Yves here. It’s not hard to shed crocodile tears for retailers suffering from an inflation induced profit squeeze. Retail is a cyclical business; that’s why historically many owned their own stores. That would lower their fixed costs and help them ride out bad times.

And even though retailers have thin margins compared to many other industries, it is also true that corporate profit share as a percent of GDP has been at extremely high levels compared to long-standing norms in recent years. So seeing companies have to refrain from passing on all price increases and seeing profit levels take a hit is an overdue development. It’s just too bad to see it not (yet) happening more broadly.

And if you think things are bad on the inflation front, there’s plenty of room for it to get worse. During the 1970s inflation, analysts and investors found it increasingly difficult to interpret and trust corporate financial statements. First, different line items were inflating at different rates, and second, any asset heavy business was not getting an adequate depreciation tax shield, so their financial statements were almost certainly overstating their true condition. Not being sure the financials are presenting an accurate picture creates even more leeriness about owning stocks.

When analysts start caring about the choice of LIFO versus FIFO for inventory accounting, you’ll know the that the underlying economics are in doubt.

By Wolf Richter, editor of Wolf Street. Originally published at Wolf Street

Target reported today that its revenues, at $25.2 billion in Q1, beat by 4% the mega-stimulus-miracle Q1 last year when consumers, awash in government stimulus cash, had gone hog-wild. This was similar to Walmart, which had reported yesterday that its total revenues too beat that stimulus-miracle quarter last year by 2.4%. That’s pretty good when you think about that buy-everything craziness that reigned a year ago in the most ridiculously overstimulated economy ever.

But both retailers reported that their costs surged – product costs, transportation costs, labor costs, and other costs. Target reported that its product costs jumped by 10.4%, and that selling and administration expenses rose by 5.6%; and that therefore operating income plunged by 43%, and that its operating margin (operating income divided by revenues) was only 5.3%, down from 9.9% a year ago, which was a shocker, and it blew out the fuse.

It Wasn’t a Revenue-Shocker, It Was a Cost-Shocker

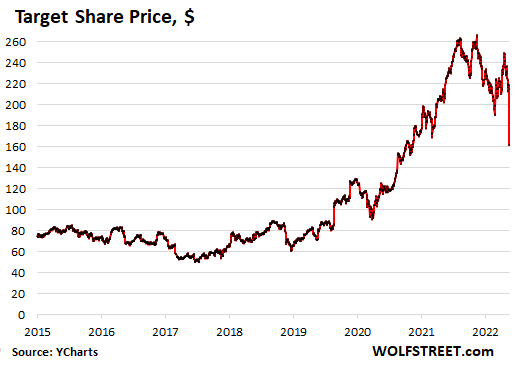

Turns out, inflation is eating up retailers’ profit margins. “Throughout the quarter, we faced unexpectedly high costs, driven by a number of factors, resulting in profitability that came in well below our expectations, and well below where we expect to operate over time,” the earnings release said. Shares kathoomphed 25% during the day and afterhours to $161.61, and were down 38.8% from the peak last August:

Target slashed its projection of its operating margin for the full year, squeezed further by inflation and cost increases and the supply chain chaos. It recognized that it wouldn’t be able to pass on all the cost increases it’s facing, though it would be trying.

But wait… That plunge only took the share price back where it had been in May 2020 as the stimulus checks were hailing down on consumers. It just shows to what ridiculous highs these shares have been whipped and that even for viable big companies, the regression back to normal, wherever that may be, is going to be rough.

Walmart reported yesterday that its gross profit decline due to “elevated supply chain costs and product mix,” with some customers shifting to lower-end products. And it said that operating expenses increased “primarily due to increased wage costs in Walmart U.S.”

Revenues rose 2.4% over the stimulus-miracle Q1 last year, and that was pretty decent considering the craziness a year ago.

