CalPERS is acting exactly the way traders on Wall Street do when they are sitting on serious losses, or in CalPERS case, underfunding so deep that they can’t earn their way out of it. They put on desperate, high risk positions in the hope they can climb back out of their hole. Pros will tell you that this is just about always a fast path to ruin. CalPERS’ version of swinging for the fences is to increase its commitments to its riskiest strategy, private equity, embark on investing in a new risky category, private debt, and leverage the entire fund.

The fundamental outlook is so poor that even Warren Buffet, known among other things for astute contrarian plays, can find nothing to buy. Yet CalPERS thinks that now is the time to load up on risk. It not only plans to add to private equity but also to load up on another speculative investment, private debt, while also leveraging the entire portfolio. Did CalPERS miss out on the finance lesson that leverage increases losses as well as profits?

This scheme smacks of CalPERS yet again going for fads after their sell-by date. Remember how the giant fund was gung-ho to get into late-stage venture capital, as in unicorns, right before their valuations started to plunge? The only reason CalPERS didn’t go ahead was press and beneficiary criticism, particularly since the plan was so badly thought out.

CalPERS appears to have learned all the wrong lessons from that episode. Instead of recognizing that they are a favorite target for gimmicks, and they tend to be very late to the party on investment trends, they instead have opted for ideas that are simpler to implement than their newfangled “new private equity business model”.

There’s an additional cause for pause in the Financial Times summary of CalPERS’ plans: CalPERS yet again is abusing transparency laws by holding discussions of these plans in secret. The fund is required to discuss this matter in public under the Bagley-Keene Open Meeting Act; it doesn’t fall under any of the few exemptions. Yet none of this information can be found in agenda or documents for the Investment Committee meeting later today.1 The fact that CalPERS planted this story (it has extensive quotes from Chief Investment Officer Ben Meng) says there was nothing that needed to be kept confidential.

Key points from the Financial Times account:

Calpers is to move deeper into private equity and private debt by adopting a bold leverage strategy that the $395bn Californian public sector pension fund believes will help it achieve its ambitious 7 per cent rate of return.

In a presentation to the Calpers board, Ben Meng, chief investment officer, said the giant fund would take on additional leverage via borrowings and financial instruments such as equity futures. Leverage could be as high as 20 per cent of the value of the fund, or nearly $80bn based on current assets. The aim is to juice up returns to help the scheme, the largest public pension in the US, achieve its growth target.

“In a presentation to the Calpers board”? No such presentation has been or is on deck to be made in open session. That is an admission that CalPERS provided closed session materials to the Financial Times. Notice the double standard: CalPERS executives routinely leak what they’ve designated as confidential material (whether it is legitimately confidential or not) while anyone else suspected of doing so, even a board member, is strung up.

But let’s focus on the substance: the idea of upping CalPERS private equity and private debt wagers, and turbocharging risk with fund-level borrowing.

We don’t need to break a sweat to show what a bad idea it is to increase private equity and private debt investments now. Financial Times stories in the past ten days give ample evidence.

Even before the coronacrisis, private equity for more than a decade has not been generating enough in the way of return to compensate for its extra risks. That means that it cannot be regarded as a prudent investment. And the wreckage of a deflationary shock that is taking out or severely damaging entire sectors of the economy, from business travel to restaurants to gyms to live entertainment to restaurants, is pulling down other areas, like commercial and residential real estate and state and municipal governments. The few pockets of opportunity won’t begin to offset the wreckage.

As we described in our related post today, the Financial Times featured a new, important paper by Oxford professor Ludovic Phalippou that shows, in considerable detail, how since at least 2006, private equity has merely produced returns similar to public equities. That means there is no justification for investing in private equity, since it needs to generate a higher return to compensate for its greater risks (greater leverage and lack of liquidity). It is a loser on a risk/return basis.

Private debt is even more loopy. Consistent with CalPERS adopting trends only when they are after their sell-by date, private debt was once an attractive investment. Private equity insiders would point out that it offered only slightly lower returns than private equity, with markedly lower risk.

By contrast, as a Financial Times story pointed out, corporations have already binged on debt between buybacks and now loan-based rescue schemes. If they don’t get more equity, they will go bankrupt on a widespread basis. From the Financial Times in Fidelity chief warns of global corporate solvency crisis:

Fidelity International boss Anne Richards has warned that the asset management industry will struggle to provide enough capital to fix the solvency problems public businesses face as economies emerge from lockdown.

