Yves here. This timely piece discusses how owning financial assets leads to conservative views, at least on economic issues. This is consistent with the widely-held belief in policy circles, that homeownership produces more “responsible,” as in property-respecting, citizens.

By Yotam Margalit, Professor, Department of Political Science, Tel Aviv University and

Moses Shayo, Pinchas Sapir Professor of Economics,Hebrew University of Jerusalem. Originally published at VoxEU

The impact of markets on participants’ values and political preferences has long been a contested issue. This column uses a large field experiment to evaluate the effects of engagement in financial markets. Participants from a national sample in England were randomly assigned substantial sums they could invest in stocks or non-financial assets over a six-week period. Results show that investment in stocks led to a more right-leaning outlook on society and economics, including issues like personal responsibility, merit, and the role of luck in economic success. It also increased support for market-friendly policies and less regulation.

Financial markets have made a dramatic leap in prominence throughout the world in recent decades. This is reflected not only in the growing size of the financial sector and its share of national income, but also in the fact that more and more individuals are engaged in the trading of stocks, either directly or via their pension savings. This trend has become even more pronounced during the COVID-19 lockdowns, with people staying at home with no sporting events to watch or bet on. Equity trading at Fidelity, for example, increased by 97% in the third quarter of 2020 from the previous year. This means that more and more people are participating in an activity that is centered on material gains, involves continued consideration of risk taking and risk mitigation, and often evokes strong notions of winners and losers. The economic benefits and risks of financial activity are widely discussed (e.g. Cornelli et al. 2020, Delle Monache et al. 2020, Furceri et al. 2019). In a new study we explore the political implications.

Many thinkers – from Montesquieu and Adam Smith to Marx, Schumpeter, and Albert Hirschman – have recognised the possible social and political repercussions of market activity. However, there is little agreement, and even less systematic evidence, about the nature and direction of the effects. Whereas some attribute to markets’ positive influences, nurturing frugality, moderation, wisdom, order, and responsibility (Montesquieu 1748, McCloskey 2006), others argue that markets commodify social relations, and make people egoistic and instrumental in their treatment of others (Marx and Engels 1848, Polanyi 1957, Sandel 2012).

Similarly, financial activity may affect political views. Recall President George W. Bush’s push to “privatise social security”. Some of his supporters argued that broadening the share of the population who have a stake in the stock market would also lead to the expansion of the ideological Right’s constituency. Yet the notion that exposure to markets – and in particular, financial markets – affects individuals’ social-economic values and policy preferences remains largely speculative.

The main challenge to understanding the impact of financial activity on individual preferences is that such activity is naturally associated with a host of other personal, social, and political factors. For example, people with higher incomes or with greater trust in free markets may be more likely to participate in financial markets. To overcome these challenges, we conducted a field experiment, the results of which are reported in a new study (Margalit and Shayo 2020). The experiment was carried out with a national sample of 2,700 adult residents of England, 60% of whom had never invested in the stock market before. We randomly assigned 1,560 of them to receive substantial monetary sums (£50) that they could repeatedly invest in financial assets over a six-week period. In the weeks before and after the study, we also tracked participants’ social and political attitudes as part of a separate study.

Beyond the main treatment group – which traded in real stocks such as Apple, Rolls Royce, and Siemens – we included a control group and two more asset treatments. These additional treatments varied from the main one in (a) whether the investments were in real or ‘fantasy’ money (i.e. did not involve actual monetary stakes), and (b) whether the investments were in company stocks, or rather in assets unrelated to the local economy – specifically assets indexed to the performance of sports teams in the US. These treatments were designed to help distinguish between different channels of influence. The sports treatment in particular replicated all the features of the trading environment (which could generate, say, excitement or risk taking), except that it did not expose participants to actual stocks.

