CalPERS looks more and more like the gang that can’t shoot straight. CalPERS’ PR department is flogging a new Bloomberg story about the unseemly departure of Chief Investment Officer Ben Meng, which means the pension fund planted it and is pleased with it. In fact, as one prominent beneficiary said, “It’s ironic that they prefer this terrible narrative over various other terrible narratives that are probably closer to the truth.”

If you are late to this story, Dan Primack of Axois provided this summary:

When Ben Meng suddenly resigned as chief investment officer of CalPERS, America’s largest public pension system, the press release quoted Meng as saying “it’s important for me to focus on my health and on my family.”

- Now, though, CalPERS officials are slowly acknowledging what seemed obvious: Meng’s decision was likely influenced by blogger Susan Webber’s discovery that Meng had filed inaccurate conflict-of-interest disclosures, including a failure to note personal investments in private equity firms that regularly seek business from CalPERS.

- Betty Yee, California’s state controller and a CalPERS director, told the Sac Bee that she was disappointed by a “lapse in both judgment and adherence to standard conflict-of-interest policies.”

An earlier Bloomberg account included that Yee had called for an emergency board meeting,now set for Monday August 17. The way CalPERS’legal department noticed the meeting is yet another criminal violation of the Bagley-Keene Open Meeting Act, if the board simply intends to talk more about Meng or the meeting is to discuss a possible disciplining or even termination of CEO Marcie Frost.

CalPERS’ Spin Misfires

Given how often CalPERS is in reputational hot water, you’d think by now it would know how to put the best face on a bad situation. Instead, if you take CalPERS’ messaging hash at face value, it confirms our criticism of CalPERS’ weak compliance function and poor controls.

CalPERS via Bloomberg tries to depict Meng as sympathetic, when readers who have worked with him give quite a different picture (see here and here) and CalPERS as fully aware for months that Meng had violated California conflict of interest laws. Specifically per Bloomberg:

…in April, a compliance team uncovered at least one conflict-of-interest violation, it set in motion a chain of events that threatened to spark a firestorm of criticism and thrust him into the center of even more hostility.

And the subhead for the story includes: “CIO approved investment in Blackstone fund while owning shares.”

This is a massive misdirection.

CalPERS knew, and chose to ignore, that Meng had a conflict of interest problem in January 2019, not April 2020. Meng filed his initial financial disclosure form on January 31, 2019, which was as of his assuming office date, January 2, 2019. That form showed three private-equity related positions: Blackstone, Carlyle, and a credit fund run by Ares.

CalPERS’ strategy for many years had been to make large commitments to private equity funds so as to pay lower fees.1 That has had the effect, as CalPERS own private equity consultant has pointed out, of concentrating CalPERS investments in the “buyout” strategy which is tantamount to saying CalPERS mainly invests with the really big private equity fund managers. Blackstone and Carlyle both are among the four biggest private equity firms. CalPERS has also for years been stressing that private equity is central to meeting its 7% return target. It was inevitable that Meng would wind up overseeing commitments to Blackstone and Carlyle and thus violate California’s conflict of interest laws.2

CalPERS should have told Meng to dispose of his private equity stakes as soon as it received his financial disclosure forms. There was simply no way for CalPERS to continue with its private equity love affair and not have it blow up Meng. As the Bloomberg article suggests, Meng should have been alert enough to work that out.

Meng violated conflict of interest laws in 2019, not 2020, and with Carlyle, not Blackstone. CalPERS via Bloomberg misleadingly tries to suggest, but in 2019, with $328 million commitment to a Carlyle European fund, Carlyle Europe Partners V.3

CalPERS’ claim it knew Meng had a problem in April means it engaged in a cover-up for months. As we described above, CalPERS had already known Meng had private equity stakes. Even before Meng filed his Form 700 in April, which by the way was nearly a month late, CalPERS should have known Meng had not sold his Blackstone and Carlyle positions because Meng is also required to clear all of his personal trading with CalPERS. In other words, CalPERS knew or was horribly remiss if it did not know that Meng had not disposed of his private equity stakes.