Retail is a low-margin business, and small cost increases can wipe out much of the margin. Walmart’s cost of sales rose 3.5% and operating, selling, and administrative expenses rose 4.5%. And therefore, operating income plunged 23%, and net income plunged by 25%.

Walmart’s shares dove 18% since it reported earnings yesterday and 24% since their peak on April 21.

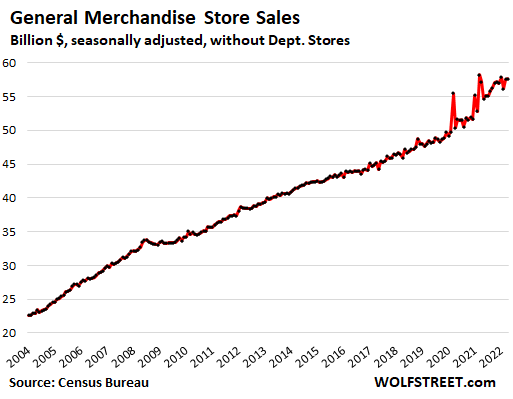

Target and Walmart are part of the retailer category “general merchandise stores,” where retail sales in April – that would the final month in most retailers’ Q1 – were very high, but were up by less than 1% from the historic stimulus-miracle April a year ago (from my report about retailers by category). Note the three giant spikes during the months when the three stimulus checks went out:

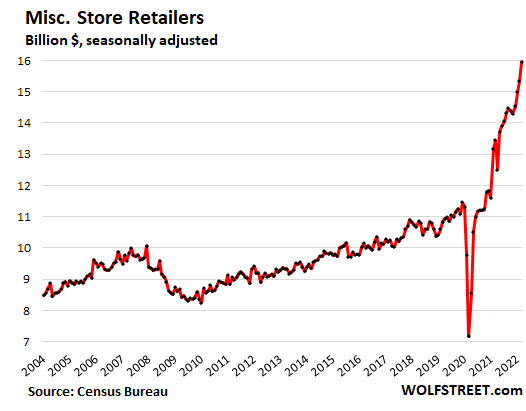

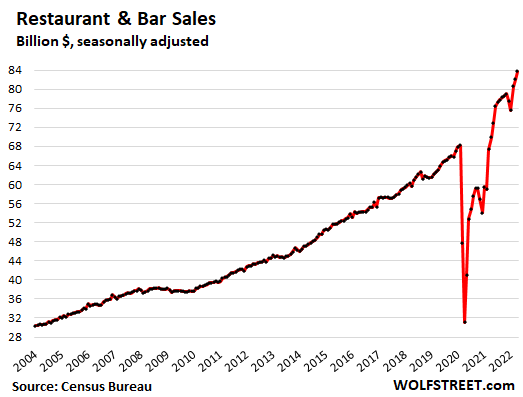

The hot retailer categories. Retail sales were hot in April and the prior months at “eating and drinking places” (+20% year-over-year) and at “miscellaneous stores,” which include cannabis stores where business is booming (+19% year-over-year).

Ecommerce sales were also strong (+13% year-over-year). Ecommerce is a biggie. Ecommerce includes the ecommerce sales of Walmart and Target.

Amazon [AMZN] had waylaid investors with its Q1 report on April 28. Total revenues grew “only” 7%, which would have been great for Target and Walmart, but it was Amazon’s slowest growth rate since the dotcom bust. In addition to a huge loss on its stake in Rivian, it also included all kinds of warnings about soaring expenses in its retail division. The whole thing was a mess. And its stock plunged.

Today, Amazon dropped 8.5% in regular trading and afterhours, to $2,120, unwinding most of the bounce since May 11. The stock is down 43% from the peak in July 2021.

Best Buy shares [BBY] fell nearly 11% today to $75.62, and are down 47% from the peak in November 2021, also on fears of higher costs and supply chain woes.

