By Wolf Richter, publisher of Wolf Street. Originally published at Wolf Street

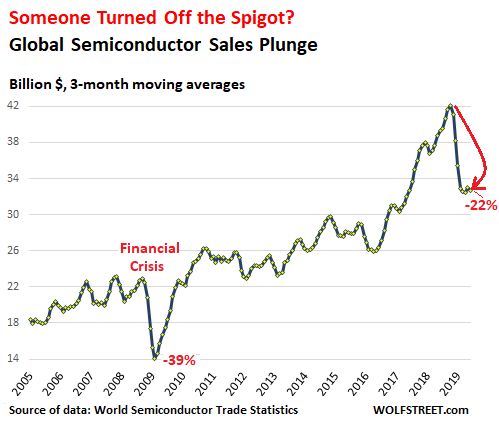

Global chip sales plunged 16.8% in June from June last year, to $32.7 billion, on a three-month moving average basis, and are down 22% from the peak in October 2018, according to the World Semiconductor Trade Statistics today. As deepest and most relentless plunge in semiconductor sales since the Financial Crisis continues, any hopes for a V-shaped recovery, such as during the Financial Crisis, have been shelved:

This was the fifth month in a row that the three-month moving average has been in the range of $32 billion to $33 billion, down about $10 billion from the peak in October last year, the steepest dollar-drop ever. During the Financial Crisis, sales plunged and then bounced back instantly, for a perfect V-shaped recovery. But this time around, sales have been stuck at low levels for five months already.

In percentage terms, the 22% drop from the peak pales compared to the 39% plunge during the Financial Crisis and the 45% plunge during the long dotcom bust. The dotcom-bust plunge was the worst, not only the deepest in percentage terms, but also by far the longest in duration.

For the first six months of 2019, semiconductor sales dropped 14.5% compared to the same period last year. And sales were down “across all major regional markets and semiconductor product categories,” the report by the Semiconductor Industry Association said.

Sales fell in all major geographic regions in June (three-month moving averages compared to the same period last year):

- Americas: -29.5%

- Europe: -10.9%

- Japan: -12.8%

- China: -13.9%

- Asia Pacific/All Other: -13.7

The culprits span the spectrum, from the decline in smartphone sales to the crypto-mining collapse. But now add a new one that is spreading across the globe:

Auto Sales Drop Around the Globe

What was at first thought to be a localized drop in China and a little bitty dip in the US and some squiggles in Europe has now turned into a serious global downturn, and there are a lot of semiconductors in each new vehicle rolling off the assembly line. While chips for EV-related components such as battery management systems are still experiencing growth, chips for ICE-vehicle components are getting hit. This include the multitude of chips in emission systems, engine management systems, transmissions, fuel systems, lighting systems, infotainment systems, driver assist systems, etc.

In the second quarter, global sales of new vehicles fell 7% compared to the same period last year, after having already fallen 6.5% in the first quarter, according to Bloomberg Intelligence. I have covered the sales debacle in select hot spots:

- In China, the world’s largest market, new vehicle deliveries are down 12% so far this year;

- In the US, the world’s second largest market, deliveries are down for the third year in a row and are back to 1999 levels;

- In India, deliveries have plunged about 25% in May and June year-over-year, for a host of reasons, including a shadow-banking financial crisis;

- In the UK, auto sales dropped to a five-year low;

- In Canada, auto sales fell 5.5% in the first half this year, after having already fallen for the year 2018, on track for the second year in a row of declining sales.

Smartphone Sales Drop Around the Globe

In terms of the number of devices shipped, global smartphone sales have declined in the first half, from mere stagnation in 2018, according to Gartner Inc., which expects unit sales for the whole year to continue on the same path and end the year down 2.5%, with the steepest declines in Japan (-6.5%), the EU (-5.3%), and North America (-4.4%).

“In mature markets, the high-end smartphone market is particularly oversupplied and commoditized, with higher average selling prices (ASPs) and no compelling new utility or experiences for users to upgrade to,” the report said.

PC/Laptop Shipments Fell Then Ticked Up

In the second quarter, global PC and laptop shipments ticked up 1.5% compared to Q2 2018, after having fallen 4.6% in Q1, according to Gartner.

