By Raúl Ilargi Meijer, an editor at Automatic Earth. Originally published at Automatic Earth

In the New Year, after a close to the old one that was sort of terrible for our zombie markets, do prepare for a whole lot of stories about China (on top of Brexit and Yellow Vests and many more windmills fighting the Donald). And don’t count on too many positive ones that don’t originate in the country itself. Beijing will especially be full of feel-good tales about a month from now, around Chinese New Year 2019, which is February 5.

And we won’t get an easy and coherent true story, it’ll be bits and pieces stitched together. What will remain is that China did the same we did, just on steroids. It took us 100 years to build our manufacturing capacity, they did it in under 20 (and made ours obsolete). It took us 100 years to borrow enough to get a debt-to-GDP ratio of 300%, they did it in 10.

In the process they also accumulated 10 times more non-productive assets than us, idle factories, bridges to nowhere and empty cities, but they thought that would be alright, that demand would catch up with supply. And if you look at how much unproductive stuff we ourselves have gathered around us, who can blame them for thinking that? Perhaps their biggest mistake has been misreading our actual wealth situation; they didn’t see how poorly off we really are.

Xiang Songzuo, “a relatively obscure economics professor at Renmin University in Beijing”, expressed some dire warnings about the Chinese economy in a December 15 speech. He didn’t get much attention, not even in the West. Not overly surprising, since both Beijing and Wall Street have a vested interest in the continuing China growth story.

But with the arrival of 2019, that attention started slowly seeping through. Former associate professor of business and economics at the Peking University HSBC Business School in Shenzhen, Christopher Balding, left China 6 months ago after losing his job. At the time, he wrote: “China has reached a point where I do not feel safe being a professor and discussing even the economy, business and financial markets..”. And, noting a change that very much seems related to what is coming down the road:

”One of my biggest fears living in China has always been that I would be detained. Though I happily pointed out the absurdity of the rapidly encroaching authoritarianism, a fact which continues to elude so many experts not living in China, I tried to make sure I knew where the line was and did not cross it. There is a profound sense of relief to be leaving safely knowing others, Chinese or foreigners, who have had significantly greater difficulties than myself. There are many cases which resulted in significantly more problems for them. I know I am blessed to make it out.”

A few days ago, Balding wrote this on Twitter:

“Most experts dismissed the speech by Xiang Songzuo (claiming Chinese GDP growth could be as low as 1.67%) as implausible…”. No, we didn’t. The GS PE guy and the PKU dean have every reason to deny it. Car and mobile phone shipment down 2% and 16% are not a 6.5% growth economy.”

That certainly sets the tone of the discussion. GDP growth of 1.67% vs the official 6.5%; smartphone shipments down 16%, car sales slumping. Not the kind of numbers you’ll hear from Beijing. And Balding does know China, whether they like it or not. On Monday, Bloomberg, where he was/is a regular contributor, published this from his hand:

China Has a Dangerous Dollar Debt Addiction

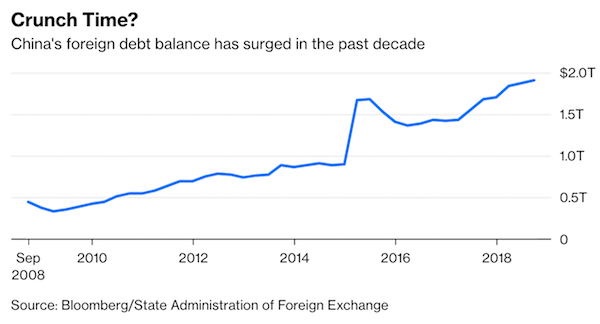

Officially, China lists its outstanding external debt at $1.9 trillion . For a $13 trillion economy, that’s not a major amount. But focusing on the headline number significantly understates the underlying risks. Short-term debt accounted for 62% of the total as of September, according to official data, meaning that $1.2 trillion will have to be rolled over this year .

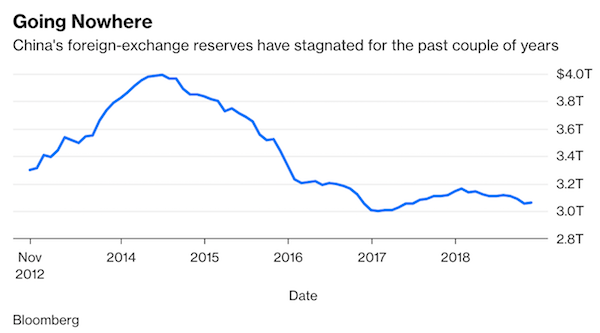

Just as worrying is the speed of increase: Total external debt has increased 14% in the past year and 35% since the beginning of 2017 . External debt is no longer a trivial slice of China’s foreign-exchange reserves, which stood at just over $3 trillion at the end of November, little changed from two years earlier. Short-term foreign debt increased to 39% of reserves in September, from 26% in March 2016.