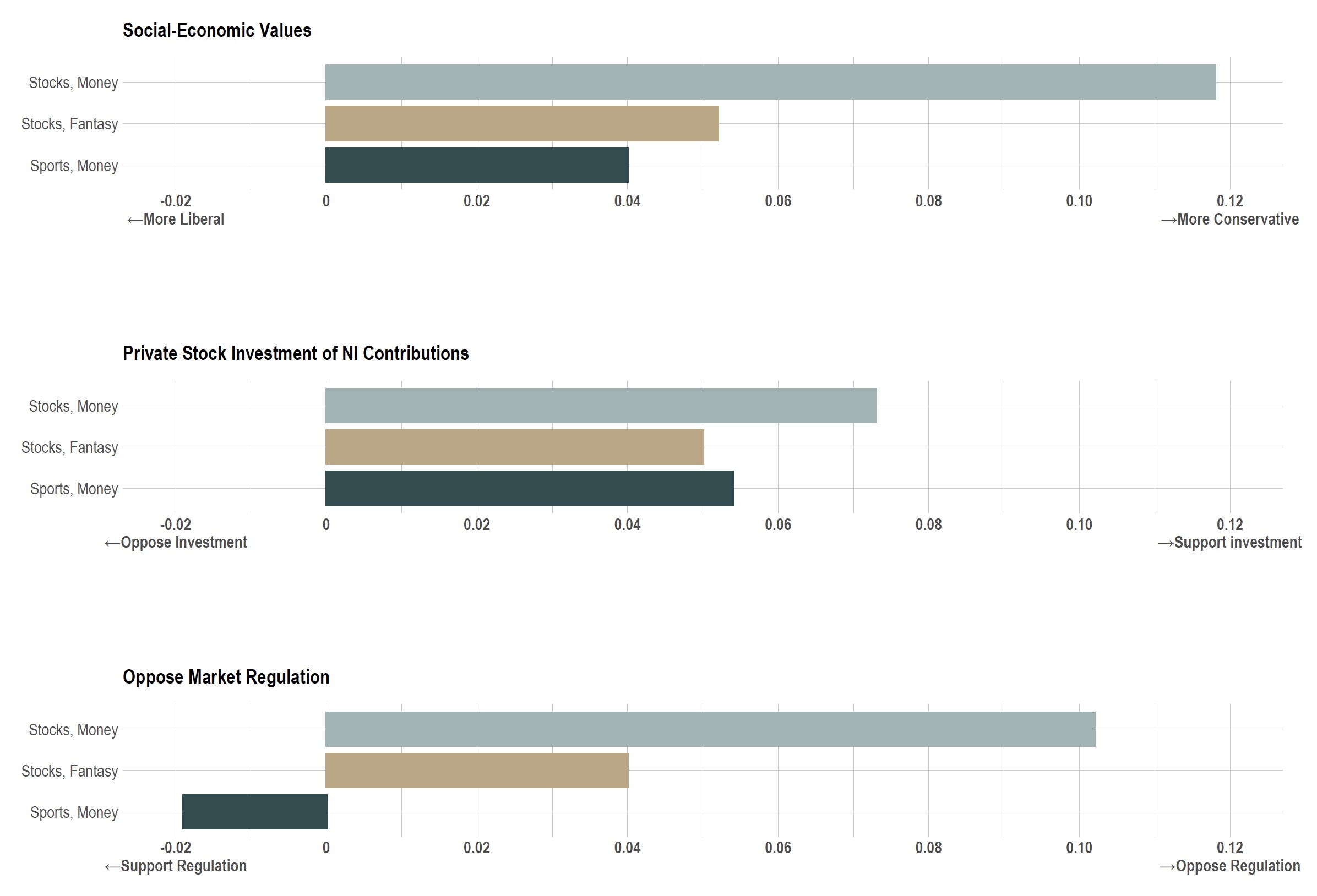

Figure 1

Note: The figures show the estimated treatment effect, after controlling for pre-treatment attitudes and characteristics.

