Yves here. We’ve written from time to time about the CalPERS long-term care insurance trainwreck. This post by policyholder and financial analyst Lawrence Grossman brings readers up to date. It describes how a proposed settlement of a class-action lawsuit over allegedly verboten increases puts policyholders in the ugly position of having to gamble when CalPERS has a vastly better grasp of the relevant odds than they do.

By way of background, the entire long-term care insurance industry made overly-optimistic assumptions about how (not) long policyholders would live and how many would lapse (just about none), and so insurers have been putting through big premium increases and greatly curtailing new policy-writing. CalPERS is in vastly worse shape than most because it grossly underpriced its plans.

CalPERS then became the target of a class action suit for (among other things) increasing premiums on policies that promised not to. The problem with suing CalPERS, however, is that the only money to be had is the money in the long-term care insurance pot. The long-term care beneficiaries cannot get CalPERS to cough up funds from its pensions to make good on the long-term care obligations. The only other possible source of money was the State of California, and there was no way the legislature was going to rescue CalPERS from the mess it created. As we wrote in 2019:

It doesn’t look like there will be a happy ending for the over 100,000 CalPERS long-term care policy holders who are represented in the class action lawsuit, Wedding v. CalPERS. That doesn’t mean there’s a good outcome for CalPERS either. However, things should work out for the plaintiffs’ attorneys.

The bone of contention is that CalPERS approved an eye-popping 85% increase in premiums in 2013, hitting only the policies with the most generous payment features. The plaintiffs contend that these increases weren’t permissible and are seeking substantial damages.

The case has been grinding through the California courts since 2013. Judge William Highberger, in his decision from a June 10 trial, explicitly called on the legislature and state government to bail out the long-term care scheme.

Needless to say, this is a highly unusual step for a judge to take in a contract dispute. At a minimum, it signals an expectation that CalPERS will lose and lose big.

But CalPERS losing would be of no benefit to the policyholders as a whole (there could be some reallocation among them). It’s highly unlikely that the state will throw money at CalPERS. Unlike CalPERS’ pensions, the state has no obligation. The long-term care insurance plan was set up to be self-funded. So in a worst-case scenario, and “worst-case” looks all too likely, the relevant plans will be insolvent.

If the case results in a significant money judgment against CalPERS, and the judge’s body language is that that’s a probable outcome, the only place the funds can come from is the long-term care plans themselves.

We appreciate Lawrence Grossman continuing his series on CalPERS’ efforts to put this matter to bed, via a complex and therefore difficult-to-analyze settlement. His earlier entries:

CalPERS’ Long-Term Care Fiasco: Private Burial to Hide Malfeasance, Failure to Implement Legislation

One quibble with this post: Grossman praises the attorneys on the long-term care suit. I have a less charitable view. They had to have known their fees would come solely from the already-too-small pot of long-term care policy assets, and thus further reduce participant payouts.

By Lawrence Grossman, CalPERS Long-Term Care policy holder and Certified Financial Planner, Accredited Investment Fiduciary, Registered Investment Adviser, and MBA. This post represents solely his personal views

After eight years of litigation of a class action lawsuit challenging CalPERS Long-Term Care Insurance’s (LTC) 85% rate increase in 2013, this summer CalPERS and the class action lawyers arrived at a Settlement that the Court preliminarily approved. In my last article I said that I suspected that the Settlement is another effort by CalPERS to exploit policyholders. Here I will explain why.

Policyholders in the lawsuit “class” number about 80,000, while roughly another 36,000 current policyholders are not party to the suit. References below to policyholders refer only to those 80,000 who are party to the class action lawsuit.

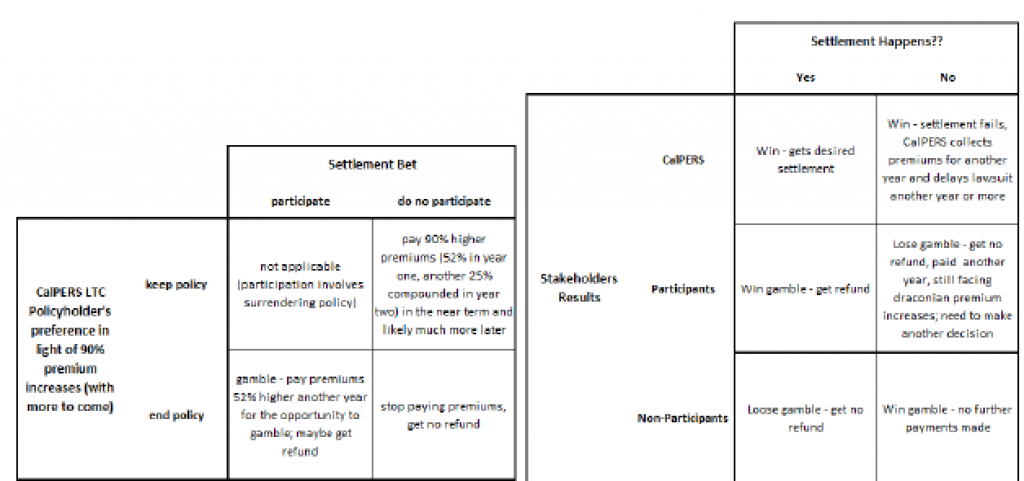

Below are two graphics summarizing the situation that CalPERS policyholders now face.

