Yves here. Climate change damage is looking so likely that investors are finally having a think about how to price that in. And since bond investors are risk averse and at least some look out a bit on the investment horizon, the bigger impact may be felt there first. Bear in mind that ratings agencies are laggards on downgrades; they tend to validate concerns Mr. Market has already registered.

I’m not all that keen about AI-based approaches (and focusing on sovereign bond ratings without understanding fiat currency issuers), but any stab at this issue is bound to provoke more modeling and study.

And I’m not sure about thinking of bond ratings and 2100. Potable water supplies become scarce by 2050, if not sooner. Drought and resource wars have the potential to redraw a lot of national boundaries even if we steer clear of collapse or near collapse scenarios. The Jackpot, sadly, is coming.

By Patrycja Klusak, Lecturer in Banking and Finance, University of East Anglia; Affiliated Researcher, Bennett Institute for Public Policy, University of Cambridge; Matthew Agarwala, Project Leader, Wealth Economy project, Bennett Institute for Public Policy; Matt Burke, Research Assistant, Bennett Institute for Public Policy; PhD candidate, University of East Anglia; Moritz Kraemer, Chief Economist, CreditRisk.io; Senior Fellow, SOAS Centre for Sustainable Finance; and Kamiar Mohaddes, Macroeconomist, Judge Business School, University of Cambridge. Originally published at VoxEU

Enthusiasm for ‘greening the financial system’ is welcome, but does the explosion of ‘green’ finance indicators reflect the science? This column reports research that uses artificial intelligence to construct the world’s first ‘climate smart’ sovereign credit rating. The results warn of climate-driven downgrades as early as 2030.

Climate change is “the biggest market failure the world has seen” (Stern 2008), with wide-ranging implications for stability – financial, economic, political, social and environmental. As estimates of the economic consequences of climate change continue to grow, financial markets and business leaders face increasing pressure to factor climate risks into decision-making.

Climate change will hit markets from all directions. In boardrooms and at AGMs, what were once token whispers of eco-marketing have become serious discussions of extreme weather events, reputational risks, activist movements (from shareholders and consumers), regulatory and transition risks, asset stranding and environmental litigation. In response, investors and regulators are calling for climate risk disclosures and a clear demonstration that portfolios and business models are consistent with the Paris Climate Agreement. Central bankers,1 finance ministers,2 the IMF3 and UN4 are in on the action (e.g. Brunnermeier and Landau 2020).

All this enthusiasm for ‘greening the financial system’ is welcome, but a fundamental challenge remains: financial decision-makers lack the necessary information (e.g. Edmans 2021). It is not enough to know that climate change is bad. Markets need credible, digestible information on how climate change translates into material risks. Instead, an explosion of environmental, social and governance (ESG) ratings and voluntary, ad hoc, unregulated corporate climate disclosures has created a confusing world of unfamiliar, incomparable, and conflicting metrics.

A chief concern is the lack of scientific foundations in risk disclosures (e.g. Fiedler et al 2021). It is easy to see why. Climate models operate at global scales and project impacts over decades and centuries. Financial models do not. How should a high-frequency trading algorithm (think nanosecond resolution) adjust to the possibility that climate may reduce global output in 2100 by 10%? How should corporate climate disclosure address issues largely beyond their control, such as the carbon intensity of the national electricity grid, or the direction of government flood strategies?

Most disclosures present companies as if they are independent of their physical (geographical) and macroeconomic surroundings. But this ignores crucial context. Climate change does not just affect firms individually, it affects countries and economies systemically. No corporate climate risk assessment is complete without also considering the effect of climate on sovereigns. Without scientific credibility, economic evidence and decision-ready metrics, the field of green finance is open to charges of greenwash.5 Getting it wrong will be costly.

