CalPERS’ Chief Investment Officer Ben Meng has filed demonstrably false financial disclosure documents, flouting the requirements of the California Fair Political Practices Commission. As a result, not only has Meng committed perjury, but CalPERS’ failure to review or require Meng to correct these documents points to a major compliance failure, since CalPERS has, or should have, records that would show that Meng’s financial disclosures were incomplete.1 Recall that this lapse follows CalPERS having had a huge spike in personal trading violations, which it has yet to explain adequately, let alone describe what it will do to prevent abuses like that from recurring. Poor controls are a disaster in the making for a financial institution, as the Wells Fargo fake account train wreck illustrates.

To make this sorry situation worse, CalPERS delayed releasing the Forms 700s until it became clear they’d be published regardless, suggesting that they were fully aware of this and potentially other lapses, yet refused to correct them.2

As we will also discuss, even the properly completed sections of Meng’s forms raise concerns, since they show that he has financial conflicts of interest with respect to private equity and has had an appetite for highly speculative instruments. The latter worrisomely may explain Meng’s appetite for risk now. Readers may recall that CalPERS has announced, with great fanfare, its plan to meet its 7% return target. It amounts to putting the available casino chips on the “more risk” numbers and then borrowing from the house to buy more chips to increase the size of the wager.3

Finally, this abuse by CalPERS top investment executive occurred just as CalPERS has been successfully moving forward legislation, AB 2473, to have its private debt investments, an area it intends to expand, exempt from Public Records Act disclosure. That means Meng could approve private debt deals that would benefit him or other CalPERS executives and the public would have no way of knowing. This bill has not yet gotten all the way through the legislature, so it is still possible it could be held back for badly-needed further review.

Background: The Importance and Legal Status of the Financial Disclosure Form 700

Under Marcie Frost, CalPERS consistently failed to comply with its own transparency policy, which is to publish promptly all of the the personal financial disclosure forms known as Form 700 filed by board members and executives annually with the Fair Political Practices Commission. Form 700s are required of all public officials to show investments in their jurisdiction so as to present potential conflicts of interest.

These are public records whether or not CalPERS posts them on its website as required by its own policy. The fact that CalPERS started foot dragging, posting them only after getting complaints, is a departure from its practice under previous CEOs. Needless to say, it creates the appearance that CalPERS was hiding something, meaning trying to protect an executive or board member.

That concern looks to be well founded. After getting inquiries as well as a Public Records Act request from your humble blogger, CalPERS eventually put the 2019 Forms 700 on its site. As we will explain, the Forms 700 by Chief Investment Officer Ben Meng as of when he assumed office and for the full year 2019 taken together show that Meng has made many false statements. This means he has engaged in a felony. As you can see on first page of the Form 700, the respondent avows (emphasis original):

I have used all reasonable diligence in preparing this statement. I have reviewed this statement and to the best of my knowledge the information contained herein and in any attached schedules is true and complete.

I acknowledge this is a public document. I certify under penalty of perjury under the laws of the State of California that the foregoing is true and correct.

Perjury is a felony in California. And Meng has no excuse that he does know how to fill out this document. First, he was a Form 700 filer during his previous stint at CalPERS. Second, CalPERS staff sends multiple e-mails to Form 700 filers offering to help if they have any questions.

This false declaration does not merely reflect poorly on Meng’s integrity and competence. The forms also show that Meng has investments in private equity funds Ares (one of the five involved in the Fred Buenrostro bribery scandal), Blackstone, and Carlyle. As we will document shortly, CalPERS has made significant investments in Blackstone and Carlyle funds, raising the question of whether Meng recused himself (we have put in a Public Records Act request that should provide an answer) But first, let us explain why Meng’s forms are false declarations.

Meng’s Felonious Forms

We have embedded Meng’s Form 700 filings at the end of this post. Note that the first one, dated January 31 2019, is as of Meng assuming office on January 2, 2019. This document is meant to show all relevant financial holdings on that date; the filers is not required to provide any history of his investments. You will see filers are not required to provide the exact dollar amounts of their positions, merely the size category each falls in.

The annual form requires more information. Filers are required to list the name of any assets they held during the year if the position is worth more than $2000 at any point in the year, not just at year end. If they disposed of an asset, they must list the date of sale. If they bought and sold an asset during the the year, they are required to list that and provide the date of purchase and/or sale.

If you compare the two forms, you can see on Meng’s initial Form 700, under Schedule A-1, which is “Stocks, Bonds, and Other Investments” Meng lists 46 holdings as of January 2, 2019. His form for the full year shows only 22 holdings. As we show below, Meng disposed of at least 23 positions without providing the date of sale as required.