The graphic “Settlement Bet” shows options that policyholders have to choose from in the Settlement. The graphic “Settlement Happens??” shows the consequences of the “Settlement Bets” if the Settlement happens or not.

Policyholders not wanting to terminate their CalPERS policies will select not to participate (“opt out”) in the Settlement (as participation will end policyholders’ policies if the Settlement is approved).

Policyholders whose preference in light of announced rate increases would be to terminate because of the new CalPERS rate increases can be divided into two groups in light of the Settlement options: (1) those that wish simply to terminate and stop paying premiums; and (2) those who wish to terminate but are prepared to gamble with CalPERS to get a refund.

In making these choices, all policyholders are being forced to gamble a lot of money. Why the Settlement is structured as a gamble is unclear, but it is. That seems incredibly unfair to policyholders who can ill afford more financial losses after their losses already caused by CalPERS LTC.

Policyholders choosing to stay with CalPERS are gambling that they can afford to pay the premiums in the future, which likely will continue to increase dramatically. Policyholders wishing to terminate, because of CalPERS record of raising rates outrageously and most likely contrary to law, are gambling for or against the Settlement going through.

In light of the critical importance of the Settlement going through or not, policyholders ought to have reasonable information to base their decisions (aka bets). But information available from the Court, the plaintiff’s attorneys and CalPERS, does not provide any objective reason to believe that the Settlement will in fact go through. Therefore, the Settlement options forced on policyholders constitute a legally imposed gamble shrouded in ignorance. I believe that policyholders are not properly equipped to make such financially complex gambles and that it is unfair that they are compelled to do so.

What is clear is that the Settlement is a win-win proposition for CalPERS, but not for policyholders.

What is also clear is that the Settlement has the look and feel of a “con job”, an exercise of deception by CalPERS to again better the financial position of CalPERS at the expense of policyholders.

Imagine this possible scenario (and remember, even paranoids have enemies).

• CalPERS is in the final stages of an embarrassing class-action lawsuit and about to go to jury trial. It could lose as the law seems clear, but CalPERS has the capacity to legally fight on for years even if such a jury trial ruled against it.

• The plaintiff’s attorneys, who have done an amazing job over the years and have been fronting all the legal costs (e.g., experts, discovery, attorneys), could by now to be exhausted and tired of not earning anything from this case.

• The two sides come to an agreement. The Settlement value is $2.7 billion. The plaintiff’s attorneys contend that the Settlement is the best possible deal. CalPERS, stonewalling as usual, does not publicly explain why it settled or why it would be good for the 80,000 policyholders.

• But in this scenario, CalPERS is just playing for time in order to delay the trial and to get even more revenues from policyholders that would terminate now if not for the Settlement gamble.

In light of CalPERS past record far short of truthfulness, and any evidence to the contrary, this scenario seems less than paranoid.

Being suspicious of CalPERS’ true intentions seems more reasonable when we dig a bit deeper and when the Settlement documents are reviewed in detail. There are, in fact, two sets of relevant Settlement documents. There is the Court decision granting “Preliminary Approval of Class Settlement” which lays out all the decision details. And there is the “Notice of Proposed Class Action Settlement” that was sent to policyholders, which describes the proposed Settlement and how policyholders may participate or not in the Settlement.

The Notice documents sent to policyholders omit some vital information found in the Court Preliminary Approval. The Notice documents emphasize that policyholders may receive a refund of all premiums paid, which can be tens of thousands of dollars; policyholders also may use the refund to purchase another policy that the attorneys are attempting to arrange. These documents explain that for those policyholders opting to participate in the Settlement “it is VERY IMPORTANT that you CONTINUE PAYING YOUR PREMIUMS to CalPERS until the Settlement is approved (emphasis in original)”.

What is not found in the Notice documents is exactly how likely the Settlement may not be approved.

The Notice only says (see Basic Information, item 8), that the Settlement may not be approved if: (1) “a certain number of Class Members exclude themselves”; (2) if the “Settlement would cause the Long-Term Care Program to become underfunded”; and (3) if the Court [does] not grant Final Approval”.