The true picture may be more precarious. China’s external debt was estimated at between $3 trillion and $3.5 trillion by Daiwa Capital Markets in an August report. In other words, total foreign liabilities could be understated by as much as $1.5 trillion after accounting for borrowing in financial centers such as Hong Kong, New York and the Caribbean islands that isn’t included in the official tally. Circumstances aren’t moving in China’s favor.

The nation’s companies rushed to borrow in dollars when there was a 3% to 5% spread between Chinese and U.S. interest rates and the yuan was expected to strengthen. Borrowing offshore was cheaper and offered the additional bonus of likely currency gains. Now, the spread in official short-term yields has shrunk to near zero and the yuan has been depreciating for most of the past year. Refinancing debt in dollars has become harder, and more risky.

Beijing’s policies have exacerbated the buildup of foreign debt. To promote Xi Jinping’s Belt and Road Initiative, the president’s landmark foreign policy endeavor, China has been borrowing dollars on international markets and lending around the world for everything from Kenyan railways to Pakistani business parks. With this year and 2020 being the peak years for repayments, China faces dollar funding pressure.

To repay their dollar debts, Chinese firms will either have to draw from the central bank’s foreign-exchange reserves (a prospect Beijing is unlikely to allow) or buy dollars on international markets. This creates a new set of problems. There are only 617 billion yuan ($90 billion) of offshore renminbi deposits in Hong Kong available to buy dollars . If China was to push firms to bring debt back onshore, this would necessitate significant outflows that would push down the yuan’s value against the dollar

The Xiang Songzuo speech was also noted by the Financial Times this week. Their conclusions are not much rosier. Recent US imports from China look good only because both buyers and sellers try to stay ahead of tariffs. And whole some truce or another there may smoothen things a little, China must launch a massive stimulus against the background of twice as much investment being needed for a unit of GDP growth.

Nervous Markets: How Vulnerable Is China’s Economy?

A relatively obscure economics professor at Renmin University in Beijing sparked a minor furore last month when he claimed a secret government research group had estimated China’s growth in GDP could be as low as 1.67% in 2018 — far below the officially published rate of 6.7% for the year up to September.

Most experts dismissed the speech by Xiang Songzuo as implausible, despite longstanding doubts about the reliability of China’s official GDP data. Yet although discussion of his claims was quickly scrubbed from the Chinese internet, the presentation has been viewed more than 1.2m times on YouTube — an indication of the raw nerve Mr Xiang touched with his doom-laden warnings.

[..] the question that is hanging over global markets is just how vulnerable is China to a much sharper slowdown? Ominously, the recent downturn has occurred even though the expected hit to Chinese exports from the trade war has not yet materialised. In fact, analysts say exports probably received a one-off boost in recent months as traders front-loaded shipments to beat the expected tariff rise from 10% to 25% that US president Donald Trump threatened would take effect in January. That rise is now on hold due to the 90-day truce that Mr Trump agreed with Chinese president Xi Jinping at the G20 meeting in Argentina last month.

[..] The amount of new capital investment required to generate a given unit of GDP growth has more than doubled since 2007 , according to Moody’s Analytics. In other words, investment stimulus produces little bang for Beijing’s buck, even as it adds to the debt levels.

[..] “They [Beijing] will soon have no choice but to launch massive stimulus,” says Alicia Garcia Herrero, chief Asia Pacific economist at Natixis in Hong Kong. “They do not want to give away their credibility because they said they wouldn’t do it, but there is no time to be cautious any more. Not having growth is ultimately the worst outcome of all.”

Christopher Whalen picks up on Xiang Songzuo’s speech as well, and quotes him saying that “Chinese stock market conditions resemble those during the 1929 Wall Street Crash”. Whereas the China Beige Book states that sales volumes, output, domestic and export orders, investment, and hiring fell on a year-over-year and quarter-over-quarter basis. Which leads to the conclusion that deflation is, or should be, Beijing’s main worry.