The fund management executive, whose investment company oversees £305bn in client assets, said many businesses would need an injection of capital to offset the high levels of debt they had accumulated during the crisis, which has left whole industries unable to operate….

The scale of cash needed to repay the public funding businesses have received from governments or central banks is likely to be so large that it is “either going to be written off or sit on balance sheets, where it will have a depressing effect”.

As for the idea of leveraging the entire fund, we had argued that German investors, who eschew private equity, instead borrow against their entire portfolio to achieve a similar level of risk. Upping the level of private equity and debt investments and adding fund level leverage is going all in at just about the worst time to do so. Has CalPERS forgotten that it took over 20 years for US stocks to get back to their 1929 levels? The Atlanta Fed’s GDPNow’s second quarter forecast is -48.5%. What about “probable depression” don’t you understand?

Not surprisingly, the Financial Times shows CalPERS to be deluded on other fronts:

Mr Meng hopes Calpers’ deeper push into illiquid assets over the next three years will help it exploit its structural strengths. Its perpetual nature allows it to make longer-term investments, while its size gives it access to top managers in private equity markets where performance is widely dispersed.

Huh? CalPERS is not special in being a long-term investor. So to are other public and private pension funds, life insurers, along with many sovereign wealth funds.

And the “access to top managers” is misguided. If Meng means “top managers in terms of performance” he ought to know it’s impossible to find them ex ante, since top tier performance no longer persists. You might as well throw darts. And the fact is that CalPERS is so large it will tend to have private equity index-like returns no matter what it does.

If Meng means CalPERS size gives it some sort of advantage with respect to the biggest funds, he’s high on his own supply. Private equity fund managers do give fee breaks on larger size investments, but anyone who makes that big a commitment gets that deal. And as the Phalippou paper makes clear (and as we’ve reported based on other studies), the biggest funds, which do classic leveraged buyouts, have delivered the weakest returns of all private equity sub-strategies.

And if anything, CalPERS is disadvantaged in its access to private equity. The former head of private equity, Real Desrochers, was seen in the markets as difficult to deal with. CalPERS’ failure to replace him and its consideration and then abandonment of its confused and shape-shifting “private equity new business model” revealed CalPERS to be in internal disarray. Private equity firms don’t make investors in political turmoil their first call. It’s too hard to close the sale.

Not surprisingly, the comments at the Financial Times ranged from politely skeptical (several “What could go wrong?”) to brutal. A sampling:

Connecticut

Leveraging up a pension fund or endowment is a terrible idea at any time, but this has to be the worst possible time to do so — virtually all asset classes are expensive and the macroeconomic environment is awful. Low rates are not a good reason to borrow. The people running Calpers should be immediately fired.

koopa troopa

Hawaii’s pension system used leverage and was hit very hard in 2018. Who the hell is running Calpers? LOL! Sad day in America. Oh yea, Hawaii isn’t front page news… Just take Hawaii’s situation and 100x it… You get California in 2025 when the S&P 500 is down 50%…

https://www.institutionalinvestor.com/article/b17wyqq1z770qw/hawaii’s-investment-chief-got-fired-then-the-gossip-started

From the basement

The top is in.

Neil at home

Can you short pension funds?

cajun food

“Bold move” is not what you want from your pension administrator

R2D4

Sounds like an absolute disaster in the making.

Kairos

I am quite shocked reading this. A return target was (is?) the curse of European asset managers in the run up to 2007. The Japanese pension funds had similar targets in the 1990s which spawned the growth of PRDCs (power reverse dual-currency notes). With rates close to zero, a target of 7% and a willingness to take illiquid assets I fear the worst for the CALPERS beneficiaries.

Needless to say, there is seldom so much unanimity of opinion in the Financial Times’ comment section, which has market savvy readers. But CalPERS is firmly ensconced in its bubble. Normally, more bad results might shake the board out of its stupor, but this board is so captured by staff that nothing is likely to change until the board is turfed out or Gavin Newsom wakes up to the risk of CalPERS getting in even more trouble than it ought to on his watch.