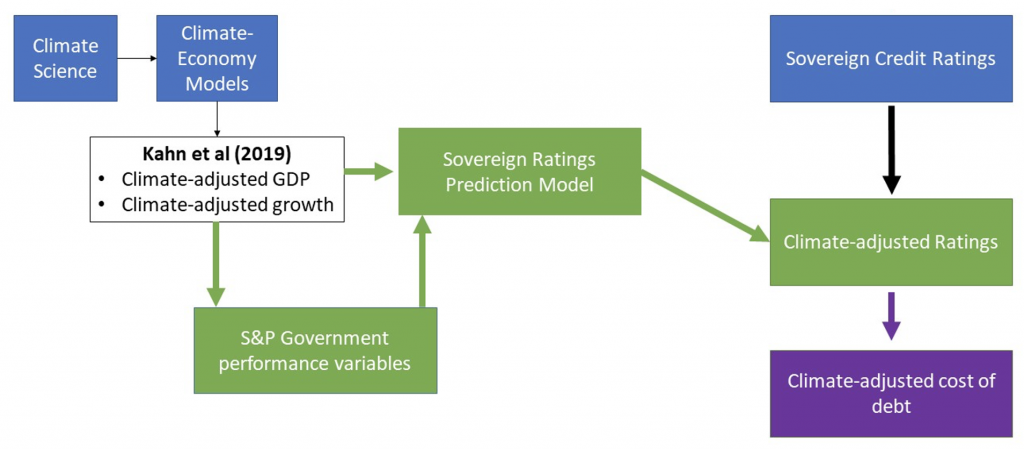

This is what motivated us to bridge the gap between climate science and real-world financial indicators (Klusak et al 2021). Rather than constructing a new metric, we focused on one that is eminently familiar to financial decision-makers: the sovereign credit rating.6 By linking climate science with economic models and real-world best practice in sovereign ratings, we simulate the effect of climate change on sovereign credit ratings for 108 countries under three different warming scenarios (see Figure 1).

We were guided by a single overarching principle: to remain as close as possible to climate science, economics and real-world practice in the field of sovereign credit ratings. To the best of our knowledge, we are the first to simulate the effect of future climate change on sovereign credit ratings. Our approach means we can evaluate the effect of climate on ratings under various climate-economic scenarios and can provide initial estimates of the effects of climate-induced sovereign downgrades on the cost of public and corporate debt around the world.

Figure 1 Bridging the gap between climate science and financial indicators

Notes: Blue boxes (top row) represent the status quo in climate science, climate-economics, and sovereign credit ratings. Economic models translate scientific projections of temperature and precipitation changes into macroeconomic impacts (white box). Green boxes and arrows describe our novel approach to closing the remaining gap between climate economics and ratings.

To this end, we develop a random forest machine learning model to predict sovereign credit ratings and training it on ratings issued by S&P (one of the largest credit ratings agencies) from 2015 to 2020. Next, we combine climate economic models and S&P’s own natural disaster risk assessments to develop a set of climate-adjusted data describing various warming scenarios. We feed these climate-adjusted macroeconomic data into our ratings prediction model to simulate the effect of climate change on sovereign ratings. Finally, we calculate the additional cost of corporate and sovereign capital due to climate-induced sovereign downgrades (Figure 1, purple).

We focus on sovereign ratings because they are decision-ready. This is distinct from ESG ratings, which, even if backed by credible science, still require investors to determine how they relate to material risk. In contrast, sovereign ratings are already used in a range of financial decision-making contexts (for example, under Basel II rules, ratings directly affect the capital requirements of banks and insurance companies). They cover over US$66 trillion in sovereign debt, acting as ‘gatekeepers’ to global financial markets. Sovereign downgrades increase the cost of both public and corporate debt, influencing overall economic performance and significantly affecting fiscal sustainability.