The Big Three vendors booked increases in shipments in Q2 – with Lenovo up 15.9%, HP up 2.6%, and Dell up 2.1% – and were able to increase their market share to a combined 64.1%, up from 60.7% a year earlier. The also-rans all booked declining shipments: Apple -0.2%, Acer -14.4%, ASUS -9.9%, and Others -6.7%.

Global IT Spending on Hardware Falls

Total IT spending, hardware and software, is expected to remain about “flat” at $3.7 trillion globally in 2019, “despite uncertainty fueled by recession rumors, Brexit, trade wars and tariffs,” according to Gartner. Software sales are expected show growth (Enterprise Software +9.0%, IT services + 3.8%, and Communications Services -1.0%).

But hardware sales – that’s where semiconductors end up – are expected to fall in dollar terms in 2019: Data Center Systems (“the cloud”), which used to be the hottest of the hot segments, -3.5% and Devices -4.3%.

“Although an economic downturn is not the likely scenario for either 2019 or 2020, the risk is currently high enough to warrant preparation and planning. Technology general managers and product managers should plan out product mix and operational models that will optimally position product portfolios in a downturn should one occur,” the report said.

The US-China trade-war debacle.

The rhetoric last year about potential tariffs and export controls triggered a stampede in 2018 on all sides to buy semiconductors to front-run actual tariffs and export controls. That is one of the reasons why semiconductor sales surged to that extent last year.

These export controls have now hit Chinese tech and telecom giant Huawei Technologies, whose telecom infrastructure equipment and smartphones contain US semiconductors. Huawei has seen this coming and has prepared for it by stockpiling semiconductors and other potentially affected components to keep its business supplied for up to six months or a year, allowing it time to realign its supply chain. Other Chinese companies have made similar preparations – all of which boosted chip sales and inventories last year, and created a hangover this year.

The Crypto-mining collapse.

The boom in the special rigs used to mine cryptocurrencies was huge and contributed to the surge in chip sales in 2017 but it collapsed in 2018, which hit certain chip makers in a concentrated manner, such as Nvidia.

Chips go into an endless variety of goods. Even a new toaster has a chip or two. The goods-based sectors globally have been ailing, and chip sales are a sign of that. But they’re also a sign of how the economy reacts to uncertainties, such as the threat of tariffs and export controls in 2018, and then the actual imposition of them.

US makers of heavy trucks – such as Peterbilt, Kenworth, and Mack – are still floating on top of what was a historic order backlog created in 2018. But orders have collapsed, and that backlog is dissipating fast. Read… Heavy-Truck Orders Collapse Stunning 81%. Lowest Since 2010

Every time Wolf gets an article posted it’s time to do the opposite.

Sorry, I don’t see a recommendation in Wolf’s post, which is why I ask, what is it you intend to do the opposite of?

And your reasoned objection to the content of this post is….?

I’ve been buying computers for our company for twenty years, until about four years ago it was always new stuff. Then the improvements in performance and reliability seemed to peak, and the last new desktops I purchased were more or less ‘perfect’.

When these exact same machines came on the refurbished market I had no hesitation about purchasing them because the new ones I purchased had never had a failure, and the cost for a PC that was once around $1500.00 went to $200-300.

My impression is that ‘improvements’ since the advent of the i5 processor and Win 7 have not been to advantage the users of PCs so much as those who wish to profit from mining our information and selling us stuff.

Improved processor speed and increases in memory past a certain point seem to deliver little improvement to the business users experience, and I suspect all that extra horsepower is being used to mask the load that commercial surveillance creates.

In my personal life, I preferred Macs, but now Apple has joined the crapification craze, and I’m starting to look for sources of ‘vintage’ refurbished Pro Books because I can’t bring myself to let go of my 2015 model.

IMO, the IT environment has turned sour, IOT in particular is an annoying mess, and IOT enthusiasts are worse than the hardware.

Cameras and phones threaten to overwhelm bandwidth no matter how much you provide, and can easily swamp the business if allowed free reign.

