By Wolf Richter, a San Francisco based executive, entrepreneur, start up specialist, and author, with extensive international work experience. Originally published at Wolf Street.

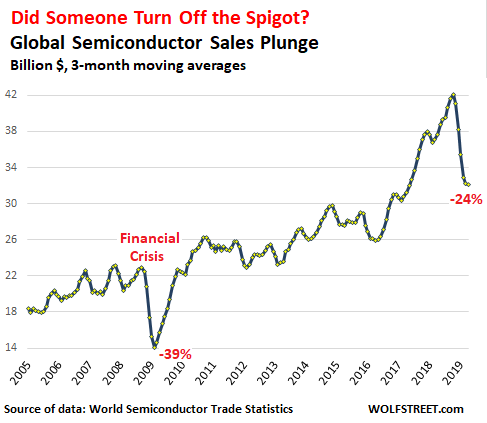

Global semiconductor sales dropped 14.6% in April from April last year, to $32.1 billion, on a three-month moving average basis, the World Semiconductor Trade Statistics (WSTS) organization reported Tuesday afternoon. The three-month moving average in April has plunged 24% from the peak last October, thus continuing the deepest plunge in semiconductor sales since the Financial Crisis:

In dollar terms, semiconductor sales plunged by over $10 billion in April compared to the pace in October 2018, the largest peak-to-trough dollar-drop ever. During the Financial Crisis, chip sales dropped by $9 billion from peak to trough.

But in percentage terms, the current plunge doesn’t quite measure up: 24% versus the 39% collapse during the Financial Crisis and the 45% collapse during the long dotcom bust.

The Semiconductor Industry Association (SIA) said in its press release that sales, based on the data compiled by the WSTS, dropped in all major geographic regions in April (three-month moving averages compared to the same period last year):

- Americas: -29.5%

- Europe: -8.0%

- Japan: -10.9%

- China: -10.9%

- Asia Pacific/All Other: -10.7

And sales may not pick up anytime soon:

The SIA “endorses” the WSTS projections that chip sales for the full year 2019 will fall by 12% from the record levels of 2018, to $412 billion. In terms of regions, the SIA expects semi sales to fall across the board for the full year 2019:

- Americas: -23.6%

- Europe: -3.1%

- Japan: -9.7%

- China and other Asia Pacific: -9.6%

So maybe next year: The SIA expects that sales in 2020 will “bounce back somewhat, posting moderate growth of 5.4%,” from the much lower levels in 2019.

The huge spike and plunge that the semiconductor industry is facing currently is a result of several factors piling on top of each other.

The China debacle.

Potential tariffs and trade tensions between the US and China and potential export controls of tech products, such as semiconductors, to China has caused a stampede in 2018 to front-run these policies.

Just how prescient this stampede was has now been demonstrated by US efforts to clip the wings of Chinese tech and telecom giant Huawei Technologies, whose telecom infrastructure equipment (think 4-G and 5-G) and smartphones, are sold around the globe. They contain US semiconductors. And Huawei has been preparing for these eventualities.

Since the middle of 2018, Huawei has been stockpiling chips and other tech components. Bloomberg reported that according to its sources, it stockpiled enough components to keep its business running for at least three months after it gets cut off from US suppliers. This would give it some time to realign its supply chain.

The Nikkei, citing “multiple sources,” reported in May that Huawei has stockpiled six months’ to a year’s worth of “crucial components,” such as semiconductors, that had a higher risk of falling under export controls, to prepare for a worst-case scenario where its key suppliers would be barred from doing business with it. And it has stockpiles of less crucial components that would last for three months.

Huawei is not the only Chinese tech company that has been preparing for these scenarios. Acquiring these stockpiles means accelerated purchases. This is likely one of the reasons for the long spike in the chart above that peaked in October. And after these companies had acquired the stockpiles, chip sales began to drop.

Decline in global smartphone sales.

Global smartphone sales went from stagnation in 2018 into decline in Q1 2019. According to Gartner Inc., sales in Q1 fell 2.7% compared to the same period last year to 373 million units. Huawei was number two, behind Samsung, and both of them far ahead of Apple. iPhone sales in Q1 plunged 17.6% year-over-year. You see, Apple is now trying to sell services to brush off its dismal iPhone sales. These dynamics put a dent into semiconductor sales.

Decline in global PC and laptop shipments.

Global PC and laptop shipments in Q1 fell 4.6% year-over-year to 58.5 million units, according to Gartner. The Big Three vendors – Lenovo, HP, and Dell – were able to increase their shipments. And their market share rose to 61.5% in Q1, up from 56.9% a year earlier. The smaller kids on the block lost out. Apple’s shipments fell 2.5%. The remaining vendors were confronted with larger drops, ranging from -7.3% for Asus and -13.2% for Acer to -20.9% for all others.

The Crypto-mining collapse.

Demand for special rigs to mine cryptocurrencies collapsed in 2018, and this hit semiconductor makers, such as Nvidia, that make these specialized chips.