And Meng can’t pretend that he didn’t understand that he was to list any security he held during the year and provide the sale date, since he did so with one investment:4

Note also that Meng more often than not refers to the same investment differently across the two forms, impeding comparison. For instance, Ares Capital is “ARCC CAPITAL CORP. (ARCC)” in Meng’s initial filing and “Ares Capital Corp” in his 2019 annual filing; “Open Joint Stock Company Gazprom (OGZPY)” in the initial filing becomes “PJSC Gazprom” in the annual. And Meng did not use ticker symbols consistently even in his initial filing, witness “Johnson & Johnson” in Meng’s initial filing.

Meng also has two entries for GLD in his initial filing, one as “SPDR GOLD SHARES (GLD),” at the top of page 7 of the pdf, and “SPDR GOLD TR GOLD SHS (GLD)” at the bottom of page 8. Are these listed separately, with different names despite the same ticker because they are held at different brokerage firms? If so, does CalPERS have access to both sets of records? And do these apparently separate holdings add up to more than $100,000, which would have required them to show that higher total? As you will see in the tally below, this is not Meng’s only duplicate item.

Anyone in finance will tell you that this level of sloppiness is troubling. An error as minor as the omission of a period in the name of a secured loan in a contract can vitiate the security interest in that loan.5 More generally, financial services professionals fetishize the consistent use of legal names (or defined terms as substitutes) for among other reasons, accurate entry in databases to prevent back office errors, particularly in trades.6

Here are the names of the securities in Meng’s initial filing that are missing in his 2019 annual filing. If you take the trouble to go through them, some of the initial filing names were two different securities name variants but with the same ticker symbol. The difference in names suggests Meng held the same security when he joined in two different accounts. This raises the question as to whether he failed to aggregate the total, creating a misleading impression (i.e., that he owned less than $100,000 in GLD when he in fact held more). In all cases where Meng showed two holdings of the same security at the start of 2019, he had either apparently sold it or corrected his reporting to show it as a single position in his full year 2019 filing.

Here are the securities that were on Meng’s start of 2019 report that disappeared entirely from his account for the full year:

Agriculture Bank of China (ACGBY)

Alcatel Lucent Sponsored Adr.

Cesca Therapeutics Inc.

China Construction Bank (CICHY)

CMS Energy Corp (CMS)

Fidelity California Municipal Fund (FCFXX)

Fidelity Cash Reserves (FDRXX)

General Electric Company (GE)

Industrial & Comm. Bank of China Ltd. (IDCBY)

IPATH SP 500 VIX SHORT TERM (vxx)

ISHARE TRUST MSCI EMERGING MARKETS FUND (EEM) (listed twice)

iShares MSCI Emerging Markets Index (EEM)

iShares MSCI Europe Financials ETF (EUFN)

iShares Select Dividend (DVY)

PDR INDEX SHS FDS EURO STOXX 50 ETF (FEZ) (listed twice)

ProShares UltraShort Barclays 20+ Yr Treasury (TBT)

Sonic Foundry

SPDR EURO STOXX 50 ETF (FEZ)

SPDR GOLD TR GOLD SHS (GLD)7

SPDR S&P Homebuilders (XHB)

Vicor Technologies, Inc.

So 23 positions listed on Meng’s initial Form 700, 21 representing separate securities, 2 as either a duplicate listing or a separate position in the same instrument, vanished when their disposition was required by law to have been accounted.8

Here are the companies with two entries with the same ticker, which appeared as only one (yet again different) name for the full year 2019. We show the ticker when listed and then the name presented in the full year 2019 report:

(CMAKY) China Mingsheng Bank

(SNP) China Petroleum & Chemical Corp

(FXI) iShares China Large-Cap ETF

And some telling details: Meng’s initial Form 700 shows two highly speculative, as in day-trader-level speculative positions: the ProShares UltraShort Barclays 20+ Yr Treasury (TBT) and IPATH SP 500 VIX SHORT TERM (vxx). Both securities get the equivalent of investor black box warning. As this video explains, a levered ETF is suitable only for intra-day trading due to its high level of volatility drag. See here for another discussion. In keeping, the Barclays description of the instrument flag that the 2x feature only works for a single day:

ProShares’ returns over periods other than one day will likely differ in amount and possibly direction from the target return for the same period. These effects may be more pronounced in funds with larger or inverse multiples and in funds with volatile benchmarks.

The VIX ETF also has volatility drag, albeit not as severe. The point is that these instruments make sense only in very limited circumstances, and tend to be used/overused by individuals who love trading action. Their inclusion in Meng’s portfolio are deeply troubling signs that of an appetite for risk for adrenaline’s sake.

Meng’s Private Equity Conflict of Interest

Meng holds positions in three private equity fund managers: Ares, Blackstone, and Carlyle, despite or maybe because the industry has continued to extract high fees even as net results to investors like CalPERS continues to fall. CalPERS lost 5.1% in private equity last year, worse than the SP 500 and worse than CalPERS’ own public equity portfolio. No less than the Financial Times has decried the industry’s fee grifting as “the real ‘Money Heist'”.