We find that participants assigned to an asset treatment shifted rightward in their social-economic values, i.e. in their attitudes on issues such as economic fairness, inequality and redistribution, and the role of luck in economic success. This shift is illustrated in the top panel of Figure 1, which shows the effect of the three treatments on an index of social-economic values (attitudes on personal versus government responsibility, income inequality and redistribution, and the role of luck in economic success). Overall, exposure to an asset treatment led to a rightward shift in social-economic values equivalent to 9-12% of the gap between Labour and Conservative voters. The treatment effect largely persisted in a follow-up study a year later. These results complement recent findings from an experiment conducted in Israel showing that investing in the stock market moves people to the left on issues of peace negotiations and security (Jha and Shayo 2019).

What drives this effect? One possibility is that investment activity itself – with its focus on material gains, risk taking, winning and losing – triggers emotions and modes of reasoning that influence views on issues beyond traditional market activity. A second possibility is that rather than the investment activity itself, it is engagement with financial markets, and stocks of real-world companies, that influences social-economic values. Investors are exposed to broader aspects of the economy and the workings of markets, including the impact of changes in interest rates, the influence of political events on prices, and the consequences of market regulation. In turn, this may foster a sense of familiarity with, and greater trust in financial markets.

Our results support the second possibility. As seen in Figure 1, the treatment effect on social-economic values is much more pronounced among those assigned to trade in real company stocks with real money. Among subjects in this group, the effect was equivalent to 11-14% of the Labour–Conservative gap. By contrast, the effect was smaller (and statistically insignificant) when investments were in assets tied to the performance of baseball teams rather than in the stock market. We also cannot detect an effect among subjects in the fantasy treatment.

A rightward shift in social-economic values occurred among both left- and right-wing voters but was more pronounced among those on the left. We find little evidence that the change in attitudes was determined by how well participants’ investments performed during the experimental period. The data also allow us to rule out that this attitudinal shift was driven by a deep change in subjects’ tolerance of risk. In contrast we find that exposure to the market increased subjects’ confidence in the ability of regular people to successfully invest in the market, as well as their own inclination to invest. This pro-market shift perhaps accounts for the broader rightward movement in social-economic values.

We also examine attitudes on a range of policy domains (second and third panel in Figure 1). Subjects exposed to the investment treatment, particularly those investing in the stock market with real monetary stakes, moved distinctly rightward in their views on policies related to market regulation and taxation. In contrast, no effect was registered with respect to government spending on unemployment assistance. Most notable was the effect on participants’ views in the policy debate over the privatisation of pension savings. Compared to the control group, we find that, following the experimental treatment, subjects in the real stock treatment were about 7.5 percentage points more likely to support allowing citizens to invest their national insurance (NI) savings in the stock market. This represents a shift of almost 31% above the baseline rate of support.

Overall, these results suggest a rather inconspicuous effect of the growing financial sector on politics, an effect that goes beyond the visible and widely discussed channels of influence, such as large campaign contributions, lobbying activity, or the prominence of Goldman Sachs executives in the US government. By encouraging a pro-market social and political outlook, markets may engender a self-sustaining dynamic whereby their growing reach leads to wider support for their further expansion.

See original post for references

All you need to find this is to browse the discussions on any investment webs. The economic (and political) views there definitely do not represent any reasonable cross-section of the society.

I have seen classic hoarding psychology, where someone who has accumulated a solid chunk of unencumbered liquid wealth, stocks or bonds or gold, overvalued it compared to everything else in the world. For example, suppose a 30 year old worker has accumulated a $40,000 nut. That will be his treasure, even though he could barely live on it for a year and it wouldn’t carry him through a major medical emergency. He is often willing to sacrifice a lot of personal, family, and social quality of life to preserve and increase his nut, and in many cases will also become quite predatory, and political reaction comes with that. And sometimes he invests it successfully and makes it into a higher class, but often enough his investment fails and his life is wasted.

Retail investors often have disproportionate emotional investmenet in their investment (pun intended).