Oh, and Chinese consumer demand has weakened, something we’ve seen more off recently. Reuters headlines “China To Introduce Policies To Strengthen Domestic Consumption” today, but that headline could have come from any of the past 5 years or so. Domestic consumption is precisely China’s problem, and they can’t achieve nearly enough growth there.

Foreign investors have convinced themselves that the Chinese Communist Party (CCP) is superior in terms of economic management, this despite ample evidence to the contrary, thus accepting the official view is easy but also increasingly risky. In a December 15 speech , Renmin University’s Xiang Songzuo warned that Chinese stock market conditions resemble those during the 1929 Wall Street Crash. He also suggested that the Chinese economy is actually shrinking.

China growth, Tesla profitability, or the mystical blockchain all require more credulity than ever before. For example, in the first half of 2016 global capital markets stopped due to fear of a Chinese recession. Credit spreads soared and deal flows disappeared. But was this really a surprise? In fact, the Chinese government had accelerated official stimulus in 2015 and 2016 to counter a possible slowdown and, particularly, ensure a quiet domestic scene as paramount leader Xi Jinping was enshrined into the Chinese constitution.

Today western audiences are again said to be concerned about China’s economy and this concern is justified, but perhaps not for the reasons touted in the financial media. The China Beige Book (CBB) fourth-quarter preview, released December 27, reports that sales volumes, output, domestic and export orders, investment, and hiring fell on a year-over-year and quarter-over-quarter basis. CBB is a research service that surveys thousands of companies and bankers on the ground in China every quarter.

Contrary to the positive foreign narrative about “growth” in China, CBB contends that deflation is the bigger threat compared to inflation.“Because of China’s structural problems, deflation has very clearly emerged as the bigger threat in a slowing economy than inflation. Consumer demand has weakened, and you see that reflected in retail and services prices,”CBB Managing Director Shehzad Qazi said in an interview.

So, China phone shipments are down 16%, as per Balding. But Tim Cook says Apple’s never done better. Still, if that 16% number is correct, either Apple or its Chinese suppliers are doing worse, not better. And 16% is a lot.

Despite Recent Battering, Tim Cook Says Apple’s ‘Ecosystem Has Never Been Stronger’

Apple Inc. stock has taken a beating in recent months, but Chief Executive Tim Cook defended his company Tuesday, and expressed optimism that trade tensions with China would soon ease. Apple shares have fallen by more than one-third since their peak on Oct. 3, and tumbled further last week after the tech giant warned of disappointing iPhone sales in its holiday quarter. But in an interview Tuesday with CNBC’s Jim Cramer, Cook said the company was still going strong, and its naysayers were full of “bologna.” “Here’s the truth, what the facts are,” Cook said about reports of slow iPhone XR sales, according to a CNBC transcript.

“Since we began shipping the iPhone XR, it has been the most popular iPhone every day, every single day, from when we started shipping, until now. . . . I mean, do I want to sell more? Of course I do. Of course I’d like to sell more. And we’re working on that.” Slower sales in China also contributed to Apple’s lowered forecast, and Cook said Tuesday he believes that situation to be “temporary.”

“We believe, based on what we saw and the timing of it, that the tension, the trade-war tension with the U.S. created this more-sharp downturn,” he said. Cook said he’s “very optimistic” a trade deal between the U.S. and China will be reached . “I think a deal is very possible. And I’ve heard some very encouraging words,” he said.

16% fewer phones, that gets you the second production cut at Apple and its ‘magnificent ecosystem’ in short order. Now sure, Cook can try and blame the tariffs. but Samsung’s Q4 2018 sales fell 11%, and its operating profit fell by 29%. It’s a bigger and wider issue, and China is at the heart of it.

Apple Cuts Q1 Production Plan For New iPhones By 10%

Apple, which slashed its quarterly sales forecast last week, has reduced planned production for its three new iPhone models by about 10% for the January-March quarter, the Nikkei Asian Review reported on Wednesday. That rare forecast cut exposed weakening iPhone demand in China, the world’s biggest smartphone market, where a slowing economy has also been buffeted by a trade war with the United States.

Many analysts and consumers have said the new iPhones are overpriced. Apple asked its suppliers late last month to produce fewer-than-planned units of its XS, XS Max and XR models, the Nikkei reported, citing sources with knowledge of the request. The request was made before Apple announced its forecast cut, the Nikkei said.