These investments create a general conflict of interest against Meng building up capabilities in house to make private equity investments in house to cut out fees and costs that CalPERS has estimated at 7% per year. That is the course of action recommended by CalPERS’ own private equity expert, Dr. Ashby Monk, as well as others.

But if CalPERS were to announce such a move, it would have as dramatic an impact as former CIO Ted Eliopoulos’ 2014 decision to get CalPERS out of hedge funds. This legitimated and accelerated an exit that was already under way.

In other words, Meng has put himself in and continues to remain in a position where doing the right thing by beneficiaries would hurt his personal balance sheet.

CalPERS has also made large commitments to Blackstone and Carlyle funds since Meng became Chief Investment Officer. We have put in a Public Records Act request to obtain records of Meng’s recusals. Since recusals have to be documented to have legal force, failure of or refusal by CalPERS to provide evidence that Meng had recused himself would be compelling evidence that Meng had failed to do so.

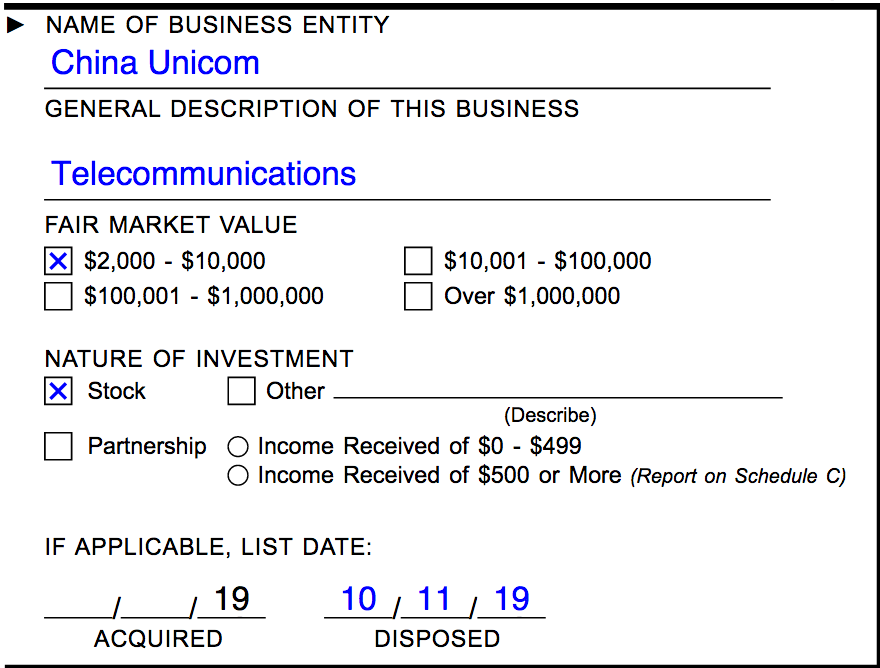

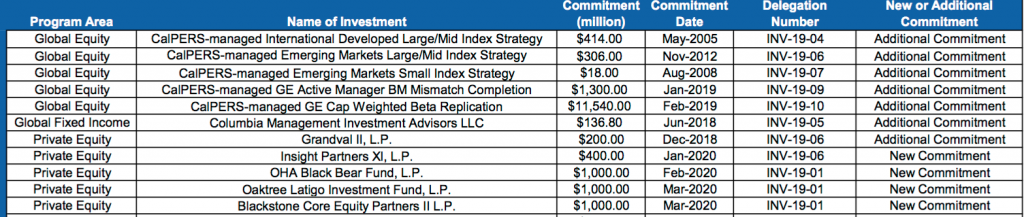

Recall that Meng joined at the start of January 2019. See this entry from CalPERS’ Private Equity Program Fund Performance Review:

![]()

The relevant columns are the two just to the right of the name. 2019 is the “vintage year” meaning when fund closed. $328,239,616 is the size of CalPERS’ commitment.

CalPERS under Meng also committed $1 billion to Blackstone this year, as you can see on page 2 of this June 2020 presentation for the quarter ended March 31, 2020:

CalPERS “Trust Us” Private Debt Bill

CalPERS is sponsoring Assembly Bill 2473 (Cooper), changing current law to exempt “Private Loans” made by a “Public Investment Fund” from the California Public Records Act (CPRA). The bill is currently before the Senate Committee on Labor, Public Employment, and Retirement. These “Private Loans” are a new and untested investment strategy which has not been commonly used for the investment of money held in trust to fund public pension obligations. These loans only have the potential to yield high interest if they are made to borrowers with a high risk of default — or even bankruptcy.

This bill was pitched by CalPERS staff as the only way that they can hit their 7-percent return target, but it contains sweeping secrecy provisions far beyond what might be seen as necessary to negotiate “Private Loan” deals. People are starting to wake-up and smell the coffee about CalPERS placing assets at risk by using leverage to engage in speculation.