________

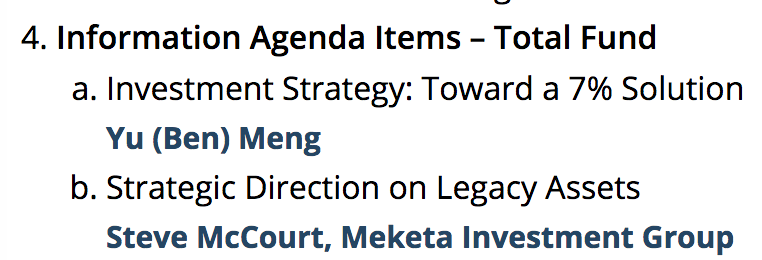

1 This has to be a closed session matter. All the items are routine and/or recurring except for #4:

This isn’t about legacy assets, plus the Financial Times makes clear Ben Meng is behind these plans, so it looks as if CalPERS is hiding the discussion of these major policy changes under the opaque and innocuous label, “Toward a 7% Solution”. That’s confirmed by the subhead of the Financial Times piece: “Calpers hopes bold move will boost efforts to achieve its 7% return target.”

The comment by Kairos is really important: “I am quite shocked reading this. A return target was (is?) the curse of European asset managers in the run up to 2007. The Japanese pension funds had similar targets in the 1990s which spawned the growth of PRDCs (power reverse dual-currency notes). With rates close to zero, a target of 7% and a willingness to take illiquid assets I fear the worst for the CALPERS beneficiaries.”

Why? Because target returns are useless for pension schemes. At the end of the day, it’s not the return, but rather:

*Do you have the cashflow to pay your pensioners over time.*

It’s actually very simple. You have to be able to pay what you owe to the pensioners at different points in time. This is rather straightforward to do…you load up on conservative debt (government, high quality corps) that pays out over the time scales you need them to. The other parts of your investment portfolio you have overlays to ensure hedging against interest rate risk, credit risk, etc. which should help make up your deficiencies if you are under-funded. If you have a young pension scheme, maybe an equity overlay. When you do all that, you then ask the question – am I able to pay the pensioners that I have? And will I be able to pay the pensioners that I WILL have.

I overly simplify, but good gods. CalPERS is obviously being used as a cash cow for someone or someones. Never be sexy if you are a pension scheme. The whole point is to be boring and worry about risk. You are paying someone’s pension, not making money to help pay for your yacht.

Oh man…I sound so old…

Back in the 1990’s I was doing research in urban property markets in the UK. Most of the shopping centres and mixed use developments dating from the 1960’s and 1970’s that I was looking at had been funded and owned 100% by pension schemes – sometimes there would even be a proud plaque at the entrance – the West Bromwich High Street mall for example had one saying that it was owned by the National Union of Miners pension fund. As someone in the property game said to me at the time (from memory): ‘Its pretty simple – pension funds had the cash to buy up the land over a few years, and good contacts with the local authorities and Unions for overcoming obstacles private developers couldn’t get past. They could then build a shopping centre, and have a reasonable expectation of capital appreciation, while the rents provided liquidity to pay the pensions’.

It seemed quite a simple model to me. Too simple and workable I suspect.

More important is the fact that it makes absolutely no sense to have pension funds from any remotely attached to reality perspective.

You can make money out of nothing but money is not real wealth, real wealth you most definitely cannot manufacture out of thin air in the same way.

In the end, having a “pension” means that the rest of society will be willing to provide you with goods and services when you get old.

The recognition that real wealth cannot be manufactured by the magic of compound interest leads to the straightforward conclusion that the most sensible way to fund pensions is through general taxes, and that the elimination of the whole giant industry of financialized scams that has grown around the current model is in the best general societal interest.

But we do not live in a world in which people are even remotely attached to reality….

To mix the metaphors in the title, the problem with blowing your brains out in public is that a lot of brain matter gets splattered over bystanders. Unfortunately, I think its the pensioners who will be the recipients of facefulls of gore.

On the other hand, to kill the zombie, you have to blow it brains out. But I never heard of the zombie management wanting to blow their own brain out TBH.