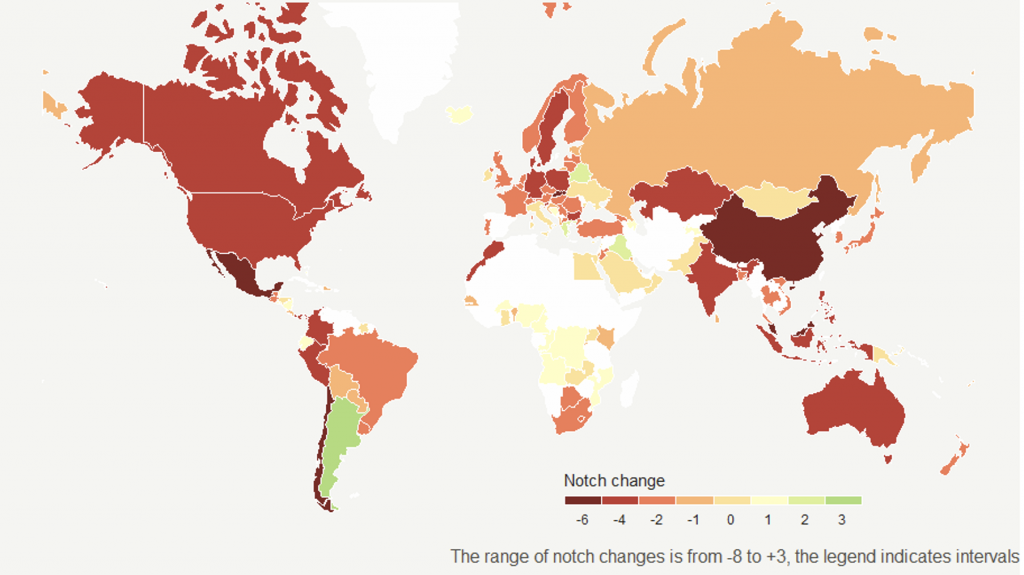

We document three key empirical findings. In contrast to much of the climate-economics literature, we find material impacts of climate change as early as 2030. Under RCP 8.5 (a high emissions scenario that closely traces recent historical emissions), we find that 63 sovereigns suffer climate-induced sovereign downgrades of approximately 1.02 notches by 2030, rising to 80 sovereigns facing an average downgrade of 2.48 notches by 2100 (on a 20-notch scale).

Figure 2 depicts the magnitude and geographical distribution of sovereign ratings changes predicted by our model by 2100 under RCP 8.5, showing that the most affected nations include Chile, China, Slovakia, Malaysia, Mexico, India, Peru and Canada all exceeding 5 notch downgrades. More importantly, our results show that virtually all countries, whether rich or poor, hot or cold, will suffer downgrades if the current trajectory of carbon emissions is maintained.

Figure 2 Global climate-induced sovereign ratings changes (2100, RCP 8.5)