Pasadena City Manager Steve Mermell recently told Pasadena Now that he and the Pasadena City Council are opposed to the strategy now that they’ve seen the details:

I am concerned that in its efforts to achieve greater returns, CalPERS is taking on additional risk, by shifting more investments to private equity and more alarmingly, borrowing money to invest,” Mermell told Pasadena Now. “While the strategy may get results, just like gambling, the downside risks are too great and it’s the taxpayer that will end up footing the bill.

Assemblymember Marc Levine (D-Marin) cast the sole vote opposing AB 2473. Assemblymember Levine went on the record with Ben Christoper of CalMatters, frankly stating:

It’s hypocritical for Democrats in the Legislature to allow CalPERS to hide the critical information about investments and investors while seeking disclosure from the president on his investments. Can you look more dopey than that?

History also shows that these officials are right to be worried. CalPERS has pitched its bill as necessary for it to be able to get into banking. In the early 20th century, most states set up private banks for similar purposes. They all turned into cesspools of corruption. The only one that remains, North Dakota’s private bank, is not a direct lender but a banker’s bank, buying participations of in-state loans that it deems prudent.

Finally, it’s cheeky for CalPERS to act as if it needs extra protection from Public Records Act inquires when it already routinely flouts the law. For instance, CalPERS has refused to provide copies of the resignation letters of recent high-level departures that are widely believed to have been forced out: Elisabeth Bourqui, Ron Legnado, and Paul Mouchakka. The First Amendment Coalition explains how case law makes these missives public records save for very limited, truly personal information, which would in most cases at most require that part of the letter be redacted. CalPERS has also refuse to let board members see these letters. So what is Marcie Frost trying to hide?

Speaking of Marcie Frost, who is responsible for this abject compliance failure? Narrowly, it is Frost. As the CEO, all CalPERS bucks stop at her desk, including whether to keep Meng on as Chief Investment Officer.

Specifically, Marlene Timberlake D’Adamo is the Chief Compliance Officer. Timberlake reports to Frost. Timberlake oversees Personal Trading Policy. Compliance has (or should have) records that showed incompleteness of Meng Form 700; if Compliance have those records, that’s a red alarm event.

But the Board clearly can’t be bothered with compliance or even basic honesty. Longstanding former Board President Rob Feckner, who is still wields disproportionate influence, and his successor, Priya Mathur, both backed the former CEO, now imprisoned felon Fred Buenrostro, up to the end. And neither attempted to explain or apologize for the damage done by their dogged defense. Mathur supported Frost when she held onto flagrant resume fabricator and perjurer Charles Asubonten.

This board has gone even further into dereliction of duty by delegating more investment authority to staff, with no checks and balances, when under the law, the board cannot delegate its responsibility. In particular, Lisa Middleton campaigned for the board even though its schedule conflicted with her board schedule at the Palm Springs city council, so she personally pressed for even less oversight in the form of shorter and less frequent board meetings, with CalPERS staff presenting a schedule that obligingly opened up her conflicted days. Since when is a self-created scheduling conflict more important than protecting CalPERS beneficiaries and taxpayers? Only when it allows CalPERS staff to evade supervision and a capture a board member.

In keeping, Middleton, who is the co-chair of Risk and Audit, even voted against discussing CalPERS audits in closed session. Middleton is so any anti-transparency she does not want the board to discuss CalPERS’ internal audits! No other public agency in the state treat every internal audit as confidential.

But Lisa Middleton is merely General Counsel Matt Jacobs’ cat’s paw. It is Matt Jacobs who has decided that he is in the business of protecting CalPERS executives and board members from embarrassment and accountability, as opposed to executing his sworn duties and protecting beneficiaries and taxpayers.

One of Jacobs’ pet practices it to treat every internal CalPERS document as “attorney client privileged” when dragging a member of the legal department into a discussion does not confer privilege. There are boatloads of precedent showing that privilege exists only when a lawyer is providing legal advice, not when participating in discussions of mere political and business matters. Oh, and when this bad practice become institutionalized? When former CEO Anne Stausboll, herself an attorney and hence knew when Jacobs was way out on a limb legally, retired and was replaced by high school graduate Marcie Frost.9

CalPERS board and executives apparently lack the survival instincts to recognize that they can’t escape accountability for much longer. When Meng’s risky gambles fail to work out, they will be the ones holding the bag. The stunning spectacle of Kentucky’s Republican attorney general Daniel Cameron suing Henry Kravis and Steve Schwarzman, two of the biggest Republican party funders, personally, along with their firms. shows that governments left holding public pension fund empty bags can and will turn on responsible parties. It won’t be long before deeply-in-the-pension-hole states like Illinois and New Jersey start looking hard at suing pension boards and officers, both to collect on their D&O policies and to pressure them to get at misbehaving big fee fund managers on behalf of taxpayers.