Leverage on top of leverage. PE is already leveraging equity at 4-9x EBITDA and Calpers wants to leverage that even more? Private debt suffers from adverse selection, it’s all the garbage banks and CLOs won’t touch and it’s run in a format whereby there is incentive to put money to work vs credit committee (even if that’s laughable too) to hold back from bad deals. Is there a way to suspend Calpers activities by the governor or someone in CA? It seems they are reaching the point of really vaporizing public capital.

And the inevitable conclusion will be all funds should be fully privatized including the management of Calpers, outsourced CIO function with blackrock etc charging 50bps on $326B…

CLOs have Cov-lite loans in there, right? So this means the private debt in question here is junkier than even those?

Using a Sherlock Holmes cocaine reference as a name for an investment strategy. What are they trying to say there?

Thank you. This is the twist that makes the point.

Yves is at her most precisely focused when it comes to CalPERS. In the years I’ve been reading her, this is the most addled policy, at the worst possible time, in such degree as now it just looks like they’re trolling us.

Or perhaps, the Machine is working perfectly.

And Trump is helping:

https://sirota.substack.com/p/news-trump-just-fulfilled-his-billionaire

+1. They have a PE

addictionproblem? ;)Is one of the perks at CalPers free airplane glue?

Like the character Arthur Dent in the book “Hitch-hiker’s Guide to the Galaxy”, I’m starting to not feel surprised at the latest antics by CalPERS. There doesn’t seem to be any point anymore. It does not matter what they try to do, they always manage to pick the wrong thing to do, even if it goes over the line to outright criminality. They can’t help themselves. They are like a Long Gone Bad TV series. If it weren’t for the pensioners, it would be almost funny. But as Neil at home said in comments – ‘Can you short pension funds?’

Lots of people here have seen the TV series “Parks and Recreation” so I can just imagine a TV series based on CalPERS. It would be hilarious. Remember that in putting together “Parks and Recreation” that the writers spent time researching local California politics for the series. Can you imagine one based on CalPERS which is actually based in California? I mean the possibilities. The staff would turn up for work one Monday to find that the entire building has been painted purple. In the middle of a pandemic, the staff would be called together in a small stadium for a three hour session on how to deal with a pandemic followed by a sing-song. And the dialogue-

CFO: “The economy is imploding with only the Feds holding up the stock market. We need to put our investments into safe places.”

CEO: “Good thinking. We will take on additional leverage via borrowings and financial instruments such as equity futures to juice up high returns.”

CFO: “Ah, this is obviously some strange usage of the word ‘safe’ that I wasn’t previously aware of.”

I’m waiting to find out how Margaret Brown gets blamed for this leak.

It seems the only leaks ever are Board members who do not toe the staff line.

In my 3 decades of interacting with CALPERS and its leaders and its staff: Those paid less than the buyers of the biz, will be bought. Look at who was there and where they are now and you see they, “Follow the money.”

This is madness, but a conventional sort of madness, the most dangerous kind, imo.

” The conventional view serves to protect us from the painful job of thinking.”

John Kenneth Galbraith

And, as NC has reported on the hostility that the few thinking board members face:

“In any great organization it is far, far safer to be wrong with the majority than to be right alone. ” -John Kenneth Galbraith

CalPERS needs an intervention.

Thanks for your continued reporting on CalPERS, PE, and pensions.

Ben (Yu) Meng’s WSJ editorial yesterday reads like it was written by the CalSTRS Ministry of Truth, even more disingenuous relative to the Meng/CalPERS standard of deceit, taking credit for the Treasury bonds that CalPERS have held for decades, and also touting the management fee savings from firing managers of publicly traded stock portfolios, but fails to mention that the greater funding of private equity will lead to fees paid by CalPERS much much greater. Fees are about 0.30% for equity managers, but ten to twenty times more, 3 to 6% for private equity general partners.

Why is Meng pushing CalPERS capital into private equity? It’s a win-win for all the Insiders. Private equity general partners receive enormous fees, plenty of cushion to grease the patronage in Sacramento, good for Board members who support it, best of all for Meng, padding his supporters’ pockets and assuring him a multi-million dollar sinecure position once his leverage scheme goes bust, while California taxpayers, as always, will be called upon again to clean up the mess

Correction — “CalPERS Ministry of Truth”

Meng’s ties and adoration for his “motherland” are well documented. Has Governor Newsom investigated whatsoever? How about the Department of Justice/FBI? Every day more mainstream press report on Chinese espionage activity in America. Why are executives and board members protecting Meng? As an outsider looking at the situation, it sure smells of a coverup with the public defense of Meng. Beneficiaries and stakeholders are owed an independent investigation into Meng’s ties to the Chinese communist party and government. Last, I wonder if any of these private investments will be going into Chinese companies, some of which put American military, businesses and society at risk.