So even if we believe this bizarre account, what could have triggered the complacent and complicit CalPERS to rouse a bit from its stupor?

As we indicated, the Form 700 filing contained no new information with respect to Meng holding Blackstone and Carlyle. Was it that the Investment Office, under its way too generous “delegated authority,” had committed $1 billion to a Blackstone fund in March? Or could it have been that someone in Compliance was alert enough to notice a new entry, that Meng had a new “teaching contract” for Schwarzman College at Tsinghua University, and that Schwarzman was the long-standing CEO of Blackstone?4

So the only explanation that fits the CalPERS spin is that CalPERS had a look in April and decided to do nothing. Four months is more than enough time for CalPERS to have acted if they intended to get in front of this problem. Instead, our contacts say CalPERS hired a lawyer for Meng less than two weeks before he departed.5 That is consistent with our Public Records Act requests having stirred the pot. On June 8, we noticed that CalPERS had not put up any Forms 700 for calendar 2019 and requested them from 2016 to present for all board members plus a long list of named executives including Meng. On July 27, we supplemented that original request with another Public Records Act request:

Please provide any materials or writings related to actual or potential recusals by Chief Investment Officer Ben Meng.

In other words, to the extent CalPERS really did wake up to the fact that Meng had a problem in April, its executives apparently concluded they would not be held to account for ignoring their legal obligation to report the issue to toothless Fair Political Practices Commission and they had nothing to worry about.

Another Criminal Violation of Open Meeting Laws, or Is Frost in Serious Trouble?

Recall that the default for a California public agency like CalPERS is that information is public, and that board decision-making is to take place in public meetings so as to allow affected constituents the opportunity to provide input before a decision is made. This right is enshrined in Article 1 of the California Constitution:

SEC. 3. (a) The people have the right to instruct their representatives, petition government for redress of grievances, and assemble freely to consult for the common good.

(b) (1) The people have the right of access to information concerning the conduct of the people’s business, and, therefore, the meetings of public bodies and the writings of public officials and agencies shall be open to public scrutiny.

(2) A statute, court rule, or other authority, including those in effect on the effective date of this subdivision, shall be broadly construed if it furthers the people’s right of access, and narrowly construed if it limits the right of access. A statute, court rule, or other authority adopted after the effective date of this subdivision that limits the right of access shall be adopted with findings demonstrating the interest protected by the limitation and the need for protecting that interest.

Nevertheless, legitimate personnel matters are exempt from public disclosure. But not surprisingly, CalPERS has taken to overstretching the personnel exemption in order to hide embarrassing topics from its constituencies. It’s pretty rich to see Frost tell a howler like this to the board….

A Bloomberg reporter is writing another story today and I wanted you to know that I made the following written statement regarding specific questions he asked. Once the story is online, I’ll forward you the link.

“When it comes to personnel matters, we follow California state law and always protect privacy and due process and the rights of the individual. And, we’ll always stay true to our mission. Every day, we focus on the 2 million people who are counting on us to provide them with financial security in their retirement.”

….when the Bloomberg piece describes a meeting between only between Frost and Meng. And you can be sure Meng was gagged as part of his departure. So somehow Frost is protecting privacy and played coy with Bloomberg when she conveyed information only she could have known about Meng through her minions.

In other words, what is considered to be private at CalPERS depends on what serves Frost’s needs, not anyone else.