Oh, and as we’ve pointed out, the CalPERS D&O policies for board members are legally unenforceable. For board members who aren’t judgement proof to continue to act like potted plants is tantamount to buying personal bankruptcy futures. Not that they don’t deserve it.

_____

1 The Forms 700 are filed with CalPERS, which keeps a copy and forwards the original to the Fair Political Practices Commission.

2 Meng could easily have filed an amended form.

3 This is not an exaggeration, as we explained in detail here: CalPERS Plans to Blow Its Brains Out: Seeks to Increase Risk by Boosting Private Equity, Private Debt, and Leveraging the Entire Fund. CalPERS plans to leverage its entire portfolio and invest more in private equity and add investments in private debt. CalPERS has given inconsistent answers as to how the borrowed funds will be deployed, but it has given the impression that they will go disproportionately to private equity and private debt. Note that other major investors, like German pension funds, use portfolio-level leverage to compensate for not investing in private equity, as to create a higher overall risk level than they can achieve with public securities, and not in addition to private equity and debt investments.

4 The observant may have noticed that Meng’s initial form, as of when he assumed office, did not have the “ACQUIRED” or “DISPOSED” items with the year filled in, while his annual form for 2019 did. That is how the Fair Political Practices blank form reads, with the year supplied, presumably as a reminder that activity prior to the current year does not need to be reported.

5 Not making this up. My lawyer saw this happen in a case by one of her partners. The name in the contract was not the same as the name as in the UCC filings, and the difference really was all of a period. It still meant the parties to the contract were unable to go after the collateral.

6 Treating CalPERS as having financial professionals in its ranks regularly looks like a fact not in evidence.

7 If we are to accept Meng’s filings on their face, as noted above, he had two separate holdings of GLD and disposed of one. Clearly other facts might hold.

8 It is in theory possible that all of these holdings fell so far in value that they were below the $2,000 minimum reporting threshold. Needless to say, that would not speak well of Meng’s investment acumen.

9 There are many accomplished individuals who have graduated only from high school but have sought actively to acquire knowledge and/or technical skills on their own. Frost is not one of them.

00 Ben Meng Form 700 as of Assuming Office00 Ben Meng Form 700 Annual for Calendar 2019

What regulatory agency or law enforcement body investigates these types of issues? Why have they been absent for so long while so many reports have been made public about crooked activities at CalPers? As a California taxpayer, it’s astonishing that this crap continues to occur.

Many thanks to this site for continuing to report on this malfeasance.

The reason things have gotten to this sorry state is that CalPERS is a governance train wreck: a nearly $400 billion pot of money accountable to no one but itself….despite having a former CEO now in the Federal pen for bribery, and having three board members leave under a cloud (one had his term just about over; the one who was in deepest with the crooked CEO Fred Buenrostro had the good fortune to die at age 82 shortly after the scandal broke).

What had kept CalPERS on the straight and narrow despite its poor governance structure was a different culture (less open corruption), CalPERS being prestigious, which attracted high power board members even if some just wanted to be in the limelight (Willy Brown pulled strings to sit on the board) and a big enough core group that actually did the work to keep on top of the considerable amount of information staff provided and was vigilant about supervision and in particular slapping back their regular efforts to take power from the board.

If I have this picture right, it didn’t take much for the efforts to compensate for the deficient governance structure (the board, well, and in extremis, Federal prosecutors, as the only check on staff) to lose steam. Key events were the selection of Buenrostro as CEO, in what I understand was a close vote. Another was the departure of hyper-competent CIO Mark Anson, at least in part because he objected to the board about how he was being pressured by Buenrostro to make certain investments (recall then that the CIO reported to the board, not the CEO, so it was legitimate for Anson to go to the board). The CEO lobbying for particular investment picks is a monster red flag and should have led to an immediate investigation. Instead Anson was rebuffed and left not long later.

There are chapters I am skipping but that gives you a flavor.

CalPERS learned all the wrong lessons after the Buenrostro prosecution. Rather than going for good oversight and transparency, the board decided to act as if being ignorant would save them (legally that is all wet) and acting as if managing the press will solve all problems, hence extreme secrecy is a good thing.

Haven’t heard Anson mentioned in a long time. That was what, 2007? IMO he’s the 2nd or 3rd most competent person I know who didn’t play dirty politics and made it to the top.

The worst is he applied for the CIO post in 2018 and CalPERS picked Meng over him.

If it is a felony, who can sue? Marcie’s declarations were felony too, and no-one seeemed to have bothered.

On Ming’s using the leveraged ETFs – there’s another explanation. That’s he’s clueless. Which, TBH, is even worse..

What I don’t get is that in a normal institution, a form like this would be done by the HR based on the trading records provided by the person in question, on their behalf. I believe it’s technically to get a double lock on them – because if they provide the employer with the wrong information, it would not be only an internal affair anymore, but perjury. And any requirements to “adjust” this would have to be explained.

But that of course pressuposes internal controls, which we know what Marcie thinks of.

