Lambert here: “[A] scenario that seems empirically relevant,” from the introduction, is dry. Very dry.

By Gauti Eggertsson, Professor of Economics, Brown University, Sergey Egiev, PhD candidate in Economics, Brown University, Alessandro Lin, Josef Platzer, PhD candidate in Economics, Brown University, Luca Riva, Ph.D. Candidate in Economics, Brown University. Originally published at VoxEU.

The Federal Reserve has recently announced a new policy strategy of average inflation targeting. The column argues that while this is unambiguously a positive step, it may not – under all circumstances – subscribe to a sufficiently aggressive make-up strategy when the zero lower bound is binding. This is particularly likely to be the case if episodes of high unemployment are not associated with material fall in inflation, a scenario that seems empirically relevant. The authors suggest alternatives that could do better, such as a targeting rule that treats the dual objective of the Federal Reserve in a symmetric way, or one that aims at minimising cumulative deviation of nominal GDP from trend.

During his recent speech at the annual Jackson Hole Economic Symposium organised by the Federal Reserve Bank of Kansas City, Federal Reserve Chairman Jerome Powell unveiled a new policy framework (Powell 2020). The revised strategy represents an important improvement over the existing one. Its most notable feature is the introduction of ‘average inflation targeting’ – the Federal Reserve is now committed to keeping average inflation at 2% over time.

Concretely, this means that if inflation is temporarily below 2% – the Federal Reserve’s target – the central bank commits to letting it mildly overshoot in the future, so that on average inflation evens out at 2%.

The new announcement is a significant departure from the existing policy framework. During the financial crisis of 2007-08, for example, inflation persistently ran below target. However, it was generally assumed – and priced in accordingly by the markets – that the Fed was only aiming at having inflation recover gradually back to its 2% target. To the best of our knowledge, nobody was expecting the central bank to deliberately overshoot its target as the economy started growing again, so that inflation would average 2% over a longer time horizon. Yet, this is exactly what Chairman Powell is proposing as the new rule of the road going forward. The current framework thus resembles much more closely a policy of price-level targeting in the presence of trend inflation, where a deviation of the price level below its trend will be met with vigorous monetary expansions as the price level catches up to the target trend. However, this may require inflation to be temporarily higher than the 2% target. Thus, it resembles closely a targeting rule proposed by Eggertsson and Woodford (2003).

In a recent paper (Eggertsson et al. 2020), we illustrate what this means in practice in the context of the publicly available DSGE model constructed by the Federal Reserve Bank of New York. Our results suggest that had the Fed adopted the new policy framework going into the crisis of 2008 – and had the market formed its expectations accordingly – then the resulting contraction in output would have been 25% smaller relative to trend.

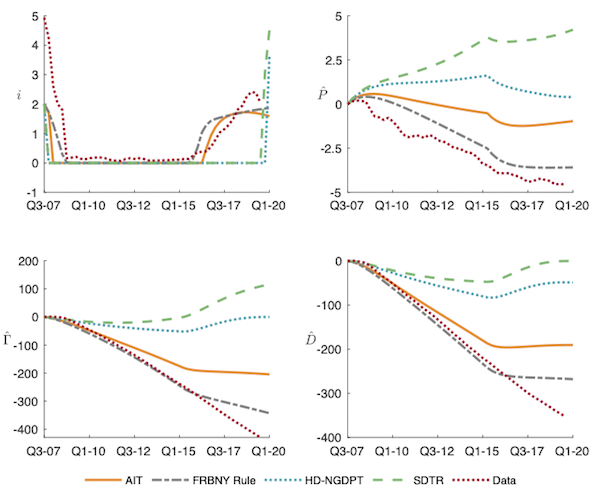

The logic behind the result is simple: inflation – measured by growth in the core-PCE price index – fell modestly below the 2% target during the crisis of 2008. As the economy recovered, however, the Federal Reserve initiated a rate hike before inflation rose above the 2% target in 2015. The Fed only wanted current inflation to hit its target, but had no intention of allowing it to overshoot, so that inflation would have averaged 2% once past misses were taken into account. Had the central bank followed the current policy framework, however, it would not have raised rates as quickly, and would have welcomed a temporary overshoot of inflation. According to our simulations, under this new policy the Fed would not have raised rates in 2015-Q4 as it did at the time, but instead would have waited until the third quarter of 2016, as shown in the top-left panel of Figure 1. Moreover, it would have allowed inflation to overshoot its target by a modest amount, thus ensuring that inflation would have averaged 2% once the recession and recovery period were bundled together. The top-right quadrant of Figure 1 reports the evolution of the price level in deviation from a trend of 2% constant growth in prices. As we can see from the red dots, the Federal Reserve started raising rates before prices were anywhere close to this trend. By contrast, under average inflation targeting (AIT), rates start rising only after the price level approaches trend.

