling against Iran. Recently the leak in undersea pipeline removed 0.5 MB/d from the market and caused a price spke to $65 for brent (WTI remains cheaper and never crosses $60 this time).

Also with a young prince in charge and the revolution against “old guard” KSA became more and more unstable so the next “oil shock” might come from them. They also have problem of depletion which until now they compensated pitting more and more heavy high sulfur oil deposits online. At some point they will be exhausted too. They also pitch for war with Iran, but they would prefer somebody else todo heavy lifting.

The only one or countries still can significantly increase oil production now — Libya (were we have problem because of the civil war after US-sponsored Kaddafi removal and killing), and Iraq where there are still untapped areas that might contain some oil; nothing big, but still substantial in the range of 1 MB/d. Looks like Iran now exports all it could. Same is true for KSA and Russia. In this sense OPEN oil production cuts might an attempt to preserve impression that they are untapped reserved. I doubt that there are much and those cuts are just a reasonable insurance policy against quick depletion of existing wells as higher price gives some space for innovation.

There is also such thing as EBITRA which gradually deteriorates everywhere and can become negative for certain types of oil (for oil sands it depends on the price of natural gas and they are primary candidate if the price doubles or triples from the current level).