The Court’s Preliminary Approval of the Settlement includes more detail about why the Settlement may not be approved, saying “CalPERS shall have the option to terminate” if: “(1) more than 10% of the Settlement Class (by policy count) timely and validly request to be excluded from the Settlement, or (2) CalPERS’s performance of the Settlement Agreement, as of the deadline for submitting requests for exclusion, would: (a) result in an LTC Fund Margin of less than 10%; or (b) if the LTC Fund Margin would be less than 10% even absent the performance of the Settlement, if the performance of the Settlement would decrease the LTC Fund Margin.”

Whether over 10% of policyholders will request to be excluded is unknown and unknowable by policyholders. CalPERS, on the other hand, has a vast amount of data to use in judging the likelihood that this termination trigger will be passed.

While the Court’s decision does not indicate what the LTC Fund Margin is, the term can be found in CalPERS annual “Actuarial Valuation” reports for the LTC fund. The Margin, also undefined in the Valuation reports, is calculated as (1) the difference between assets on hand and future net liabilities (future liabilities less future revenues) which (2) is then divided by the value of future premiums.

CalPERS LTC Fund Margin, according to the CalPERS LTC Actuarial Valuation – June 30, 2020, has not been at least 10% in any of the past 5 years. In fact, the 2020 valuation Margin of 1.3% failed the 10% test even though that 2020 Margin calculation reflected the planned 90% premium increases.

The Margin calculation is extremely complicated and reflects a host of assumptions about the future, and therefore seems easy to manipulate. (The Settlement does not address that.) For example, the Margin calculation includes multi-decade long assumptions about investment returns, demographics, mortality, morbidity, policy lapses, claims utilization, expenses and more. Between 2019 and 2020, the Margin moved from negative 85.5% to positive 1.3%. Of that 86.8% Margin shift, only 14.4% reflected real changes in the value of assets on the balance sheet which had increased about 3%; the other 72.4% of Margin change reflected changed assumptions.

The biggest factors improving the 2020 Margin were an increase in the expected return from investments and the planned 90% premium rate increases. The improved expected return is also particularly surprising as most investment professionals marked down expected long-term returns in 2020 in light of the bubble in equities and interest rates at all-time lows.

Without guidance from either the plaintiff’s attorneys or CalPERS, available information makes it seem unlikely that the proposed Settlement would lift the Margin to at least 10%. That conclusion is doubly so in the event that CalPERS did not want to settle, as the manipulable Margin calculation is the perfect tool kill the deal.

In support of the Settlement passing the Margin test, the best argument that can be made is very simply that the Margin did surpass 10% in 2013-2015 when the last 85% rate hike went through. But past performance is not a guarantee of future results and that appears illustrated here; as previously noted, the 2020 Valuation Margin of 1.3% already reflects an immediate 90% rate increase.

CalPERS has not provided policyholders with any reason why they should believe that the Settlement will happen. More stonewalling, more of the same. On the other hand, CalPERS professional staff certainly has carefully examined the odds and consequences of the potential outcomes.

What the facts best fit is a strategy by CalPERS to extract maybe a year more cash out of policyholders, delay the lawsuit, exhaust plaintiff’s lawyers, and deflect attention from the disaster that it has created. The Settlement is a pure gamble with unknown odds that all policyholders have been forced to make, which too many do not understand, which will unfairly injure many, and which will certainly improve CalPERS financial position. Trusting CalPERS again is of course for policyholders the definition of insanity.

I’m sure Yves knows from her contacts there, but when you read things like this you have to wonder just how very deep the rot is within Calpers.

Its one thing to have an incompetent and malign senior management, but when you see this sort of thing you have to assume that multiple layers of people within the organisation see absolutely nothing wrong with behaviour that would make a hedge funder blush.

wonder of they could get money from the board? arent they individually responsible for the actions of CALPERS?

I am one of those who paid faithfully on time,upgraded when available,never got sick and accuse PERS of malfeasance and nisfeasancew. !!!!

From what I can see from that chart, all of the deals offered by CalPERS suck for all those policyholders. But I have another option that CalPERS should offer. How about they offer each policyholder an all expenses trip out to Las Vegas which means a hotel room and restaurants. Once there, CalPERS will offer each of them all the money that they have paid into their policy plus a stake of a coupla thousand dollars at the roulette & blackjack tables – so long as they sign an agreement to quite all present and future legal disputes with CalPERS while the policy is cancelled.

Tell me that a lot of people, when they see all that cash while being in the middle of Las Vegas, would not just say ‘Sure!’ For CalPERS, this will reduce the number of policy holders and a lot of future obligations, especially if some of these people have a big win. For the policyholders, they stand a chance of a big win if they want to try their luck at the tables. Sure its gambling but I am guessing that the odds are better in Las Vegas than with sticking with CalPERS.