But why does this help? The reason is that markets are forward-looking – during a crisis period like 2008, under the new policy framework private-sector agents would have anticipated an extended monetary policy stimulus as the economy embarked on a recovery. The expectation of a more sustained intervention would have reduced the economic contraction in the first place, much like regular interest rate cuts, which were not available in 2008 once rates had reached zero.

While the new policy framework is certainly an important innovation, it is worth asking: could it be improved further? In our analysis we identify an important limitation: average inflation targeting unsurprisingly only prescribes a make-up strategy based upon inflation falling below its target. This may seem trivial until one realises there is no similar stipulation for the second part of the Fed’s dual mandate, generally believed to be full employment.

Figure 1 Dynamic response to a cost push shock in the FRBNY DSGE model, under different policy strategies

Notes: The top-left panel represents the nominal interest rate. The top-right panel shows the price level. The bottom panels represent targeting criteria for HD-NGDPT (left) and SDTR (right). Monetary policy rules: AIT (solid orange) = Average Inflation Targeting; FRBNY Rule (dash-dot black) = modified Taylor rule from FRBNY DSGE model; HD-NGDPT (dot blue) = History-Dependent Nominal GDP Target; SDTR (dash green) = Symmetric Dual-Objective Targeting Rule; The dotted red line represents the data. The crisis state starts in 2007-Q4 and reverts after 32 quarters. The vertical axes for the top-right panel reports percent deviations from its trend. The vertical axes for the bottom panels report deviations from initial levels (2007-Q3 = 0). The vertical axis for the top-left panel reports annualised percentage points. The horizontal axes shows quarter and calendar year.

Let us explain why this matters by considering the following scenario. Suppose there is a large demand shock that requires a monetary stimulus sizeable enough so that the policy rate collapses to zero, without any room for further cuts. This is precisely the type of scenario that the new framework is designed to guard against. Typically, with a fall in output, there is also a drop in inflation. Despite interest rates collapsing to zero, the new policy framework then (1) signals low interest rates for an extended period, thus compensating for the Fed’s inability to cut rates; and (2) provides a stronger signal the larger the fall in inflation. But imagine now that in addition to a large demand shock – which suppresses output and inflation – there is also a negative supply shock, that adds upward pressure on inflation. Assume that this ‘cost-push’ shock is strong enough to prevent any fall in price growth. In this case, the signal of a future monetary stimulus, usually essential when interest rates hit zero, is choked by the supply shock, even though it may be desperately needed.

With the current Federal Funds rate at zero and record unemployment, there are some indications that the situation described above may correspond to the one the Federal Reserve finds itself in today. Despite all the slack, there has been little downward pressure on inflation; a natural reason for this might be that the economic shock generated by the COVID-19 pandemic corresponds not only to a demand contraction, but also to a simultaneous supply shock. One could even argue that the same applied during the Great Recession, for there was very little fall in inflation at the time despite a significant drop in output and a sharp rise in unemployment (perhaps due to oil supply disruptions around the same time which created upward pressures on prices). As shown in Figure 1, the price level dropped only by about 5% relative to trend. While the simulation results we describe above suggest that the new policy stance would have mitigated the output contraction in the Great Recession by 25%, one question remains: could more have been done?

An alternative policy regime that overcomes the problem introduced above is the Federal Reserve targeting an index that incorporates both elements of its dual mandate – namely, the price level and output. One such index is simply nominal GDP, which is defined as the dollar value of production in the US. Suppose the Federal Reserve were to target average nominal output relative to its trend over time. In this case, if nominal GDP is below trend the Federal Reserve commits to overshooting in the future, so that on average the nominal GDP target is met. If an economic contraction occurs with no drop in inflation, this policy regime prescribes a substantial monetary stimulus at the zero lower bound due to the fall in real output. This makes the strategy more robust than policy frameworks, such as average inflation targeting, that rely on a fall in inflation. In Eggertsson et al. (2020) we call this policy a history-dependent nominal GDP target (HD-NGDPT). Had the Fed adopted a policy regime of this kind in 2008 – and provided it was widely believed by the market – approximately 80% of the contraction in output would have been eliminated. The reason is that this policy would have committed to a substantial monetary easing, prescribing a lift-off from the zero lower bound only in the last quarter of 2019, as show the top-left panel of Figure 1. This is in stark contrast to the newly adopted average inflation targeting of the Federal Reserve, which in our simulations would have started raising rates already in mid-2016. As shown in the bottom-left panel of Figure 1, the reason for this delayed increase in rates is that the threshold for lift-off is not just average inflation, but instead a measure of average deviation of nominal GDP from trend.