Yes, the problem is it would have to be a prosecutor…which means the Attorney General or say a county prosecutor for a county which has employees as CalPERS beneficiaries. However, these routine-ness of flagrant abuses could also be used as evidence in private litigation.

However, bear in mind Form 700 filing are taken very seriously by California officials, both state and local level. This sort of thing will register with a lot of players, particularly members of the legislature. And the legislature is one of the few things CalPERS fears.

which means the Attorney General or say a county prosecutor for a county

Would we be talking Kamala Harris at any point?

This is a really bad look for MF. Either she didn’t review Meng’s Form 700s or she did review them but was not competent to notice the problems in the filings. Perhaps this will call into question how competent she is to evaluate the performance of the other CALPERS principals who report to her, and perhaps finally move the Board to belatedly examine how qualified she actually is to be in charge.

Again, well done, Yves!

This is the thing that amazes me – like most people at some stage in my career I’ve had to sign personal disclosure forms – simple ones in my case as I don’t have much in the way of personal investments – but they are treated very seriously right through the organisations I’ve been with precisely because of the potential for liability and/or public embarrassment if they turn out to be wrong, even if its a genuine error. I’ve always been told to err on the side of caution, listing things even if they aren’t strictly speaking required. This is just common sense and standard good practice.

It hardly needs stating of course, but ordinary mid level employees of Callipers can’t be unaware that they have a CEO who is not competent and a CIO who is reckless and possibly conflicted, with (seemingly) nobody in a senior position willing or able to call them out. I’ve been in that situation in the past, the impact on day to day work can be quite dramatic. If the people at the top are clearly looking after their own skins as their sole priority, then everyone else will do the same thing. Work quality (and integrity) gets thrown out the window with remarkable speed. Quality employees spend all day brushing up their resumes for an exit, the others fight among themselves for scraps from above. Those near the end of their careers just shrug and keep their head down and plot an early retirement. For a pension fund that is potentially disastrous. Who knows what sort of lousy locked in decisions are being made on a daily basis.

Trying to get the view from 20,000 feet here as the details are as obvious as they are murky. It has not escaped my notice that when things start to fall apart for CalPERS that there is one obvious fall-guy here and that is Meng. Well, maybe not fall-guy as such as they are presumed innocent of crimes that they have been accused of. And things will fall apart for CalPERS as nothing goes on forever – nothing. CalPERS are aiming on a 7% growth and barely nudged the meter at 4% so the clock is already ticking on this organization. So why Meng? Consider the following.

Someone is going to have to be fitted up for an orange jump suit and it sure won’t be Frost if she can help it nor any of the Board. The Staff will all swear that they were just following the directions of the Board itself and they are as innocent as the Vestal Virgins. Meng is new on the scene so probably does not have a deep bench of allies yet. Washington has already been gunning for him because of his China stint so they would let him swing in the wind if not supply the rope itself. No, the outlook does not look good at all here.

Governor Gavin Newsom will want to put the scandal when blows up quickly behind him before it engulfs his government because of its lack of action in preventing this. So a sacrifice will be needed. And just wait till the Californian taxpayers get the bill for bailing out CalPERS and the howls start. Someone will have to be shown on TV being frogmarched in handcuffs out of CalPERS Headquarters. Guaranteed too that a Trump government will refuse to bail them out and maybe not a Biden government either so somebody will have to be the bunny. No, Meng is the perfect guy to be chosen.

In just the details that has been presented here in this article, there is enough for any decent trial lawyer to hang him out to dry. So why does he double down so much? Is he stupid as well as reckless? I am guessing that he is simply following that old adage that you may as well hang for a sheep as a lamb. So let the good times roll – while they last. But if I were him, I would make sure that there is a private plane kept warmed up at Sacramento International Airport.

Meng is new on the scene so probably does not have a deep bench of allies yet.

Meng is constantly networking with politicos, which explains why Meng got and holds the CIO role as he is compliant in returning the favors through investments in the favored general partners

Has Meng been at CALPERS long enough to be implicated in its underperformance? He’s quite new. But if he is being sacrificed to save other people, that suggests that the “other people” are getting scared, which is a hopeful sign. Writing on the wall.

“China Unicorn”? Really?

“Meng holds positions in three private equity fund managers: Ares, Blackstone, and Carlyle, despite or maybe because the industry has continued to extract high fees even as net results to investors like CalPERS continues to fall.”

“These investments create a general conflict of interest against Meng building up capabilities in house to make private equity investments in house to cut out fees and costs that CalPERS has estimated at 7% per year. That is the course of action recommended by CalPERS’ own private equity expert, Dr. Ashby Monk, as well as others.”

“CalPERS has also made large commitments to Blackstone and Carlyle funds since Meng became Chief Investment Officer.”