Data Center boom slows down. China’s fault again.

Data centers are part of the infrastructure of the “cloud.” This business had been on a relentless boom. And it may still be, but…. Intel caused its shares to swoon with its Q1 earnings report when it disclosed that chip sales of its data-center unit had fallen 6.3% from a year ago, due to weakness in China and large stockpiles among its customers. This came after a warning in January about slowing data center sales in Q4.

CEO Bob Swan said that Intel’s customers in China had “absolutely” stockpiled extra data center chips in 2018 due to the risks of tariffs or export controls. And those stockpiles are still around and need to be consumed.

This spike and plunge in semiconductor sales is a result of a confluence of factors. The global decline in demand for smartphones and PCs – both now mature markets – would have been enough to turn chip sales down. But the China trade issues, the frontrunning of tariffs and export controls, the stockpiling of chips, now topped off by actual tariffs and export controls did much of the rest.

Exports-at-all-costs for economic growth comes home to roost. Read… US Cleanest Dirty Shirt Among Manufacturing Giants: Germany at Crisis Level. China, Japan, South Korea Contract

I am a bit disappointed at the analysis by Wolf, focusing on 1-year doom-and-gloom rather than the big picture. The graph makes it clear that, unlike the drop in 2008, the current plunge is market returning to the mean after a bumper year (mid-2017 to mid-2018). Increases in 2017 and 2018 were outside a long-term trend for superconductor sales over the last 15 years, so it’s normal that there would be regression.

Good point.

Reminiscent of the dot.com boom/bust that was also a case of front running the then feared Y2K theoretical problem with older computer hardware in software: When the year 2000 rolls over on the calendar then computer will melt down. (Didn’t happen.) There was a huge amount of new hardware and software purchased starting in 1997 to replace older hardware. The replacements were purchased ahead of normal rotation replacement schedules and cause the IT stocks to boom. Once the year 2000 rolled over and nothing melted down then purchases went back to a normal replacement schedule. The NASDAQ and Dow tech sectors swooned.

Partly true. In the y2k programs, IT capex rose from an average run rate of 8% to 45%. Vendors warned customers that any equipment out of warrenty was not y2k compliant, which boosted vendor revenues, and caused the “dot.com ” boom.

After 2001 cleanup, IT capex was reduced to xzro for 3 years, onlly to recover to its historical 8% slowly.

Vendor greed caused the dot.com bust.

Agreed…

A regression to the mean is a regression to declining growth. Is that sustainable?

Capitalist economies don’t function well when things revert to the mean. There must always be growth, and when there isn’t trouble mounts as is currently the state with regards to semiconductors.

It’s not a return to the mean. It’s a return to the growth trend.

Good analysis here. Interesting how trade tensions compound to make this market more volatile. If this dynamics extrapolate to other sectors the business cycle could well be in recession territory. Is this our canary in the coal mine?

Data centers?? Snooping into our private lives to sell us more junk and exercise better control over the “cattle” is what drives the economy now? Specialized chips to store our inner workings for subsequent data mining and analysis? It’s all good cause, profit?

Good grief. What will happen if they can’t stick pins in us like butterflies and map out each tick and twitch? Talk about predator states (and states of mind). No wonder we’re going over the edge.

Voislav makes a good point that this does look like regression to the mean, unlike the Great Recession crash down from normal levels.

Wolf’s point may still be valid, though, if you take into account that the Great Recession was a financial-driven crisis and tech was collateral damage.

I feel that the Trump era will be looked-back upon as an artificial boom caused by Keynes’ style “animal spirits”. The underlying issues of the fading (and too timid) Obama stimulus package remained, but were over-ridden by a boom in investment by about half of the American populace who had been told (and believed) for 8 years that Obama’s over-regulation was absolutely wrecking the economy.

Trump’s election caused a feeling of relief and elation from that segment of the economy: happy days are here again! the Great Regulator is gone (and his simpering minion Hillary vanquished). It’s time to expand our businesses and be ready to collect the riches falling from the fingers of our New York real estate billionaire!

Hence the boom in chip manufacturing. (and fracking wells, etc)

The air is coming out of that balloon a bit now as the excitement fades. People are starting to realize that the Trump Economy is very much like the past Trump enterprises…always looking for the greater fool.

Windows PCs are my hobby that keeps me somewhat involved in the real world since I retired. Intel is in real trouble since they laid off 10,000 employees. They are like Boeing. Executives are extracting wealth for themselves at the expense of the company’s future. AMD on July 7th will start selling its 12 core/24 thread 7nM CPU at twice the cost of its replacement. Intel is stuck with a 14nM die for another two years. A trade war between exceptional USA and chauvinistic China can only escalate. Even if war, the first conflict since the 1953 Armistice, is avoided; the disruption of the supply chains over what is and isn’t made in China will cause disruptions and increase costs. China will keep the 737 Max grounded. Tariffs will rise to 25%. PCs will remain stuck where they are. It will be something else that pops the bubble and the survivors will then give it a name.