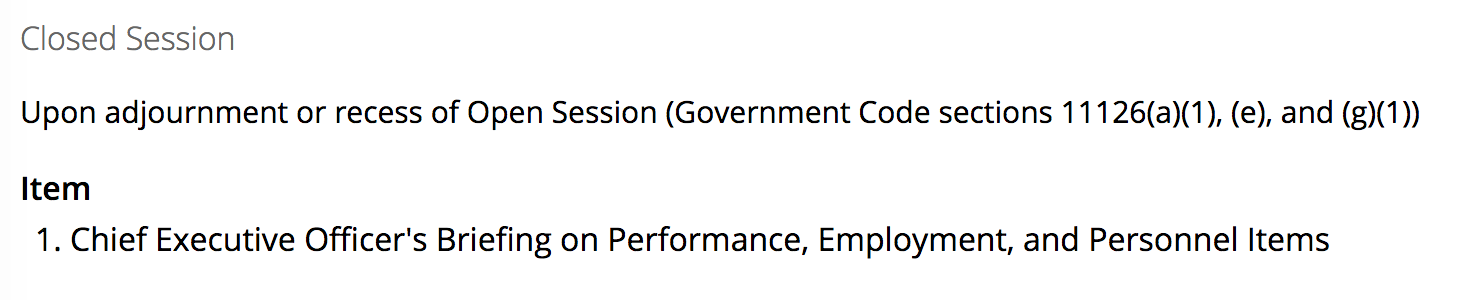

Here is how CalPERS has justified its closed session for August 17:

Because Meng is no longer an employee, he is not entitled to the personnel exemption in Section (a)(1). And given how much CalPERS babbled on Meng’s behalf to Bloomberg, it’s clear they don’t take his privacy seriously.

Bear in mind that under this section, it is the boards’ option to discuss personnel matters in private. Given that CalPERS has chosen to provide a great deal of internal detail to Bloomberg, and that separately, Controller Yee called the meeting to discuss policy, it would seem that any discussion would be of senior executives who ought to be able to stand up and defend their actions. In other words, the personnel excuse looks intended to try to improve a coverup, rather than serve the public.

Section (e) covers pending litigation and the matter has to be ripe for this section to apply. So is CalPERS thinking of suing Meng? Doubtful given how they just painted him as a victim in Bloomberg, plus litigation would result in more embarrassment, which is the last thing CalPERS wants. So this is another legal overreach by General Counsel Matt Jacobs.

For Section (g) to apply, CalPERS arguably could be discussing the hiring of a new Chief Investment Officer, but it is highly unlikely given that Yee called this session and wants to do a post mortem plus it is inconceivable that staff could be far enough along on the recruitment of a replacement to have anything to tell the board. Thus this section is not invoked legitimately unless discussion is expected to include a discipline or termination of CEO Marcie Frost:

(g) This article does not prevent either of the following:

(1) The Teachers’ Retirement Board or the Board of Administration of the Public Employees’ Retirement System from holding closed sessions when considering matters pertaining to the recruitment, appointment, employment, or removal of the chief executive officer or when considering matters pertaining to the recruitment or removal of the Chief Investment Officer of the State Teachers’ Retirement System or the Public Employees’ Retirement System.

Frost has six staunch cronies on the board and they would argue it would be too disruptive for her to go on the heels of Meng’s ouster unless another shoe were to drop between now and the board meeting.

As for Meng, our reader vlade explained via e-mail why his departure was good for CalPERS:

Most people on the trading desks trade (on their account). But most of them stop when they get to MD level or higher, it’s just too problematic in too many way. If Meng could not stop trading as a CIO, he’s not good enough for the role.

.

_____

1 The large private equity funds provided for tiered pricing, with larger commitments getting fee breaks.

2 From the California Government Code; this section is known as the “Political Reform Act” and is enforced by the Fair Political Practices Commission:

87100. No public official at any level of state or local government shall make, participate in making or in any way attempt to use his official position to influence a governmental decision in which he knows or has reason to know he has a financial interest.

87103. A public official has a financial interest in a decision within the meaning of Section 87100 if it is reasonably foreseeable that the decision will have a material financial effect, distinguishable from its effect on the public generally, on the official, a member of his or her immediate family, or on any of the following:

(a) Any business entity in which the public official has a direct or indirect investment worth two thousand dollars ($2,000) or more.

(b) Any real property in which the public official has a direct or indirect interest worth two thousand dollars ($2,000) or more.