With the situation as it stands, I can well understand how the ‘market’ might be impacted adversely by customer satisfaction alone, let alone the trade-war issue.

The lack of increases in performance is simply because the hardware isn’t getting much more powerful each generation. Moore’s Law has been degrading for years.

“the hardware isn’t getting much more powerful each generation. Moore’s Law has been degrading for years.”

Not exactly.

The number of transistors is still going up per unit area, with the scale of ICs now well below what was supposed to be a fairly hard barrier – production chips for consumer use are now being fabbed at 7 nanometres.

Furthermore, the levels of integration are rising, and cache is expanding apace.

Specialized processing is now being outsourced to dedicated silicon, aka GPUs, which are now integrated with processors at speeds of up to a gigaflop/sec, and much faster if packaged on their own. In this case I’m thinking of the Ryzen APUs with Vega graphic processors, not the Intel integrated graphics.

Even more important is increasing use of parallel processing, with chips having six, eight, twelve, or 16 processor cores. Some software isn’t catching up as fast as other software, but the rising demands of things like real time malware scanning, distributed content management and rendering, and the like are keeping multiple cores busy.

The single core, single thread speed hasn’t been going up that fast… but 12 or 16 threads plus a GPU can get a lot more done.

But for general office use? A five or six year old computer is just fine.

We’ve sort or reached a mature stage of ‘good enough’ in desktop computers, just as we don’t need general purpose automobiles to do 250 kph, or airliners to fly higher than 14,000 metres,

Real time data analysis, scientific visualization, or high end gaming may need a LOT more to do an optimal job, but that’s a small portion of the user population.

It’s nice to have the crypto-miners moving on, though. High end graphics cards were ridiculously expensive recently, as RAM had been for the last 7 years.

I finally let go of my old Quad pentium-pro (compaq DL380) a couple years ago, because I couldn’t get any cards for it any more. Linux/BSD guy here, it still had amazing desktop performance. Oh well, everything is multi-core 64 bits nowdays anyhow, and RAM sizes allow me to eliminate swap.

I would not shed one year for the semiconductor industry. They had zero problems with not reacting to the crypto craze by ramping up production(and watching the prices of gpu’s skyrocket). Now that things have returned to quasi normal don’t think that they are doing awful.

To add to what Watt4Bib said above, the only improvement to the PC we have seen in the last five years has been the Solid state drive becoming mainstream. Processors and video cards improve slightly each generation, but not enough to jump in and buy a new Mobo and CPU. I am still using a six year old processor that can keep up with software released today (no problems with games either).

GPUs actually are continuing to improve each generation. Both in performance and in technology (ray-tracing is a game changer).

Yes, I use my laptop for computer aided design, surfing the world with GoogleEarth Pro (lots of image processing), life-like Rendering of models and the GPU improvement (scene processing software and hardware (fast memory)) over the last few years has been impressive.

GPU’s are going from 1080 to 4k.. the average user’s eyeballs can’t tell the difference between them. We are reaching the limit of human eye resolution.

Not remotely true. The difference 4k makes for real-time visuals is night and day. Less so for prerecorded video, but if you’re getting UHD content you’re usually also getting HDR, which is much more important than the increased resolution. The real discernible 1:1 point for digital and analog film is probably around 8k.

And anyway, while GPUs can mostly now do consistent 4k/60fps, plenty of people would say the sweet spot is something like 1440p/120, or even higher (you can buy 144hz monitors, and people swear by them).

Uh, is not the drop back onto the long term trend line? Do we assume competence amongst all players in this market? Are people stashing cash in the form of purchased feed stocks?

The recent semiconductor sales spike seems to coincide with DRAM memory price gouging (https://www.techrepublic.com/article/samsung-hynix-micron-sued-for-dram-price-fixing-that-could-have-raised-pc-prices/ mentions that the memory companies’ revenues doubled between Q1 2016 and Q3 2017).

So Samsung/Hynix/Micron got sued for price fixing last year (once again), and the memory prices completely coincidentally started coming down pretty quick after that.

How much of the sales drop is due to the memory cartel simply taking a breather to minimize the size of this round of fines? The sales graph looks like it is just back to the trend line, after all.