In Eggertsson et al. (2020) we also illustrate an alternative policy regime we term the symmetric dual-objective targeting rule. Instead of misses of nominal GDP alone, this strategy points the central bank to shortfalls in inflation and real output.1 If the central bank misses these targets – for example, due to the zero lower bound – it commits to make up for its mistakes in the future, much as average inflation targeting that has now been adopted. According to this policy regime, however, the Fed also takes account of shortfalls in output. This policy regime results in relatively similar outcomes to HD-NGDPT, and is also illustrated in Figure 1.

One attractive feature of average inflation targeting is that is formulated in terms of a widely understood economic object, namely the evolution of inflation. Thus, in order to communicate them the central bank need not state any specific time frame in which the zero lower bound will be binding in the future. Instead, the market will take care of the forecasting job. The same can be said for both policy regimes we introduce above; the only additional feature is the presence of some measure of aggregate activity, but these measures are also generally well understood by markets.

Overall, the new policy regime adopted by the Federal Reserve represents an important improvement relative to the existing framework. What we argue above, however, is that this strategy can be potentially improved even further. Since both our proposals are centred around the additional incorporation of the output-employment mandate of the Federal Reserve, we believe these innovations are squarely within the current dual mandate. Indeed, as we show in Eggertsson et al. (2020), our alternative policy regimes do a better job in achieving the Fed’s dual mandate2 than the current framework.

References available at the original.

Several (many?) members of the FOMC plainly stated that “inflation will not be permitted to approach the target from the upside,” clearly making the 2% “target” actually a ceiling. Sorry, I don’t have links, but they were sometimes quoted at Naked Capitalism.

Core PCE prices in the US exclude food and energy. It measures purchase of goods and services. In a downturn that measurement seems likely to fall. However, prices in my local grocery stores have increased significantly over this summer and into fall. The price of gasoline hasn’t fallen. How can a Core Personal Consumption Expenditure (PCE) exclude food and energy and still have a meaningful measurement of real inflation on Main St.? The inflation measurements have been fiddled by pols for so long it’s hard to know what reality based starting point the Core PCE measures. (Also, keeping real interest rates at near zero is taking money out of savers’ pockets before it can ever be spent on anything.) My 2 cents.

Have you gone through the looking glass? This is Jackson Hole not Laramie. One reaches Jackson Hole on a private jet and the prices of the energy required to get there and food consumed there are of little consequence. Besides, prices of food and energy are notoriously volatile, and although human life as we know it would come to a screeching halt without food and energy it is difficult to fit into the usable economic methodology. Kind of like the relationship of private debt to the study of economics. It is simply not a good fit so it can be studiously ignored. In the meantime, try not to spend too much of your seed capital, and hope that interest rates don’t go negative and they ban paper money. If these guys literally start stealing your money you can’t call the cops.

If these guys literally start stealing your money you can’t call the cops. chuck roast

Individual citizens should be protected* from negative interest to a reasonable degree but, literally, fiat is NOT your money; it’s a public utility that large users/hoarders of it should pay for.

*Which implies that all citizens (at least) be allowed fiat accounts of their own at the Central Bank where they can be shielded from negative interest and fees to reasonable limits.

Got Gold ?

“during a crisis period like 2008, under the new policy framework private-sector agents would have anticipated an extended monetary policy stimulus as the economy embarked on a recovery.”

Maybe I’m a rube, but is that just signalling to the Stock Market….we will never let you fail no matter your choices?

And, if the other main point of the Fed is full employment, are they ever going to “innovate” and quit lying to themselves and everybody else about real unemployment? Or am I being a rube again and everybody knows the are lying to us about real unemployment because employment doesn’t really matter to the asset class?

When the FED says it’s controlling inflation, it means wage inflation, not price inflation. Controlling wage rise and letting price keep rising is best for corporations and for the 1%. When they say that they’re trying to keep inflation below 2%, I have to laugh. Their measurement is flawed anyway and the error is probably +or-50%! I did not fully read the article because it’s kinda long and it has all these graphs which are probably meaningless.