(c) Any source of income, except gifts or loans by a commercial lending institution made in the regular course of business on terms available to the public without regard to official status, aggregating five hundred dollars ($500) or more in value provided or promised to, received by, the public official within 12 months prior to the time when the decision is made.

(d) Any business entity in which the public official is a director, officer, partner, trustee, employee, or holds any position of management.

(e) Any donor of, or any intermediary or agent for a donor of, a gift or gifts aggregating two hundred fifty dollars ($250) or more in value provided to, received by, or promised to the public official within 12 months prior to the time when the decision is made. The amount of the value of gifts specified by this subdivision shall be adjusted biennially by the commission to equal the same amount determined by the commission pursuant to subdivision (f) of Section 89503.

For purposes of this section, indirect investment or interest means any investment or interest owned by the spouse or dependent child of a public official, by an agent on behalf of a public official, or by a business entity or trust in which the official, the official’s agents, spouse, and dependent children own directly, indirectly, or beneficially a 10-percent interest or greater.

3 The Carlyle fund closed in late October 2019, which means it is inconceivable that the fund was approved before Meng joined, not simply based on the time but also based on the lack of adult supervision in private equity before Meng joined. Former Chief Investment Officer Ted Eliopoulos announced his plan to leave CalPERS in May 2018 and left in November 2018. CalPERS had had no head of private equity for well over a year as of when Eliopoulos departed. CalPERS did not announce the hiring of a new Managing Investment for private equity until May 2019.

4 A colleague dismissed the notion that this gig amounted to fee for bona fide services: “After watching Meng’s charade with David Petraeus, it’s pretty clear that these ‘talks’ are content-free. ”

5 Needless to say, no one outside the CalPERS bubble buys the health pretext. Staff at CalPERS confirm that there was no indication that the 51 year old Meng had any physical ailment. And for anything short of the sudden onset of a debilitating condition, a senior executive in good standing would give notice.

“As we indicated, the Form 700 filing contained no new information with respect to Meng holding Blackstone and Carlyle. Was it that the Investment Office, under its way too generous “delegated authority,” had committed $1 billion to a Blackstone fund in March? Or could it have been that someone in Compliance was alert enough to notice a new entry, that Meng had a new “teaching contract” for Schwarzman College at Tsinghua University, and that Schwarzman was the long-standing CEO of Blackstone?”

As reported

1) Ben (Yu) Meng’s 2019 Form 700 states that Meng received between $10,000 and $100,000 in 2019 from the Schwarzman College at Tsinghua University in Beijing for Meng’s services as a “Teacher”.

2) The Schwarzman College at Tsinghua University in Beijing is funded by Steven Schwarzman, the CEO of Blackstone

3) Ben (Yu) Meng was employed by CalPERS during the entire calendar year 2019. Evidently Meng decided he needed to supplement his more than a million dollar annual CalPERS compensation with payments received from the Schwarzman College at Tsinghua University. Curious how Meng found time to be a “Teacher” in Beijing while he was the CalPERS CIO in Sacramento.

4) Meng also continued to own shares of Blackstone, Carlyle, and Ares.

5) Meng allocated a $1 billion contract to Blackstone and a large contract to Carlyle.

Marcie Frost, calpers CEO and Meng’s supervisor, by all evidence, instead of effectively addressing these gross abuses of public trust, instead decided that the solution was more mendacity by the calpers Ministry of Truth

Frost…”Every day, we focus on the 2 million people who are counting on us to provide them with financial security in their retirement.”…so it can be quietly stolen and the blame laid on “incompetence” rather than malice… Somehow that last section was left out, must’ve been a clerical error or innocent oversight, Sorry…

https://www.youtube.com/watch?v=ef99bFBTR54

But in all seriousness what should one expect from the State of California? For instance, in Cali the rules of the road are different from other places, i.e., the driver with the more expensive car has the right of way. Pelosi and feinstein masquerade as politicians of the people while they enrich themselves and their families on the public dime. Your social standing is compiled by counting how many dollars you have. If a worker complains, you replace them with a member of the international class of poverty who knows that having a hedge to sleep under is way, way better than not having a hedge to sleep under (Is that why they are called “hedge funds”? Because they intend to have everyone other than themselves sleeping under a hedge?) Cali is and has been for a number of years, corrupt to the core. “As goes California, so goes the nation” is another olde truism that seems to be holding forth once again.