I have a friend who had gambling karma, at least with respect to Vegas. She made $23K in one week, slots, roulette, cards. She got comped after that because they assumed she was a high roller as opposed to very lucky on not big wagers. She never lost more than trivial money on later trips and regularly pulled down a few grand. But she wasn’t a CalPERS beneficiary, just a shrink with a nice practice in Studio City.

“… CalPERS professional staff certainly has carefully examined the odds …”

As carefully as they examined the vitae of some recent seniormost hires? There seems to be an implicit assumption here that may warrant more careful examination.

Not sure if anyone can answer this but what about the policy holders who have already filed a claim and are being paid by the LTC plan? What is going to happen to them? (Once you file a LTC claim you stop paying into the plan.) Personal note: my mother is getting paid out of the plan ever since we filed a claim for her 3 years ago but she didn’t opt in for inflation coverage when she originally signed up many years ago.

If you are already on claim now, your benefits continue as if nothing had happened except that you get a refund of some past premiums. The formula is too complicated to summarize here and depends on whether or not you reduced your benefits in response to the rate increase. There’s another group of participants who are not on claim now but will be by the time the settlement is approved. They will have the option of ending their coverage and receiving a refund of premiums paid minus benefits received to date, or staying in the program.

There are other intricacies affecting class members who have let their coverage lapse since the 2013 increase, died since then, or already gone on claim and exhausted their benefits.

Roughly 60,000 of the 80,000 members of the settlement class are current policy holders who are not (yet) on claim. The other 20,000 are spread among eight other categories. The fact that this is so ungodly complicated only compounds the other difficulties of the situation.

This is right up front.

The books at CalPers may be overcooked, but this is as raw a deal as I have seen in my 68 years.

Screwing the elderly and the helpless when you have a duty to protect them.

It’s pretty clear that TPTB have no problem “Letting ‘Er Rip” with Covid and killing off or crippling a large segment of the populace.

There they have “mistakes were made”, here there is no mistake.

I keep thinking about Marek’s disease and a largely unvaccinated African American populace.

There have been lots of “Unintended consequences” from NAFTA, the 1994 crime bill….are more and nastier coming?

A good 20 years ago I was looking into long term care facilities and policies. The best advice I found just surfing around was that it was foolish to buy LTC policies before the age of 65 because either party could face an early demise – so money down the rat hole. LTC insurance can’t survive as a mutual insurance company if everybody is long-term sick and nobody is long-term healthy. But the bet you make is that you’ll be reasonably healthy into your seventies. If the insurance company could get everyone to start contributing in their working years it would be different. It would be more like the SS fund. This effort will take government backing because everybody likes to gamble. And LTC insurance will require a government guarantee. Should have already happened.

Thanks for this article. My uni gives pre-retirement planning seminars every winter/early spring. I’ve attended each one for several years just to keep my information up-to-date for when I retire. There’s always a 2 hour talk and handouts by an excellent eldercare attorney from the nearby big city. 10 years ago he recommended everyone look into LTC insurance. A few years ago, he started noting that the original policies were mispriced because they used an actuarial model not suited to the product but only realized later they should have used a different model, so premiums were going up. The last seminar of his I attended he did not recommend LTC insurance because the premiums were swinging wildly, the insurance companies were trying to sell their LTC business to other insurance companies (who could then raise premiums), and thought it at best a gamble whether the insurance company policy would be worth much (or still exist) when it comes time to use it. He didn’t say “don’t buy”. He said “consider carefully” before buying.

That said, it sounds like CalPERS used the same mispriced modeling as other companies but is making things much worse for policy holders instead of trying to smooth out what they can. Everything is like CalPERS… even CalPERS.

Thanks for your continued reporting on CalPERS, PE, and pensions.

My parents had LTC insurance through a company that was undergoing liquidation while they were using their policies to cover things like in-home and nursing care. Although I never had any notable troubles with them, I seriously doubt that they’re still in business.

Methinks that the liquidation had its roots in a mispriced business model.

So what can policyholders do to organize around these issues and demand from their legislators, the legislative body that oversees the CalPERS board, and the CalPERS board, to restructure and regulate CalPERS long term care?? There is a long list of processes and oversight mechanisms that need to be reversed, restructured revised and regulated. Where to start? Unions? Retirees? Policyholders? Time to organize, people.

Otherwise, the CalPERS board and staff will continue to get away with this blatant breach of fiduciary responsibility not only with Long Term Care but with pensions. I plan to write to the court AGAINST the settlement. Heads I win, tails you lose, indeed. And the CalPERS board and attorneys are laughing all the way to the bank, at the tragic expense of LTC participants.