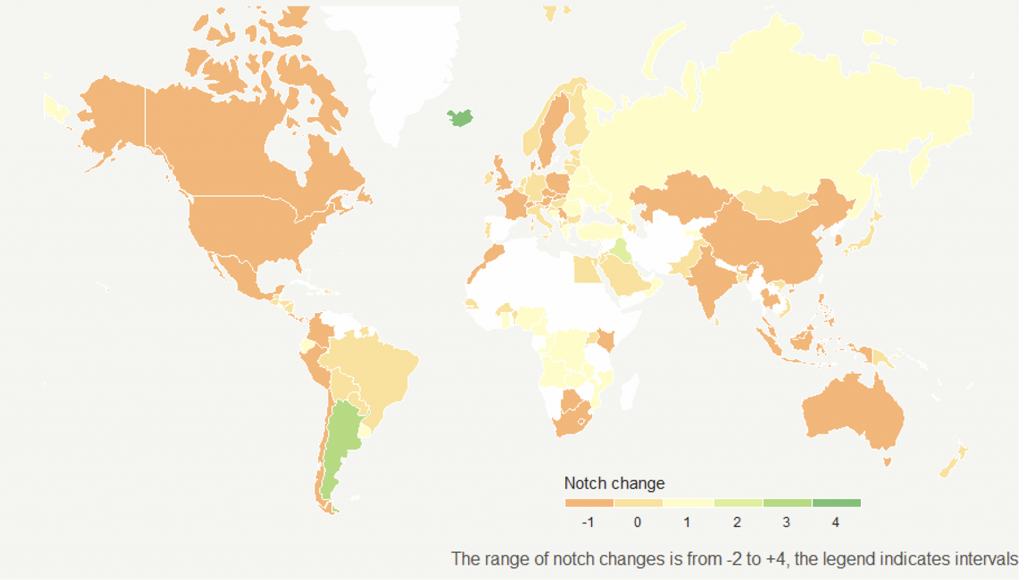

Second, our data strongly suggest that stringent climate policy consistent with the Paris Climate Agreement will result in minimal impacts of climate on ratings – with an average downgrade of just 0.65 notches by 2100. Figure 3 shows that the most affected countries are Chile and China with climate-induced sovereign downgrades of 2.56 and 2.05 notches, respectively.

Third, we calculate the additional costs to sovereign debt – best interpreted as increases in annual interest payments due to climate-induced sovereign downgrades – in our sample to be between $22–33 billion under RCP 2.6 (low emissions), rising to $137–205 billion under RCP 8.5. These translate to additional annual costs of servicing corporate debt ranging from US$7.2–12.6 billion under RCP 2.6, and US$35.8–62.6 billion under RCP 8.5.

Figure 3 Global climate-induced sovereign ratings changes (2100, RCP 2.6)

There are caveats. Due to a lack of scientifically credible quantitative estimates of how climate change will impact social and political factors, these are excluded from our model (Oswald and Stern 2019). Thus, our findings should be considered as conservative.

Moreover, our results should be understood as scenario-based simulations rather than predictions. High emissions scenarios (e.g. RCP8.5) closely track recent observed trajectories and remain useful over near- to midterm timescales (Schwalm et al 2020). But the pace of renewables deployment and climate policy (e.g. regulations banning sales of new petrol and diesel vehicles) offer hope that future trajectories may fall closer to low emissions scenarios such as RCP 2.6 (Hausfather and Peters 2020). We do not comment on the relative probabilities of any given warming scenario playing out in practice.

Despite these caveats, our results are qualitatively similar when changing the time series of ratings used to train the prediction model, restricting the sample to investment grade sovereigns, and varying assumptions about the degree of temperature volatility within the baseline climate-economic model.

The key take-home messages are that it is possible to ‘do climate finance’ without compromising on scientific credibility, economic rigour or decision-readiness. Existing climate science and economics can support credible, decision-ready green finance indicators. This research is of interest to investors, sovereigns and credit ratings agencies alike. Governments issue ever-longer dated bonds, of which life insurance companies and pension funds are eager buyers, thus enabling them to match their own long-term liabilities. Therefore, investors should consider the long-term creditworthiness of sovereign issuers.

Currently there is no reliable yardstick for assessing sovereign creditworthiness beyond the current decade and this research fills this gap. Data on adaptation and resilience will be increasingly important. National statistical offices could play a decisive role, using the recently adopted UN System of Environmental Economic Accounts – Ecosystem Accounts (SEEA-EA)7 as a framework for tracing environmental investments and expenditure.

Our study offers a first methodological approach to extend the long-term rating to an ultra-long-term reality. Based on the methodology applied here, future research could focus on developing ultra-long ratings not only for sovereigns but also for other issuers including corporates.

See original post for references

Regarding water supplies, a new technology approach is needed, mainly, emphasis on science, physics, and common sense to deploy inexpensive point of use filters that are fail safe, reliable, and effective. There seems to be very little effort or attention to this obvious approach.

This is link-whoring, a violation of our written site Policies. Using our comments section to elevate your LinkedIn page in Google searches is absolutely not on. I have ripped out your link and banned you.

Water, energy, and pollution need to be addressed in an integrated manner and seldom are.