As a CA taxpayer, this is upsetting. Meng ownership of private equity firms — Ares, BlackStone and Carlyle — is a clear and gross violation of conflicts of interest. By forcing out senior staff and centralizing decision making at CalPERS, one person, Ben (Yu) Meng is the one and only person deciding how much CalPERS (CA taxpayer) dollars are invested in the same companies that he personally owns.

Yves how can these violations happen? What is the CEO / Chief Counsel / Chief Compliance officer doing to stop this gross abuse and violation of conflict of interest and further loss of public trust? Is there someone I can email?

Ben Meng forfeited CalPERS a $1 billion dollar payout earlier this year.

https://www.bnnbloomberg.ca/calpers-forfeited-a-1-billion-payday-by-scrapping-market-hedge-1.1419987

Meng now fails to disclose major security positions he owns on his required financial conflicts of interest form.

Wow. He’s not just dim, he’s corrupt, too, by all appearances. What a deal for CalPERS. Marcie can sure pick winners. /s

Thanks for your continued reporting on CalPERS, PE, and pensions.

Attorney General Becerra is gonna be all over this like white on rice!

Real soon.

Trust me, I’m a Realtor.

Ms Smith, thank you for your tenacity. Smells like there is blood in the water.

Well, as I see this, he is not the only one to have filed false form 700’s. Henry Jones, Board president and Theresa Taylor, Board Vice President have also committed perjury filing false forms.

No corrective action has been taken as was done with Mathur when she filed false form.

Mr Jones was heard saying at a board meeting that if the board moves responsibility to staff the board members cannot be sued. You’d think the really highly compensated attorney would set him straight.

The changing of meetings to accommodate 1 member who sits on a city board was ridiculous. If you can’t participate then don’t run! I suspect it had something to do with diversity needs. What is even more ridiculous is the request was accommodated.

The legitimizing of hiding transactions by the legislature is also telling.

CalPERS is subject to the Bagley-Keene act and the legislative body deliberating this must be reminded that this is for a reason, to keep them honest with the retirement fund which is very tempting to bad actors.

Someone needs to file charges to make this stop, I propose our cities, counties and public agencies get on top of this.

California is a Banana Republic.

I once filed a Bagley-Keene complaint against CalPERS with Attorney General Kamala Harris. The AG’s Office at that time published the relevant materials and had a portal on their website for complaints. I was contacted by a representative of the office and was informed that AG Harris had determined that the office would no longer enforce violations of the open meeting law, as she had decided that her role was defending state agencies (contrary to Article V of the state constitution). I was directed to the State Auditor, whose staff counsel informed me that while the violation appeared to have merit, the State Auditor lacked enforcement authority. The staff attorney then confided that he was a CalPERS member and that I should file a civil suit to enforce the law.

Harris’ successor Xavier Basura, a Clintonite hack whose law license had been on inactive status for nearly two decades, wiped the Bagley-Keene portal from the Attorney General’s website. The “Attorney General’s Guide to the Bagley-Keene Open Meetings Law” was given a new title page listing the State Auditor (although the content is unchanged). When Naked Capitalism exposed CalPERS for engaging in a multi-million dollar copyright violation against Dow Jones, NYT, and LAT, Basura stepped-in as CalPERS “public defender,” even though the agency spends tens of millions on in-house and outside counsel.

Follow the money…

Prosecution of Criminal Activity By State Agencies

All this points out to a serious conflict of interest in how the State AG office functions. Which is doing a great disservice to the public at large and even to those working at the very agencies they purport to defend. Crriminal activity requires prosecution, not more special protection.

Because while the public in general believes that the AG office works as a Prosecutor would (except at the state level), in reality they serve more like a city attorney does: Representing the financial interests of the state or government organization.

That is the reality. And, yet,. I agree with David: there is no need, particularly when each and every state agency has their own inhouse counsel, not to mention frequently spending millions on outside legal services.

Ben (Yu) Meng personally owns stakes in the same three private equity general partners that he decides to invest CalPERS money. This is a blatant conflict of interest, and a blatant violation of the agreement signed by CalPERS investment staff.

Given how CalPERS operates and the lack of oversight, the best case is some media cover this case, public furor leads Meng to sell shares in these three companies, and then the CalPERS Ministry of Truth goes into overdrive to say based its rigorous vigilence, Meng has corrected the previous minor inadvertent oversight, so all is well.

CalPERS is a cesspool of bile. Marcie, Ben (Yu) Meng, and several Board members have no regard for ethical norms or conduct. They focus only on maintaining and expanding their power by managing perceptions, which is more difficult given Yves reporting, but with over 50 staff in their Ministry of Truth working to spread lies and with their lucrative contracts given to leading legal and PR firms, CalPERS has always been able to control the narrative, despite their constant dishonesty and corruption. Where are the checks and balances? They don’t exist.

Don’t forget about Matt Jacobs’s culpability as the General Counsel who condones it all. IIRC he was brought in during the bribery scandal and served more to cover butt than clean up.