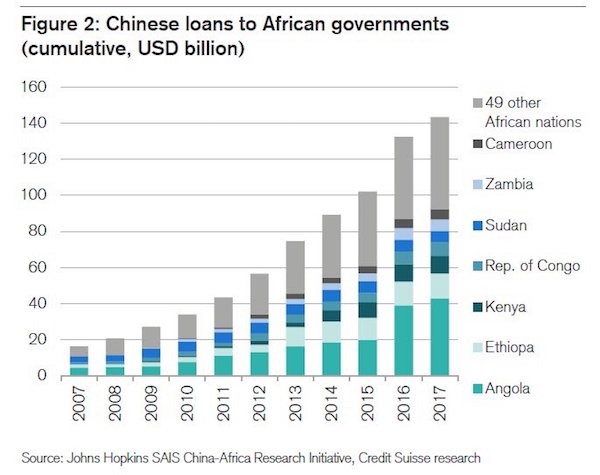

And very much not least there was this graph of Chinese investments in Africa. What are the conditions? At what point will they call back the loans? And when countries can’t pay back, what’s the penalty? How much of this has been provided by Beijing in US dollars it doesn’t have nearly enough of?

It’s like the much heralded Belt and Road project, or Silk Road 2.0, isn’t it, where the first batch of participating nations have started sounding the alarm over loan conditions. Yes, it sounds great, I admit, but I have long said that in reality Belt&Road is China’s ingenious scheme to export its industrial overcapacity and force other countries to pay for it. It’s like the model Rome had, and the US still do, just all in one single project. And this one has a name, and it can be expanded to Africa.

But no, I don’t see it. I think China’s debt, combined with the vast distance it still has from owning a global reserve currency, will call the shots, not Xi Jinping.

China won’t be taking over. At least, not anytime soon.

My problem here is that Xi will focus the Chinese people on an external threat as the wheels come off the economy. I knew the official line was bogus. I just didn’t know it was this bad and getting worse.

Any thought of a war between China and US could easily be dismissed and scoffed at previously as nothing more then the dreams of low ranking officers/grunts of the US military and PLA. The shocked public reaction to the resignation of Mattis from Chinese pundits changed something. They respected his views and professionalism in spite of his… mixed reputation, I noticed that the commentary in various media outlets from retired Chinese personnel started to change. Xi’s order to prepare the military for war immediately followed. A potential conflict in the South China Sea or over Taiwan is definitely possible.

Most economists can’t imagine and don’t think about what all that unused industrial/manufacturing capacity could be re-purposed for. Why, economists didn’t think the Great War would last a year at the time. That kinda proves the dismal science is only interested in cheering on markets and capitalism.

I’d agree with this – the strength of nationalist feeling within China is almost always understated by foreign observers. A conflict over Taiwan (to give one example) would be very popular ‘on the street’ in China and would be an ideal smokescreen for Xi if the economy goes awry. Chinese strategy also sees control of Taiwan as absolutely central to Chinese domestic security.

The only question is whether the Chinese military establishment believes it can keep a war ‘local’ and that depends on their calculations as to whether the US (or Japan, etc) would be willing to escalate up to a full ‘hot’ war. The Chinese can be as wrongheaded in their assessment of the west as the west can be of China. There is no guarantee that sensible decisions will be made.

How could they be wrong-headed? They also have Sun Tzu The Art of War on every business book shelf, don’t they?

China’s number one priority is to avoid fighting a war for Russia, against the US.

For Taiwan, the task is to avoid being the trip wire for the US to fight China.

Beyond that, it is sad that some in Taiwan is foregoing the chance at the Mandate of Heaven, by claiming to be a different country. If Taiwan somehow possessed a secret weapon to enjoy decisive strategic military superiority, the same people would likely claim sovereignty over mainland. But she doesn’t, for now. And that principle is conveniently set aside.

I don’t know I agree. Fighting Russia and breaking up “East Asia” could be beneficial. Sorta like a US regime supporting Iran and the Shia would dump “Russia” in a sec as a “ally”. China could ally themselves with the EU creating a new global power against the Russia/KSA(Sunni)/Lukud alliance(badly under posted by this site, it really is the power elite nobody talks about and who Trump himself is heavily indebted too.

It’s another possibility, as you mentioned (fighting Russia).

I was commenting about fighting for Russia, against the US.