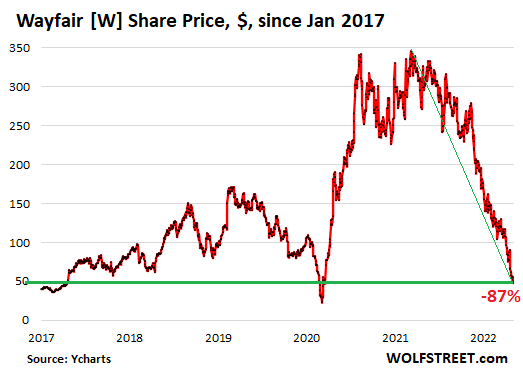

Wayfair [W], the online furniture retailer, had reported a huge loss on May 5, and its revenues actually fell 14% from the stimulus-miracle-Q1, and its shares have gotten shookalacked, including today (-14% during regular trading and afterhours), and are down 87% from their peak in March 2021 and are where they’d been in 2017. Because raging inflation, at some point, is no one’s friend.

TV commentary on the Target announcement put blame on management for not pre-announcing that the quarter would be a miss and the impact to the full year forecast. And on Monday, Wal Mart announcement included some odd nuggets such as the volume increase in sales of half gallons of milk and private label / off brand deli sandwich meats.

The share drop in Target yesterday was pretty jarring.

Big drops in Wal,art, Target, Costco, Amazon, etc. means that the “efficient market” totally misread the impact of inflation on retailers and customers.

sounds right though…I think social media, work-from-home, and the self-sorting of communities along income lines means that your typical Wall Street research analyst is severely detached from the real world.

Regarding Walmart operations in Central America, they’re trying to sell their stores in Nicaragua, El Salvador and Honduras. They’ll be remaining in Guatemala, Panama and Costa Rica. In the news a month ago.

As the sole American producer of my line of widgets, I keep a careful eye on my East Asian competitor’s products (meaning those which are imported and against which my widgets compete), So I watched them raise prices this year and because I have been thrifty over the years and as a consequence, have no mortgages on my production facilities, the CNC machine cells, as well as the warehouse, and despite pay increases for my people, we have remained profitable.

So I took the opportunity to go on the attack. To wit, I lowered prices here and there, which put pressure on my competitors precisely as air and ocean freight was going nuts (it’s largely normalized although bad news always ledes so this isn’t in the news).

Yes, along the way we ate a huge increase in bar stock aluminum, and polymer pellets (used in injection molding), both of which have also retreated significantly (although not to where they were last year but way down from the insane prices). Again, not in the news.

Machine tools didn’t go crazy and electric motors floated higher but sharp negotiating has largely kept them in check (I import these because there are no domestic sources in my market). A real downside has been increased lead times for components which just two years ago we could order with 15-days lead now at 135 days and a few suppliers warning to expect 180 days. Fortunately, we can afford to increase quantities and hold larger stocks of inventories of electronics.

All this happening as competitors are sitting on greater stocks of inventory for which they have paid more and cannot reduce prices in response. Minor point being, we’ve gained market share. Major point being, it’s not bad news everywhere.

Good on you. Most large corporations would raise prices in a situation like this!

You are a extremely prudent business owner with long term sustainability baked into your thinking process. Kudos!!

You may end up being in the first wave of American manufacturing becoming much more profitable or manufacturing being brought back to American shores. From what I can see, there is going to be a hard recession, high interest rates and supply lines which depended on just-in-time delivery and manufacture will be falling over in a heap. The later should help give you a better edge with your East Asian competitors I would guess.