Don’t know whether it was subject to any research, if yes, I’d be curious to see.

There’s behavioural finance research that suggests we overvalue something that we own relative to when we don’t. I think it was all focussed on goods or property, but the rationale would extend to investments too.

Managers of branches of national franchise businesses like McDonald’s dependent on cheap labor too. They are encouraged to identify with the company though unless they move up in the organization I think they get wise. A very close friend of mine was a Starbucks manager for a decade or so, and he was eligible to move up to middle manager but found that the New Age company man zombification required was inhuman and for him impossible.

He cashed out and started his own, better coffee shop, but had to take on too much debt and is not accumulating much net worth. He things of it as a challenging, rewarding, well paid job. (H has testified at the legislature in favor of a $15 minimum wage.)

It does not tell us what happened to the control group. Impossible to determine the effects of the treatment without that, isn’t it?

I don’t recall W’s attempts to privatize Social Security, but I certainly remember Bill Clinton’s. The impeachment scandal prevented him from achieving his goal: Alexander Cockburn wrote a piece entitled ‘How Monica Lewinsky Saved Social Security. ‘

“One possibility is that investment activities itself–with its focus on material gain, risk taking, winning and losing–triggers emotions and modes of reasoning that influence views on issues beyond traditional market activity.”

It seems to me that this suggestion raises a deeper issue. Some have argued that the ultimate success of capitalism (financial, industrial or both) is due to having transformed human nature such that everyone living within it becomes an excellent calculator of gains and loss, pleasure and pain.

Is it possible that such a long process of socialization to capitalist logic makes us all ( in many areas of our lives) capitalist calculating machines?

And if so, how could such a system be dramatically changed?

I suspect the catalyst for change would be a substantial market crash that takes the usual warning:

” Stocks can go down in value as

well as up.”

And adds:

“Stocks can also tank down the

pan!”

At that point, the previously unthinkable can rear it’s (ugly for some) head!

I’m a millionaire! Suddenly I have an opinion about capital gains tax.

https://www.youtube.com/watch?v=EHUtHITYb94

Good article. I like to call this ‘buy in’. Once someone has a stake in stock markets and the finance industry, e.g. most commonly through their pension (which is becoming mandatory in many countries, through forced auto-enrolment), the effect described in this article is triggered.

The antidote to all of this is pretty simple: The ethics of investing.

It’s extremely easy to find and point out ethical problems with investments. Ask someone what pension fund and plan they are invested in, find the pdf listing the individual companies invested in, and then Google them for ethical issues (usually you don’t need to – you’ll already know the bad ones by name).

Then point out the ethical issues to the person, and watch them have a meltdown while they try to fob off concerns about ethics as passé and childish.

The problem is though, this doesn’t provide people with a solution/alternative that is ethical, so the above is not a perfect antidote to ‘buy-in’. People still need to retire at some point, and those who accumulate money well enough to b able to put money away for retirement, still want to know what they should do for a sustainable retirement.

I have no idea what to do, myself. I can’t depend on political/economic-policy change to sort this for me. So at some point I’m probably going to have to have a look at how to invest ethically, even though I feel it is probably impossible.

How are ‘investements in real company stocks’ and ‘assets unrelated to the local economy’ different. I mean stocks are like baseball cards — since most are on the secondary market – If they were part of an IPO then they would be investments in a real company – otherwise they are like trading baseball cards and gambling – pushing stock prices up benefits the owners of those stocks if they can unload them before they become to hot but – indead they are unrelated to the local economy

_So i guess the participants were misled to believe their investments helped the local economy and, were thus moved in their stance by being misled by the fact structure of the study – Can’t blame the misinformation on the study authors as- the financial sector (particularly the financial capital side of the economy) has been conning and training society that what they do is no different than what a productive industrial economy does.

I think the message is desperate disruptive behavior follows nothing left to lose. Give people something to lose with economic justice and the slamming and banging will subside. If you only throw them a bone they’ll use it as a club.