That, combined with him hailing from Wilson-Sonsini, white shoe lawyers to the tech scene, makes me fear he is fine supporting an environment where pensions support as much frothy tech-garbage investment as possible with no regard for how those investments impact the long term welfare of their beneficiaries.

On the bright side (from a purely sarcastic/financial side), any investments we Californian’s had in frackers’s worthless junk bonds have been rescued at full face value by the Fed. It is an excellent demonstration of the validity of MMT, applied in the worst way possible. Sigh.

Pensions are a good issue to talk about when bridging gaps with people who may not agree with you on much else. Deflecting a prevalent narrative against public employees (while noting problems with ‘pension padding’ and ‘double dipping’) to criticism of ‘Wall st.’ investments leads to envisioning how investments can be made to benefit society and provide the resources (not the money) needed for people to use when retired. And in California, if it helps your standing in a conversation, you can blame Democrats!

Please bug your reps anyway.

Jacobs hails from DLA-Piper, where he was a white-collar criminal defense specialist trading in Get-Out-of-Jail-Free cards for the Too Big to Jail crowd, following a brief stint currying relationships at the US DOJ for the Eastern District of California.

Not Wilson-Sonsini.

As Dave knows, Larry Sonsini was CalPERS’ counsel for a bit, when they were trying to launch that “private equity new business model” scheme.

Jacobs didn’t do a “brief stint” at the DoJ. LinkedIn says he was there nearly 10 years.

In 2020 Q2, Yu Meng decided and CalPERS committed $1 billion to Blackstone Core Equity Partners II LP.

(https://www.wsj.com/articles/californias-biggest-public-pension-commits-1-billion-to-blackstone-fund-11591741033)

Of course Meng’s large personal holding of Blackstone had no influence on this decision.

That is in the post, in the last table, in the final line. Of course CalPERS puts important tables like that in microtype to discourage anyone, particularly the board, from reading them.

I do love, however, that that the Journal, which has no dog in this fight, depicts the investment as firming up CalPERS relationship with Blackstone as the opening line of its story. .

Yu Meng’s form 700 states that while he was employed at SAFE, the China Admin of Foreign Exchange, that Meng was also a Teacher at the Schwarzman College at Tsinghua University, a side gig for which Meng reported receiving from $10,000 to $100,000 per year.

Steve Schwarzman, the Blackstone CEO, funded this study program in China that paid Meng while Meng was working for the Chinese government. Then Meng secures the CalPERS CIO position, personally owns a stake in Blackstone, while at the same time Meng directs CalPERS to invest billions of CalPERS capital in Blackstone.

These are all verifiable facts. Does this strike anyone else as improper governance? Did Meng even purchase the stakes in these private equity companies with his own money or did the companies give Meng the ownership as an expression of appreciation?

The CalPERS website https://www.calpers.ca.gov/page/about/organization/transparency-accountability, section “Travel Information and Costs”, 2019-20, lists the partial costs of many Meng trips. For one trip, Meng flew to Tokyo to attend a climate conference for which CalPERS paid over $20,700 total, and CalPERS paid $17,353.95 for the airplane ride.

Yes, CA taxpayers paid over $17,000 for just one of Meng’s round trip flights.

Where is the oversight? As CA taxpayers do we just shrug our shoulders and say well that’s the way it is? Where is the accountability?

Meng, Yu (Ben)

Chief Investment Officer

10/05/19-10/11/19

Tokyo, Japan

Stakeholder Meeting/Event: Inaugural Task Force on Climate-related Financial Disclosures Summit; Green Innovation Summit; Due Diligence Meeting

17,353.95

400.35

2,437.90

520.50

–

–

20,712.70

dividing the $17,353.95 paid by CalPERS for Meng’s adventure to Tokyo by the distance, 5,144 miles, gives $3.37 per mile. I can not find a flight on a travel web site that is this expensive — was this trip on a private jet?

also how much carbon dioxide did this trip spew into the atmosphere so that Meng could attend a conference to talk about climate change?

I can’t wait for Yves to take down the CA Lottery. Takes in billions, pays out millions, where does the money go? It’s supposed to go to public education. Wouldn’t know that from the sorry state of CA schools.

I worked with Ben Meng at Barclays Global Investors. He is the get-ahead-at-all-costs type.

I remember him misrepresenting himself as portfolio manager in email signatures despite officially holding the title of research officer per company org chart.

And he spends a significant amount of time networking within the company instead of contributing trading strategies.

State worker vesting this month with CalPers at my 5th year. Everything I’ve learned since being on the civil service side, public perspective of CA governance is greater than the reality.

Our state government is so big, our gaps may be smaller but the number of gaps comparatively is exponential. I’d be curious if/when we surpass the number of federally employed citizens, as inevitably the pension has ties to employment variance. It appears to be pretty close comparison to date in a quick search.

Incredible content and discussion. Keep up that badass investigatory skills Yves!