Point of use is the most inefficient approach imaginable from a materials standpoint. They are certain to be energy inefficient too.

Is it really though? From where I sit, the science seems to be saying we need to stop the vast majority of our economic activity pretty much immediately if we are to have any hope of turning things around. We need to stop producing, stop burning, stop manufacturing, and stop investing.

As things go even more pear-shaped, one of the last things bankers will need to be worrying about are sovereign credit ratings. Much higher up on the bankers’ worry list will be how not to be eaten.

I thought this argument about sovereign credit ratings assumed a can opener. But who wants to open that can of worms? Firstly, no sovereign needs to borrow anything nor service borrowed debt. For the emergency that climate change is/will be it will have to be paid for by spending directly into the emergency. It will require sovereigns to buy their own bonds and owe only themselves. No selling bonds to “investors” who will then take their billions earned on the most dire misery and invest it in what? Nothing, that’s what. So the whole virtuous circle is nonsense. It’s absurd to argue about “investors’ material risks” when it could actually be the end of civilization. And that dumb chart of sovereign risk anticipation: So am I to assume that Greenland, all of Eurasia, Iceland, the Sahara and the Sahel, Madagascar, Argentina (!), and Iraq aren’t gonna face sea level rise and nasty weather and a collapse of all global trade except on wartime restrictions and etc.? I don’t buy that for a second. It looks like banking and finance is trying to appear analytical so nobody notices they are whistling past the graveyard with very dry lips. And even if and when some bonding happens the investors should be limited to pension funds (ones that are not corrupt… but, are there any?).

Exactly which AGM do you have in mind? Air-to-ground missile? Agrargemeinschaften? Asian Gypsy Moth? Did I get that right? Or did you mean Association Genevoise des Malentendants? If you had another meaning in mind, please choose the appropriate one for me: https://www.acronymfinder.com/AGM.html

If you ask me about the weather, I, as a meteorologist, could swamp you with acronyms that would make you sorry you ever asked. But I’m not that guy.

BTW, it stopped raining and it’s going to be pretty nice out. Or, as we in the trade say, ISRAIGTBPNO.

From the context it is clearly Annual General Meeting.

One can cynically argue that if financiers and rating agencies are beginning to worry about climate change … it demonstrates it is already too late. We use an expression in Spain for those that always arrive late: a buenas horas mangas verdes, that can be translated literally as ‘too late green sleeves’ and makes reference to certain police corps with green sleeves in their uniform in the XIX century that were then famous for arriving always too late to the facts that demanded their presence.

Isn’t the whole concept of The Jackpot that a whole lot of people die, but then the survivors enter a kind of golden age of private sector driven innovation? The Jackpot itself is the boom that comes after a massive civilizational bust, right?

I seriously doubt anything like that scenario is going to happen. I think we’re just going to have a massive bust, and then things are going to stay busted for a long time, until society can start to piece itself back together.

The private sector mostly doesn’t innovate, because innovation is hard and expensive; there’s little private incentive to make risky investments in research if you don’t have some assurance that you’ll be able to make the money back later. The private sector does precious little genuine innovation, and more often than not when you look into things touted as private innovation, you either find that a. the underlying research was at least partially funded by a government, or b. the company is essentially a glorified contractor living off the government teat (this latter is the case with basically all of Elon Musk’s business endeavors. The dude is a contractor; none of his businesses would survive without Uncle Sam giving him fistfuls of cash).

Please don’t mislead readers. We’ve discussed The Jackpot repeatedly. I suggest you read William Gibson’s The Peripheral.

It’s dystopian.

And “The Jackpot” specifically refers to about a 40 year period where everything goes to shit. Starts in about 2027. About 80% of the world’s population and most species die. “The Jackpot” is the acknowledgment that it was awfully lucky that anyone survived.

My mistake, I’ve never actually read the book. Turns out The Jackpot is the collapse itself, and the name is grimly ironic.