One of the key items, under reported from the gentleman’s speech is that, surprise surprise, Chinese companies don’t make very much money. In fact they have terrible profit margins, and what money is made is often used to speculate in the stock market or real estate. In general, the average Chinese businessman has very little confidence in the future of their business. If you have confidence you invest in the business, not try to get as much money out of the country as you can. Modern China is very much built on shoddy foundations. When the tide rolls out …

Would that also explain why Western businesses, especially American ones, haven’t invested in their companies either? That lack of investment seems to be a result of the the neoliberal slash, burn, and pillage method of profit making; I am not sure that it is the current lack of confidence, but the belief that investing and growing your company for the long term is for suckers.

The sorrow and the insanity of it all is that there are plenty of people who not only want to work, and still have the necessary skills, and plenty unmet needs of all kinds, but the damn investment of all the excess capital floating about is just not happening. Not only is the American, the EU, the Chinese, and the whole planet’s economy likely to crash soon, it is going to happen because the “owners” of the available resources are refusing to use them for the necessary, but still productive and profitable, economic investments. We are just here waiting for whatever country’s economy will crash first and get those dominoes falling.

The crash will be the Biblical Great Tribulation and it will be worldwide.

I’ve been a China Bear since I first visited the country in 1998, and I’ve been proven consistently wrong. The CCP has been very skillful in keeping the train on the tracks. However, its becoming clear that they are rapidly running out of tools – each successive boost to the economy has yielded lower returns, and the problems – most notably rampant investment in low return infrastructure, has been building up more and more potential problems. More and more the Belt and Road scheme looks like a desperate attempt to spend their way out of problems rather than a real strategy. I think they are running out of ideas, and only a fundamental restructure of the economy can save them – Michael Pettis has been writing about this for some time – he advocates a fundamental turn to domestic spending (i.e. putting money in ordinary Chinese citizens pockets), but even that isn’t as simple as it sounds.

I suspect the Chinese government knows this well – hence the recent very severe security crackdown. Its been gradually ramped up (I’ve heard numerous stories of long term foreign expats who have left lately due to harrassment or fear of harrassment), and many Chinese are doing the same. The Chinese government knows there are bad times coming and are determined to keep a firm grip. Given the very firm control they have over the main controls of the economy, they could still steer themselves to a more sustainable growth model, but it really will be difficult for them. There is every possibility of getting stuck into the trap of deflation, which along with rapidly worsening demographics could spell big, long term trouble – Japan on steroids if you like.

The conventional wisdom is that China is not interlinked sufficiently with the world economy for a severe depression (or even outright crash) to have much wider consequences. But as the article suggests, the spread of Chinese invesment throughout Asia and Africa might well have unforseen consequences. Its very clear that the deals done under the Belt and Road are intended to keep locals on the hook for Chinese investments. This could spell big trouble for a lot of countries.

I don’t think your bear stance is wrong–it might only look that way in the short term and contrasted with what I view as Chinese hawks intent on scaremongering. Peter Lee of China Matters has an interesting post “Debunking the China Debt Trap Myth, Sri Lanka Hambantota Edition”, a case which contradicts the prevalent impression that China’s Belt and Road infrastructure projects are a debt trap scheme. (In fact, it’s the usual suspects operating here: Citigroup, Deutsche Bank , HSBC and Standard Chartered and fund managers primarily in the US and Europe.)

Fully agree. I think we can add that China has seen one of the most amazing population moves in history. First it has moved hundreds of millions of peasants off the land and into apartment buildings in cities. We have yet to see how this plays out during harder times (when you are in a flat with no income to buy food it is different than being on the land). Second the 1 child policy really helped fuel the growth. It limited investment in the young (fewer of them) and made all else possible. Imagine if China’s population had doubled in the last 30 years as India’s has done. But now the price must be paid. As the saying goes China had to get rich before it got old. We now have a declining working age population with the implications for growth being clear.

To see where China has come from (my first trip around the country was in 1983) to where it is now is truly amazing. But the professor in his speech also made a very interesting point. He says that China’s problem has not been the speed of its growth, but the quality of it. When you focus on speed alone, you can very easily slip up on quality … This is what has been obvious to keen observers for a long time, and to a lot of the smart money in China, and that is what is going to become clear to the rest of the world rather soon. I think it will be one of those slowly, slowly then all at once kind of moves. The caveat being that in China the biggest fear amongst the government and the people is “luan” (translated basically meaning chaos). Collective memories are there of the points in the not so distant past where starvation and chaos did reign – and this puts some additional urgency in trying not to go over the cliff.