You forgot to add #6, which is as Yves reported earlier, Meng’s form 700s contained many false statements given that a comparison between Meng’s initial form 700 vs his 2019 form 700 contains many entries that can not be reconciled.

Yes, Marcie had a choice, either address the false statements and conflicts of interest in Meng’s form 700s or try to hide them from the public, and Marcie decided, contrary to CalPERS stated principles, to try to bury them even though form 700s are public documents. Four months later, only because of Yves repeated public request acts, was calpers forced to release these public records, notwithstanding Henry Jones’s subsequent disingenuous claims likely provided by the CalPERS Dept of Spin that these form 700s are private personnel matters.

To know to request Meng’s 2019 and 2020 700 forms and compare them is a talent limited to true forensic accountants. That’s our dear Yves. Why the State of California didn’t do this is worse than a mystery – it’s almost evidence of collusion by somebody. And that sweet little Marcie failed to do this is also an indication of possible collusion. So malfeasance seems to apply. For almost everyone involved. So that raises a question in my mind – just how far and deep are the tentacles of private equity? I’d like to know why this sort of almost “innocent” enablement isn’t simply a case of obstruction of justice? While they fleece the biggest retirement fund in the USA. Let’s ask Mitch – after all, Kentucky is right in the middle of a similar law enforcement.

This is not even a matter of schadenfreude anymore but more akin to watching fish being shot in a barrel. He could have gone on for years working for CalPERS but at the end of the day, he just could not help himself and started playing funny-buggers with his disclosure forms. Did he not learn in Master of Business Administration 101 that if you cannot cover up your tracks, that you should do the right thing? This is getting so serious this that the State Government of California might actually be forced to do something (cue the fainting couches). I mean, perhaps an audit is due for the rest of the CalPERS Board to make sure that they do not have any conflicts of interest. Myself, if I had my way and was the Governor, I would call in the CalPERS Board and make them say that they had no conflicting interests in their financial reports. But if they lied and they did, then it would be the Number 9 Treatment. And you would have to only do it once. For the encourager les autres you understand-

https://www.youtube.com/watch?v=1OLTvxzHWXU

What is the crime when an institution engages in a coverup of a criminal act? And, if someone would show that CP then indimidated any employees to help with the coverup, would not it fall under the federal RICO? (now that would be fun!)

I’m still somewhat amazed that nobody could see the awful conflict of interest involved in having a CFO having a financial stake in what should be considered contractors to the organisation. I’ve personally been in organisations where very senior people were ‘encouraged’ to resign for significantly less obvious violations (in one case, it was a CEO’s wife who held interests that could have been seen as influencing decisions). In one organisation I worked for, a senior manager was permanently sidelined (and eventually given an early pension) for not declaring a financial interest in a key decision but she was not actually removed because it was considered potentially too embarrassing if the conflict became public knowledge.

Even if this was an ordinary private company, not a public pension fund, this would be considered highly dubious at best. This isn’t about Meng. It’s about deep organisational rot. I really don’t know how this can be cured. I hate to quote Jordan Peterson as a source, but he once said something along the lines of ‘its very easy to make a good organisation dysfunctional, but almost impossible to fix a dysfunctional organisation.’ The problem of course is that you can’t just wind up a major pension fund and then start again from scratch.

Personal items, so that we can make it closed to other interested parties. Looks childish.

Attorney general Basura is gonna be all over this like white on rice, you betcha.

Real soon…

I seriously doubt that. He’s no better and they’re all scratching each other’s backs.

You are new to CalPERS! Tom regularly makes this sort of comment. It’s his running deadpan.