At some point maybe the board will figure things out at CalPERS but I am doubtful. A greater push into private equity is all about Ben Meng’s career strategy – finding the next better higher paying gig he can schmooze his way into. Having given up on active investing in public markets, the responsibility for oversight of which Meng has entirely devolved to his Deputy Dan Bienvenue, he can now focus his attentions on the smallest part of the portfolio but the one that will have the biggest potential impact on his personal bottom line when he snags his lifelong coveted job at Blackstone, TPG, Carlyle or wherever. It really is a farce Yves. CalPERS already has 2/3 as much committed but uninvested capital in private equity, on which it is paying a 1.5% for the privilege, as it does money which has actually been put to work. The staff in Private Equity resisted putting more money to work because they could not find attractive deals so as a % of fund private equity exposure has fallen in recent years. What Meng’s push means is that he will be overriding staff and buying bad deals to get money into the space. Of course by the time it becomes apparent how bad these deals were Meng will be long gone and living large.

As for private credit the fund has spun its wheels ever since it created the team there over three years ago under a completely ineffectual head, a CalPERS lifer, who has now moved on to other easier duties for which he is equally ill suited. Think as well about the insanity of using leverage by an institution where the head has repeatedly told it’s stakeholders and the general public that he does not believe the fund has the ability to add value actively investing in public markets. If you can’t do that how can one imagine when to use leverage to try to boost returns. Might as well give dynamite and matches to children.

The Calpers Investment Strategy:

One for you

One for me

One for you

One for me…

Buried in Obfuscation…

Followd by: Who Could Have Knowed? and not on My Watch!

Reminded me of Raymond DeVoe’s observation acknowledged by Warren Buffett in 2017: “More money has been lost reaching for yield than at the point of a gun.” Don’t really know, of course, but I will default to a view that the CalPERS staff are not financially stupid or naive people. Setting aside underlying concerns related to past performance and behavior patterns, maybe this Investment proposal and related media strategy is perceived as a “Win-Win” by CalPERS staff:

1.) Perhaps it is intended to trigger formal reconsideration of the 7% ROI target in a deflationary environment where financial assets have been pushed up beyond historically high price valuations despite the COVID crisis, yet liquidity appears to be abundant.

2.) This proposal implicitly sets forth the risk parameters associated with the incremental debt leverage. If the investment target is not formally reset to a lower level, they can argue: “We tried.”

Seems to me the real mistake here is not publicly recognizing and discussing current financial market and economic conditions driving this proposal in an open forum, publicly acknowledging the associated risks, and soliciting input from plan beneficiaries and California state taxpayers.

3 paragraphs from Meng’s WSJ editorial yesterday are pasted below. While they have several misrepresentations, the most deceptive is: “Leverage can exacerbate some short-term volatility.” This misleading statement grossly misrepresents and understates the risk of leverage, failing to convey that leverage can result in a permanent loss of capital.

“More assets” refers to a plan to use leverage, or borrowing, to increase the base of the assets generating returns in the portfolio. Leverage allows Calpers to take advantage of low interest rates by borrowing and using those funds to acquire assets with potentially higher returns.

This approach is not without risk. Private debt can reduce liquidity. Leverage can exacerbate some short-term volatility. But prudent use of leverage can reduce risk over time by allowing Calpers to keep more exposure in diversifying assets such as Treasury bonds, while pursuing higher returns in other parts of the portfolio.

We have factored in these realities carefully and have implemented a comprehensive, forward-looking plan for mitigating risk. Over the past several months, we have meticulously planned a measured shift toward this strategy, improving liquidity management, installing proper controls and a centralized management framework.

I know several pensioners of CalPERS, all of whom were law enforcement and retired between 50 and 55 years of age, receiving north of $100K. Regardless of their “investment strategy”, how many of these former employees can taxpayers continue to support? Each position is 2, 3 or even four persons deep, with only one who actually reports to work while the others are delivered to the lap of luxury. Contrast this with SS (which we’re continually reminded is broke) where the average retired recipient receives $1,200 – $1,400/ month at the age of 65 and it becomes abundantly clear why it is unsustainable. Even the illustrative Jerry Brown called CalPERS a giant Ponzi scheme.