Yes, didn’t the Chinese Government recently up the standards for rebar used in concrete construction to incorporate more vanadium into the steel alloy? Presumably a response to some of the excessive earthquake destruction in western cities. Having said that, most of the city construction occurred before the rebar standards were lifted.

I don’t quite get it. Is the claim that China’s foreign liabilities will soon exceed its foreign reserves? Because otherwise I see no particular reason to worry about the shrinking dragon’s hoard. Especially if a lot of the outlays are loans to other countries that can be scaled back and presumably can be expected to be paid back, at least in part.

I also can’t quite parse the next to last paragraph. What does “export its industrial overcapacity” mean? Exporting the excess products? Literally exporting the capacity? The US has long done the latter, while China did the former. Is the idea that China will switch to the US model?

The cynical view of the Belt and Road initiative is that its primary aim is to export surplus capacity in steel and concrete production. This simple version of the model goes that China uses seed capital to promote railways, roads and ports around the world paid for with cheap loans to other countries. The infrastructure is then built with Chinese labour, concrete and steel (soaking up their capacity). If the project is a financial success, then China gets paid back. If its a failure, then China then squeezes the foreign government for payment in other ways. Either way, China wins.

This is a simplification of course, but the basic cynical view sees Belt and Road as just a way to keep old steel mills and concrete plants open, mostly using other peoples money, with the side benefit that it keeps all sort of opportunities open for improving China’s trade, its ability to influence other countries, plus old fashioned graft.

China, of course, denies this.

I believe there is also industrial strategy behind belt and road initiaitves. China is a country hungry for resources, I would assume that most of those resources must travel via ships… making china vulnerable to a seaborne power (US navy and its Island nation allies like Japan, Taiwan, Phillipones etc…). Linking up Central asia to china gives China access to resources that are not vulnerable to shipping disruption, which are also safe from any disrutpion along China’s coastline. And the logistic advantage can also flow outward… if China should ever need transport supplies, militarily reinforce or ‘discipline’ an ally…

A China less dependant on shipping, is less dependant on good relations with the US.

I have an even more cynical view for you. The One Ball One Chain policy is designed to colonize every country it can reach as thoroughly as possible. The purpose will be to exterminate non-Chinese industry wherever it can and turn all the countries it can into natural resource colonies and captive markets for Chinese manufactures . . . a Metropole-Hinterland concept. . . a series of Tibets.

Please reread the piece. It made a point you apparently missed: the borrowing, both by Chinese private companies, and the government, has been increasingly in dollars. That means Chinese businesses and China are at risk of both default (rollover risk) and higher costs/inflation due to debt costs rising due to the dollar going up and funding costs increasing greatly.

I’m not seeing the downside for the Chinese here. If Beijing hammers the value of the yuan it will negate the effect of American tariffs on Chinese goods. Furthermore, it’s depreciation will serve to shut out foreign firms in domestic markets. That’s probably bad news for Wall Street, but it won’t hurt Chinese investment aboard due to the fact these transactions aren’t typically using yuan. The numerous exceptions to those agreements are on a strict bilateral basis which undoubtedly favors Chinese interests.

The question is, would that stop Wall Street from lending more dollars to China? I think not. The West has been obsessed with the mythical China market for well over a century. It’d probably take a global depression to charter that course and that doesn’t seem likely.

The main downside of devaluation of the Yuan for China is that it will provoke a massive outflow of savings – I would not underestimate the capacity for a panic to set in if the Yuan was seen to be about to tank – almost every Chinese person I’ve met has an exit strategy in place for their family and their money if they suspect that things are going into reverse. Chinese government policy has been to keep the yuan stable against the major currencies of the world for a reason, and its not just to make trading easier. It will also put enormous strain on those Chinese individuals and businesses that have borrowed investment money in dollars or euro and as the article suggests, this amounts to trillions in liabilities.

Again, that assumes the Chinese wouldn’t be able to borrow more USD, There aren’t any promising growth opportunities as enticing as China in the world. Not with the decades of wage stagnation and the massive disparity in the distribution of wealth in the US.

The depreciation of the yuan wouldn’t necessarily spark a panic and/or suddenly tank either. I’m not ruling out the fact that China isn’t already in economic trouble, or soon will be, but as you mentioned above the bears have been consistently wrong for awhile now.

If the Yuan is significantly devalues, there will very rapidly be large pressure in the US to declare Beijing a currency manipulator and impose serious tariffs, say 50 or 100%, or restrict imports in national security areas. Economics news would rapidly became highly entertaining, at least to admirers of the Marquis de Sade. On the bright side, Yves would have plenty of things to write about.