It’s time to get rid of the FED.

Pretty much. Something happened around 1980. Trying to remember what that was. /s

https://www.epi.org/productivity-pay-gap/

It’s such a mystery. Almost like an “invisible hand” is holding down wages for 90% of workers. /s

https://www.epi.org/publication/charting-wage-stagnation/

Inflation is a transferring wealth to the rich. With every 1% of inflation, a guy like Trump, who is $420 million in debt against assets, basically gets subsidised to the tune of $4.2 million annually.

Poor people don’t have much debt because they cannot borrow much in the first place. Yes, perhaps on a credit card at 29.9%, where 1% more or less really doesn’t matter. However their wages get devalued by inflation so they get screwed. They have no wage bargaining power for their wages to keep up with inflation.

That’s why the 1% and central banks are so keen on inflation. Inflation is the single biggest reason why wealth inequality has become so enormous.

Oh, and nowadays prudently saving some of your hard earned cash in order to survive bad times or for your pension is called “cash hoarding”. We certainly don’t want that to happen!

It’s disgusting.

Lenders (the rich) don’t want generalized inflation — that means that they are being paid in dollars that are worth less over time than the dollars they lent out.

Borrowers (the rest of us) want moderate and predictable inflation because we are working stiffs who don’t get returns to capital — we benefit by repaying our loans with dollars that are worth less over time than the ones we borrowed.

Which group do you suppose outnumbers the other?

LOL, love these wonky ivory-tower types getting all wrapped around the axle based on the Holy Fed’s latest “policy framework messaging”. Anything to distract the proles from the fact that the Fed’s actual self-imposed dual mandate has, for at least the last 40ish years, consisted of the following 2 items:

1. Do whatever it takes to keep financial-asset prices increasing exponentially. That includes robbing savers by way of negative real interest rates and printing as many GDP-multiples as needed in order to make the parasitical speculator class whole whenever its own greed causes it to blow itself – often with dire repercussions for the rest of us – up.

2. Do whatever it takes to crush wage inflation, thus keeping labor in a state of ever-worsening precarity and debt serfdom. Elite policymakers in DC and the corporate MSM provide crucial help in this mission by promoting open borders, coups and wars to provide a steady flow of desperate refugees, identity politics to nix any danger of emerging class-solidarity amongst the bottom 90%, and the promotion of debt rebranded positively as “credit” at every turn.

Speaking of providing crucial help in the above, I would be remiss to fail to credit the academic-economics profession, which fits Upton Sinclair’s famous “it’s hard to get someone to understand…” aphorism in terms of “failing to grasp” the above reality. I mean, why risk opening your eyes to the horror you and your ilk have inflicted on the non-useless-eaters when you are well-paid to wax wonkish with your cronies at brunch and spend your days penning immortal prose like “The authors suggest alternatives that could do better, such as a targeting rule that treats the dual objective of the Federal Reserve in a symmetric way, or one that aims at minimising cumulative deviation of nominal GDP from trend”?

The economics of globalisation has always had an Achilles’ heel.

In the US; the 1920s roared with debt based consumption and speculation until it all tipped over into the debt deflation of the Great Depression. No one realised the problems that were building up in the economy as they used an economics that doesn’t look at debt, neoclassical economics.

Not considering private debt is the Achilles’ heel of neoclassical economics.

The FED does the best it can with an economics that doesn’t consider debt, which really isn’t very good at all.

Greenspan and Bernanke can’t see the problems building before 2008.

https://www.youtube.com/watch?v=vAStZJCKmbU&list=PLmtuEaMvhDZZQLxg24CAiFgZYldtoCR-R&index=6

At 18 mins.

(When you use neoclassical economics that doesn’t consider debt, the economy runs on debt and then crashes in a Minsky Moment, 1929 and 2008.)

No one can work out what caused 2008, and afterwards and they attribute it to a “black swan”.

Janet Yellen is not going to be looking at that debt overhang after 2008 and so she can’t work out why inflation isn’t coming back.

It’s called a balance sheet recession Janet, you know, like Japan since 1991.

Jerome Powell is not looking at the debt overhang after 2008 and so thinks the US economy is fixed and raises interest rates.

Raising interest rates with all that debt in the economy will soon cause a downturn and there is no way he will get anywhere near normalising rates.

He soon has to backtrack and reduce rates again.

The FED never stood a chance.