This all just reminds me of our dearly departed, the late, great Richard Feynman. To paraphrase, “Never get so carried away that you go against nature and let the math equations lead your logic.” Unfortunately that is exactly what we have done in our desperation to make “capitalism” work. And we still can’t define what we are doing. It’s truly batshit. We have gone against natural reason like lemmings; like a pandemic of the mind. No wonder that a tiny coronavirus is bringing us back to earth.

I wonder if the next instalment of the CalPERS saga will be taking a big stake in the Hertz insolvency offering.

There is no way that a public trust fund such as CalPERS should be putting fund assets at such risk. He and his staff claim that these are “opportunistic” investments — but they’re acting like Leo DiCaprio jumping onto the Titanic just as it leaves the quay. Certainly a higher rate of return can be promised by a failing borrower — but the down-side isn’t just a lower return. It’s losing the principal. Pension funds and insurance companies can’t squander their reserves like that. It’s a per-se violation of fiduciary duty.

What is Meng’s touted up-side? He tells Bloomberg today that CalPERS can increase its chances of hitting their crack-head return target of 7-percent from a ludicrous 39 percent likelihood to what?

Still a worse chance of success than a coin-flip. It would be a far better strategy to engage in a political dialogue with the state legislature and the local contracting authorities to look for a way to spread-out the pain that is already a certainty than this cowardly strategy of acting like a gambler down to his last few chips doubling-down on a pair of jacks…

I’d be laughing, but I’m a CalPERS beneficiary. Meng’s high-handed authoritarianism makes me think that whack-job Indiana congressman Jim Banks may be on to something…

David, I agree with your last paragraph. Meng’s ties and adoration for his “motherland” are well documented. Has Governor Newsom investigated whatsoever? How about the Department of Justice/FBI? Every day more mainstream press report on Chinese espionage activity in America. Why are executives and board members protecting Meng? As an outsider looking at the situation, it sure smells of a coverup with the public defense of Meng. Beneficiaries and stakeholders are owed an independent investigation into Meng’s ties to the Chinese communist party and government.

Amazing! It’s like they’ve never heard of the hard on austerity oriented economists and officials have for getting rid of public pensions.

Just imagine the lure into the abyss them buying stocks will be?

Nice Title, glad you jumped on this

A new ideology, neoliberalism, hid the dodgy, old, 1920’s neoclassical economics that lurked underneath, which still has the same old problems it’s always had.

The economics of globalisation has always had an Achilles’ heel.

In the US, the 1920s roared with debt based consumption and speculation until it all tipped over into the debt deflation of the Great Depression. No one realised the problems that were building up in the economy as they used an economics that doesn’t look at debt, neoclassical economics.

Not considering debt is the Achilles’ heel of neoclassical economics.

When you use this economics, policymakers run the economy on debt until they get a financial crisis.

Policymakers don’t realise it’s the money creation of bank loans that is making the economy boom as they head towards a financial crisis.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

US policymakers run the economy on debt until they get a financial crisis in 1929 and 2008.

https://www.youtube.com/watch?v=vAStZJCKmbU&list=PLmtuEaMvhDZZQLxg24CAiFgZYldtoCR-R&index=6

At 18 mins.

As a CEO, I can use the company’s money to do share buybacks, to boost the share price; get my bonus and top dollar for my shares.

Share buybacks were found to be a cause of the 1929 crash and made illegal in the 1930s.

What lifted US stocks to 1929 levels in 1929?

Margin lending and share buybacks.

What lifted US stocks to 1929 levels in 2019?

Margin lending and share buybacks.

A former US congressman has been looking at the data.

https://www.youtube.com/watch?v=7zu3SgXx3q4

All the mistakes of the 1920s are being repeated.

“The Great Crash 1929” John Kenneth Galbraith

“By early 1929, loans from these non-banking sources were approximately equal to those from the banks. Later they became much greater. The Federal Reserve Authorities took it for granted that they had no influence over these funds”

He’s talking about “shadow banking”.