Again thanks to PlutoniumKun for giving me a steer on China’s economy. I don’t find Western Economists that helpful. There has been a perennial avalanche of articles, opinion pieces etc… all saying that this time the Chinese economy will crash. Like a faulty timepiece they will be right once in a while but don’t rely on their writings, pod casts etc… for anything useful. Given all the bad publicity about China, all denigrating China’s financial probity and economic management, you’d think that their Ministry of Propaganda would have been subjected to a route and branch reform. But no nothing. Sun Tzu anyone? Come upon your enemy using stealth?

What have we in the west to show for our collective governments’ economic policies post 2007/8 and what does China have? I would say that we have not much and the Chinese a lot.

One belt one road seems to fit in well with 3,500 years of Chinese history. The Great Wall and the Gand Canal, both huge public enterprises built to increase security and encourage economic development. With this sort of example behind them, are we underestimating China’s strategy?

Does anyone have any examples of Chinese economic history written by Chinese authors? I would be grateful.

Chinese econom y history wirtten by tradional Confucian authors tended to say expensive infrastructure projects led to dynastic downfalls.

For example, this from Wikipedia (Sui Dynasty), referencing the construction of the Grand Canal:

almost every Chinese person I’ve met has an exit strategy in place for their family and their money if they suspect that things are going into reverse.

‘

—

What percentage does that present (people having an exit strategy), of all the people in China?

It’s hard for me imagine a lot of people have that option.

And what does it say about, for example, One Belt One Road?

Obviously, only a small percentage have that option. But they are the ones with all the money.

It’s not immediately apparent, though possible, how a small percentage, with their money, will set off a mssive outflow and cause a panic in Yuan.

So what if they leave with “all the money”? China will still be the one with all the factories.

Reminds me of pre-2010 borrowing in Euros/Krona by Lithuanians, Latvians and Estonians. The problem is that the Chinese economy is so much larger relative to the US/Europe than the Baltic countries are to the EU.

The only thing I would add to what PlutoniumKun said is that as the yuan falls relative to the dollar, loan payments (and principal) will increase in yuan terms, leaving less revenue for consumption or investment. It will also make it harder for Chinese to roll over loans and, I would expect, we would see more loan failures hitting US/EU banks. US/EU banks have possibly hedged that risk, so who knows where the ultimate loses will end up. Would be ironic if the counterparties for some of those hedges were in China. Feeling like 2008 all over again.

Huh? You miss the impact of defaults by domestic businesses who can’t afford their newly much higher payments on their dollar debts. Chinese domestic businesses are borrowing in dollars.

The moneyed class in China have already got their money out and invested in Sydney, Melbourne, Vancouver and London properties, domestic, commercial and industrial. Two years ago the CCB established capital controls to the extent that apartments being completed now will most likely never be paid. The building boom has flopped and all those cities are experiencing property price corrections. To my mind this was the signal that most missed regarding the wobbly Chinese economy.

Meantime, Trump has launched his trade war, causing several Chinamen running around with their nappies around their knees. All the bellicose rhetoric from Xi and his parasites are empty threats. They are stretched beyond their economic capacity so all the fancy guns appearing on warships and stern warnings to the US Navy in the China sea are nothing more than smoke screens. Both sides know both forces would be decimated on any engagement and excepting a deranged finger hitting a launch button, all the sabre rattling will die down pretty quickly.

It is clear that China are not opening up their economy any further, and in fact they are showing every sign of retreating from any move away from a totalitarian society. The game is up. The West are sick of waiting for the promised conformity to the rules based order and China has run out of time. They have enough problems of their own, not the least Taiwan who have no intention of allowing a China takeover. Add to that the internal strife over religion, empty cities, insufficient food production, a polluted country and dealing with stolen electronic patents – one can only imagine things will get worse for their citizens. Greed pushed the West in China and greed will flatten the Chinese economy just as quickly. The countries that will suffer are those that signed up to the Silk Road bullshit which is starting to hit the fan.

China has cheated for twenty years. Rigging their currency, stealing patents, software and western know how, supressing citizens, running covert operations in every country they can – we have known their economic numbers are crap for ever. Their chicken are coming home to roost. Sob! (sarc)

‘The moneyed class in China have already got their money out and invested in Sydney…’

Here is a nice example

So, I wonder when the conservative and neoliberal economic wunderkind of the West will be forced to admit their ideology of property rights leads to political freedom is simply wrong.