His company might end up being bought.out.

you nailed it. the stock market is way way way over priced. most so-called american companies own nothing but a name and perhaps some distribution infrastructure, maybe.

nafta billy clintons hedge funds are most likely everywhere today trying to find more value to strip, they will turn over every piece of sand they see. so that might not even be a fact.

so what is the stock markets really worth? perhaps values from the early 1990’s.

gorton fish company was selling seafood this last march undercutting vandekamps and others. but if you looked on their packaging, harvested and processed in the u.s.a..

the prices were down right cheap if you look at whats going on, i was kinda stunned.

obviously the others were taking advantage of nafta billy clintons free trade miracle, and offshoring processing to china, the shipping back and forth is as stupid, as any of nafta billy clintons policy disasters.

they are simply pricing themselves out of the market, so that a few parasites can prosper at everyone elses expense.

retail is owned lock stock and barrel by china, and they have to pay the price china demands, and it all goes down the supply chain till it hits the retailers, who are so stupid, they think free trade was a bonanza for them. no stinkin civil society to deal with, only profits are far as the eye can see.

I have a bit of an issue with saying retail is low margin as traditionally it has not been. Wholesaling really can be low margin and I know wholesalers with a markup on purchase prices of less than 5 percent. Markup on retail is normally closer to 35 percent or 15 percent for grocers.

Performance of US Retail is not exactly matched by retail in other countries. This would point to the structure of US Retail having specific issues and the environment being a little different. Ignoring the elevated leverage where debt has been run up and assets sold off there are other US specific factors.

The first being bad covid data where retailers have unexpected costs involved in hiring temporary staff due to worker sickness. Not to mention bonuses paid just for helping a business survive through covid. So I would argue the labor cost rises are not yet about wage inflation, but a cover up for weak management.

There is limited rail freight capacity, warehouse storage and port handling capacity with the result that supply chain lead times are longer. Swapping of transportation methods is occuring and renting of extra warehouse space is going on at high cost. This points to retail management being unable to change forecast and replenishment settings fast and accurately enough for conditions.

One component of administration costs is marketing and retaillers spend a lot of money and time getting advertising, along with shelf placement. When the market changes the temptation of retail advertising and sales is to double down on previous strategies which cost lots of money to little effect now due to disposable income shrinkage impacts.

I could go on, but think it is important to point out some of the issue are transitory and some are strategic issues for the US retail market segment. Shares in retail are likely to be volatile unlike real low margin businesses where this is just like a normal days business and an opportunity. The real bad days for retail are yet to come.

My tiny business uses vacuum tubes and as I predicted all the Russian ones disappeared immediately after the start of the war.

Odd tho, at leas one manufacturer, Sovtek (also showing up under the Groove Tubes and ElectroHarmonix brands) has reappeared.

But at about 2X the old price. I suppose someone is exporting through a cutout somewhere.

Another new brand from China has also showed up. Never ones to miss an opportunity, those guys.

“First, different line items were inflating at different rates, and second, any asset heavy business was not getting an adequate depreciation tax shield, so their financial statements were almost certainly overstating their true condition. Not being sure the financials are presenting an accurate picture creates even more leeriness about owning stocks.”

I have no financial interest in the following link. I do have a 4-year degree in accounting, so I know what New Constructs does is incredibly valuable. It restates the entirety of a company’s financial statements so that they give a truer picture. I’m not into investing like I was years ago, but I was like WOW, that’s amazing when I first came across the site! It’s not an easy task to interpret the footnotes in 1000’s of financial statements on a regular basis. About 10 years ago, their stock screener was free. They charge a fee to access their reports now. Maybe you can get something similar with Capital IQ for $30,000 a year, but I think even they don’t do what New Constructs does!

https://www.newconstructs.com/

i noticed shelves are emptying of paper goods again, ie, kleenex, toilet paper, like early in the pandemic…i got to wondering how the transportation costs impact that supply…ie, starting with harvesting trees in the south or pacific northwest, shipping them to pulp mills, then shipping paper to paper products manufacturers, and from those to retailers….what is the cost per roll to truck toilet paper 500 miles when diesel is $6 a gallon?

No, not the TP outages again !! I noticed in recent months the glaring price increases and changes to the end product by count or volume or what have you. I haven’t observed any recent outages of paper goods in our neck of the world, in the southeastern US.

I will not be buying Bounty paper towels in any near future…off brands and store brands.