Tom is a connoisseur of California dysfunction.

Like mustard on a tie at a county fair. Like butter on my muffin. Like a Rolling Stone (albeit, it’s Keith Richards when the nurses have forgotten his medication).

Holy Toledo! The Dark Lords of Pirate Equity must be miffed…

Matt Jacobs and Marcie Frost should be expecting a visit from the Nazgul for failing to deliver their prey in proper form.

CalPERS circling the wagons? Waiting for the cavalry (aka gov and state lege) to come to its rescue? Millions of Californians depend on the Board competently exercising thier fiduciary duty, yet instead this cronyist, incompetent Board is reaching absurd new heights of rationalizations.

Thanks for your continued reporting on CalPERS, PE, and pensions.

2, 4, 6, 8

Defenestrate

Then obfuscate

Go team!

I’ve seen a number of Ponzi schemes go down, my favorite being Bruce McNall, but he’s just chopped liver compared to this gargantuan undertaking which isn’t really a Ponzi scheme, but what is it?

It’s accepting favors from vendors; self-dealing (indirectly); failure to disclose; false disclosures; abuse of trust – quite a litany and probably more administrative misdemeanors also.

They’re circling the wagons for a reason. This should just be the start of a thorough housecleaning.

From the last CalPERS post:

“And our experience is when an institution becomes rotten, not only do the remaining upstanding and capable people leave, but the ones who remain become increasingly obsessed with watching internal plots and cover-ups and devote energies to making sure they are on the right side of them, as opposed to doing their jobs.”

It can be debated whether the “upstanding and capable” part applies, but the latter reasons are why I left. It was all palace intrigue all the time. Soul-crushing. I became willing to gnaw through my wrists to escape the bronze-handcuff pension of the “flagship, destination employer.”

as a public employee hoping to get out before CalPERS falls over, bringing stuff like this up with HR is invariably met with head patting and condescending denials.

“CalPERS is too big to fail, you rube. stop getting the others wound up”

lots of recruitment efforts invested in these deceits as well.

Thanks for sticking it out as long as you could, better days may come.for you service. The perfidy is so deep, but better days could come.

Thanks for you service. The perfidy is so deep, but better days could come.

OK, so how to fix this. Would require several somebodies with forensic chops, investment chops, pension chops, HR chops, what else? Yves, of course, would be da bomb, but she is busy-busy, so I hesitate here, but would cheer wildly if she could. Is Bill Black available? Brooksley Born (born 1940) probably retired, but couldn’t hurt to ask. Who else would you put on your fantasy internal audit team? Nomi Prins? Chris Tobe of Kentucky Retirement Systems? Margaret Brown? JJ Jelincek? The last two know the territory, but there are insiders who may know even more. Yves has a contact at KES who would be very, knowledgeable, perhaps Mr. Tobe, but somebody there who is trustworthy. Hubert Horan? Again, probably busy, but could ask. I can only give $$, but where do I sign up?

Let the Games Begin.

Commenters may wish to tone-down the triumphalism. The reality is that after the brain-drain of the last few years, it will be a challenge to find someone with adequate qualifications willing to work for the incompetent and captive Board of Administration that is the rotting head of this fish.

There is also the taint of a potential RICO and/or Honest Services Mail Fraud that lurks in the background, as pointed-out by Vlade. Who would voluntarily walk into that spinning buzz-saw? Who are the executives and the Board captive to? What political influencers have graduated from mere skimming of retirees’ savings to lopping-off huge chunks of their flesh?

Three little words: Follow the Money…

David thank you for your comment and articulating the challenges that face CalPERS ahead. At the end of the day, we all just want our retirement pensions and clearly you are thinking not just months down the road, but years too. I also applaud and commend you for your countless public comments in front of the CalPERS Board. I speculate days go into your research and prep work. I think our fellow pensioners should recognize your hard work because it is not just 3 minutes of your time.

Yves, thank you as well for your insurmountable effort protecting us pensioners.

We all appreciate you both!!