A very interesting discussion.

This led me to go in search of Brad Setser https://www.cfr.org/blog/Setser . Setser, you may recall, was Nouriel Roubini’s macro-doppelganger back in the day when Dr. Doom was calling the housing bubble. Subsequently, Roubini went on to fame as a latter day Nostradamus and went behind a pay-wall. Setser went over to the darkside and became staff at the Council of Foreign Relations.

Setser is of interest because he recognized that the giant internal Chinese credit bubble of 15 years ago could, and probably would be wiped out by the CP forgiveness of local credit institution liabilities. And the next internal China debt/credit bubble could happily begin anew.

His macro understanding of international credit flows and bookkeeping was very insightful. His blog is called Follow the Money. It could probably be a regular read.

Yes I remember those days. I kept trying to get them to stop taking about billions of dollars was real money because shorty it was going to be trillions of dollar was real money;-) I always liked the commenters there as I do like you all here.

Thanks for the link. I always enjoyed reading him at the site.

for one viewpoint of how certain actors in the PRC economy behave, I follow https://www.chinalawblog.com/

It provides info on the fashionable “scams” and seems as objective as possible and it’s “biases” are open.

Here is a recent instance of some of the changes along with warnings… https://www.chinalawblog.com/2019/01/chinas-sinosure-its-back-and-it-wants-your-first-born.html

Another view of China other than doom and gloom.

http://www.atimes.com/article/all-under-heaven-chinas-challenge-to-the-westphalian-system/

Thanks for this. Facinating

Excuse me if this has been posted already, but here’s a link to a translation of the professor’s lecture:

https://chinachange.org/2018/12/28/a-great-shift-unseen-over-the-last-forty-years/?utm_source=SupChina+Free+Newsletter&utm_campaign=3e774866f4-20180920+newsletter_COPY_02&utm_medium=email&utm_term=0_96063830a5-3e774866f4-165076183

His solution to low growth is tax cuts and austerity. Shocking.

Regardless, thanks for posting this!

China is very interesting and I’m glad I lived to see it. I think it doesn’t matter if they devalue the yuan because they retained their socialist networks and can enhance them. The expense of getting rid of foreign debt will be absorbed by lotsa people. 1.3 billion consumers is also nothing to scoff at. A little stimulus will go a long way. And China will eventually have an MIC to rival ours and tout its own ‘Global force for Good’. I don’t think they will foreclose on Africa because they will survive their own foreclosures (because good safety net). And when they slow down it will bounce around the world to their benefit. They will always have the lowest value for their currency – especially when you look at China’s wealth per capita. They’ve still got considerable “upside”. Russia just gave/sold them a huge tract of land for agriculture in southern Siberia. And the last thing Russia wants is a destitute China crossing that indefensible border in “hoards”. So Russia will float their oil and gas as much as possible. We should all get real. The question we should ask is Why can’t the wonderful efficiencies of capitalism service their debt? I don’t think that’s a dumb question; it IS the question because it’s the only economic game in town, sadly. And I think it is very cool that the Chinese safely landed their moon goddess on the dark side of the moon. Wow.

Russia and China.

Russia with her vast geography, could use more people, especially after losing so many in the wake of the dissollution of the USSR.

Would Russia invite Chinese immigrants, like what happened centuries earlier when ‘hard working Germans were invited to settle there?

Don’t worry, Donald Trump has a “northwest” passage for illegal Chinese immigrants surging into the US right now…………….well well alive. No wonder he consistently whines about the “southern border”. He doesn’t want his followers to know what is happening in Washington and Oregon.

Those Chinese know how to do a mean acupuncture though!

The great China growth boom is over. It probably went on to long and now you get overcapacity. But that is the way all capitalistic influenced ideals end.

Sugar rush highs that last 30 years or 1 year. Then the gloom and doom.

Ilargi has gotten everything so wrong for so long now that he has no credibility, whether right this time or not.

That is an ad hominem attack and against our written site Policies.

And he has been right about RussiaRussia, the humanitarian crisis in Greece…and pray, what’s wrong with his article before this one?

https://www.theautomaticearth.com/2019/01/the-fed-is-the-ugly-truth/

I used to read his stuff since The Oil Drum and TAE, so my comment isn’t ad hominem at all, it’s based on history. Obviously over the past twelve years we haven’t run out of oil and the world hasn’t come apart. It may yet do so, but how long can people be fundamentally incorrect and retain credibility?