They thought leverage was great before 1929, they saw what happened when it worked in reverse after 1929.

“The Great Crash 1929” John Kenneth Galbraith – a recommended read for US policymakers, they might realise they are repeating old, 1920’s mistakes.

At the end of the 1920s, the US was a ponzi scheme of over-inflated asset prices.

The use of neoclassical economics and the belief in free markets, made them think that over-inflated asset prices represented real wealth accumulation.

1929 – Wakey, wakey time

Where had all that wealth gone to?

In the 1930s, they pondered over where all that wealth had gone to in 1929 and realised inflating asset prices doesn’t create real wealth, they came up with the GDP measure to track real wealth creation in the economy.

The transfer of existing assets, like stocks and real estate, doesn’t create real wealth and therefore does not add to GDP. The real wealth creation in the economy is measured by GDP.

Inflated asset prices aren’t real wealth, and this can disappear almost over-night, as it did in 1929 and 2008.

Real wealth creation involves real work, producing new goods and services in the economy.

Free market thinking split into two separate paths in the 1930s.

We took the wrong path.

In the 1930s, Hayek was as the London School of Economics trying to put a new slant on old ideas.

While Hayek was at the LSE, the free market thinkers at the University of Chicago were working out where it all went wrong in the 1920s.

The Chicago Plan was named after its strongest proponent, Henry Simons, from the University of Chicago.

He wanted free markets in every other area, but Government created money.

To get meaningful price signals from the markets they had to take away the bank’s ability to create money.

Henry Simons was a founder member of the Chicago School of Economics and he had worked out what was wrong with his beliefs in free markets in the 1930s.

Banks can inflate asset prices with the money they create from bank loans.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

Henry Simons and Irving Fisher supported the Chicago Plan to take away the bankers ability to create money.

“Simons envisioned banks that would have a choice of two types of holdings: long-term bonds and cash. Simultaneously, they would hold increased reserves, up to 100%. Simons saw this as beneficial in that its ultimate consequences would be the prevention of “bank-financed inflation of securities and real estate” through the leveraged creation of secondary forms of money.”

https://www.newworldencyclopedia.org/entry/Henry_Calvert_Simons

Real estate lending was actually the biggest problem lending category leading to 1929.

Richard Vague had noticed real estate lending balloon from 5 trillion to 10 trillion from 2001 – 2007 and went back to look at the data before 1929.

Henry Simons and Irving Fisher supported the Chicago Plan to take away the bankers ability to create money.

“Stocks have reached what looks like a permanently high plateau.” Irving Fisher 1929.

This 1920’s neoclassical economist that believed in free markets knew this was a stable equilibrium. He became a laughing stock, but worked out where he had gone wrong.

Banks can inflate asset prices with the money they create from bank loans, and he knew his belief in free markets was dependent on the Chicago Plan, as he had worked out the cause of his earlier mistake.

Margin lending had inflated the US stock market to ridiculous levels.

The IMF re-visited the Chicago plan after 2008.

https://www.imf.org/external/pubs/ft/wp/2012/wp12202.pdf

Why did it cause the US financial system to collapse in 1929?

Bankers get to create money out of nothing, through bank loans, and get to charge interest on it.

https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf

What could possibly go wrong?

Bankers do need to ensure the vast majority of that money gets paid back, and this is where they get into serious trouble.

Banking requires prudent lending.

If someone can’t repay a loan, they need to repossess that asset and sell it to recoup that money. If they use bank loans to inflate asset prices they get into a world of trouble when those asset prices collapse.

As the real estate and stock market collapsed the banks became insolvent as their assets didn’t cover their liabilities.

They could no longer repossess and sell those assets to cover the outstanding loans and they do need to get most of the money they lend out back again to balance their books.

The banks become insolvent and collapsed, along with the US economy.

In the 1930s, Hayek was as the London School of Economics trying to put a new slant on old ideas.

While Hayek was at the LSE, the free market thinkers at the University of Chicago were working out where it all went wrong in the 1920s.

Unfortunately, Hayek turned up at the University of Chicago in the 1950s.

He started throwing his weight around and forced them to accept his own half-baked ideas about the markets.

Here Is Jerry Brown who ultimately failed to do something about it all.

https://www.latimes.com/projects/la-me-pension-crisis-brown/

What is Gavin Newsom doing?